Article contents

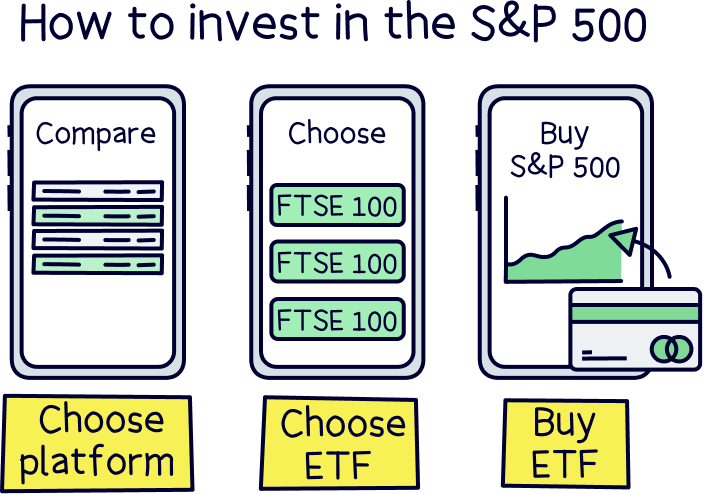

You can invest in the S&P 500 in just 3 simple steps. First, find the right investment platform for you (we’ve listed the best below), then find the right ETF for the S&P 500 (we’ll cover that below too), and then buy. Simple!

Keen to invest in the future of the American economy, the S&P 500 (SPX)? You’re in the right place. Here’s a run through of the best way to invest in the S&P 500 if you’re from the UK, and we’ll cover the ins-and-outs of the S&P 500 too – just to make sure it’s the right investment for you.

The S&P 500 (Standard and Poor’s 500), is the largest 500 companies that are listed on stock exchanges across the US. It’s technically called a stock market index (a set group of companies that makes things easier for investors to measure, in this case, the American economy). Another popular index is the FTSE 100 (top 100 companies in the UK).

We’ll cover the S&P 500 in much more detail below, as we’re sure you’re keen to find out how to actually invest in it.

The S&P 500 is currently sitting at:

This is probably going to be easier than you think! As the S&P 500 is an index, and a very popular one, there are investment funds set up to make it super easy to invest in the S&P 500.

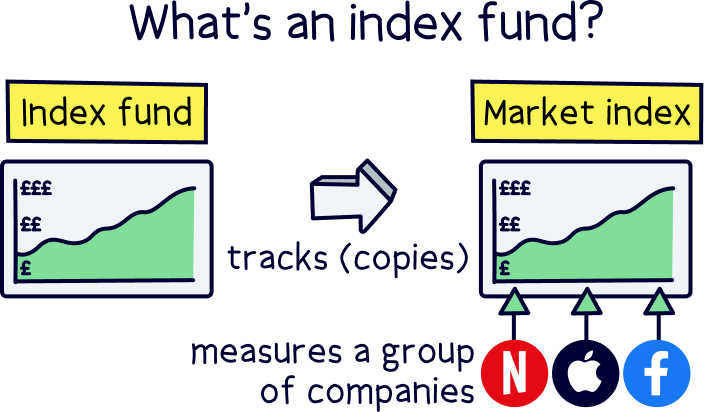

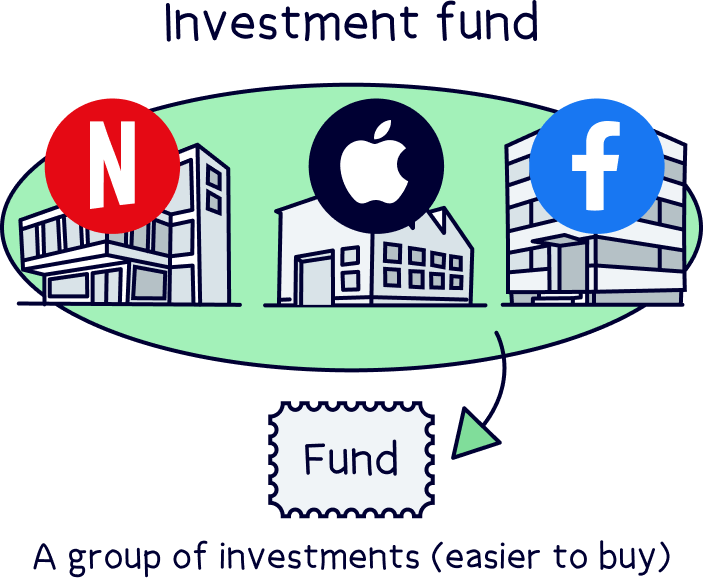

An investment fund is simply a collection of lots of different investments (such as shares in companies), all pooled together into a single investment. Funds that track stock indexes are often called index funds.

