How to build a low-cost DIY pension.

Take control of your retirement savings with a self-invested personal pension.

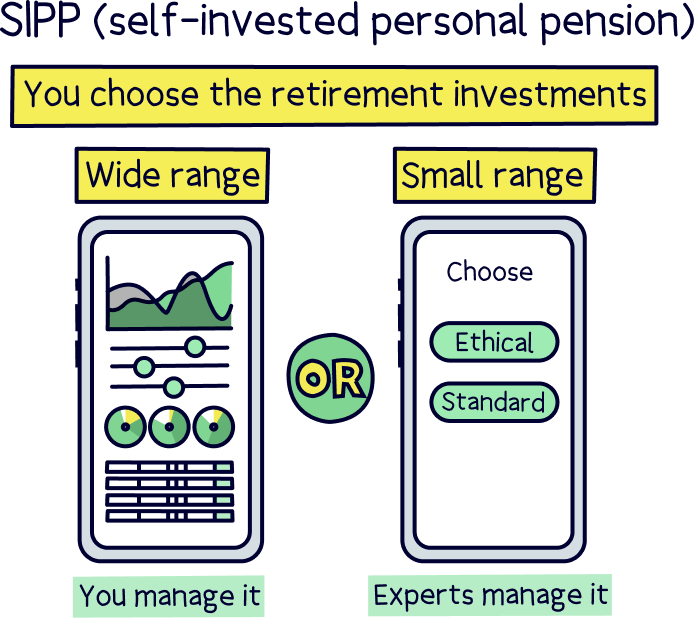

A SIPP (self-invested personal pension) is where you get to decide where your retirement savings are invested. You can choose to make all the investment decisions yourself, or pick from a smaller range of options where the experts handle things for you. A SIPP is a great way to take more control over your retirement planning and savings, and they’re not as scary as you might think!

An easy to use app that allows you to save and invest within a pension and an easy access pot (ISA). Great if you're new to investing.

A super low cost investment platform allowing you to save and invest within a pension and an ISA, and with a great range of investment options.

Find the right SIPP for you by comparing more providers.

Compare SIPPs

Manage your own pension investments or let the experts handle things

Great for combining old work pensions together

Can be low cost

A great way to boost overall retirement savings

Popular option for self-employed people to manage their pension

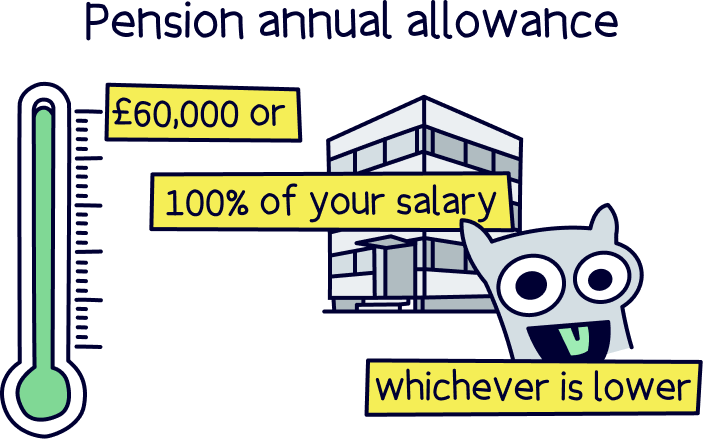

Save up to your total salary, or £60,000 per year

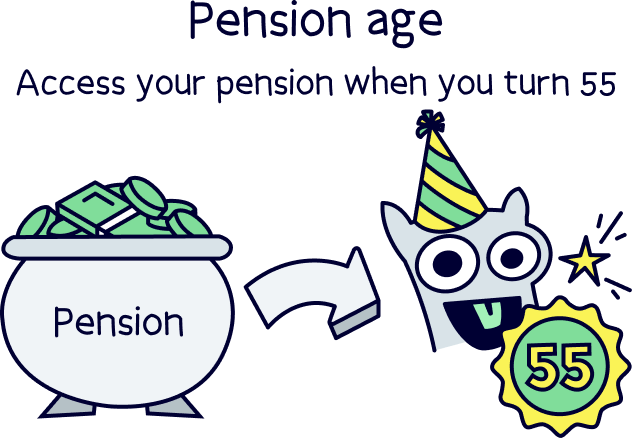

Start withdrawing from age 55 (57 from 2028)

