It’s that time of year again with all the tax changes set for the years ahead, and this year there’s a lot that could impact your back pocket, your pension and your savings. There’s always lots of changes, but here’s the key ones in a nutshell.

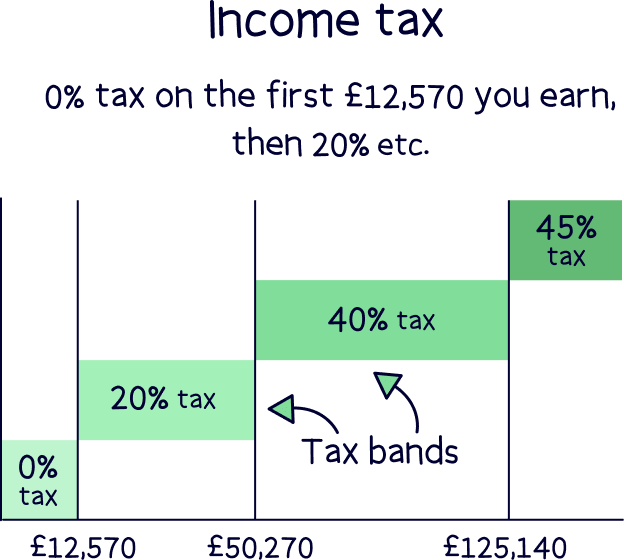

1. The bands for how much tax you pay on your income are frozen for even longer, up until 2031. This means you’ll pay 20% tax on what you earn between £12,570 and £50,270, 40% on what you earn between £50,270 and £125,140 and 45% above that. As people generally see an increase in wages over time, this pulls people into the higher rates of tax, and is seen as a hidden tax increase.

2. If you are self-employed and pay yourself from a limited company via dividends, this has increased by 2% on anything you earn up to £125,140. So the new rates from April 2026 are 10.75% from £12,570 to £50,270 and 35.75% up to £125,140, and 39.35% above that.

3. If you are a landlord, you’ll also pay 2% more on your rental income, for all income bands.

1. Did you know you can pay tax on your savings? Well you can! This has increased by 2% from April 2026. It gets a bit complicated but anything above your Personal Savings Allowance, which is £1,000 if you earn less than £50,270 from things like your salary (not savings), £500 if you earn between £50,270 and £125,140, and £0 above that.

You’ll now pay 22% tax on your savings interest if you earn less than £50,270, 42% if you earn above £50,270 and 47% if you earn above £125,140. Ouch.

It’s pretty essential to be saving into an ISA to avoid taxes on your interest, which is a tax-free savings account, and we also suggest not having too much cash savings either, as it will cost you in the long term versus sensibly investing your money…

Cash savings, even with interest, gradually reduces in value over the years as the price of things like food get more expensive each year (called inflation).

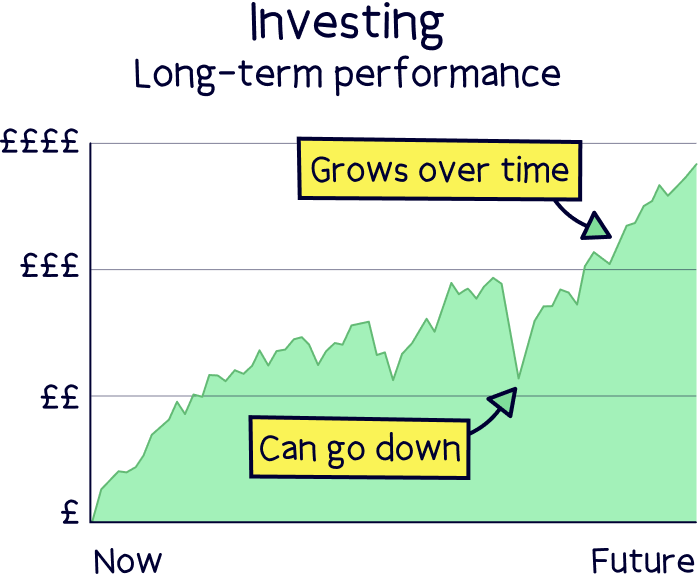

When investing sensibly, you can often stay ahead of this price increase as investing sensibly typically increases more than cash savings on average over time. There’s ups and downs along the way, but it’s not as scary as you might be thinking. Check out an easy to use app like Beach¹, where you can invest within an ISA, and the experts sensibly invest your money over time.

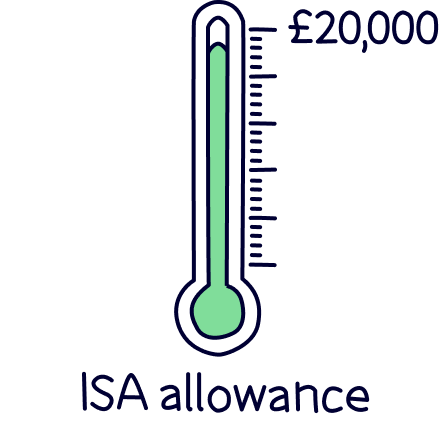

2. The ISA limit for cash savings is reduced from £20,000 per tax year (April 5th to April 6th the following year), to £12,000. Starting from April 2027, and only if you are under 65. This is a change to try and get you to invest more of your savings instead, which benefits you in the long term (with potentially lots more money) and benefits the economy as money that is invested helps grow businesses, which in turn creates things like more jobs.

In the UK, we are very risk averse, and the majority of people have far too much cash savings, which typically isn’t the right place for your money. As we briefly mentioned above, cash savings generally reduce in value over time as the price of things increase, so you ideally want your savings growing more than the price of things increasing, which can only be done with sensible investing.

Cash savings are great for emergencies, and having around 3 months worth of bills in cash is often a recommended figure. Anything above that could be invested for your future. You can still withdraw your investments when you need them (it usually takes a little bit longer), and it’s not as risky as you might be thinking when invested with experts.

So, your total ISA allowance remains at £20,000 per year, with all £20,000 being able to be invested but only £12,000 allowed as cash.

Nuts About Money tip: consider investing, it can really benefit your future. Here’s our top picks of the best Stocks and Shares ISAs.

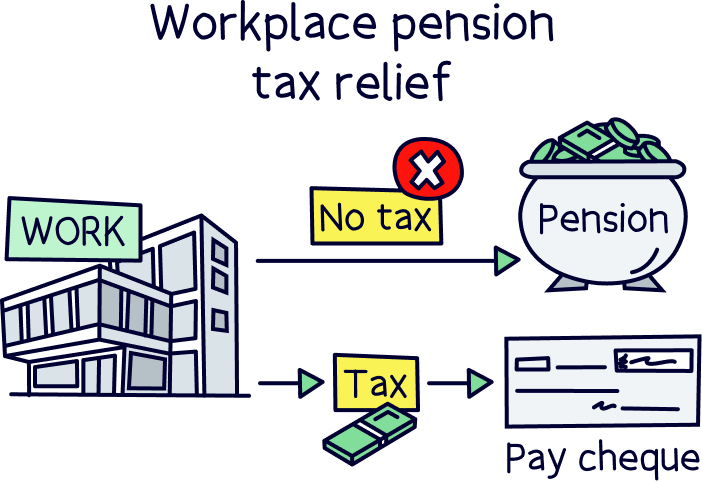

This one is a bit confusing, but saving into your pension gives you a huge tax benefit, you essentially don’t pay any tax on what you put into it - if you do this via your pension from work, no tax is applied as it goes in from your pay.

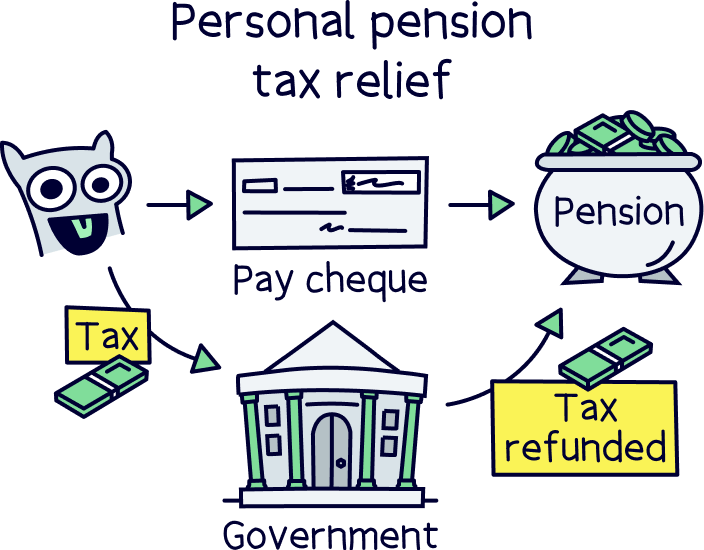

If you pay into your own pension separate from your work, then you get the tax back as a cash bonus.

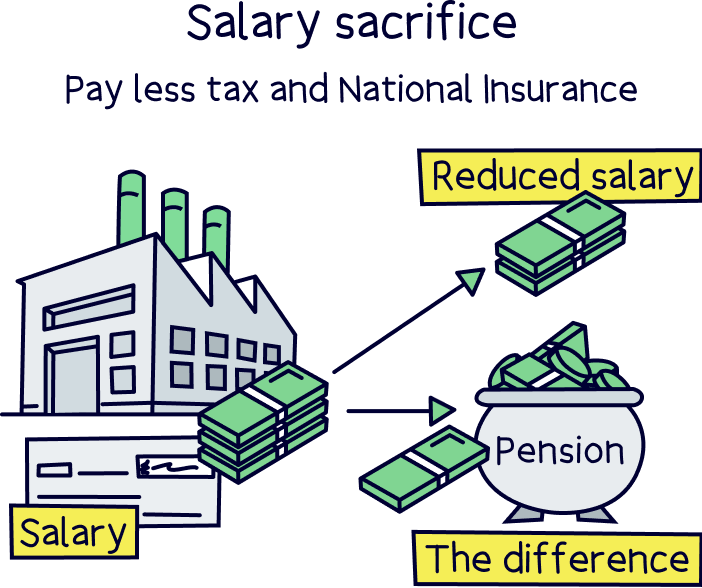

This is called tax relief and has not changed, you can (and should) pay into your pension and keep getting tax relief. What has changed is something called salary sacrifice, which is a little trick your employer can do where they reduce your salary and put the difference into your pension. This means you pay less national insurance contributions, and they also save on employer national insurance contributions.

This salary sacrifice scheme has essentially been scrapped. Technically, it’s reduced to a £2,000 allowance for pension contributions, so you might still save a tiny bit, but essentially it’s a chance to scrap it without lots of paperwork changes. This doesn’t come into force until April 2029.

What this means now is there’s not much difference with saving more into your pension from work (above what your employer will match), versus saving into a pension you set up yourself. So, now you could shop around for the best pension for you, such as one with a great mobile app, or service, a well performing or more suitable pension plan, or where your other pensions are (for instance if you have combined them) and save more into that, without losing out, and still benefit from pension tax relief.

If that sounds interesting, check out our top picks for pension providers, and learn more about pensions with our guide to personal pensions and SIPPs.