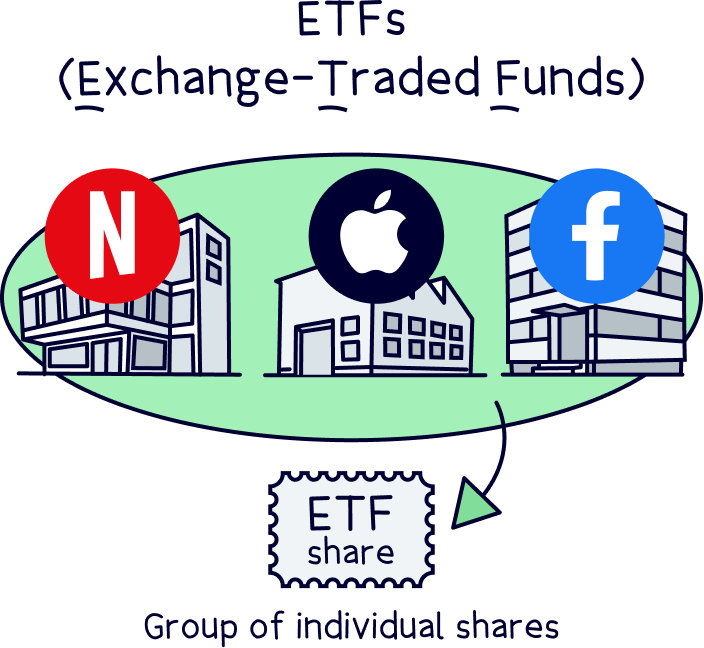

And to make things even easier, investment funds can be traded on stock exchanges, just like individual company shares, making them super easy for you to buy directly. These funds are called exchange-traded funds, or ETFs.

Therefore, all you need to do is buy an ETF that tracks the S&P 500. As simple as that. Let’s run through how to do that now.

First things first, you’ll need to find an investment platform that offers ETFs and index funds (exchange-traded funds). Don’t worry though, we’ve done the hard work already, and reviewed all the best ETF platforms, and here’s who comes out top:

£10-£100 fractional share

Lightyear is a slick investment app that's easy to use, has a decent range of investments and low cost (commission-free). It also offers one of the best rates for saving cash. You’re able to store and trade in multiple currencies, and businesses can open accounts too.

ETFs and shares are completely free of any commission. You’ll only pay currency conversion fees when buying foreign stocks (e.g. US stocks), and it’s a very low fee (0.10%). And, this applies to both a Stocks and Shares ISA and a General Investment Account (GIA), making it one of the lowest options out there.

If you’re new to trading and investing, it’s a great place to start and learn. It’s easy to use, and you’ll be able to buy the shares you’re after in no time. Plus, there’s a good amount of analysis for each stock too – so you’ll learn as you trade, and find new opportunities too.

The range of investments is good for stocks and ETFs, and includes options from across the world.

eToro is one of the best investment platforms out there - and is by far the most popular, with over 30 million customers.

Why? eToro is very low cost (commission-free stocks), easy to use, and has lots of awesome trading features. There's also a community of other traders to learn from and even copy.

It’s also got the largest range of assets to trade and invest in – including stocks, ETFs, crypto, CFDs, currencies and commodities (such as gold).

0% fees

InvestEngine is a super low cost investment platform allowing you to save and invest within a pension and an ISA, and with a great range of investment options.

There's no fees for an account, and no commission to buy and sell investments. And there’s a wide range of investment options, with over 700 investment fund options (ETFs only).

It's more than just low cost though, it’s pretty easy to use, there’s some great features to help you invest, and the customer service is excellent.

Minimum deposit: £100

Best for: those looking for a low cost platform with a range of fund options

• Easy to use

• Very low cost

• Commission-free

• Great range of ETFs

• Great customer support

• Only ETFs (but a wide range)

• No financial advice

AJ Bell is well established, with a good reputation.

It's one of the cheapest traditional stock brokers out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is great too.

Overall, it's one of the best options.

