Article contents

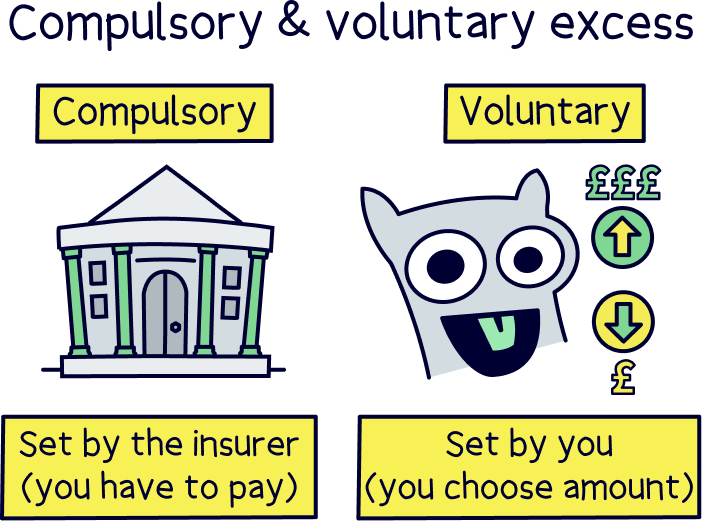

Excess on insurance is how much you’d pay out yourself, if you had a successful claim on your insurance (and so get compensation). It’s made up of compulsory excess, which the insurance company decides how much you pay, and voluntary excess, which is how much you decide to pay.

Heard the word excess while looking for insurance but not quite sure what it means? You’re in the right place. Here’s what compulsory excess means, and a run through of what insurance excess is overall.

The bad news with insurance is that you normally have to pay out yourself, if you make a successful claim (which is where the insurance company pays you compensation or bills on your behalf), and the amount you have to pay is called the excess.

The total excess you’ll pay is made up of two parts, the compulsory excess and voluntary excess. The compulsory excess is how much the insurer sets, which is non-negotiable and you can’t change it, and voluntary excess is how much you set, and you can change it.

We’ve actually got a whole guide on what voluntary excess is, if you want to learn more about that – but we’ll cover the key points below too.

In most insurance claims you will have to pay the excess, but sometimes, you might get the excess refunded back to you, for instance if you were involved in a car accident that wasn’t your fault – your insurance company will try and get the excess from the other person's insurance company.

And often, if you’re getting compensation, e.g. your items were lost or stolen, you won’t actually pay the excess out yourself, it will be deducted from your compensation figure.

For instance, if you’ve insured your luggage for £1,000, and you have an excess of £200, you’ll actually get £800 back from the insurance company (if your claim is successful).

Note: insurance excess covers almost all types of insurance, e.g. car insurance, travel insurance, contents insurance and home insurance.

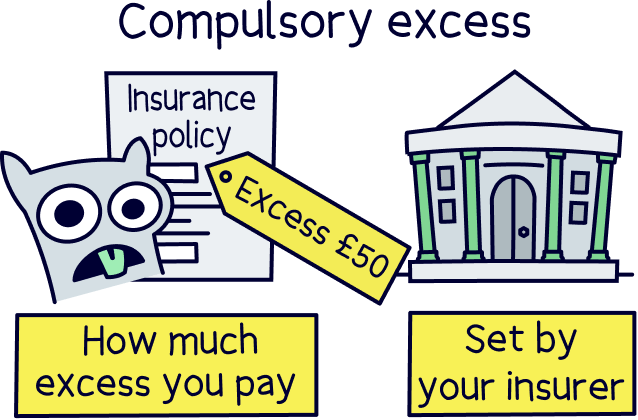

Compulsory excess is the excess set by your insurer, and unfortunately not adjustable. They’ll determine what the compulsory excess is based on you, the insurance you’re after and even different types of claims on the insurance policy (which is the details of the insurance cover).

For instance, if you’ve got travel insurance, you might have a compulsory excess figure of £25 if your items are lost or stolen, but there might be a higher excess, £250, for legal costs if you’re involved in an accident involving someone else or their property (called personal liability cover).

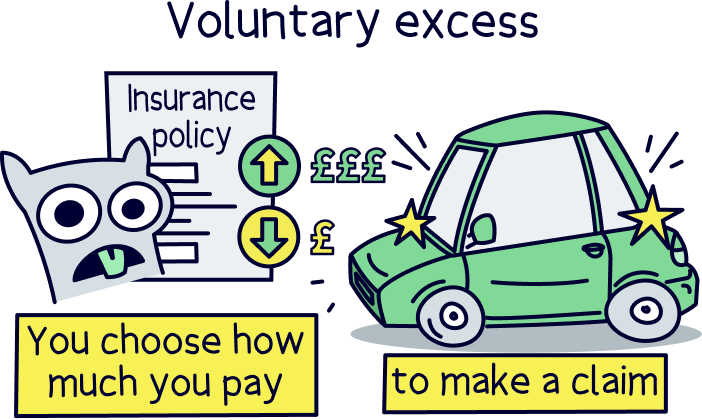

Voluntary excess is a bit different, this is where you actually set the amount of excess (money) you pay. Sounds pretty good right?

