The government has just launched a new online service to make voluntary National Insurance contributions (payments), which could help boost your State Pension (the government pension).

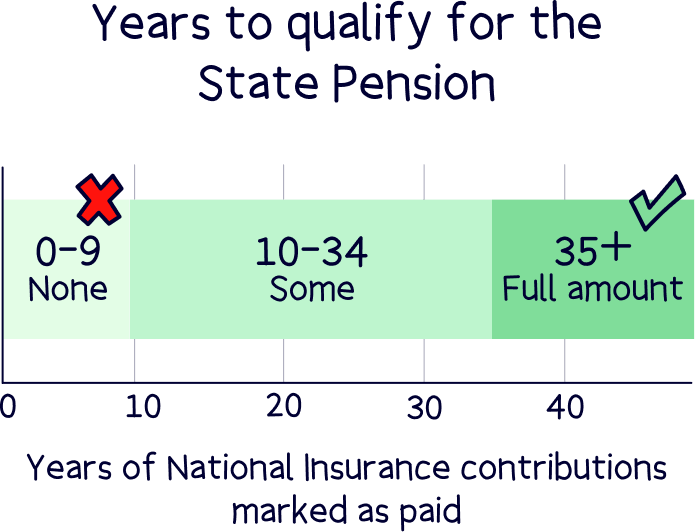

You’ll need to have made at least 10 years worth of National Insurance contributions over your lifetime to get some State Pension, and 35 years to get the full amount – so making up any gaps could make a huge difference to your retirement income.

The welcome upgrade to the ‘State Pension forecast’ tool by the government, means you can now make payments online to fill any gaps in your National Insurance history.

With the online tool, you can see if you have any gaps in your National Insurance record, see if this would affect your State Pension, and by how much, and then make voluntary contributions to make up any shortfall – meaning you can get back on track to receive the full amount of the State Pension when you retire (reach State Pension age, currently 66).

Until 5th April 2025, you can make voluntary contributions to fill any gaps all the way back to 2006. After 5th April 2025, you’ll be able to make voluntary contributions for the previous 6 tax years.

Here’s where to access the State Pension forecast tool, and it’s also available on the HMRC app.

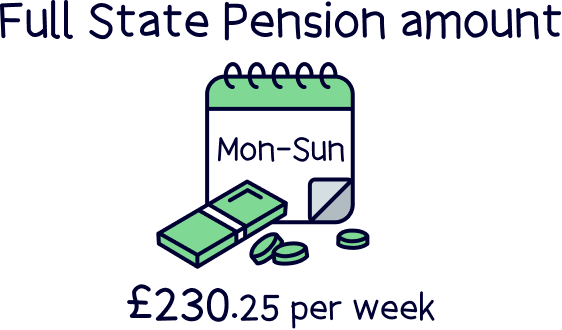

The full State Pension is currently £230.25 per week (£11,973 per year), so unlikely to provide a comfortable retirement by itself. If you’re worried about having enough for retirement, here’s our guide to how much you’ll need in your pension pot, and the best private pension providers to help you save more (such as getting a massive 25% bonus when you save).