Article contents

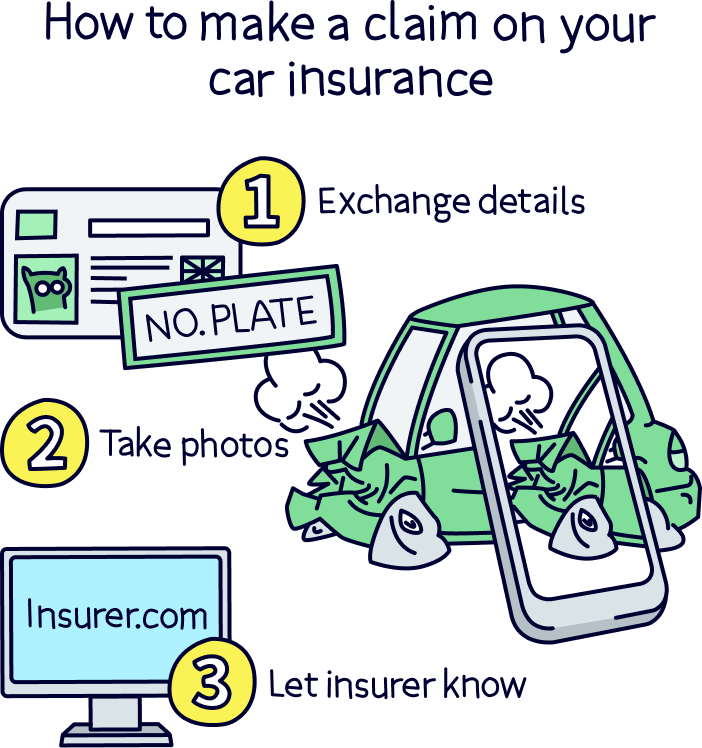

Swap details with anyone else involved, and then simply give your insurer a call, ideally within 24 hours. If it’s a serious incident, involve the police and get a crime reference number too.

If you ever find yourself needing to make a claim on your car insurance, it’s important to know what’s involved in the process. We’re going to run through exactly what happens when you make a claim, and how you can avoid any issues or delays occurring along the way.

When you’re raising a claim on your insurance, you’re formally requesting that your insurer pays for something covered by your policy. In this case, you’re asking that your insurer pays out compensation for an incident involving your vehicle – this could be an accident involving another car, theft, or vandalism.

There are four main types of car insurance claim. Depending on the nature of the incident, the time it takes to resolve your claim can vary.

This is when you, or somebody else, is injured during the incident. If the injured individual requires medical treatment or an assessment then this needs to be factored into the claims process, and can delay things a fair bit.

This refers to any damage done to the vehicle itself. The extent of the repair work (and if your insurer has a preferred mechanic) can impact how long it will take for your claim to be resolved.

If your car cannot be repaired, or if the cost of repairs is deemed too high by your insurer, then this is known as a ‘write off’. You’ll need to agree on a settlement figure with your insurer, and so timings will depend on how long this process takes. Always be sure to research the value of your car (or a similar model) to ensure that you’re getting fair compensation from your insurer.

If your car is stolen, your insurer will carry out an investigation once you’ve reported the theft to the police. The time it takes for your claim to be settled will depend on how long this investigation takes.

If you ever need to make a claim on your car insurance, here’s what you need to do:

Once you get in touch with your insurer, you’ll usually need to provide them with some basic info on the incident - this includes:

If you’re claiming because of fire damage or vandalism, the process is exactly the same. You should also get in touch with the police immediately, and they’ll provide a crime reference number that you’ll need to share with your insurer.

You should also get in touch with the police if the following occurs during an accident:

If you’re involved in an accident with someone without insurance, you’ll be able to claim from your own insurer if you have comprehensive cover. However, this will mean losing your no-claims discount, and you may still need to pay your normal excess.

Most insurers have their own rules here, but in general, you should aim to report any incidents or accidents within 24 hours. If you miss the deadline for reporting an incident, your claim could be invalid, so make sure to contact your insurer ASAP.