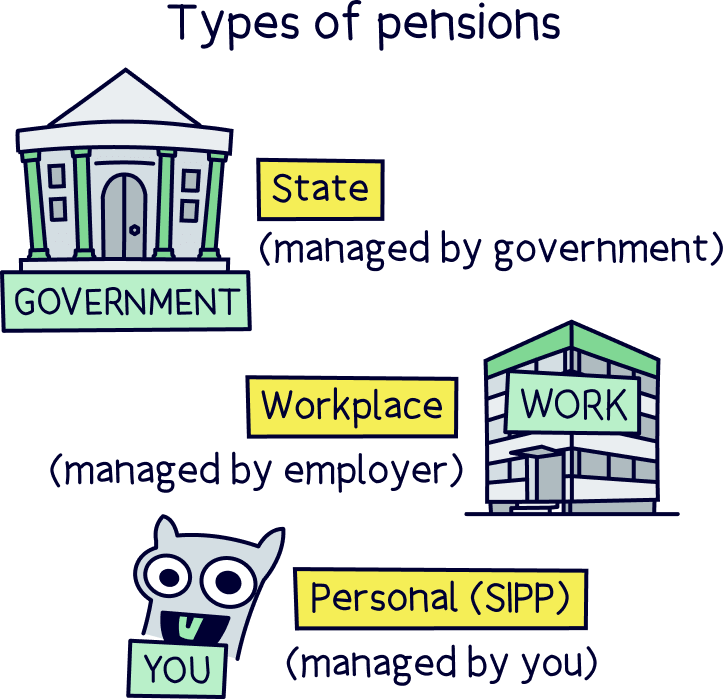

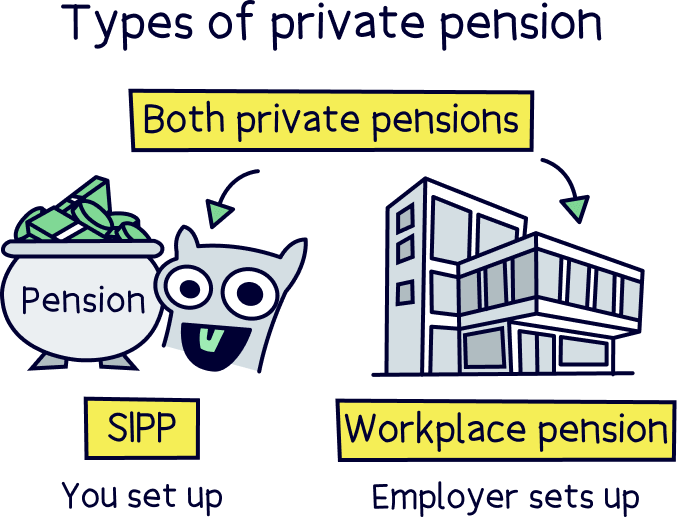

A self-invested personal pension (SIPP for short) is a pension that’s all yours (personal to you), one that you look after, decide how much money to pay into it, which pension provider to use, and which investments to make. And ultimately when you’d like to withdraw from it (as long as you’re over 55 (57 from 2028)).

They are a great way to build a nice big retirement income for you later in life. It’s different to the pension you may get from the government when you retire (which is called the State Pension), and it’s different to a pension your employer sets up for you (if you’re employed), called a workplace pension.

A SIPP is technically a type of private pension, which simply means it’s not the government pension, it’s a pension all in your name (private to you), which you look after, and decide things like how much to add to it (a workplace pension is also a private pension).

SIPPs are often used alongside a pension from work (if you are employed), to boost retirement savings. For instance if you have maxed out your workplace pension contributions to the point where your employer won’t add any extra cash if you do, then it can often make sense to save more into a pension you control, a SIPP.

Note: if you’re self-employed, you’ll need to manage your own pension, they are super popular, and pretty much your only pension option. More about self-employed pensions.

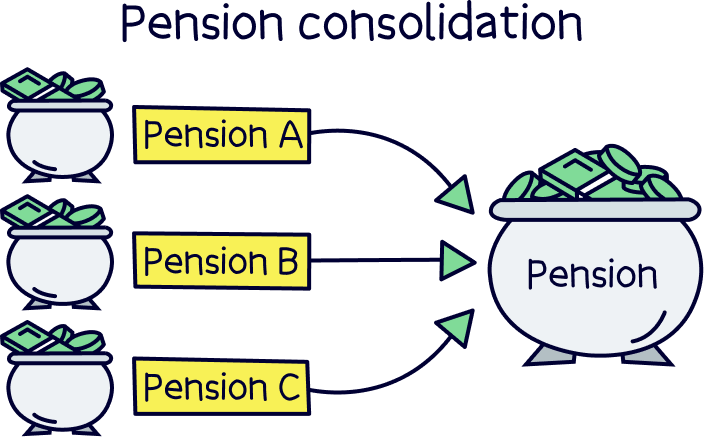

Did you know? You can also move old work pensions over to a SIPP to manage all your retirement savings in one place.

