The Bank of England has announced the Bank of England base rate has been cut from 4% to 3.75%.

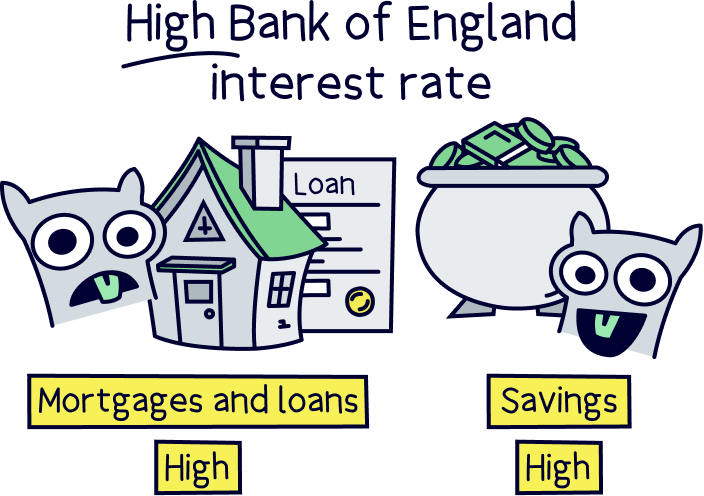

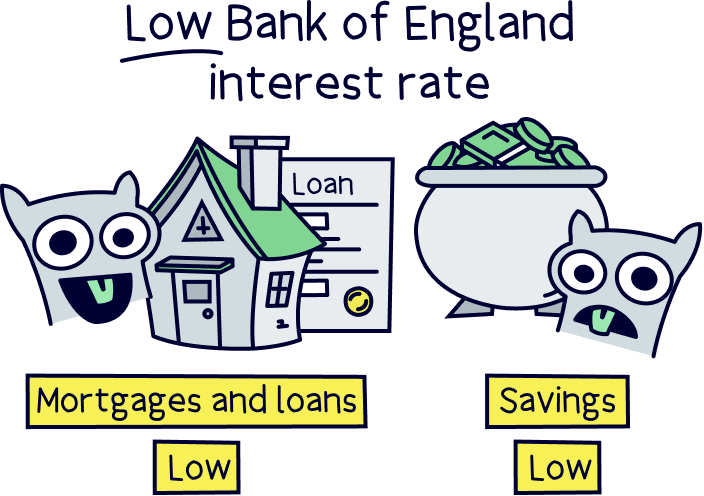

This rate affects things like mortgages and savings accounts, as what banks offer you, such as a mortgage rate or an interest rate on your savings account, tends to be linked to the base rate.

This means that your mortgage might get cheaper either when you next remortgage (if you’re on a fixed term deal), or immediately if you’re on a variable rate. It also means any cash savings you have is likely to make less interest too.

Nuts About Money tip: it can be a good idea to invest your money rather than having a lot in cash savings. When done sensibly, you could earn a lot more over time. Here’s our best managed ISAs (where the experts handle things).

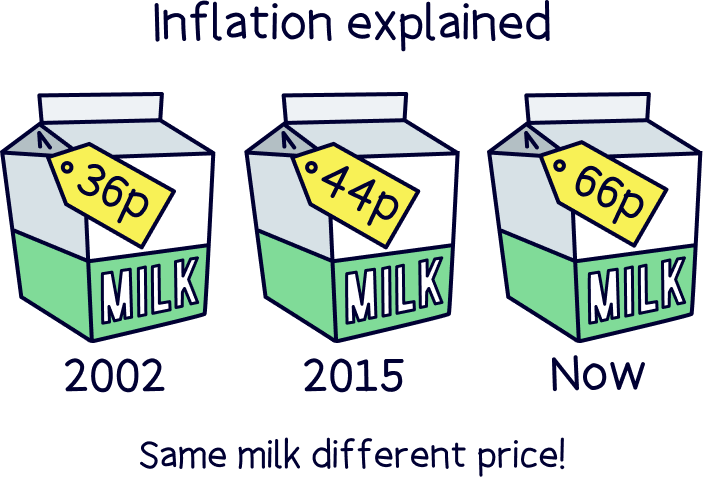

The base rate is designed to essentially manage inflation, which is the price of things (like food and bills) increasing over time.

When inflation is high the Bank of England tends to raise interest rates to encourage people to save more and spend less (which reduces inflation). And when inflation falls, then can reduce the base rate to encourage a bit more spending. Their official target is 2% inflation per year, and in recent years this has been significantly higher (4-11%), but inflation has been falling, and is currently at 3.2%.

If you are saving cash, make sure you’re with one of the best saving accounts. It’s now more important than ever to make sure you’re getting every penny in interest you can.

For those with mortgages, make sure you’re getting a good deal by checking our mortgage comparison tool. And, it’s a good idea to get a mortgage broker to search the market for you too.