Article contents

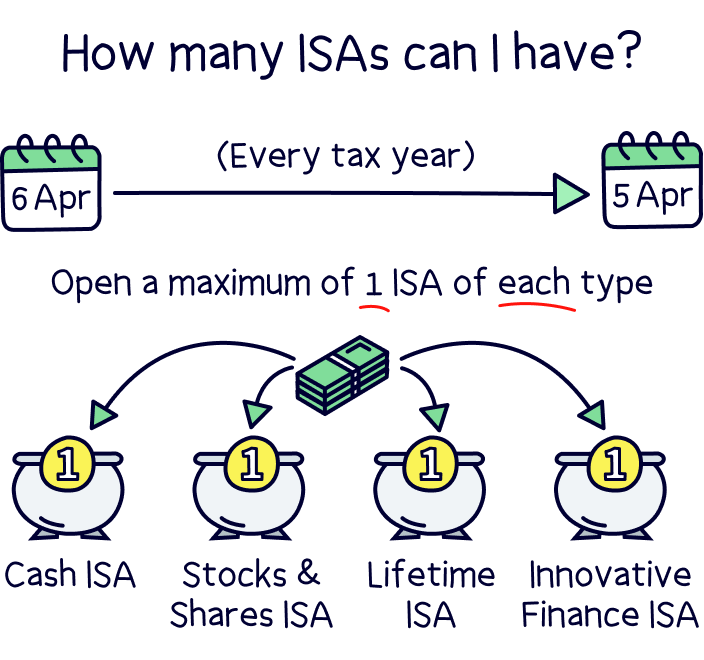

You can have more than one ISA – in fact you can have loads of ISAs – but you can only put money into one ISA of each type per tax year – Cash ISA, Stocks & Shares ISA, Innovative Finance ISA and Lifetime ISA.

An ISA is an Individual Savings Account. It allows you to save and grow your money, tax free.

That’s right. No tax at all!

The UK tax year runs from the 6th of April to the 5th of April the following calendar year. During that time, you’re allowed to drop a total of £20,000 into ISAs (your ISA allowance). You can split that amount into the various types of ISAs.

There are four main types of ISAs:

There are also Junior ISAs, but being young and free, they dance to their own tune. We dive deeper into those in our guide to Junior ISAs.

You can’t open and pay money into more than one of the same types of ISA in a tax year. But you can open a new one of each type every year if you want to – and stack them up over time (but you don’t need to open a new one every year).

The only thing you can’t do, is pay into two ISAs of the same type in the same tax year.

Let’s dive into having multiple ISAs a bit more…

You put cash in. It earns you interest. The interest you earn is tax-free. There are two main types of Cash ISA:

Variable-rate Cash ISAs, where your interest rate can change over time. Normally in-line with the Bank of England base rate, which is the interest rate banks themselves borrow money for, but also get paid the same amount for storing money with the Bank of England.

So if this increases, they sometimes pass this onto customers, and the customer gets a higher interest rate too. And if the Bank of England lowers the base rate, the customer's interest rate will often go down too.

Fixed-rate Cash ISAs, where your interest rate stays the same over a set amount of years. These often have the highest interest rates as you are agreeing to keep your money with a bank for a long period of time, normally 1-5 years.

Interest rates are super low at the moment, the best you’ll find is 1.75% (for a 5 year fixed rate), so a Cash ISA probably isn’t the best idea for long term savings.

Learn more with our guide to Cash ISAs.

Also called ‘Investment ISAs’, these allow you to invest your money in:

You might have heard that Stocks and Shares ISAs are risky and complicated. But this is actually not true! They’re great for long-term investing, and everyone, whatever your knowledge or experience, can open one easily and start growing their savings.

With most Stocks & Shares ISA, the investments are managed by experts (unless you want to manage it yourself), who know what they’re doing with your hard earned money. They’ll typically invest in stocks and shares that keep your money safe and grow over time – so often, big successful businesses.