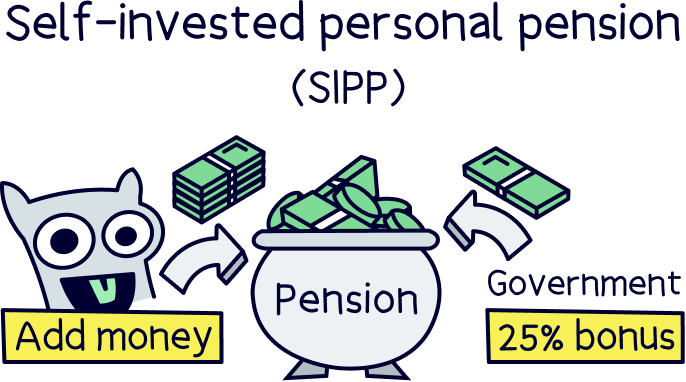

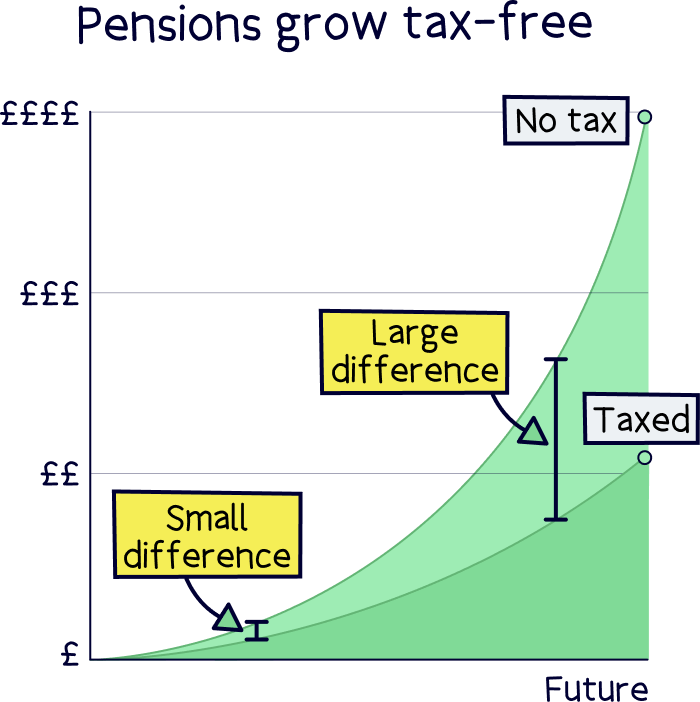

With a SIPP, you’ll get all the typical pension benefits (which we’ll cover in more detail below), such as contributions being tax-free (you’ll automatically get a whopping 25% bonus from the government on everything you put in to refund 20% tax, and you can claim back 40% or 45% tax if you pay it).

You can start withdrawing from age 55 (57 from 2028). And your money will grow tax-free too, so it can grow much larger over time (you’ll likely pay tax when you withdraw from it).

Although they may seem complicated, a SIPP is a type of savings account for your retirement, where the money you add is usually invested (like with most pensions). Everything in that account, such as your money and investments get all the benefits of being inside a pension, such as no tax to pay as it grows, and tax relief on the money you add.

The government loves to collect tax, but has allowed pensions to have tax benefits to incentivise people in the UK to save more for their retirement (so everyone isn't relying on them when they are too old to work).

Just like saving accounts, there's lots of different versions of SIPPs as each provider (a company that offers pensions), can offer their customers a range of options, such as only providing a limited amount of investments, or they could offer a huge range of investments – it all depends on what services and investments the investment platform (SIPP provider) actually offers.

SIPPs are usually split into two categories, which are self-managed SIPP providers and expert-managed SIPP providers…

Where you make your own investment decisions from a wide range of investments (such as what stocks and shares and investment funds to purchase – explained below). These are often called investment platforms.

A super low cost investment platform allowing you to save and invest within a pension and an ISA, and with a great range of investment options.

Find the right self-managed SIPP for you.

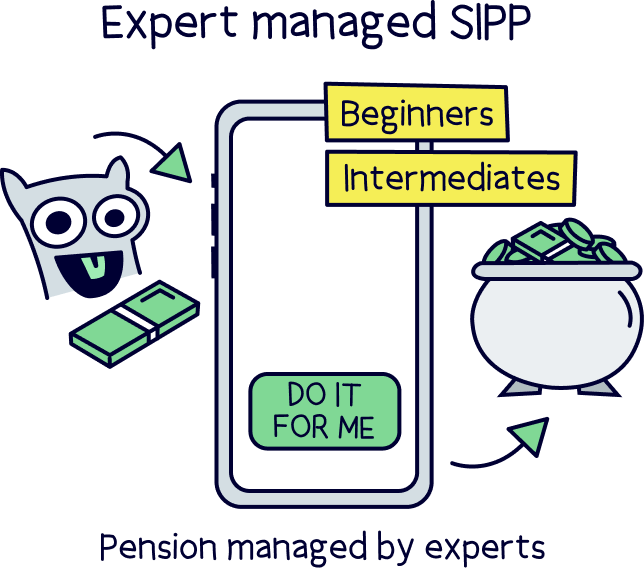

Where you let the experts handle the investments within your SIPP, and you simply add money as and when you like until retirement. These are typically the best option if you aren’t experienced with investing.

Note: these can often be called ‘robo-advisors’ although that term is fairly outdated now. It was a reference to using technology (such as an app) to set and manage things up, rather than a human like a financial advisor. Most modern pension providers have an app now.

An easy to use app that allows you to save and invest within a pension and an easy access pot (ISA). Great if you're new to investing.

Find the right expert-managed SIPP for you.

If you’re self-employed, a SIPP is pretty much your only pension option to save for retirement, but is a great option. You don’t need to be an expert in investing, you can simply let the experts handle that side of things (see our top pick just above), and you simply add money as and when you like.

There’s one thing to be conscious of, and that’s whether you are a sole trader or working under a limited company…

If you’re a sole trader, which means working under your own name, rather than an official limited company, you have a wide range of SIPP options to choose from, as you’ll be paying in directly from your own personal bank account – so you can essentially pick any SIPP you like.

Learn more about this with our guide to pensions for sole traders.

An easy to use app that allows you to save and invest within a pension and an easy access pot (ISA). Great if you're new to investing.