It’s hard to say exactly how long a car insurance claim will take to settle. There are many different factors involved (the type of incident, any potential injuries, the actions of the other driver, etc) and so there’s no guaranteed timeline for you receiving compensation.

However, some situations are more likely to delay your settlement, such as:

There are a couple of factors that will impact the cost of your insurance after making a claim. Firstly, it depends on whether the incident has been deemed an ‘at fault’ or ‘no fault’ claim.

‘At fault’ means that the incident or accident was judged to be entirely your fault. However, this doesn’t always mean that you’re directly responsible. If someone damages your vehicle and isn’t able to be located, then the claim may still be classed as ‘at fault’, as the insurer won’t be able to recover the full cost of repairs. This may not seem entirely fair, but it’s important to know.

‘No fault’ means the responsibility lies entirely with the other party involved in the incident, and usually means that the insurer is able to recover the full costs of repair.

You might be thinking that ‘no fault’ means you won’t see an increase in your insurance costs. Unfortunately, this isn’t the case - with any type of claim, you’ll be viewed as higher risk by the insurer, which will be reflected in your premium.

However, the increase in costs may not be as dramatic as you expect. In 2018, a major insurance comparison study showed that at-fault drivers could expect to see their premium increase by £136 on average. Non-fault drivers, on the other hand, saw an average increase of £102.

If you’re paying your insurance in monthly instalments, then this may not be as shocking as you’d expect. However, cost increases can vary significantly, depending on the severity of the incident and your driving history. And is especially annoying for new drivers, who are already paying a lot!

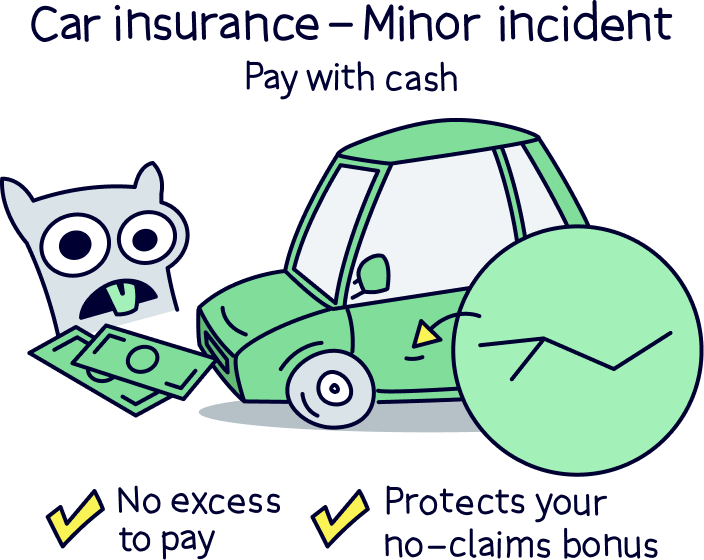

You don’t always need to make a claim if you’re involved in an accident - and sometimes this can be the right decision! For example, if you’re involved in a minor accident, you might want to cover small repair costs yourself, rather than paying out your excess fee or disrupting your no-claims bonus.

However, even if you decide not to claim, you should always let your insurer know that you were involved in an accident.

If any issues arise with your insurer during the claims process, search for their complaints procedures online and follow the steps. This should be your first port of call, and hopefully you’ll be able to resolve the complaint with them directly.

However, if you’re still struggling to find a resolution with your insurer and you feel like you’ve hit a brick wall, you can always contact the Financial Ombudsman.

This is a neutral financial service, and they aim to settle disputes fairly between businesses and consumers. However, it can take up to 5 months for the Financial Ombudsman to process and begin working on your case – so it’s definitely not a quick fix.

If you’re ever involved in an accident and need to make a claim, be sure to bear all of the above in mind. Stay in contact with your insurer, and contact them as quickly as possible – along with the police, if necessary.

Try to also ensure that you collect enough information about the incident itself – things like the location, time of day, driver details, and photographs too. And that’s all there is to it.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible