Article contents

Saving early in the tax year gives you the benefit of compounding your money more over time, as the money you make, makes more money too. There’s also psychological benefits, such as a quiet confidence you’re already making use of your ISA early, and you may end up saving a whole load more over the year.

Saving into an ISA for your future? Good decision. Find yourself panicking in March or early April every year when the tax year deadline (5th April) comes round again and you want to add money? You’re not alone.

There could be a better way of saving, resulting in some great benefits, both financially and psychologically. Read on to learn more.

Did you know a huge chunk of money deposited into ISAs is in March and the first few days of April (much more than the rest of the year). Funny isn’t it? We all need a deadline sometimes to take action.

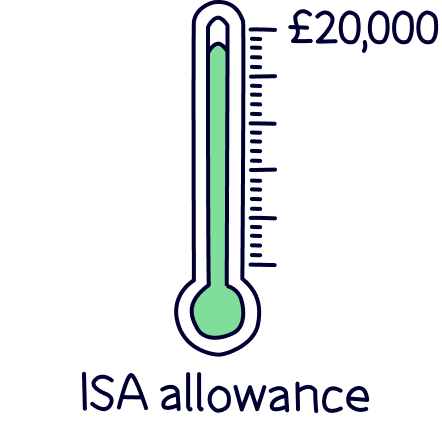

Well, instead of leaving it to the last minute, have you considered adding to your ISA as soon as the new tax year starts? If there’s any spare cash that is. And we don’t mean find £20,000 sitting under your sofa in April (unless you do have it lying around), we mean adding as much as you can afford early, rather than waiting until the last minute.

Check out Lightyear, it’s super low cost, has a great mobile app, and a great range of investments. They always have a great interest rate with their Cash ISA too.