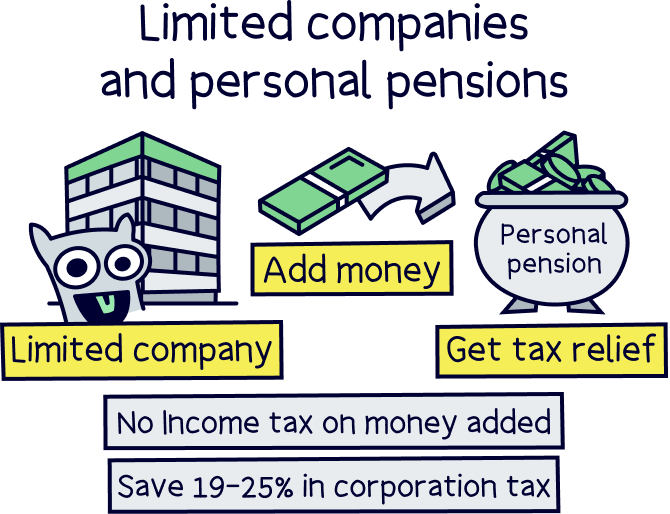

If you’re a limited company director, you can save directly into your own SIPP using your company bank account by making ‘employer contributions’. This is a great option as your pension contributions count as a business expense, which means you save on corporation tax too (saving between 19% and 25% extra).

You also have the option to save from your own bank account too, just like a sole trader, but you won’t be able to save on corporation tax.

However, the range of SIPPs is smaller, as you’ll need to use a pension provider that allows employer contributions.

And with employer contributions, there’s no rule about only saving as much as you pay yourself, meaning you can save up to £60,000 per year into your pension.

Learn more about this with our guide to pensions for limited company directors.

PensionBee simplifies pensions by handling everything for you. Simply sign up and choose what pension plan you want from a few options. The app is easy to use and rated 5 stars.

With an expert-managed SIPP, you’ll typically have one or a few investment options, such as their standard option, or maybe a socially responsible option (good for the planet and people in it).

With a self-managed SIPP, where you manage the individual investments yourself, you’ll often have thousands of investment options. These include:

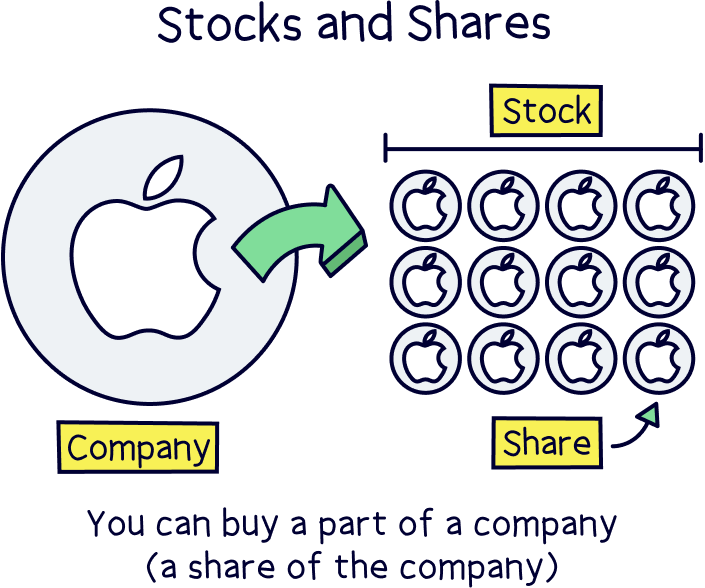

Shares represent small parts of the ownership of a company, they’re a ‘share’ of the company. Shares are typically traded (bought and sold) on stock exchanges across the world, such as the London Stock Exchange (LSE) in the UK, and the New York Stock Exchange (NYSE), in the US.

All the shares of a company combined, equal the overall value of the company. The value of each share can go up and down depending on the performance of the business (such as sales), or the stock market in general.