Once you’ve decided on the right investment platform for you, you’ll also need to decide which investment account you want to use. In the UK, there’s 3 options, a General Investment Account (GIA), a Stocks and Shares ISA, and a personal pension.

We’ll run through these more in-depth further down, this is just a quick summary to guide you on the right account for you.

Nuts About Money tip: if you’re unsure which account to use right now, go with a GIA, you’ll be able to open the other accounts later if you want to.

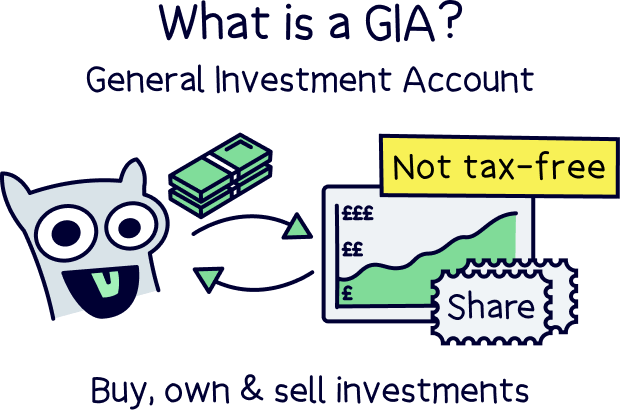

This is the standard investing account with no bells-and-whistles. You can open as many as you like, and pay in as much as you like too, but you might have to pay Capital Gains Tax on your profits in future – when you sell, and if your profits exceed £3,000 per tax year (April 6th to April 5th the following year).

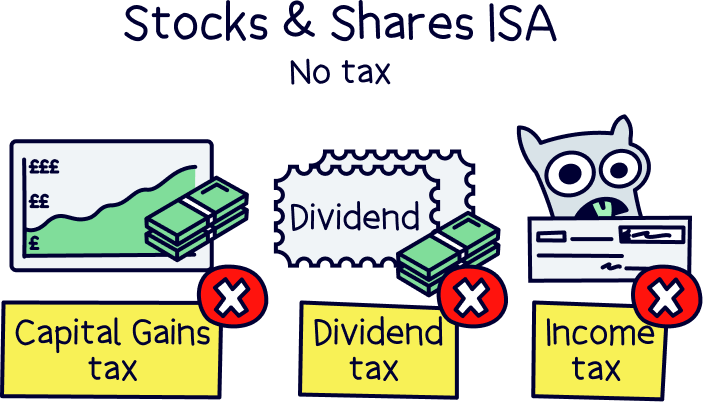

A Stocks and Shares ISA is an investment account to save completely tax-free. Pretty amazing right? You can save up to £20,000 per tax year, and you’ll never, ever, pay tax on your profits or investment income.

However, you can only pay into one each tax year – so pick wisely. We’ll cover our recommendation for how to best use your ISA later on.

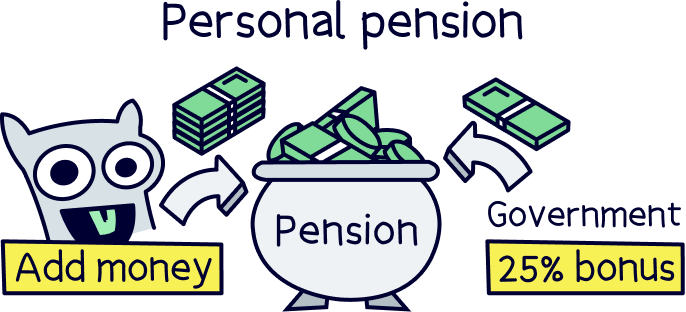

A self-invested personal pension, or SIPP, is the perfect account for saving for retirement. You’ll get a massive 25% bonus on everything you save (not a joke!), and your money will grow tax-free.

However, you might pay tax when you withdraw it later down the line. And you won’t be able to touch the money until you’re at least 55 (57 from 2028).

Okay, now you've set up your investment account with your investment platform. Let’s get onto the S&P 500 and find the right ETF for you.

On your investment platform (click to scroll up and see our top investment platforms), you’ll see a huge list of lots of different ETFs – don’t panic, you’ll soon know what they all mean.

We want to find an S&P 500 index fund – and you should be able to search using the search box on most investment platforms. Once you've done this, you should see a list of all the S&P 500 ETFs, there’s quite a lot isn’t there? Let’s run through this in a bit more detail.

