Article contents

The best way to spend money abroad is to use a prepaid travel card, where you top-up beforehand, and spend with super low fees. Or, use a direct debit travel card that connects directly to your bank account, and works just the same as your bank card, but with much lower fees.

Jetting off for a well deserved getaway abroad? Don’t let travel money stress you out when you should be relaxing and enjoying yourself.

There’s lots of options out there, which we’ll run through, but if you’re just here for the very best – it’s often a prepaid travel card (although not just any) – these cards can have super low fees, and you simply top them up before you go (or while you’re away), and spend them just as you would with your bank card (we’ll run through them in more details below).

There’s also a direct debit travel card, which links to your bank account directly, so no need to top-up – simply link the card to your bank account using an app you download to your phone, and start spending.

However, having said that, not all travel cards are the same. Here’s the best picks:

Want to spend money abroad? Check out Wise, their card is low cost and works with all the major currencies worldwide.

Wise is one of the best travel cards out there. It's super popular, with over 16 million customers around the world.

It's got some of the lowest fees you'll find, and it's available in over 40 currencies and 150+ countries.

The card is contactless, and there's a great phone app (and website) to manage everything too.

£5 welcome bonus

With Currensea, you can get a travel card that connects directly to your bank account – it acts just the same as your bank card, and transactions come directly out of your bank account.

The only difference is you won't have to pay hefty bank fees, saving anywhere from 85% to 100% of the cost.

It's a great alternative to a prepaid travel card if you want something a bit simpler.

Want to spend money abroad? Check out Wise, their card is low cost and works with all the major currencies worldwide.

There’s 5 main options to spend money abroad, which are:

Let’s run through each in more detail below.

It’s often not a good idea to use your existing credit or debit card, such as a card with a high street bank (debit card), or a regular credit card not designed for travel. Almost all banks charge hefty fees when spending abroad.

There is often a very bad exchange rate (how much your Pounds gets in another currency) when spending your money.

And, often a hidden fee not mentioned by the bank, plus there can also be a foreign transaction fee every time you spend (e.g. £1 per transaction), and if you want to get cash out from an ATM (cash machine), there can be cash withdrawal fees too.

All of these can really add up and cost you a serious amount of money without even knowing it.

You might have also heard of travellers cheques, which are something you can buy beforehand (it’s a paper cheque). When needed, you exchange them for cash.

These are very old school, and it will be hard to find a place to convert them to these days! However you can still use them, but it’s much easier to simply take a card with you, and much safer than carrying cash and cheques.

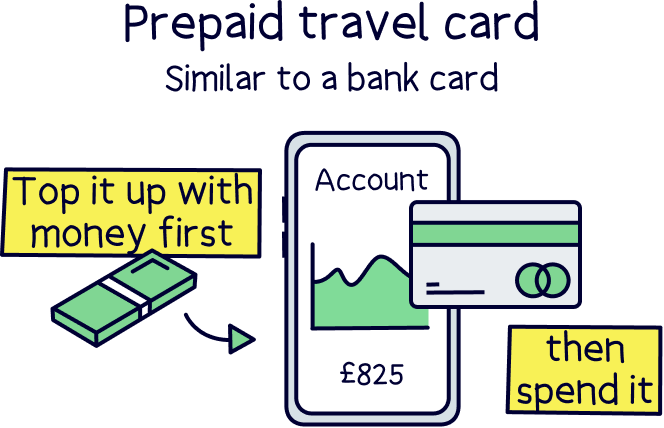

This is often going to be the best option for most people. Prepaid travel cards are easy to set up, there’s no credit checks, and they often have some of the best exchange rates you can get, and no fees to spend abroad.

They work just like a bank card for all your spending in the UK, and you can use them in the UK too if you want.