As a rule of thumb, you could expect to earn around 8% per year on average. Which is pretty good!

It's a much better option than saving your money in a low interest-paying Cash ISA, where the highest rate you’ll find is around 1.75%.

Let’s say you manage to put away £10,000 in a Cash ISA with an interest rate of 1.75%. That’s £175 interest per year.

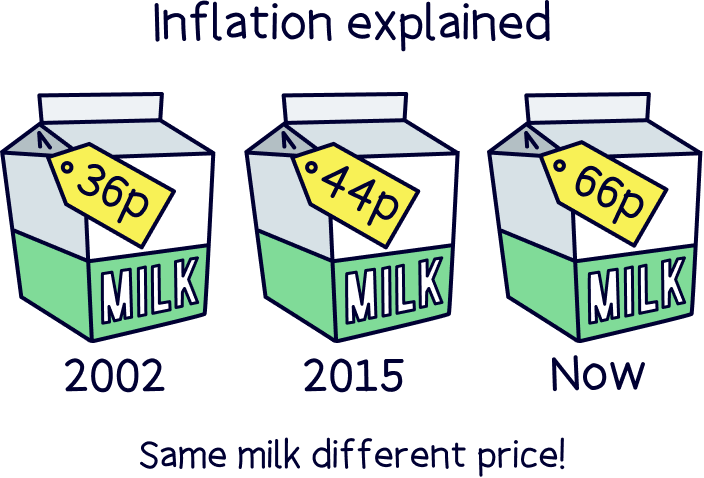

That’s not bad. But the problem is inflation – the general cost of everyday goods and services rising, such as food and petrol.

At the moment inflation is around 5% per year and rising further (2022). That means what you can buy with your cash is getting lower by 5% per year, or put simply, you can buy 5% less things this time next year.

Here’s an example, in the year 2002, a pint of milk cost 36p, now it costs 66p, nearly double! That’s inflation at work.

If you save your money in a Stocks and Shares ISA, you’ll grow your money on average by around 8% per year over time. So your payback from the £10,000 would be £800 per year. That’s higher than inflation, so your money will actually be able to buy more stuff this time next year! You’re winning!

Learn more with our guide to Stocks & Shares ISAs. You can even invest with an ethical ISA too.

Innovative Finance ISAs allow you to lend out your savings to individuals or companies through what is called a “peer-to-peer lending platform” (for example, Funding Circle). This cuts out the middle-man – i.e. the bank. Borrowers then have to pay the money back over time – with interest. And most of that interest is for you.

Learn more about Stocks & Shares ISA. They're super easy to set up and save. And experts handle the investing for you.

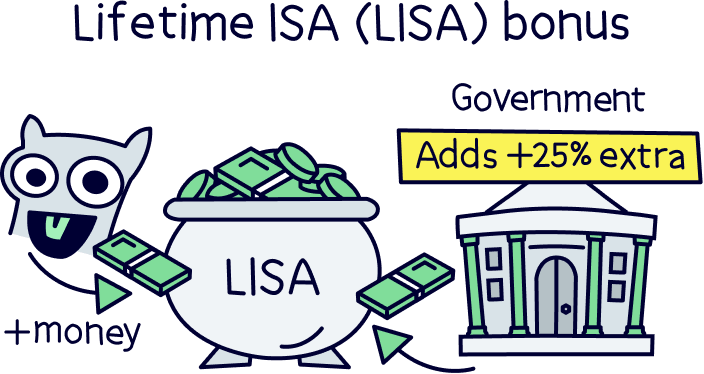

If you’re saving to buy your first property or you’d like to save for later in life (over 60) in addition to a pension, a Lifetime ISA offers some serious perks. You can save up to £4,000 and the government will give you a 25% on the amount you save.

That’s potentially an extra £1,000 per year. Completely free!

Learn more with our guide to Lifetime ISAs.