There’s two main types of ETFs, there’s ‘accumulating’ (Acc), and ‘distributing’ (Dist). And you’ll probably find most popular ETFs have both options.

Accumulating is where the money the investment makes in dividends is re-invested back into the investment itself (so more of the investment bought). Dividends are payments from the business (some of its profits) to the owners of a business (e.g. the shareholders, or investors). Large, successful companies often do this regularly.

So, with an accumulating ETF of the S&P 500 – if a company pays out any dividends, the investment fund (ETF) benefits, and it uses this money to buy more shares – and as a result the value of the ETF usually increases over time. This has a compounding effect, as the fund now owns more shares overall (which can grow in value), which means you’ll make more money over time, and this snowballs over and over.

With distributing ETFs, the dividends are instead paid directly to the owners of the ETF, rather than reinvested. So, they provide an income to anyone who happens to hold a share of the investment fund. Cash will simply appear in your investment account. Distributing ETFs will grow slower over time as they’re not benefiting as much from compound interest.

You might also notice there’s lots of different companies offering the same S&P 500 ETF. The top ETF providers across the world are:

An ETF provider (the company who has made the ETF) manages the investment, they’ll buy and sell all the individual investments (e.g. shares of a company) to put together the ETF, and manage all the day-to-day management.

For instance, they’ll buy shares of all the 500 top companies in the US to put together their S&P 500 ETF, and they’ll continually adjust the investments if companies fall out of the index, and new ones enter.

Each provider charges a fee to do this, which is an annual fee based on the percentage of the investments (for instance 0.10% of your investment in the ETF). And with ETFs, this fee is represented by the Total Expense Ratio (TER). You’ll pay this fee to hold the ETF as an investment, although it’s actually automatically deducted from the fund itself by the provider, you won’t pay out any cash.

With S&P 500 ETFs, they’re super low cost, as there’s not much management to do (as it just tracks the S&P 500 index). In fact, here’s what you’ll pay with the most popular providers:

All quite similar aren’t they? Effectively they’re all the same ETF, just from different providers. So, if cost is a real issue, you could simply go for the lowest cost (Invesco).

Now all that’s left to do is buy, buy, buy.

After you’ve decided which type of S&P 500 ETF you’d like, either accumulating, or distributing (get the dividends), and which provider you’d like to use, all that’s left to do is deposit your cash to the investment platform, and buy, buy, buy. You’re now the proud owner of an S&P 500 ETF – good job!

Investing in the S&P 500 is typically seen as a great investment over the long term, as it represents the United States economy, and to an extent, the whole western world (it's used as the benchmark for other investment strategies to compare against). But that doesn’t mean the good performance is guaranteed to continue into the future.

The S&P 500 (Standard and Poor’s 500) is one of the most popular stock market indexes in the world – there’s trillions of pounds of investors money, from across the world, and of course lots of UK investors.

It tracks the largest 500 companies listed on stock exchanges in the United States – the two main ones are the New York Stock Exchange (NYSE) and the Nasdaq (National Association of Securities Dealers Automated Quotations).

An example of some of the largest companies in the US, and so part of the S&P 500, are:

To be included in the S&P 500, the company must have:

There’s a few other small criteria to be included too, but these are the main ones.

Rather than each company having an equal share of the index, the index is ‘weighted’ by the size of the companies in the index, with the bigger companies having a bigger share of the index.

As part of the measurement, it uses the number of shares that are publicly traded, which means able to be bought and sold freely to the public, rather than shares held by people who work there (so not traded).

The S&P 500 is an index managed by the S&P Dow Jones Indices, and can be used as a measure of the American economy. And has seen some great returns over time (how much it’s grown). Since it began in 1928, it has returned an average of roughly 9.8% per year, so you can see why lots of investors are keen to invest in funds representing the S&P 500!

Note: the most popular ticker symbol for the S&P 500, which is a short code to identify stocks and indices, is SPX (or $SPX).

Investing in an exchange-traded fund is a great way to invest and build a portfolio of investments, without actually having to buy all the individual investments – you can simply buy one, or a handful of ETFs, and have a well-rounded investment portfolio, suited to your goals (such as long-term growth or providing a regular income). Making it much easier, and much cheaper too (you’ll typically save a lot in fees to buy individual investments).

They can contain a huge range of investment, such as tracking an index like the S&P 500, or they could have specific types of investments, such as only technology companies (technology stocks), or energy companies – there’s a huge range of ETF options out there, all suited to different types of investors.