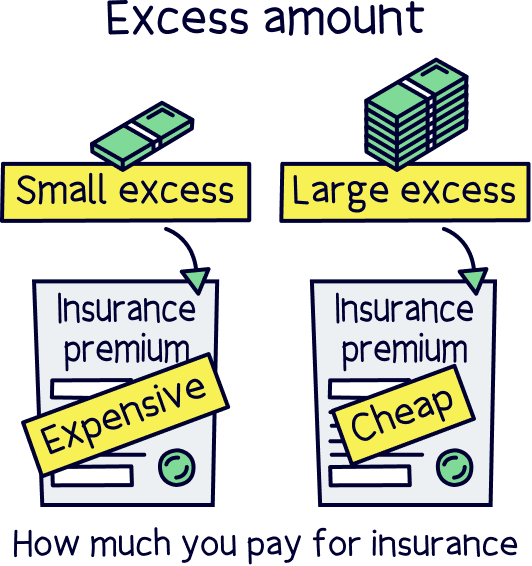

You decide exactly how much you want as the excess, from a cost range set by the insurer. And this will actually change the cost of the insurance itself. Normally, a higher excess will mean a lower insurance cost (called the insurance premium), and a lower excess will mean a higher insurance premium.

This means you can get the balance just right for you and your budget, with a completely personalised insurance policy.

Insurance companies have an excess for two main reasons. The first is to stop you claiming low amounts, which means lots more admin for the insurance company, and they wouldn’t make money. And the second is to deter fraud – you’ll normally lose money yourself if you do claim.

Sometimes, you can also get insurance with no excess, simply called no-excess insurance. This sounds like a great idea, and it definitely can be, but typically means the insurance premium will be higher (sometimes by a lot).

And even though it’s called no-excess insurance, there can still be an excess to pay on the more expensive claims, for instance personal liability cover – which is the legal costs if someone else's property is damaged (e.g. a hotel room) or they get injured in an accident involving you.

You can also get something called an insurance excess waiver (sometimes called excess insurance), and this is where you pay an extra fee when you take out the policy (or sometimes later), and this will ‘waive’ the excess, so you don’t have to pay it, if you ever did make a claim.

It can be a great idea, but ultimately the insurance will cost more, so it’s all down to you and the specific deal as to whether you opt for it or not – although it can be a great idea for travel insurance on bigger trips, and also things like car hire insurance, where the excess can be pretty high.

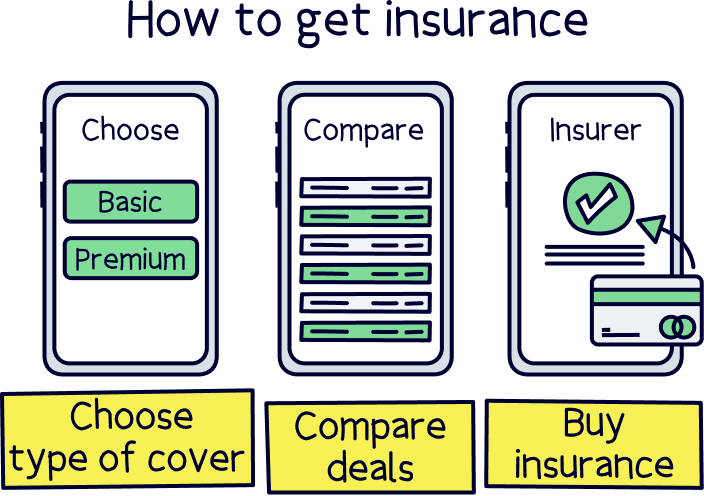

Excess is a bit complicated right? The good news is that finding a great insurance deal can be pretty easy – and that goes for all types of insurance (e.g. car insurance and travel insurance).

In fact, it can take just 10 minutes, and you can be covered straight away. The best way to find the right insurance deal for you is to use an insurance comparison site, such as Confused.com¹.

Once you’re on the site, simply fill out your details, and answer the questions about the type of insurance you’re looking for (e.g. the type of car you drive). They’ll then compare insurance from a wide range of insurance companies, and narrow it down to the best deals for you – it only takes a few seconds too.

Then from the shortlist, simply pick the best one for you (normally the cheapest). You’ll normally be taken to the insurance company’s website, with all your details pre-filled, and all that’s left to do is have a check over of your details and buy the insurance. Job done!

Nuts About Money tip: if you’re heading on holiday and looking for travel insurance, we’ve got a great guide on how to get travel insurance.

We hope that’s made excess and compulsory excess a bit easier to understand. Insurance can be a pretty complicated topic. As a recap, compulsory excess is part of the total excess that the insurance provider sets – and unfortunately you can’t change this.

However you can change the voluntary excess (within a range), and this will make your insurance premium (the cost of your insurance), cheaper or more expensive, depending on if you increase or decrease the excess. So you can get the right balance between the insurance cost, and the excess you might end up paying on a successful claim.

And that’s all there is to it.

Head over to Confused.com to find the best deal for you. They search almost every deal out there.

Head over to Confused.com to find the best deal for you. They search almost every deal out there.

Head over to Confused.com to find the best deal for you. They search almost every deal out there.

Head over to Confused.com to find the best deal for you. They search almost every deal out there.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible

Head over to Confused.com to find the best deal for you. They search almost every deal out there.