Our top travel money cards for holiday spending.

The lowest fees, easy to use, and easy to set up.

£5 welcome bonus

T&C's apply.

With Currensea, you can get a travel card that connects directly to your bank account – it acts just the same as your bank card, and transactions come directly out of your bank account.

The only difference, is you won't have to pay hefty bank fees, saving anywhere from 85% to 100% of the cost.

It's a great alternative to a prepaid travel card if you want something a bit simpler.

• Save between 85% and 100% on bank fees

• Links directly to your existing bank account (works with all major banks)

• Spend abroad like a local with a debit card (and free card delivery)

• 0% exchange rate fee on paid plans

• 0.50% exchange rate fee on the free plan (very low)

• Uses the best exchange rate (interbank rate)

• Cash withdrawals free up to £500

• Works with all 180 currencies

• Great customer service

• Safe and secure

• Need to get a paid plan to get 0% exchange rate fees (£25 per year)

• Not much else!

50% off annual fee (save £30)

T&C's apply.

Hilton Honors is the rewards scheme from Hilton Hotels. You can build up points by using their debit card, and get things like discounts on hotels and resorts (and even free stays).

You can even get VIP access to concerts and sports events, and use them for shopping and car rental. You get points every time you spend with a Hilton Honors card.

Fee: £60 per year (£30 with 50% off for the first year)

Welcome bonus: get 2,500 points when you spend within 3 months of signing up.

With the Hilton Honors debit card, you’ll be able to earn up to 3 Hilton Honors points for every £1 you spend (that’s eligible for points).

You’ll get the Hilton Honors silver status, giving you extra perks and things like free nights when you book with points.

The exchange rate on the card is the best possible (the real exchange rate with no hidden fees), with a low 0.50% fee when you spend. And there’s a low 0.50% fee when withdrawing under £250 from an ATM (per month). Above this it’s 2.5%.

Fee: £150 per year

With the premium Hilton Honors Plus debit card, you’ll earn up to 4.5 Hilton Honors points for every £1 you spend (that’s eligible for points).

You’ll get the Hilton Honors gold status, giving you things like free room upgrades.

The exchange rate is the best possible (the real exchange rate), with no fees added. There’s also fee free cash withdrawals up to £500 per month (2.5% fee above this).

The Hilton Honors debit card is pretty great, it’s in collaboration with Currensea, meaning you can benefit from their great travel card technology, where you connect your card directly with your bank account, so no need for any prepaid cards or transferring money to other accounts – when you spend, it’s simply taken from your existing bank account.

The Hilton Honors points you get are great, and why not benefit from free stuff when you’re spending abroad anyway? You can build up points to use for future holidays, free extras like room upgrades, and even day trips – the list goes on, and well worth checking out.

• Best exchange rate possible

• Low fees

• Spend directly from your bank account

• Earn Hilton Honors points for free stays and extras

• Easy to set up and use

• Not free (annual fee)

• Suited to more frequent travellers

Wise is one of the best travel cards out there. It's super popular, with over 16 million customers around the world.

It's got some of the lowest fees you'll find, and it's available in over 40 currencies and 150+ countries.

The card is contactless, and there's a great phone app (and website) to manage everything too.

• Very low cost money transfers

• Easy to use

• Over 40 currencies available

• Fast payments

• Debit card for spending (such as on holidays)

• Great for foreign nationals and expats

• Awesome business account for international payments

• Earn interest and invest cash (including businesses)

• Very safe and secure

• Only £200 fee-free cash withdrawals (fees after this)

• Not much else!

Super easy, and low fees. Spend away and it comes directly out of your existing bank account.

£5 welcome bonus

T&C's apply.

With Currensea, you can get a travel card that connects directly to your bank account – it acts just the same as your bank card, and transactions come directly out of your bank account.

The only difference, is you won't have to pay hefty bank fees, saving anywhere from 85% to 100% of the cost.

It's a great alternative to a prepaid travel card if you want something a bit simpler.

• Save between 85% and 100% on bank fees

• Links directly to your existing bank account (works with all major banks)

• Spend abroad like a local with a debit card (and free card delivery)

• 0% exchange rate fee on paid plans

• 0.50% exchange rate fee on the free plan (very low)

• Uses the best exchange rate (interbank rate)

• Cash withdrawals free up to £500

• Works with all 180 currencies

• Great customer service

• Safe and secure

• Need to get a paid plan to get 0% exchange rate fees (£25 per year)

• Not much else!