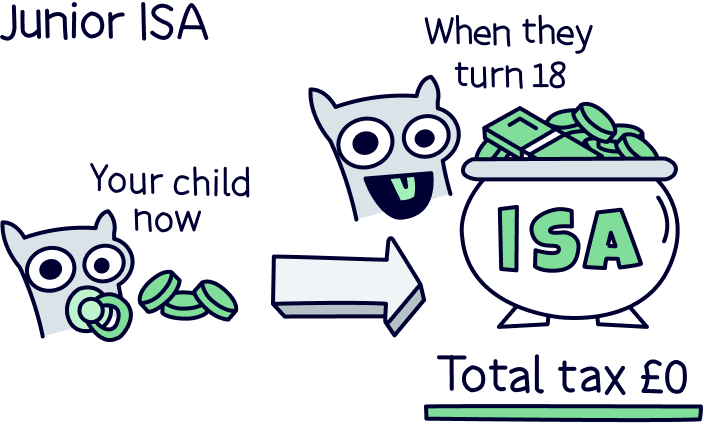

Looking to open a long-term savings account for your kid’s future? A Junior ISA (or JISA) is a great option. You can opt for a Junior Cash ISA or a Junior Stocks and Shares ISA. (a Junior Stocks & Shares ISA is far better for long-term saving).

It will be in their name, and technically their money, which they’ll be able to access when they turn 18.

And because it’s your kids money, Junior ISAs are not included in your annual £20,000 ISA allowance. They have their very own allowance that is separate. (Right now, it’s £9,000.)

Learn more with our guide to Junior ISAs.

So, to sum it all up, in one UK tax year (6th April to 5th April), you could open:

✅ One of any of the above types of ISAs

✅ One of all the above types of ISAs

But not:

❌ More than one of the same types of ISAs

Ready for a welcome plot twist?

You don’t have to close your ISAs from previous years when you open new ones.

Yep, you can keep them all open. This means you could end up with a bunch of ISAs that you’ve accumulated over the years – either ISAs with different providers or different types of ISA with the same provider.

(When we say providers, we mean banks, building societies and investment platforms – basically, whomever you’re getting your ISA from).

You can’t pay into more than one of the same types of ISA in the same year. So if you pay £1,000 into one of your Stocks & Shares ISAs in May, you need to keep paying into that same account for the rest of the tax year – until the following 5th April. Then you can swap after that.

But you can pay into more than one ISA if they’re a different type – for example, you can put £1,000 into your Cash ISA and £1,000 into your Stocks and Shares ISA.

And you can also transfer your funds from one ISA to another. So if you want to do some ISA spring cleaning by moving your money into fewer accounts, this is:

So, there we go. You can have as many ISAs as you like, as long as you only pay into one of each type each tax year (6th April to 5th April the next year).

So if you open a new one, you then can’t pay into any old ones. (It’s also worth noting, you don't have to open a new one every year, you can keep one for years and years).

The main types of ISAs are:

Every year, you can use your £20,000 ISA allowance however you like across all of the ISAs, except from a maximum of £4,000 per year for Lifetime ISAs.

For long term saving, we recommend you open a Stocks & Shares ISA. You’ll earn a lot more money than a Cash ISA. They’re super easy to set up and it’s all managed for you by experts.

And if you’ve got kids, an awesome bonus, you can also have a Junior ISA, which is completely separate, and in your kids name, and you can put £9,000 in per year.

Happy saving!

Learn more about Stocks & Shares ISA. They're super easy to set up and save. And experts handle the investing for you.

Learn more about Stocks & Shares ISA. They're super easy to set up and save. And experts handle the investing for you.

Learn more about Stocks & Shares ISA. They're super easy to set up and save. And experts handle the investing for you.

This article was written by the team at Nuts About Money, and fact-checked by 2 independent reviewers. You’re in safe hands.

Learn more about Stocks & Shares ISA. They're super easy to set up and save. And experts handle the investing for you.