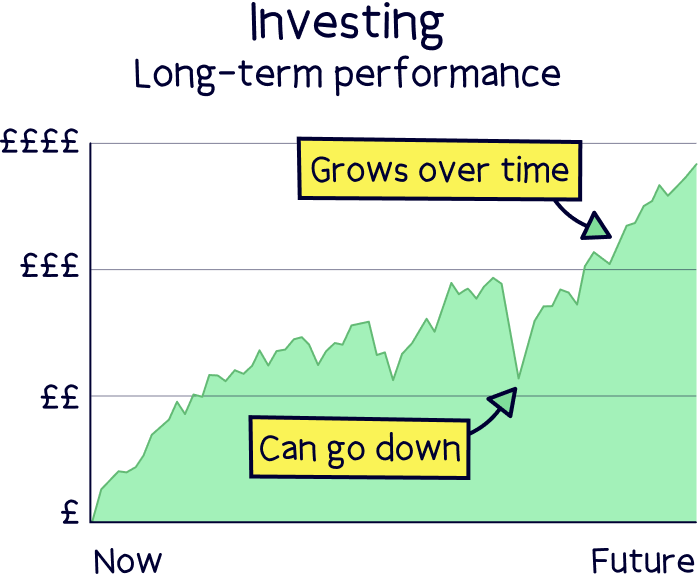

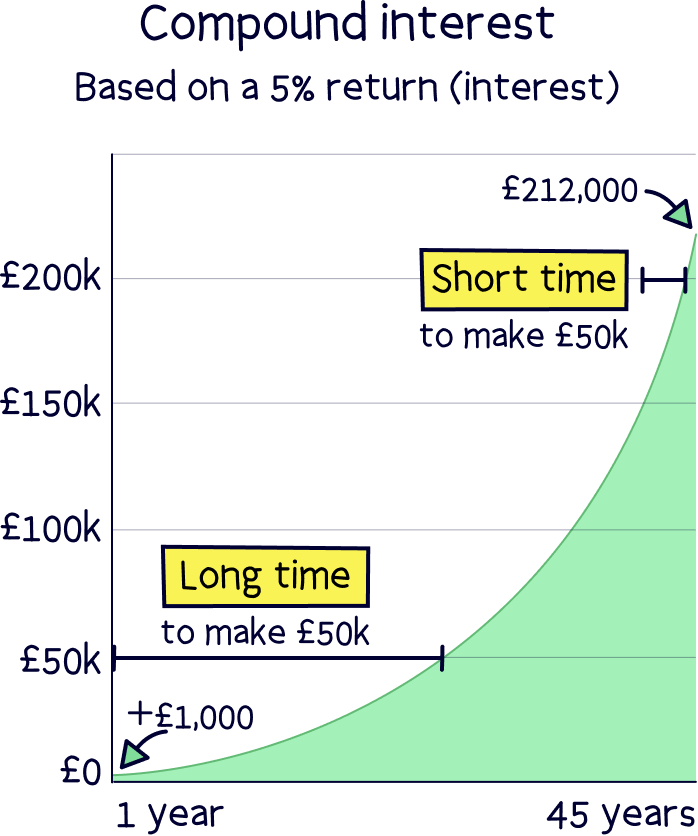

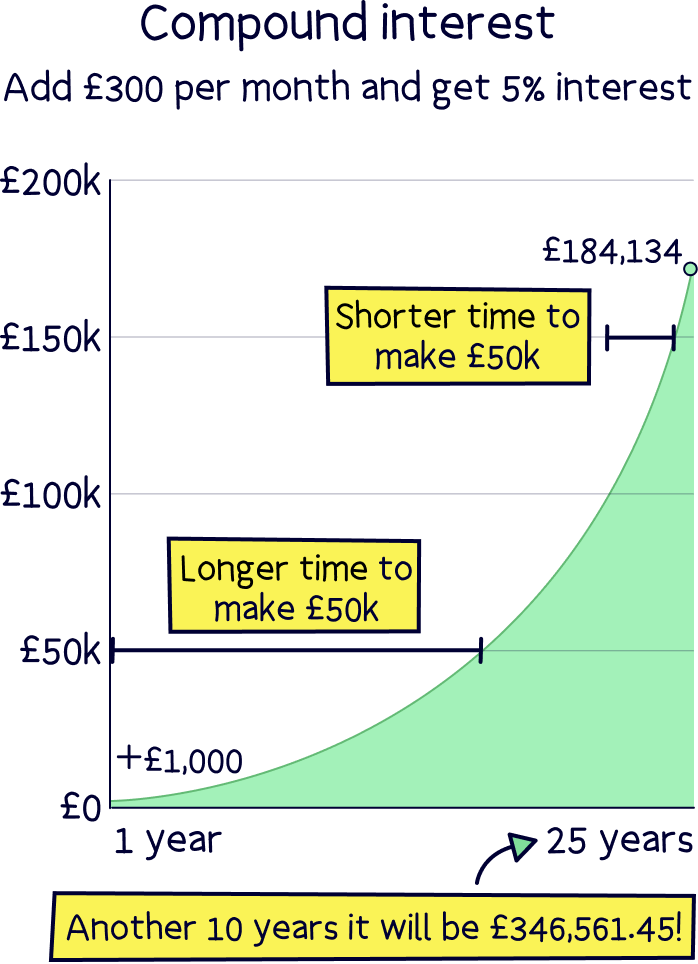

There are multiple benefits to this. The first is that you’ll benefit more from compound interest over time. This is where the money you earn, also earns interest, which snowballs over and over. In terms of investing, that still applies, as the value of your investments increase on average with compounding too. This is based on a historical long term investment strategy, and investments can both rise and fall.

This might seem like a small benefit initially, but over many years, this could grow to be worth £1,000s extra, even £10,000s. Getting your money invested as early as possible can make a huge difference.

Top investors often give the advice ‘time in the market beats timing the market’. A great saying to think about, and saving early puts you a full year ahead.

The second benefit is more psychological, if you do manage to add £20,000, or as much as possible, you feel like you’ve completed the ISA challenge for the year already. This is a great feeling and not to be underestimated.

There will be lots of things happening in the year, and lots of goals to achieve, but knowing you’ve already achieved a big one of filling up your ISA to as much as you can is a huge deal that will sit with you all year. Some might call it being smug, we’re happy with that.

The third benefit is that you’ll know you have actually added money to your ISA. Lots of people have good intentions, but never actually get round to adding to their savings (March panic anyone?).

Life gets in the way, and if money is in a current account or in a cash account that’s easy to access, it gets spent, and often quickly. By prioritising your ISA early, you’ll be guaranteed to have that money working for you, and not spent on clothes or meals out. You might be surprised how easily you get by without dipping into your savings when it’s tucked away somewhere less accessible.

Finally, you’ll be inspired to save even more money than you normally would. We’re not joking here, but if you’ve put away a nice sum of money in April, in the following 11 months you might find yourself with spare cash to save. For some people it becomes a fun game to squirrel away as much as possible and dream of quitting your job earlier. You might see £20,000 as a target to reach for the year (or one much lower), or you might have already used your allowance in April (well done if so).

