Mortgages are getting more headlines than Love Island this year, and with the market in constant flux, we’re teaming up with our mortgage partner Tembo to get the inside scoop.

Each month, one of their experts will provide commentary on the latest news from lenders, the Bank of England and more.

Without further ado, let’s cover off July’s headlines.

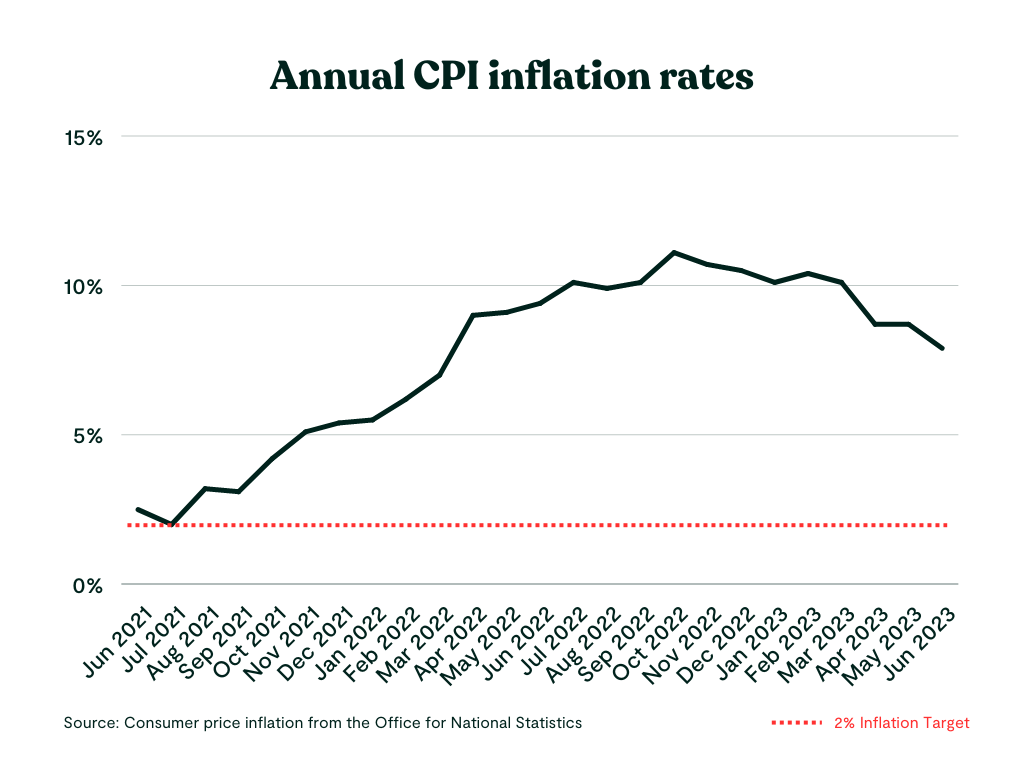

At 7am on Wednesday 19th July, the latest inflation data landed. Much to Rishi Sunak’s relief, it was good news.

Inflation has fallen faster than expected to 7.9% in the year up to June, down from 8.7% in May. Better yet, core inflation (excluding volatile and seasonal prices) was down too.

Up to this point, inflation has been pretty stubborn, keeping everyday expenses and the cost of borrowing high. Although at first this was caused by rising food and fuel prices (heavily influenced by Russia’s invasion of Ukraine disrupting supply), this then shifted to being stoked by the rising costs of goods and services.

Recent inflation figures show that falling prices for motor fuel led to the largest downward contribution to monthly change in inflation, falling by 22.7% in the year to June 2023, compared with 13.1% in May.

And while food prices rose in June 2023 by an annual rate of 17.4%, this increase was less than in May, and from the recent 19.2% high back in March - the highest annual rate for over 45 years.

Both of these factors have led to inflation being less than it was in May 2023.

Raising the base rate is the Bank of England’s main tool in tackling high inflation.

In increasing the cost of borrowing, the Bank aims to reduce public spending, so that the cost of goods and services comes down, thereby reducing inflation.

And while inflation has been sticky, well… The Bank of England has raised its base rate 13 consecutive times to try and reduce it. The base rate currently stands at 5% - the highest level since 2008.

The current inflation rate is way above the government’s 2% target, so the latest news isn’t cause for celebration. But it is a positive sign that inflation is slowly getting under control, and therefore that mortgage rates might be reaching their peak.