The alternative is a mutual fund, which is very similar (an investment that has lots of different investments within it, and looked after by a fund manager). The difference is an ETF is simply a fund you can buy on a stock exchange (such as the London Stock Exchange in the UK), and traded frequently, whereas a mutual fund you’ll buy directly or via a stock broker (like AJ Bell¹).

Investment funds, such as ETFs and mutual funds can hold a huge range of different investments, such as:

A share of a company, is part of the ownership of a company – you own a ‘share’ of the company. All of the shares combined total the value of the company. The share price can go up and down, and is normally affected by the business performance (e.g. sales), and the stock market in general.

Shares can be bought and sold on a stock exchange, and there’s typically a stock exchange in every country in the world, such as the New York Stock Exchange (NYSE) in the USA (plus others).

Nuts About Money tip: if you’re looking to buy individual stocks and shares, rather than ETFs and investment funds (or alongside), check out the best share dealing accounts.

A bond is essentially loaning your money to large corporations or governments in exchange for a regular income, in the form of an interest payment. Bonds are typically seen as lower risk than stocks and shares, but don’t tend to grow your money as much over time.

Investment funds can also hold property, normally commercial property, such as offices and shops that provide a regular income (rent).

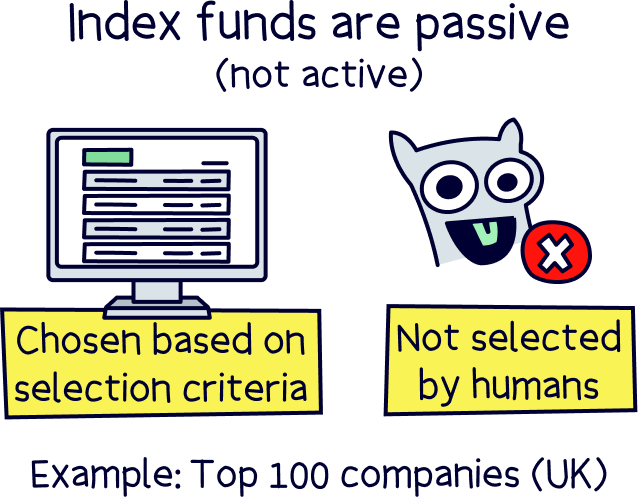

There’s also two main types of investment funds, passive funds and actively managed funds.

Passive funds are investment funds, such as ETFs, that typically track a stock market index (also called stock indices), and so also often called index funds. A stock market index, like the S&P 500, or the FTSE 100 – is a set measure of a stock market, or a subset of the stock market (e.g. the top 100 companies listed on the London Stock Exchange, the FTSE 100).

As an index fund simply tracks and matches an index, there’s not much effort or investment decisions required for the fund manager. That’s how they get their name passive investment funds.

And because there’s not much involvement from the fund manager, passive funds are typically much cheaper than actively managed funds.

Actively managed funds are where the experts (fund managers) do a lot more work. They’ll put together a mix of investments to achieve a set goal of the fund, for instance, long term growth or to provide a regular income. They’ll continually monitor the investments and make changes when necessary.

And because there’s a lot more involvement from the fund manager, the fees are higher – of course they can vary depending on what the fund is.

There’s lots of actively managed funds out there, and you can find a great range with all of the recommended investment platforms above.

We’ve touched on the types of investment accounts you can use to invest in the S&P 500, but let’s run through them in a bit more detail. The right investment account can save you a lot of cash in future, and they all have different benefits and restrictions too.

A General Investment Account (GIA) is your typical investment account, there’s no benefits, but there’s also no restrictions. You can invest as much as you like, and have as many accounts as you like across all the best investment platforms.

However, you will have to pay tax on your investment profits and income, if they’re above the tax-free allowances, which runs across the tax year (April 6th to April 5th the following year).

The tax you might pay is Capital Gains Tax, Dividend Tax and Income Tax. With Capital Gains Tax, you’ve got an allowance of £12,300 in profit per tax year, before you have to pay tax, and this only applies when you sell your investments.

The amount you’ll pay is 18% if you’re a basic rate taxpayer (earn less than £50,720 per year), and 24% if you’re a higher rate taxpayer (earning more than £50,270 per year).

A Stocks and Shares ISA lets you save and invest completely tax-free!

You can save up to £20,000 per tax year, which is your ISA allowance, and applies to all of your ISAs together (e.g. a Cash ISA (to save cash), or a Lifetime ISA (to save for your first home)).