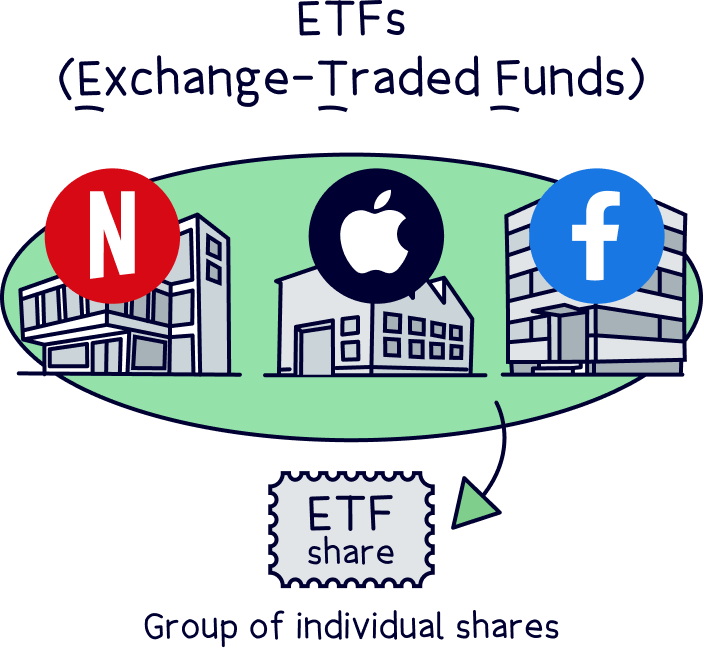

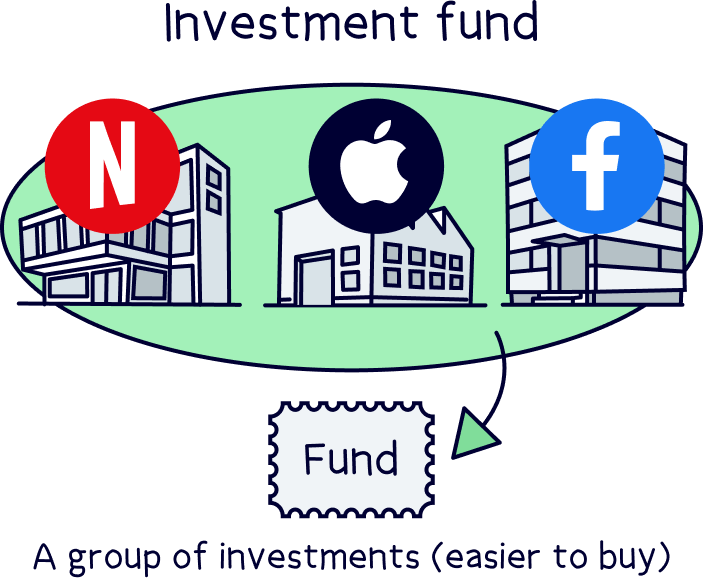

Investment funds are a collection of lots of different investments, all pooled together into a single investment, and they’re super popular. They provide a great way to build a well diversified investment portfolio (your total investments), as you only need to buy a share of an investment fund, rather than lots of different investments.

Investment funds can also be traded on stock exchanges, and these are called exchange-traded funds (ETFs).

There’s two types of investment funds, either passive, or actively managed funds. Passive funds typically track a stock market index, which is a set group of stocks, such as the S&P 500 (the largest 500 companies in the US), or the FTSE 100 (the largest 100 companies in the UK), for this reason they’re also often called index funds.

Actively managed funds are where a fund manager is making the investment decisions to achieve the goal of the fund, such as long-term growth or provide a regular income.

Bonds are effectively loans to large corporations and governments in return for interest payments. They’re typically seen as safer than stocks and shares, but typically grow your money much less. In the UK, these can be called ‘gilts’ if it’s issued from the UK government.

Nuts About Money tip: it’s often not a good idea to invest randomly in things (such as your favourite brands), you should follow a set investment strategy that gradually grows your money over the long-term. That’s why for most people we recommend letting the experts handle your pension for you. They do it for a living, and know what they’re doing!

You can only save as much as your whole income (e.g. salary) per tax year (April 6th to April 5th the following year), or a maximum of £60,000, whichever is lower. This applies as a total to all of your pensions, so includes paying into a pension from work if you have one, and includes the 25% from the government you get when saving into a SIPP.

Note: if you are paying in from your own limited company, there’s no limit on your income, the limit is £60,000 per year.

If you haven’t used up your allowance from the last 3 tax years, you can also use the total remaining amount in the current year (if you've had a pension open), which is called the ‘carry forward’ rule.

Note: you can now contribute as much as you like into a SIPP over your lifetime. Previously you were only allowed to save a maximum of £1,073,100 in total in your pension pots, called the lifetime allowance (otherwise you’d pay more in tax). However, if you add more than this, you’ll still only be able to withdraw £268,275 (25%) tax-free. You still get the 25% bonus (tax relief) and it grows tax-free if you add more so it can still be worth it. And the withdrawal limit is likely to rise in future, although not guaranteed.

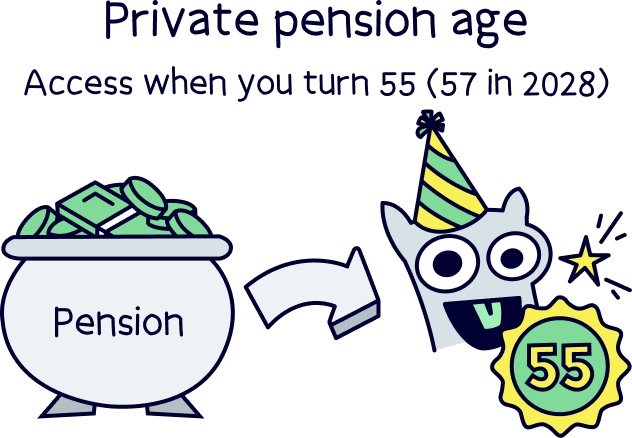

You can’t withdraw any money from your SIPP until you reach the age of 55, which is increasing to 57 from 2028. Any money you add is locked away for retirement. Technically, you can but you’ll pay very hefty penalties often making it not worth it.

Note: if you are terminally ill, you may be able to withdraw money.

You can’t transfer your current pension from work (workplace pension) to a personal pension or SIPP if you are still paying into it (i.e. still employed). You’ll have to wait until you move jobs to transfer it.

If you have any pensions from old jobs, you can transfer them any time. Here’s a guide on how to transfer your pension if you’d like to learn more.

Manage your own pension, which provider to use, and where your money is invested. It’s a great way to control and plan your retirement. So if you’d prefer lower fees, you can opt for a low-cost provider, or if you want to make lots of different investments, you could opt for a SIPP provider who does that. Or a provider that’s easy to use. The choice is all yours.