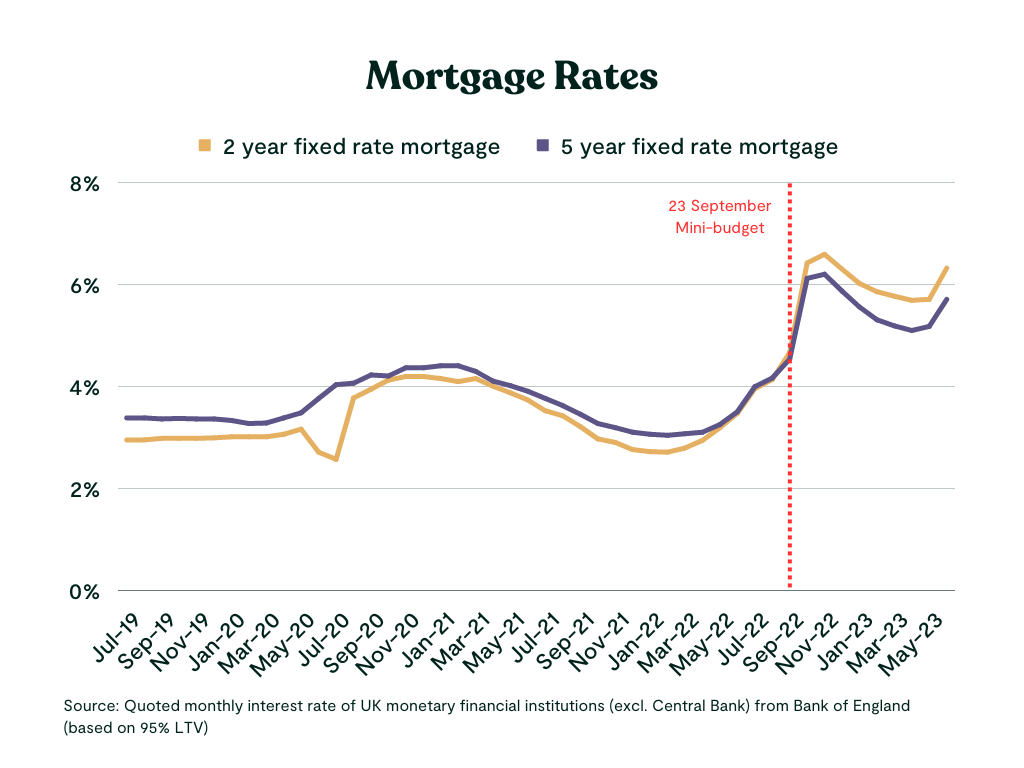

Swap rates - a leading indicator for mortgage rates - fell just after the announcement - and fixed-rate mortgages reduced initially too, from 6.81% on Wednesday to 6.79% on Thursday, but as of today (25th July) they are back up to 6.83%. We’d expect to see the ‘butterfly’ effect of the inflation news to continue to soften mortgage rates over the next fortnight, but we also need to be realistic about the new normal.

We’re living in a higher inflation environment, and it’s highly unlikely we’ll see a return to the sub-2% deals and ‘cheap money’ we saw during the pandemic. Interest rates of between 4-5% are much more likely to be our new normal.

While this may sound like a less than perfect time to buy, right now there is a window of opportunity for both first time buyers and homesellers looking to move.

Why? Well, it’s not just interest rates that are tumbling. House prices are falling at their fastest rate in 12-years, and buyer enquiries fell 45% last month.

This combination - faltering property price growth & reduced buyer demand - provides first time buyers with an opportunity to bag themselves a steal on selling price. Tembo, the award-winning digital mortgage broker¹, has seen some of their chain-free buyers negotiating discounts of 10% or more with relative ease, as sellers are forced to be more realistic about market conditions.

This benefits homesellers, too. When house prices rise, upsizing to a larger property becomes more difficult because the gap between your current place and the next 'rung' of the ladder grows.

With prices now falling, this trend reverses. Prices of homes further up the ladder will likely see the biggest drops, as they were the most inflated from the Covid property boom. This means buying now could mean upsizers see a small hit on their home's sale price, but could get a bigger proportionate discount on their onward purchase.

The fall in demand will also put lenders under pressure to meet their lending targets, which could encourage them to price more competitively. It’s likely the market will continue to be volatile for some time, particularly if lenders do end up in price wars. But, Tembo expects to see these initial positive changes continue to impact mortgage rates over the next fortnight.

This will not only help buyers looking to start a new mortgage deal, but also homeowners who are worried about remortgaging onto a new rate. For those looking to move to a new mortgage deal, Tembo’s experts advise against locking in for long periods right now:

“For those more comfortable with risk, consider taking out a variable or tracker deal while you wait to see if things improve. There are also other options to consider if you're struggling to make your repayments affordable, such as switching to a part and part or interest only mortgage for a short time. The Tembo team can help advise you on the best option for you.”

Perry Graves, mortgage broker at Tembo

For now, the spotlight is on the Bank of England. On the 3rd August, they will meet to decide what, if any, changes will be made to the base rate. Analysts had predicted it would increase by 0.5 percentage points to 5.5%, but after Wednesday's announcement, those same analysts now predict it will rise by 0.25%.

Author: Perry Graves, an expert mortgage advisor at Tembo¹.

If you’re looking for a mortgage, or would like some advice, get in touch with Tembo¹ – they’re got award winning service, and you’ll even get 50% off their fees with Nuts About Money (and you’ll only pay when you get your mortgage, just having a chat is completely free).