50% off annual fee (save £30)

T&C's apply.

Hilton Honors is the rewards scheme from Hilton Hotels. You can build up points by using their debit card, and get things like discounts on hotels and resorts (and even free stays).

You can even get VIP access to concerts and sports events, and use them for shopping and car rental. You get points every time you spend with a Hilton Honors card.

Fee: £60 per year (£30 with 50% off for the first year)

Welcome bonus: get 2,500 points when you spend within 3 months of signing up.

With the Hilton Honors debit card, you’ll be able to earn up to 3 Hilton Honors points for every £1 you spend (that’s eligible for points).

You’ll get the Hilton Honors silver status, giving you extra perks and things like free nights when you book with points.

The exchange rate on the card is the best possible (the real exchange rate with no hidden fees), with a low 0.50% fee when you spend. And there’s a low 0.50% fee when withdrawing under £250 from an ATM (per month). Above this it’s 2.5%.

Fee: £150 per year

With the premium Hilton Honors Plus debit card, you’ll earn up to 4.5 Hilton Honors points for every £1 you spend (that’s eligible for points).

You’ll get the Hilton Honors gold status, giving you things like free room upgrades.

The exchange rate is the best possible (the real exchange rate), with no fees added. There’s also fee free cash withdrawals up to £500 per month (2.5% fee above this).

The Hilton Honors debit card is pretty great, it’s in collaboration with Currensea, meaning you can benefit from their great travel card technology, where you connect your card directly with your bank account, so no need for any prepaid cards or transferring money to other accounts – when you spend, it’s simply taken from your existing bank account.

The Hilton Honors points you get are great, and why not benefit from free stuff when you’re spending abroad anyway? You can build up points to use for future holidays, free extras like room upgrades, and even day trips – the list goes on, and well worth checking out.

• Best exchange rate possible

• Low fees

• Spend directly from your bank account

• Earn Hilton Honors points for free stays and extras

• Easy to set up and use

• Not free (annual fee)

• Suited to more frequent travellers

Top up your card first, and then spend away. Low fees.

Wise is one of the best travel cards out there. It's super popular, with over 16 million customers around the world.

It's got some of the lowest fees you'll find, and it's available in over 40 currencies and 150+ countries.

The card is contactless, and there's a great phone app (and website) to manage everything too.

• Very low cost money transfers

• Easy to use

• Over 40 currencies available

• Fast payments

• Debit card for spending (such as on holidays)

• Great for foreign nationals and expats

• Awesome business account for international payments

• Earn interest and invest cash (including businesses)

• Very safe and secure

• Only £200 fee-free cash withdrawals (fees after this)

• Not much else!

Revolut is a popular money app (it does a lot of things to do with money), and you can also exchange currencies and spend abroad. The app has a lot of great features, but there’s some hidden fees to be aware of…

Exchanging money at the weekend will cost 1%, and there’s a limit of £1,000 per month for how much you can exchange for free (e.g. converting or spending during the week), after that it’s 1% for the rest of the month (on the free plan).

They also use their own exchange rate – it’s good but not the best rate (which is called the interbank rate).

For cash withdrawals, there’s a £200 limit (or 5 cash withdrawals) per month, then it’s a massive 2% (minimum £1).

You can reduce these fees, and increase the monthly exchange limit, but you’ll have to sign up to a paid plan, so often not worth it for just a travel card.

• Free to open (and there’s paid plans)

• Free exchange on weekdays (up to £1,000 per month)

• Revolut’s has its own interest rate (good but not the best)

• Expensive to exchange money on weekends (1%)

• Low free cash withdrawal limit (£200)

• Must use their mobile app to use card

Full bank accounts with great exchange rates and card to spend abroad.

Chase is a free bank account, and allows you to spend abroad with no fees.

• Free to open (no monthly fee)

• No fees on spending abroad

• Uses the Mastercard exchange rate

• Withdraw up to £500 per day abroad (max £1,500 per month)

• Must use their mobile app to use card

Starling is a great mobile bank, and free to use.

