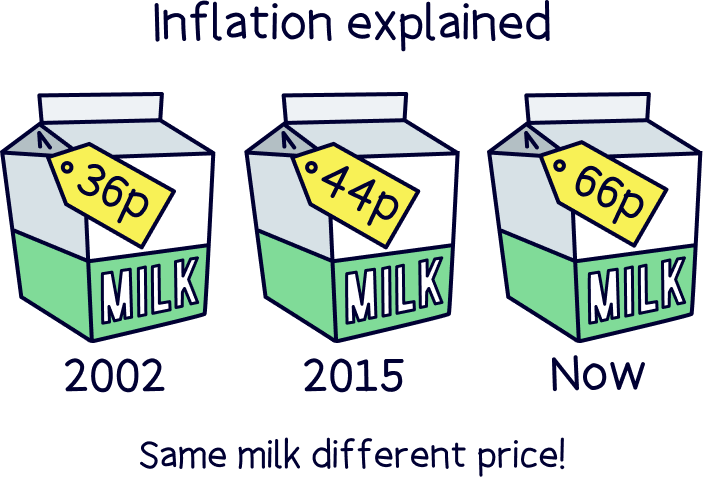

It’s bad news again for the UK, inflation has risen to 3.6% for the 12 months to June, up from 3.4% for the 12 months to May.

Inflation is the price of essentials and everyday things increasing over time (such as food and clothes). Meaning your everyday bills are continuing to rise.

The rise this time was fuelled by increasing petrol and diesel prices and food, as determined by the ONS.

The Bank of England expects inflation to rise to 3.7% before September, before dropping back to its target of 2% (but no target given for when).

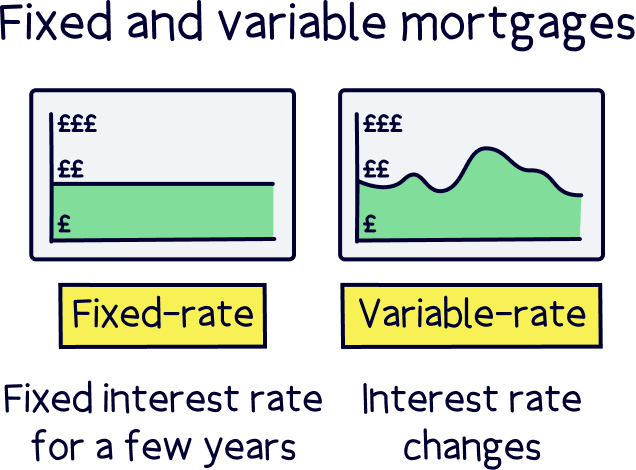

They use the Bank of England base rate as a tool to combat inflation, and it’s the rate they give the banks in exchange for interest, and can affect how much the banks then give to you. So, it affects things such as mortgages and savings.

The Bank of England base rate is currently 4.25%, and with rising inflation, it likely means this rate won’t be cut for some time.

If you have a mortgage that’s coming up for renewal soon (the fixed interest rate on your mortgage is ending, if you have one), make sure you are getting the best rate out there. Use our mortgage comparison tool to check and apply for a new mortgage easily with the help of a mortgage broker.

If you have savings, make sure you are getting the best savings rate, the difference between savings providers is huge these days, and you could be missing out on a small fortune. Here’s our best savings accounts to check.

And if you do have savings, consider investing some of your money rather than keeping it in cash savings, your money could grow much larger over time (on average over the years), and is a great way to combat high inflation reducing the value of your savings. If you’re not sure where to get started investing, check out Beach¹, it’s easy to use, with investments managed by experts. Or check out all of our best investment platforms.

Note: your capital is at risk when investing.