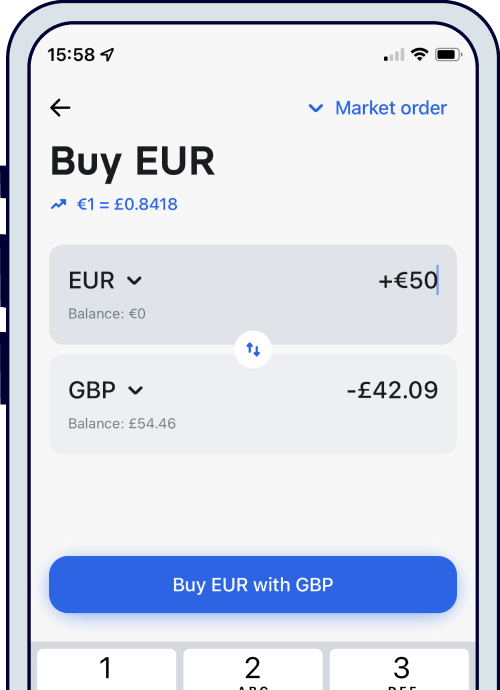

Before you go, all you need to do is transfer some money from your bank account over to your card (they often have great mobile apps and websites to make this easy to do), and then, with a click of a button, you’ll be able to exchange your money into whichever currency you’d like – for instance Euros if you’re going on a holiday to Spain.

And you can even keep the Pounds (GBP) on your card and spend in the foreign currency and every transaction will convert the right amount of Pounds to the local currency (e.g. Euros) when you spend, normally for the same fee.

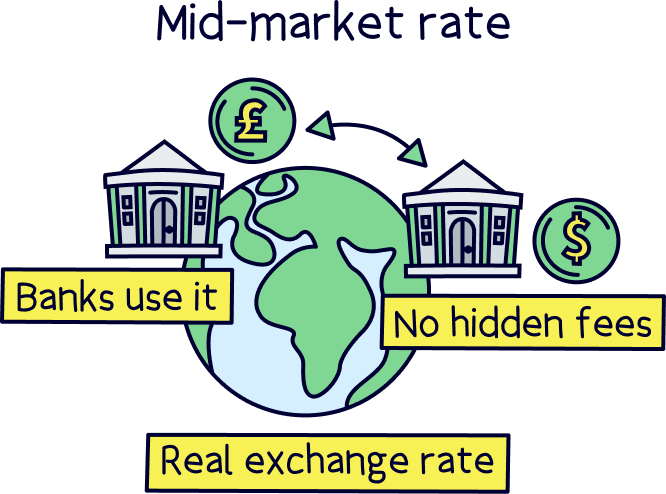

The actual exchange rate you’ll get is often the lowest possible, called the mid-market rate, or interbank rate. This is the rate banks themselves use to exchange money – so you can’t get much cheaper!

Prepaid card providers will then add a fee on top of this when you want to exchange cash. With Wise¹, this can be as low as 0.41%. And that’s all you’ll pay, except for a delivery fee for the card (around £7).

The only downside is you can’t use them for ‘pre-authorised’ transactions – that’s where you put your card number down for something that you’ll pay later, such as car hire.

Here’s where to learn more about the best prepaid travel cards.

Note: not all the prepaid travel cards are the same. Some can be expensive.

This is another great option. You can get all the protection and security of your current bank account, and not have the hassle of opening a new bank or credit card account for cheaper exchange rates when abroad.

Think of these as a middleman in front of your bank account when you spend abroad. The card will do the currency exchange instead of the bank, every time you spend, and all for a low exchange rate (normally the interbank rate).

So, imagine you spend Euros in France, your bank will think you’re spending Pounds, but you’ll actually be spending in Euros via your travel card, so you avoid all of the bank fees completely (which can be around 3-5%). Sounds pretty great right?

The best direct debit travel card is Currensea¹ (just 0.50% fee to exchange money).

Using a travel credit card abroad can be another way of spending money, often thought of as cheaper, but it’s not always (or even most of the time).

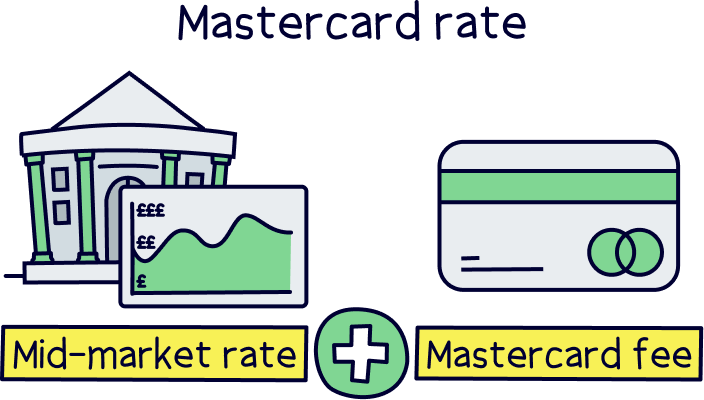

They’ll often use a pretty low rate to convert currency, such as the Mastercard or Visa rate, although some credit card companies can add extra fees on top of this.

There can also be a fee to withdraw money from an ATM (e.g. £3 per transaction). However, a big warning here, it’s not a good idea to withdraw cash from a credit card, even if it's a travel money card.

This can appear on your credit file, and looks bad to lenders (companies you might borrow money from in future), as it can appear like you have no cash from elsewhere and need to use the credit card for cash.

If you do withdraw cash, you’re normally charged interest on it too, until you repay it, and this can be around 30% per year, charged daily.

There can also be transaction fees when you do spend money in a foreign currency, for instance £2 per transaction. Some cards don't have these, and some do – please check, as they can really add up.

You’ll also need to apply for the credit card, which involves a credit check, and you’ll be given a credit limit too (how much you are allowed to spend).

The great thing about using a credit card is that you’ll have better protection than a debit card, as credit cards have ‘section 75 protection’...

This means you can often request a refund from the card provider to get your money back if there is a genuine reason, such as you didn’t get the product or service paid for. This is also called a ‘chargeback’. Prepaid travel cards and debit cards have the same ability, but not officially section 75 protection.

And finally, if you do want to use a credit card, make sure you pay it back in full, on or before the repayment date, otherwise you could face hefty fees!

This is where you open a completely new bank account in order to benefit from their low fees when spending money abroad. They’ll give you a debit card which works abroad, and will convert your money as you spend it.

These can have low exchange rates, and typically they’ll use the low Mastercard rate (as the card is often a Mastercard), and add a fee on top for each transaction.

You’ll also be able to withdraw cash from an ATM, normally without a fee, up to a certain limit (e.g. up to £300 per month).

And in order to actually use them, you’ll need to send cash over from your bank account, to your new bank account.

They’re a great option, but not typically cheaper than the better prepaid travel cards (Wise¹), or a direct debit travel card (Currensea¹). And, you’ll have to open a whole new bank account in order to benefit from them, which can include credit checks.

They can be worth it if you are looking for a new bank account and typically travel a lot.

Note: don’t use your normal debit card abroad, or for overseas spending. It’s likely to have poor exchange rates, and lots of extra fees. Only use one designed for travel.

It is a good idea to take money abroad, and pretty essential too – for those small purchases, or tips, or to pay street vendors who don’t accept card.

However, you’ll typically get a bad exchange rate when converting cash anywhere, especially when you’re at the airport or already abroad. Not to mention ATM withdrawal fees, from both your card provider (if you use your main bank account) and the overseas ATM provider.

It’s also much safer to spend money on a card than keep lots of cash lying around in your hotel room, and you’ll get protection when you use it and want to refund charges later.

It can often be better to withdraw cash from an ATM with one of the above card types, rather than converting cash with a bureau de change – you’ll benefit from the same exchange rate as spending on the card (normally), and with the best card providers, there won’t be any withdrawal fees (until you reach a limit).

There we have it for the best way to take money abroad. We recommend using a prepaid travel card, or a direct debit travel card.

With both types of card, you’ll benefit from a very low exchange rate, which is typically the interbank rate (the low rate banks themselves use), and a small fee added on top.

You’ll also be able to open an account easily, with no credit checks, and there will be a great phone app and website to use to manage everything.

Credit or debit cards, that are designed for travel, can also be a good idea, but typically there’s not much in it fees wise when comparing to a prepaid card, and in fact, likely to be more expensive. You’ll also need to make a full application, which can be time consuming and involve credit checks. Unless you’re travelling a lot, it’s probably not worth it.

And that’s the travel money sorted, all that’s left to do is enjoy the trip abroad!

Want to spend money abroad? Check out Wise, their card is low cost and works with all the major currencies worldwide.

Want to spend money abroad? Check out Wise, their card is low cost and works with all the major currencies worldwide.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things banking, cards, and spending and receiving money, for both individuals and businesses – with many years of combined experience writing about it. Some of our team were top financial advisors. We know how to save a small fortune in fees, and how to find the right card and account for you.

More than 20 years of combined experience researching and writing about banking

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of financial companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Want to spend money abroad? Check out Wise, their card is low cost and works with all the major currencies worldwide.