• Free account option (or paid plans)

• No fees on spending abroad

• Uses the Mastercard exchange rate

• Withdraw up to £300 per day abroad

• Must use their mobile app to use card

• Not great customer service

Monzo is a free mobile bank and becoming very popular in the UK.

• Free account option (or paid plans)

• No fees on spending abroad

• Uses the Mastercard exchange rate

• Good split bills feature

• 3% fee on cash withdrawals abroad (free in Europe it it’s your main bank account)

• Must use their mobile app to use card

Revolut is a popular money app (it does a lot of things to do with money), and you can also exchange currencies and spend abroad. The app has a lot of great features, but there’s some hidden fees to be aware of…

Exchanging money at the weekend will cost 1%, and there’s a limit of £1,000 per month for how much you can exchange for free (e.g. converting or spending during the week), after that it’s 1% for the rest of the month (on the free plan).

They also use their own exchange rate – it’s good but not the best rate (which is called the interbank rate).

For cash withdrawals, there’s a £200 limit (or 5 cash withdrawals) per month, then it’s a massive 2% (minimum £1).

You can reduce these fees, and increase the monthly exchange limit, but you’ll have to sign up to a paid plan, so often not worth it for just a travel card.

• Free to open (and there’s paid plans)

• Free exchange on weekdays (up to £1,000 per month)

• Revolut’s has its own interest rate (good but not the best)

• Expensive to exchange money on weekends (1%)

• Low free cash withdrawal limit (£200)

• Must use their mobile app to use card

Borrow money for your holiday, with low exchange rates.

The Barclaycard Rewards Card is the best option for travelling if you’re after an actual credit card (need to borrow the money).

There’s no annual fees, and no fees to spend money abroad, or to withdraw cash, and it uses the Visa exchange rate (which is low, although not quite the ‘real’ exchange rate).

You’ll also get 0.25% cashback on your spending.

• No annual fees

• No fees to spend money abroad

• No fees to withdraw cash

• Get 0.25% cashback

• Interest rate: usually 25.9%, but can go up to 31.9%

• Late payment fee

Interest rate: usually 25.9%, but can go up to 31.9% – make sure you repay in full every month to avoid these high fees. There’s also fees for late payments (you have been warned).

Credit limit: usually borrow up to £1,200.

There’s a wide range of travel money options available to you, but travel cards are often the best way to spend abroad – long gone are the days of getting a wedge of cash out and stashing it in your wallet, suitcase or even socks!

And with that said, there’s a wide range of travel money cards too – from prepaid cards, to debit cards (bank cards) and even credit cards (borrowing money). Either can be a great option for you, and we’ve listed our range of top options above.

However, to get that range of options, here’s the criteria we used to research and review them:

And there’s also a lot of different travel money card providers (companies) out there, but we’ve narrowed it down to just the very best, ones we use ourselves, and recommend to our friends and family, and our lovely readers of course – so whichever one you choose from our list, you can be confident it’s one of the very best options out there.

Interested in learning more? Here’s our full review methodology and how we test.

Often just called a travel money card, these are a fairly new concept for travel cards (well, the last few years), and you could say it’s the modern way for travel money – essentially, your new card links to your existing bank account, and when you spend money, it simply deducts it from your bank account.

It works via what's called a Direct Debit, which is an agreement between you and a company to take money out of your bank account, you’ll probably be familiar with this as it works for things like your phone bill or energy bill.

This means there’s no need to create a brand new bank account, or apply for a credit card, or anything like that. You spend money on your new travel card and the money comes out of your bank account. Simple.

By the way, it also means you don’t have to face any hefty charges your bank charges you (often hidden fees), even though you’re still using your bank account, you simply pay the travel card fee instead – which is usually considerably cheaper – and overall, it’s one of the cheapest ways to spend money abroad.