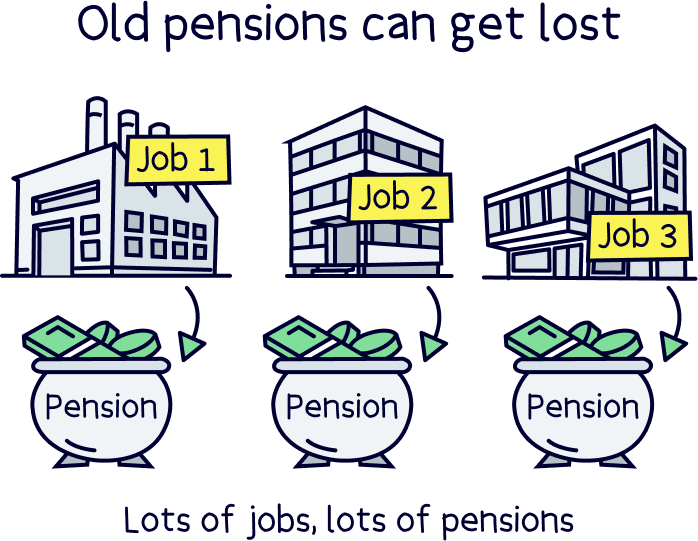

You can combine all your pensions into one (except your pension from a current employer if you have one), called consolidating your pension. If you’ve had a few jobs, you’ll probably have lots of workplace pensions, and if you want to, you can consolidate all of them into one single personal pension.

This has quite a few benefits. The first, with some pension providers, the more you have saved, the lower their fees will be (saving on fees can save you big money over time).

Plus, it gives you a single place to see how much money you have and it makes it easier to manage where and how your money is invested. It also means you won’t forget any pensions when it’s time to retire! As much as 3.3 million pensions are lost (totalling £31.1 billion), according to The Association of British Insurers.

And on a more sombre note, it’s much easier for your loved ones to track down your pension(s) if you pass away if they’re all combined into a single pension.

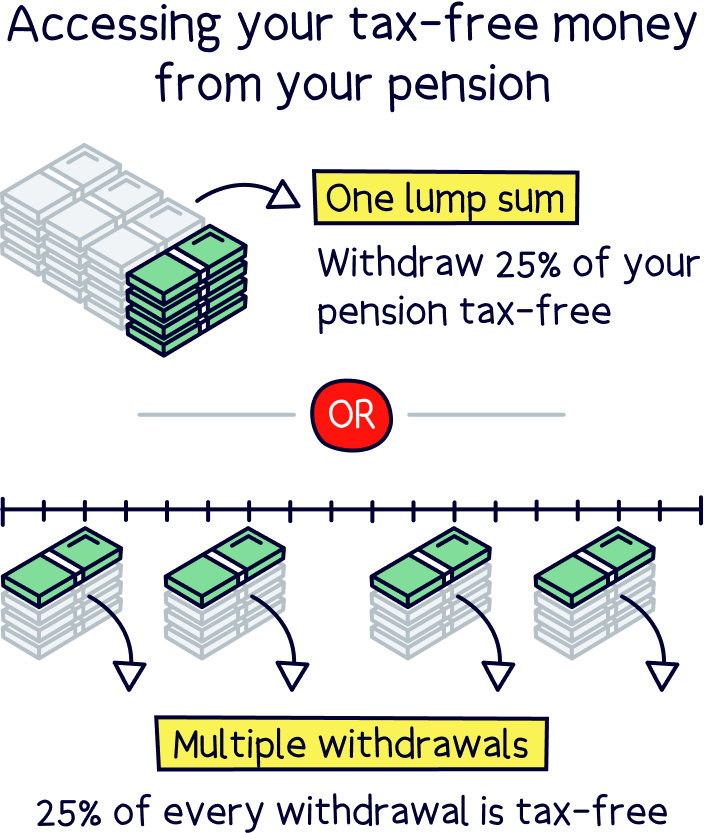

When you hit the ripe old age of 55 (57 from 2028), you can start to withdraw cash from your pension if you want to (although we recommend keeping it saved for as long as possible so it grows even more!).

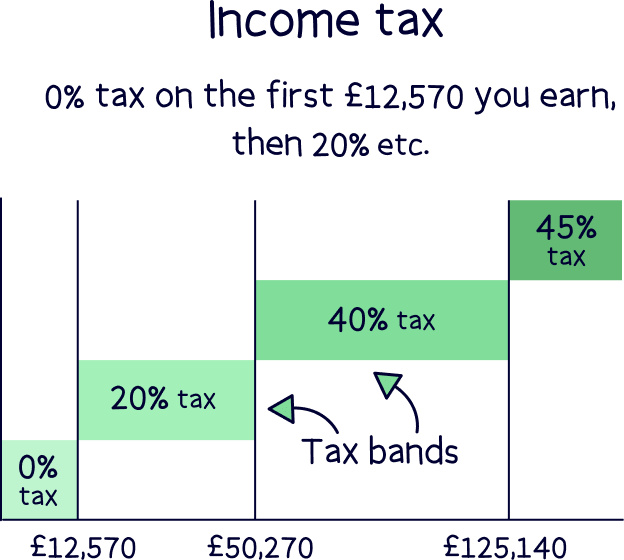

25% of your pension can be taken completely tax-free – and you can take this as a lump sum if you like. Otherwise, you can take an income from your pension and 25% of every payment will be tax-free. The remaining 75% counts as ‘taxable earnings’ (meaning you might have to pay tax).

The amount of tax, if any, will depend on your total income at the time, and is income tax, so the same tax as a salary.

There is a limit however, which is withdrawing a maximum of £268,275, which is called your lump sum allowance.