If you have used your allowance for the year (£20,000), don’t just stop saving! You can still save and invest, it just won’t be in an ISA. There’s 2 other main accounts you can choose, either a general investment account (GIA), or a pension. As we’re talking about lifetime savings, rather than retirement savings we won’t go into pensions right now (but they have some great benefits).

Check out Lightyear, it’s super low cost, has a great mobile app, and a great range of investments. They always have a great interest rate with their Cash ISA too.

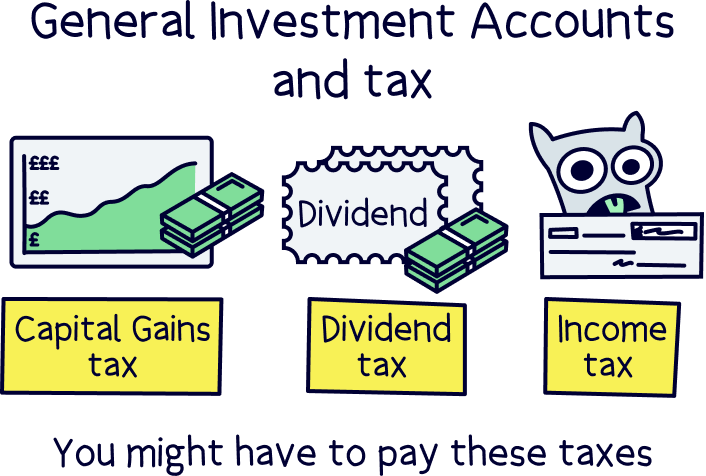

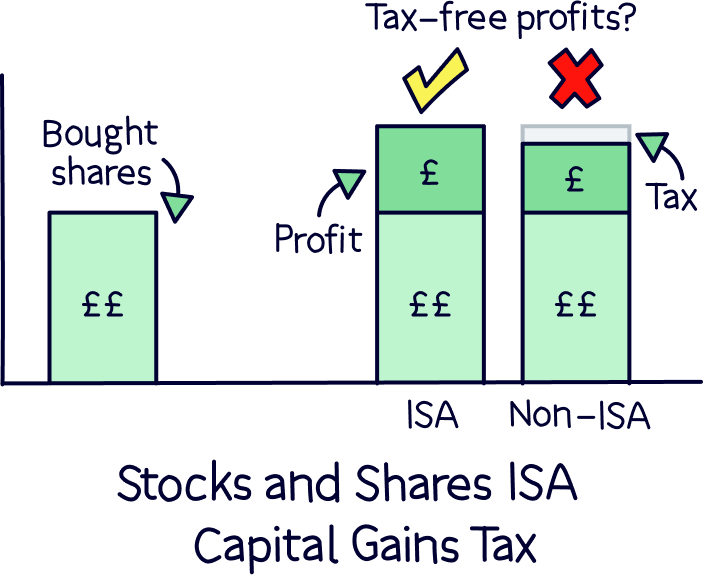

A general investment account is where you can invest, just the same as an ISA, but the money you make will be taxable. Don’t let this put you off, you are only paying tax on the money you make, so you’re still banking a profit even if you do pay tax.

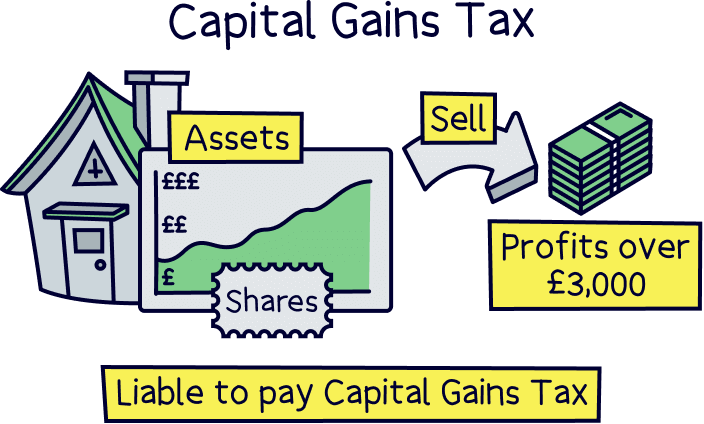

You won’t be paying tax on everything you make either, you get an allowance of £3,000 that you can make, in profit, each tax year (this can change over time), called your Capital Gains Tax allowance. Anything under this is completely free of tax. Do bear in mind that tax treatment depends on individual circumstances and that different taxes can apply depending on which investments you hold.