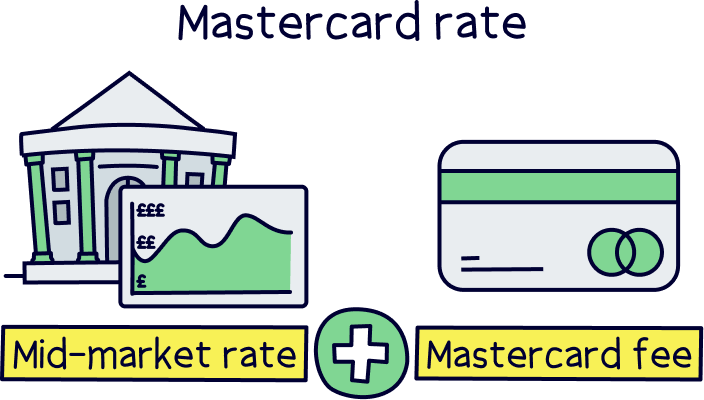

The exchange rate is typically also one of the best possible, either the interbank rate (the best rate banks give each other), or the Mastercard rate (effectively the best rate, but provided by Mastercard, the card issuer).

You’ll also get a great mobile app to use and manage your spending and payments, and you’ll still be able to do all the normal things such as withdraw money abroad (often for free).

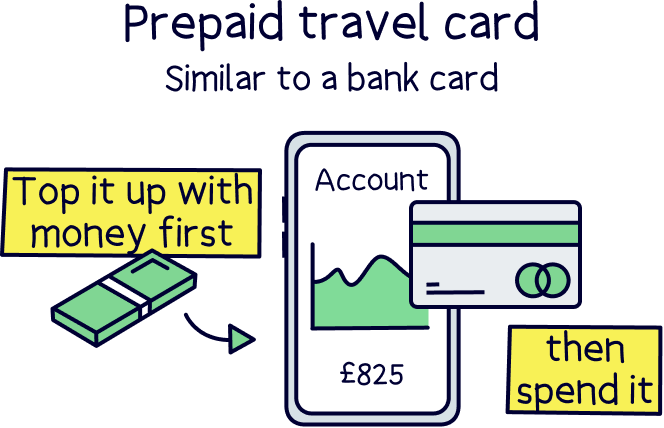

A prepaid travel card is where you transfer money to the card first, often called pre-loading it, and then you are able to spend on it abroad.

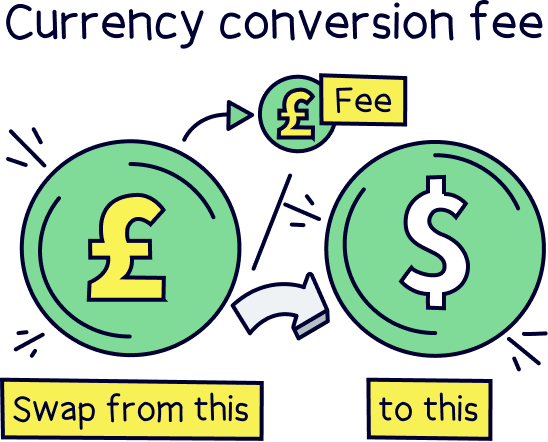

They often come with much cheaper fees than using your high street bank account – you’ll typically pay a currency conversion fee when you add money to the card, for instance if you want to convert all your cash to another currency like Euros – or you can keep it as Pounds and then convert it when you want to spend it.

With the modern prepaid cards (see our list above), you’ll be able to manage your money on the account with a great mobile app (or website) – and can add or withdraw money when you like.

You’ll also be able to withdraw money abroad from ATMs too.

Nuts About Money tip: learn more about the best prepaid travel money cards.

A debit card is the card you get with your regular bank account (your current account), and you’re able to spend away as you like and the cash comes out of your bank account.

A travel debit card is where you open a bank account with a bank that allows you to spend abroad and has relatively low fees to do so – so you spend using your card abroad (ideally in the local currency) and the bank will convert what you spend back in Pounds and take it from your account.

This bit is important. Most high street banks, so the big name banks are super expensive – don’t use them! Instead, use a modern bank, often a mobile bank, who has low currency conversion fees and uses an exchange rate with no hidden fees in either (such as the Mastercard rate, which is pretty much the best rate possible, and provided by the card provider, Mastercard).

These modern banks also come with great banking apps to manage your travel money (and if you want to, you can use it as your main bank account). These banks aren’t necessarily designed just to be travel money cards, but some people use them for just that – but unfortunately, you still need to open a full bank account to use them, and in reality, they act the same as a prepaid card, where you’ll need to send cash to them from your existing bank account.