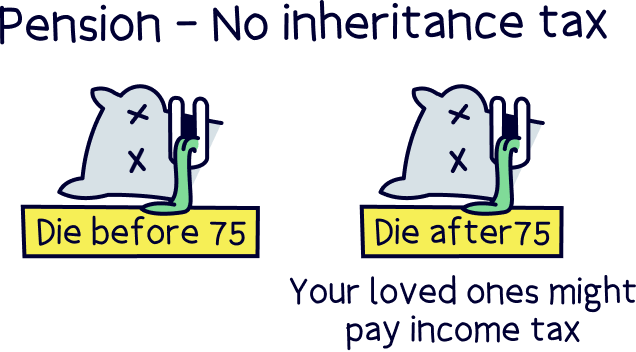

A SIPP, just like most pensions, are a bit special where they can be passed on tax-free in some circumstances.

For example, if you pass away under the age of 75 your beneficiary (the person who receives your pension) can receive the whole amount tax-free.

If you pass away after the age of 75, your beneficiary will have to pay income tax on the amount they withdraw, and they can withdraw it as they like, either as a lump sum or withdraw as and when they want to. The amount of tax they’ll pay depends on their personal income tax rate at the time.

With self-invested personal pensions, you’ll pay a range of fees, depending on what type of investments you want to make. Just like most things, you can pay a lot or little depending on the provider (company).

The pension provider itself will typically charge a fee to manage your pension account, which is often called an annual administration fee, or platform fee.

It’s normally a fee on the total amount of your investments and charged each year, and can range from 0% to 1%+ per year depending on the pension provider. It can sometimes be a flat fee too (e.g. £12.99 per month).

Most pension investments are within investment funds, and these typically charge an annual fee too. The amount depends on the fund itself, and can range from 0.05% to 1.5%+. Passive funds (explained above) are often lower cost than actively managed funds (explained above) as there's less work to do by the fund managers.

If you’re buying and selling your own investments such as stocks and shares, and investment funds, you’ll normally pay a share dealing fee.

This is a fee for the investment platform (the pension provider) to buy and sell investments for you, and you’ll usually pay it each time you buy or sell an investment. This can sometimes be free (commission-free), or range from £1.50 to £11.95, it all depends on the investment platform you choose.

If you want to transfer an existing pension, and move all of your investments from one provider to another, there might be transfer fees. These are typically the same as the dealing costs, and apply per investment, but can vary, and sometimes there won’t be any fees at all.

There might also be an admin fee from the old provider for the process of transferring, although these are rare these days (but it's worth checking).

Depending on the provider, and what you do with your SIPP, there may be extra fees. For instance, to start withdrawing money from your SIPP there might be an admin fee (often around £150 per year).

With a self-managed SIPP, you might have all of these fees (account fee, investment fund fee and share dealing fee), it all depends on which investments you want to make.

With an expert-managed SIPP, you’ll normally just be shown one total fee, which is a total of the account fee and the investment fund fee. Which makes it a bit easier to understand.

Keen to get saving within a SIPP? Good decision! It’s a great way to build a comfortable life in retirement – hopefully meaning no money worries, and no stress (except maybe which holiday to go on).

You can open as many SIPPs as you want, so you could actually have a personal pension managed by the experts, and a SIPP that holds some investments that you’d like to make yourself. Although don’t open too many, or you may lose track, remember all those lost pensions out there! We typically recommend having one to manage all of your retirement savings.

Opening a SIPP, and transferring any old pensions you have is easy too – if you choose the right one, your new provider will handle pretty much everything. The only hard part is finding the best one for you.

And that’s where we come in, we’ve already done the research to find the best options for you. Here’s where to compare all the top SIPPs, or check out our top picks below.

Huge range of investment options and a flat fee per month (lower cost for large balances).

Easy to use. Great for managing a pension and general savings together. Combine old pensions service.

A SIPP follows the same rules as all other private pensions, such as your pension from work – you can’t access your cash until you’re 55 (57 from 2028). Which is the official pension withdrawal age.

However, we recommend that you keep it invested for as long as possible so it grows even bigger over time! You can take money out as and when you like, if you need to.

Note: once you start withdrawing cash from your pension pot, you normally won’t be able to add as much money back in as normal. Your allowance reduces from £60,000, or your total annual income, to £10,000 per year. This is called the Money Purchase Annual Allowance (MPAA).

When you retire, or decide you want to start withdrawing from your pension (from age 55), you can take 25% out as a tax-free lump sum if you want to. Sometimes people do this to pay off the rest of their mortgage if they have one.

You don’t have to though, and if you don’t, 25% will still be tax-free, and you could take a regular income with 25% of each payment tax-free. Or, in various other ways, 25% will still be tax-free.

The remaining 75% will be eligible for tax, and how much you’ll pay will depend on your income and the tax rules at the time. The tax is income tax, which is the same tax as your salary now.

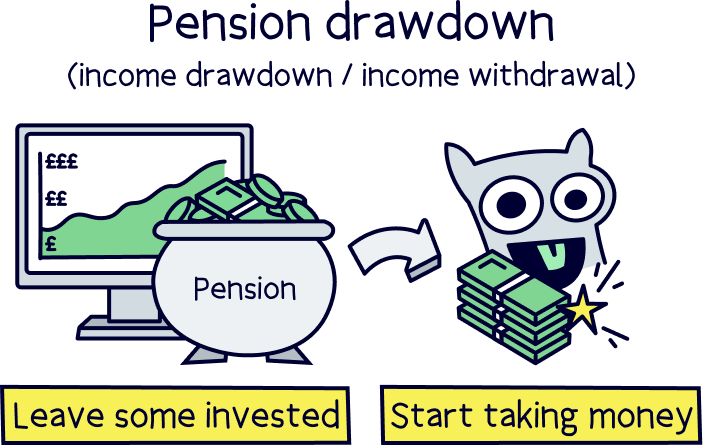

There’s two main options for retirement, you can either keep your money invested (often in lower risk investments) so it keeps growing over time and simply withdraw a regular amount from it each month, which is called drawdown.