This is also why there’s lots of trading activity in March and April, and lots of people sell their investments to book in their profits to avoid or reduce tax, and then rebuy again later.

It’s completely legal to do this in the right way, and a large number of people sell their investments in a GIA in March and then add this money into their ISA in April. This uses their Capital Gains Tax allowance for the current tax year, so reduces tax, and then makes use of the ISA going forward in the next tax year.

The cycle then repeats again, adding money to their GIA throughout the year as they have already filled up their ISA.

If the GIA balance is already large, you might do this all in one go on April 6th or shortly after (the new tax year), selling £20,000 worth of assets in your GIA, and immediately buying them again within the ISA. This is called ‘bed and ISA’.

Okay, convinced about saving earlier now? Give it a try, you might really surprise yourself how much you can put away when the focus is at the start of the tax year rather than the end, and you get the benefit of compound interest to grow your money larger over time.

So how do you actually invest then, and where? And what ISA to use? There’s a huge range of options these days. Here’s our top pick…

Check out Lightyear, it’s super low cost, has a great mobile app, and a great range of investments. They always have a great interest rate with their Cash ISA too.

£10-£100 fractional share

Lightyear is a slick investment app that's easy to use, has a decent range of investments and low cost (commission-free). It also offers one of the best rates for saving cash. You’re able to store and trade in multiple currencies, and businesses can open accounts too.

ETFs and shares are completely free of any commission. You’ll only pay currency conversion fees when buying foreign stocks (e.g. US stocks), and it’s a very low fee (0.10%). And, this applies to both a Stocks and Shares ISA and a General Investment Account (GIA), making it one of the lowest options out there.

If you’re new to trading and investing, it’s a great place to start and learn. It’s easy to use, and you’ll be able to buy the shares you’re after in no time. Plus, there’s a good amount of analysis for each stock too – so you’ll learn as you trade, and find new opportunities too.

The range of investments is good for stocks and ETFs, and includes options from across the world.

In the UK, we’re very lucky to have ISAs, they don’t exist in every country, and getting the benefit of tax-free saving is huge, especially in these current days of enormous tax rates. Focusing on getting more money into your ISA as soon as you can will seriously benefit your future - and in more ways than one.

Your money invested (or even saved) earlier means a larger impact from compound interest over time (the money you make, itself making more money). Aside from financially, the psychological benefits of adding money are huge too…

You’ll benefit from that smugness, and pride, that you’ve already nailed your savings for the year. You’ll be glowing inside. But don’t stop there, you’ll find yourself motivated to keep saving throughout the year too, so you might find yourself saving a huge deal more than you otherwise would have by leaving it to the last minute in March.

Instead of cash sitting in your current account, or a low rate savings account with your high street bank, getting it into your ISA (and invested) reduces the potential that you’ll spend it too - so it’s a bit like a double win. You spend less, and you are inclined to save more. You probably won’t even notice you’ve got a little bit less cash to spend.

Based on historical performance, over time, you’ll also make significantly more than a savings account. There are ups and downs, and investing accounts act differently to a savings account, such as your money being safeguarded differently, but don’t let any of that put you off. With a sensible investment strategy, the right investment platform, and time, your future could be very bright. The main thing is getting started!

Make the most of a general investment account (GIA) if you have used up your ISA allowance, you’ll still benefit from investment growth and can invest in a wide range of investments, you just might pay tax on your profits when you sell. Different taxes apply depending on your investments.

At the end of the year, you might be able to reduce or avoid tax by selling investments in your GIA and then moving these to your ISA in the next tax year - you’re now in the realms of top investors, not just making investments for their future, but planning how to best reduce taxes too (which can have a big impact on your money over time). Though remember that tax treatment depends on individual circumstances.

Convinced? Give it a go - you might be surprised about the physiological benefits of saving more. You might even find you enjoy playing the game, and will end up saving a massive amount over the years, potentially changing your life in future, through small habits now.

Not sure where to start? Check out Lightyear¹, they’ve got a commission free ISA and GIA, with one of the lowest FX fees around, a great mobile app, and a good range of investment options. Fees within investments can apply, and your capital is at risk when investing as the value of your investments can go down as well as up.

Check out Lightyear, it’s super low cost, has a great mobile app, and a great range of investments. They always have a great interest rate with their Cash ISA too.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out Lightyear, it’s super low cost, has a great mobile app, and a great range of investments. They always have a great interest rate with their Cash ISA too.