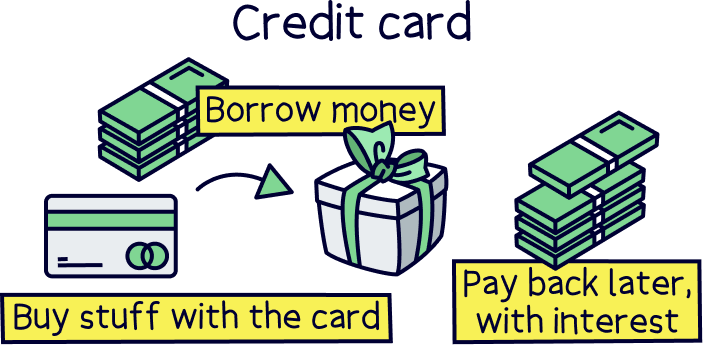

A travel credit card is where you spend abroad with borrowed money (from the credit card company) and then you repay the money afterwards, either all in one go, or monthly.

Note: make sure you apply for a credit card specifically for travel, not just any credit card, or the fees will be extortionate – you have been warned!

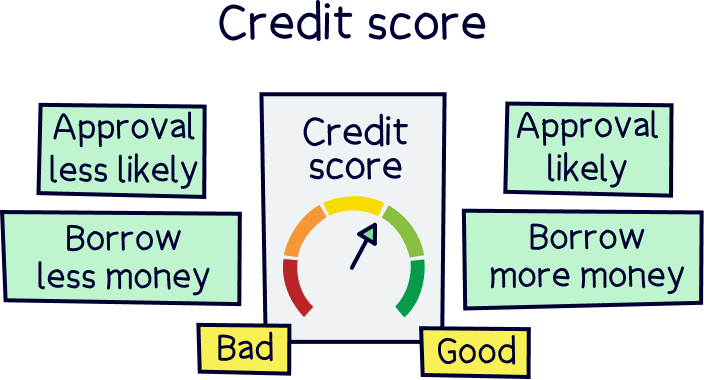

These are a good option if you need to borrow a bit of extra cash for your holiday, rather than having it already, as you’ll spend on your card as you like, and then repay later on – if you repay in full at the earliest opportunity, you likely won’t have any interest or fees added, but if you miss repaying in full straight away, you’ll likely face some hefty fees, which can negatively impact your credit score.

You’ll also need to undergo a full credit check (one that shows on your credit history) when you apply for one, so you will need good credit history, and there will be a limit applied to the card, which is a limit on how much you can spend (a credit limit).

A benefit can be that you get ‘section 75’ protection with credit cards, which means you are able to request a refund from the card provider if something happens, such as you paid for a service but didn’t receive it (although there’s no guarantee your credit card provider will refund it).

Although, this is often seen as an outdated benefit now, as the card providers with other options (e.g. Mastercard) offer an equivalent benefit called chargeback protection, which acts in pretty much the same way.

If you’re looking to buy and hold multiple currencies within one account, and then spend them as you like on your card, then the best option is to use a prepaid card option (like Wise¹).

With these you can simply convert your cash within the app to the currency you want, and keep it there until you need it.

Or, if you have another currency somewhere else, you can send this directly across, to be kept securely within your account.

With a typical bank, even a modern one, you can’t hold multiple currencies – you would typically have a bank account for one currency, such as Pounds in the UK.

Yep. You can use most travel money cards with Apple Pay and Google Pay. You just need to add them to your wallet on your phone. It's pretty simple to do (but we won't go into it here).

With any travel money card you can withdraw cash abroad from an ATM (cash machine), however, there are some important things to be aware of – there will either be a free withdrawal limit, or no limit, for how much you can withdraw, normally a set amount per month (e.g. £500 per month).

After that limit, you might have some hefty fees, so it’s definitely worth checking out.

Also, the ATM abroad will probably charge fees (e.g. £2 per withdrawal), but it’s pretty much impossible to avoid these fees abroad. But it is often cheaper to withdraw money from an ATM abroad with a travel money card than it is to exchange cash before you go (for instance at the airport).

Yes, using a travel money card is perfectly safe, and a great option – much safer than using cash, and stashing it in your hotel room.