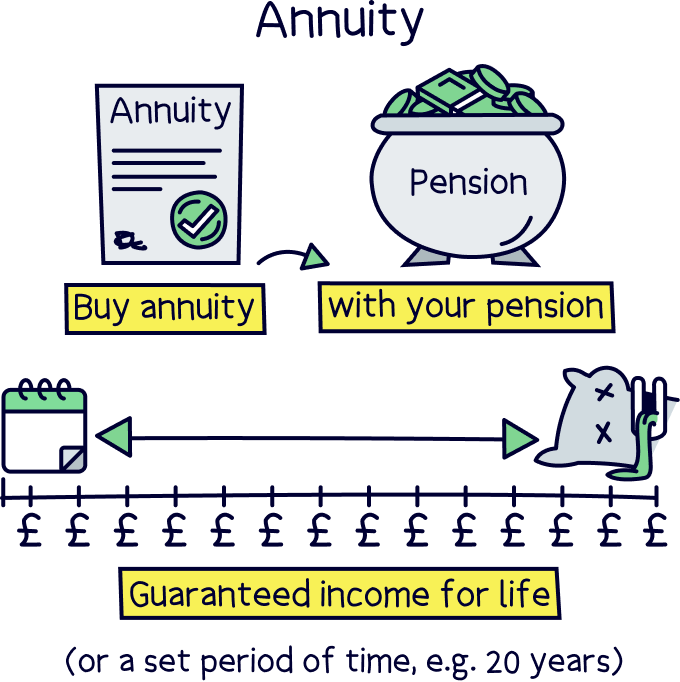

Or, you can use the whole amount (or any partial amount such as 75%) to buy an annuity – this gives you a guaranteed income every month for the rest of your life, or a set period of time, such as 20 years.

The choice is yours! And most pension providers will explain all your options when the time comes, but you could also speak to a financial advisor too, and get a free advice appointment with Pension Wise.

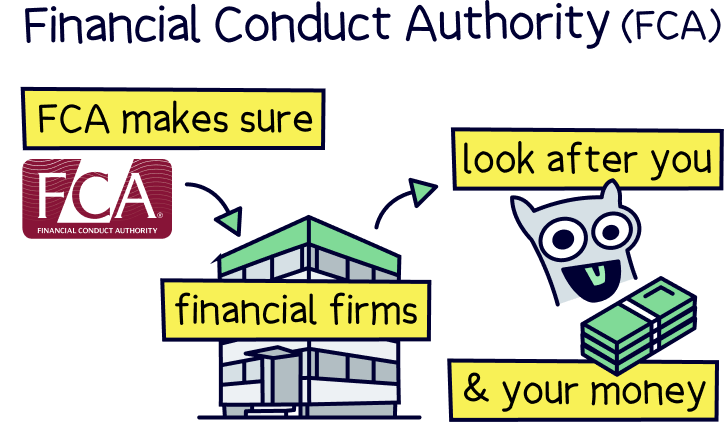

Yep! All pensions, including SIPPs, are very safe to open and use. In the UK they are looked after by the Financial Conduct Authority (FCA), who are responsible for making sure investment companies are themselves looking after their customers and their money.

Pension companies need to be authorised by the FCA and are regularly reviewed to make sure they are operating correctly.

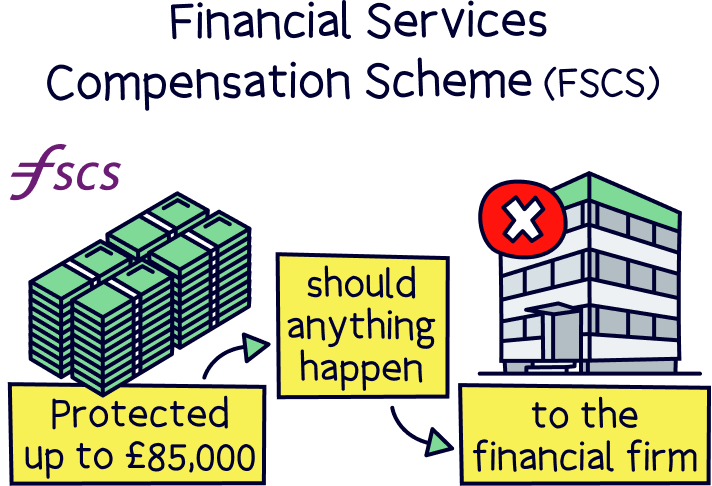

This also means your money is protected by the Financial Services Compensation Scheme (FSCS), which can provide compensation up to £85,000 should a pension provider, such as an investment platform going out of business, and not be able to return some of your money (if they were holding some of your cash).

However this is a very last resort, your money and investments are held within your SIPP, typically with a separate bank to your pension company, all in your name, and can only be returned to you.

Compare all the top providers to find the right one for you.