Article contents

Imagine you have a big chunk of money you want to invest. Pound cost averaging is an investment strategy where you invest it little by little over time, instead of all in one go. This helps to spread out the risk of investing your money.

Got a big chunk of money? Hooray! Want to invest it? Good decision.

If you're not sure where to invest, take a look at the best Stocks & Shares ISAs – they can be an ethical ISA too.

But you might be wondering: should I invest it all in one go? Or should I spread it out and invest it little by little, known as pound cost averaging (or dollar cost averaging in the US)? It’s a tough call but here’s some info that should help.

If you have a big chunk of money (maybe you’ve sold your house or you’ve received some inheritance) and you want to invest it, you have two options:

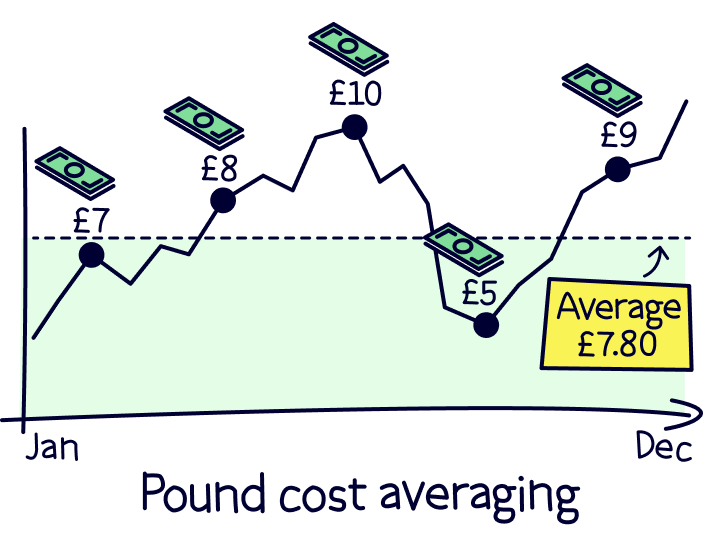

Pound cost averaging is the second option: instead of investing that sum of money in one go, you spread it out and invest it in smaller chunks as regular contributions over a longer period of time (when investing for the long term). You effectively drip feed your money into investments. This could be over the course of a few weeks, a few months or even many years.

Pound cost averaging shouldn’t be confused with investing a percentage of your income. Investing a percentage of your income each month will come with the same benefits as pound cost averaging as you’ll be investing smaller amounts on a regular basis. However, it works a little differently as you’re investing your money as it comes in rather than storing a big chunk of money in a savings account and taking small amounts out to invest little by little.

Check out our recommendations for the best investment platforms.

Pound cost averaging is a way of spreading out the risk of investing your money in the stock market (and other investments), and of trying to even out the ups and downs of the stock market.

Let’s rewind a little. When you invest, you’re buying things like stocks and shares (which are essentially ownership stakes of companies) so that when they (hopefully!) increase in value, you’ll make more money.

In an ideal world, the value of your investments would always climb up and up as the market rises. But in reality, the market will go up and down (called market volatility) and the average value of shares will also rise and fall accordingly (markets almost always go up in the long run though, so if you leave your money invested for long enough and you’ve chosen your investments wisely, you should still increase your savings!).

Let’s say you decide to invest your whole chunk of money in one go as a lump sum investment. Now imagine that the next day, the market drops and all your investments decrease in value.

Before you start panicking, it’s not the end of the world. They’ll hopefully still increase in value again later down the line. But the annoying thing is that if you’d waited an extra month, you could have bought those same stocks and shares (or whatever kinds of investments you made) for less money. And therefore, you’d have made even more money when they eventually increased in value. Annoying, right?

Well now let’s say that instead of investing your whole chunk of money in one go as a lump sum investment, you instead set up a recurring payment so you’re investing it in smaller chunks over a longer period of time. Let’s again imagine that the next month, the market drops.

Well, guess what? Because you only invested a small amount of your money while the market was up, that means you have the rest of your money free to invest at lower prices now the market is going down. Kerching!

Now, it’s important to note that if the market is going down, you’re still losing money (remember, your investments are decreasing in value). However, when the market goes up again, your investments will increase in value. And if you bought them for less because of your regular contributions, that means you’re making a bigger return (more money).

In this way, pound cost averaging is a way of hedging your bets so that you’re not putting all your eggs in 1 basket.

Pound cost averaging (drip feeding your money into investments) has some pretty convincing benefits besides just helping you to hedge your bets. Here are the main ones.

While pound cost averaging has its perks, it’s not all roses and sunshine. And to be honest, there are many people who aren’t big fans. Should you jump invest as a lump sum instead? Here are the negatives.

So, is pound cost averaging a good idea? Well, it’s impossible to give a straight yes or no answer as it all depends on you, your attitude to risk and the market!

Are you a nervous investor? If you want to invest but you keep getting cold feet, a pound cost averaging strategy could be a great solution for you and your investment decisions. Investing smaller amounts over a longer period is often less scary than investing your whole chunk of money all at once. So, it’ll probably make it easier to take the plunge and start growing your money!

The same goes if markets are currently volatile and you’re nervous about the market making a big drop right after you’ve invested your money. Pound cost averaging can help you to spread your bets and even out those ups and downs so you can be more sure of your returns.

That said, it’s important to remember that markets go up more often than they go down! So, even though pound cost averaging can be useful in some situations, it can mean you end up paying more for those stocks and shares overall rather than less.

Plus, remember that pound cost averaging will mean having to store the money that you’re not yet investing in a generic savings account. Thanks to inflation and current bad interest rates, leaving that cash sat around for too long will usually mean it’ll lose value as goods get more expensive over time.

One thing we will say is this. If you do decide to go with pound cost averaging, we’d recommend setting yourself a strict timeframe to complete your investments. That way, you can avoid your money sitting around for too long as cash, and set it to work making you a return sooner rather than later!

If you have a big chunk of money that you’re looking to invest, pound cost averaging can be a great way of hedging your bets to make sure you’re not investing all your money right before the market drops. But there’s no official best strategy, it’s up to you.

Warren Buffett (a very successful investor) once said “it’s time in the market, not timing the market”, and we think this is great.

Instead of trying to ‘time the market’ by investing a lump sum of cash as an entire investment when you think it’s the best time, if you make regular payments of regular amounts you can benefit from simply being in the market over time. You don’t have to worry if the market declines and falls (that’s better for your future performance as it will bring your average price down).

Ultimately, no matter what investment strategy you choose, lump sum investing or investing small amounts over time – it’s sure to be better than leaving your money sitting around not working for you. The longer your money is in the market, the more potential you have for growth in the future.

A good investment strategy is to invest a part of your monthly salary each month with regular contributions into your investment account – it will soon add up and potentially turn into large amounts in future.

Just remember the best strategy is long term investing. That’s why trying to time the market becomes much less important. And past performance is not a reliable indicator of future performance. Even if the market conditions seem great, you can never really know. Timing the market is very difficult.

As far as we’re concerned, the most important step is making the choice to invest your savings in the first place. So, congrats. You’re part way there already!

If you’re still unsure what’s best for your financial circumstances. You can always speak to a financial advisor – check out Unbiased¹ to find the best one for you.

If you’re looking for somewhere to invest, check out the best investment platforms and if you want to learn more about investing, here’s our guide to investing for beginners.

Check out our recommendations for the best investment platforms.

Check out our recommendations for the best investment platforms.

Check out our recommendations for the best investment platforms.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out our recommendations for the best investment platforms.