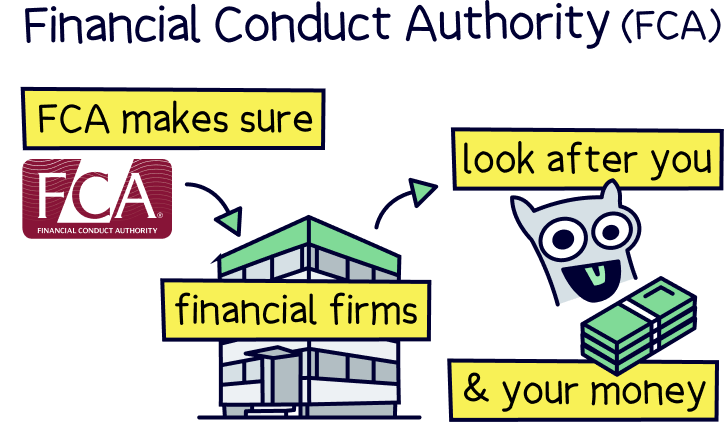

Travel money cards need to be authorised by the Financial Conduct Authority (FCA) in the UK, in order to provide their services to you – and they make sure your money is well looked after.

If you preload any money to a card, your money will be stored in separate bank accounts from your travel money card provider’s money, and it’s all in your name, and can only be returned to you, should the provider go out of business.

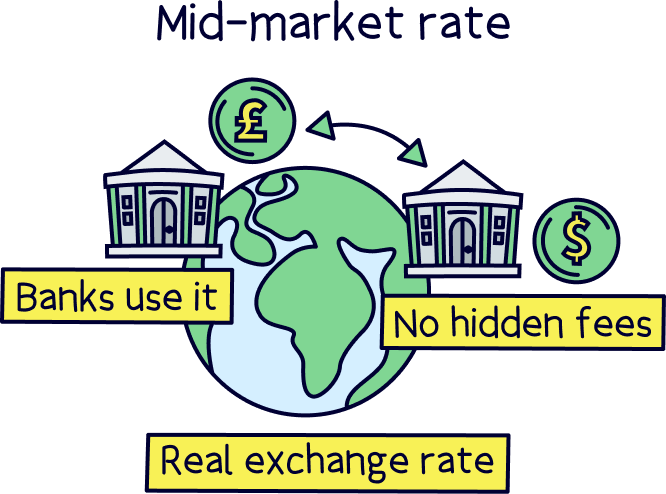

The interbank rate (also called the mid-market rate), is the best exchange rate you can get, and is the exchange rate the banks give each other when they lend to each other – so there’s no fees hidden within the rate itself.

There’s often hidden fees when banks and other financial companies exchange your money, for instance they have a worse exchange rate, and then pocket the difference between that and the interbank rate.

With all of our options, we’ve looked for this top rate. Often with the top cards, it’s provided by the card issuer, which is often Mastercard – they have their own rate, but it’s very similar to the interbank rate.

Travel money cards who use the interbank rate often add a small fee on top in order to still make money, but it’s not hidden in the exchange rate, so it's much more transparent. It could also be a monthly or annual fee instead too.

There we have it for the best travel money cards, you have a wide range of options:

They all serve the same purpose, to spend money abroad, and they all act in the same way – simply use the card to spend in the local currency, and you’ll benefit from the low fees. But, each option is suited to a different type of person, and what they’re looking for…

For instance if you travel regularly you might want to switch your bank account to a bank account that’s great for travel and use their travel debit card. Or, if you’d like to borrow a bit of cash, you might want to use a travel credit card.

However overall, the easiest option is to get a debit debit travel card or prepaid travel card, and you can simply use them for your holidays, without needing to open a brand new bank account, and then forget about the card until your next holiday – all the great ones we've listed above are cheap, with low fees and typically you are only charged when you spend money.

That it’s – now all that’s left to do is enjoy your holiday!

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things banking, cards, and spending and receiving money, for both individuals and businesses – with many years of combined experience writing about it. Some of our team were top financial advisors. We know how to save a small fortune in fees, and how to find the right card and account for you.

More than 20 years of combined experience researching and writing about banking

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of financial companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Pay less bank fees when spending in foreign currencies, while still using your same bank account.