However, you can only pay into one Stocks & Shares ISA per tax year – so pick wisely. A great strategy for investing can be to let the experts manage the investments within your Stocks and Shares ISA – they know what they’re doing, and you could benefit from the tax-free growth, and their expertise with the bulk of your savings.

You can then use a GIA to make your own investments alongside the experts, and unless you have lots of cash within a GIA, you might not pay any tax anyway.

We’ve reviewed all the best expert-managed investment platforms, and the best performing Stocks and Shares ISAs to make things easy for you to find the best investment options for you.

A personal pension is to save and invest for your retirement, and has some awesome benefits. You’ll get a massive 25% bonus from the government on everything you pay in, how great is that?

And if you’re a higher rate (40%) or additional rate (45%) taxpayer, you’ll be able to claim some of the tax back at those rates too.

Your money will grow tax-free too, you don’t have to worry about taxes until the time comes when you want to retire and withdraw cash, at which point, the first 25% of your pension is completely tax-free, and with the rest, you might pay Income Tax on it, just like your salary now, but it depends on how much your income is, as you’ll still get the first part of your income tax-free (currently £12,570).

The downside is your money is locked away until you are at least 55 (57 from 2028).

For investing, there’s two main types of personal pension, there’s simply a ‘personal pension’, which is typically managed by experts, and they’ll grow your money over time in a sensible way (PensionBee¹ is a great option for this. Here’s our PensionBee review to learn more).

And the other option is a self-invested personal pension (SIPP), and this is where you make your own investment decisions, that’s which investment to buy, and when to buy and sell.

We don’t recommend these unless you know what you’re doing when it comes to investing, but check out the best pension providers to find all the best investment platform options.

Nuts About Money tip: if you want to invest in the S&P 500 within your pension, you can with our top recommendation above.

Yep, it’s completely safe to invest in the S&P 500 via ETFs.

The ETF provider (the investment company), and the investment platform, will both be authorised by the Financial Conduct Authority (FCA). The FCA are the people who make sure your money and investments are looked after, and the company is operating in the right way – also, they’ll have been reviewed and approved to look after your money, and will also be constantly monitored.

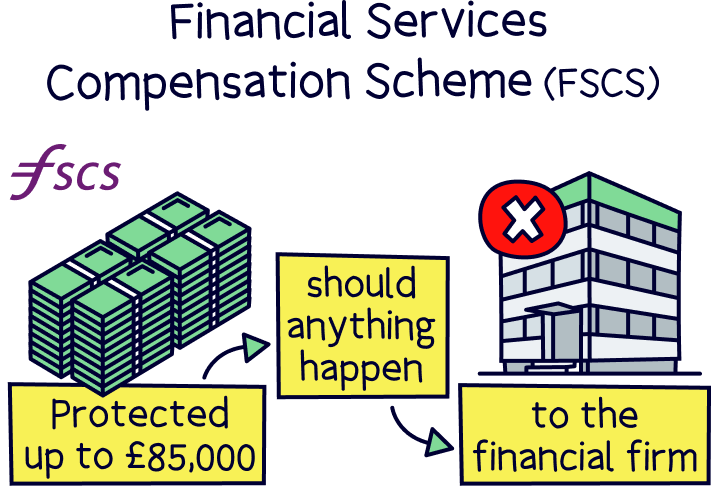

This also means your money is protected by the Financial Services Compensation Scheme (FSCS). That’s where your money is protected up to £85,000, and compensation is provided if something happens to the investment platform or investment provider (such as going out of business).

However, as your investments are held all in your name, they can only be returned to you. They’re also typically held with large banks, such as HSBC, rather than the investment platform itself.

To check if a company is registered and authorised by the FCA, check the FCA register.

Note: FSCS protection only applies to retail investor accounts (so ‘normal’ people), rather than professional investors and companies.

This doesn’t mean the value of your investments can’t go down in value – they can.

That’s all there is to investing in the S&P 500. There’s lots of index funds (exchange-traded funds) set up that track the S&P 500, making it super easy, and cheap to buy and invest in the S&P 500 (and other stock indexes, such as the FTSE 100).

As a full recap, you can invest in just 3 simple steps:

And, we’ve made it even easier for you, to see our recommendations, scroll up or click our recommended investment platforms.

Want to learn more? Here’s our investing home page.

There we go. All the best investing in the SPX and all your future investments!

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible