Article contents

To pay tax or not to pay tax? Easy choice! It’s far better to save your money in an ISA, and specifically a Stocks & Shares ISA for longer term savings, and a Cash ISA for short term savings.

So you’re thinking about saving your money. Great idea! There’s a lot to get your head around, and lots of different types of savings accounts that have different benefits, so you’ll want to find one that suits you. And that’s what we’re here for!

Along with the ‘normal’ savings accounts that you might find at your bank or building society, you also have a choice of ISAs – a.k.a. Individual Savings Accounts.

An ISA is a bit different to a normal savings account, and they’ve got much more benefits which will typically grow your savings a lot more over time. This article will explain, simply, everything you need to know and your best savings option.

So, ISA vs savings accounts, what's the difference?

A savings account is basically a piggy-bank that expands. It holds your money. And because your savings generate interest, it makes you money too!

But how does your money increase?

When you open a savings account, you can earn money from the amount you save – called interest. Different accounts offer different interest rates (that’s the percentage of your money that you earn from your savings.)

But don’t just choose the savings account with the highest interest rate. Have a look at the type of savings account too:

Each year you get a Personal Savings Allowance from the government, which means some or all of the interest you make in a normal savings account (not an ISA) is tax-free! Here’s how much you’ll get:

Let’s use an example to explain how it works. Imagine you have £20,000 in savings, and you have a savings account with 3% interest – you’d earn £600 in interest per year.

If you were a basic rate taxpayer, all of your interest would be tax free as it’s under your £1,000 Personal Savings Allowance.

If you were a higher rate taxpayer, you’d have to pay tax on £100 of your interest, as you’d be earning £600 in interest, but your Personal Savings Allowance is £500 (£600 - £500 = £100).

And if you were an additional rate taxpayer, you’d pay tax on all of your savings. Isn’t it tough at the top?!

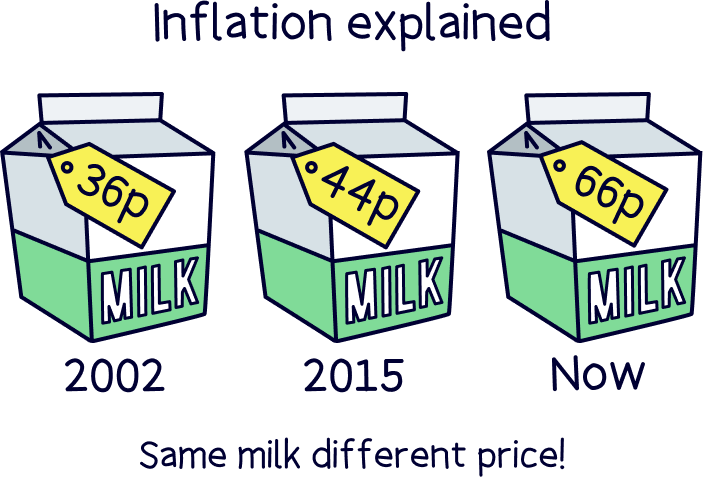

One important thing to know when you’re saving is inflation. Inflation is the rising costs of goods and services of everyday things such as food and energy bills. And it’s currently very high!

Here’s an example: in the year 2002, a pint of milk cost 36p, and now the same pint of milk cost 66p – nearly double! That’s inflation at work.

Inflation is outpacing interest rates on savings accounts. What this means is that when you have an inflation rate of 6% (which it has been in 2022), but an interest rate of 1%, the ‘buying power’ of your cash is reducing, by around 5% per year (6% - 1% = 5%).

Which means your money can roughly buy 5% less things this time next year. That’s quite a big deal – your hard earned money is losing value, fast!

So, how do you beat inflation?

The best way to beat inflation is to save your money within certain types of ISAs.

Let’s dive into what they are and how it works.

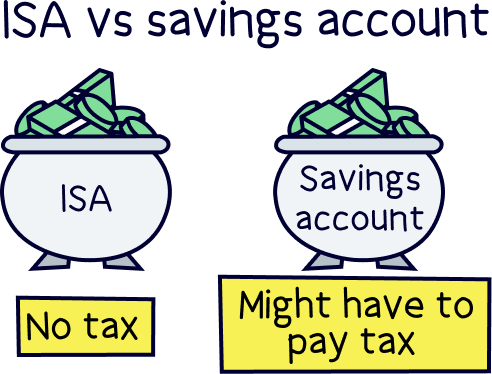

An ISA is a type of savings account with one major benefit: you can save and grow your money completely tax-free!

There are five types of ISAs—Cash ISAs, Stocks and Shares ISAs, Lifetime ISAs, Innovative Finance ISAs, and Junior ISAs.

Cash ISAs are pretty similar to savings accounts. You can get easy-access Cash ISAs or fixed-rate Cash ISAs that lock your savings away for a certain period of time (1-5 years). Just like a savings account, usually, the longer the term, the higher the interest rate.

Stocks & Shares ISAs give you the opportunity to invest your money in successful and growing companies by buying shares in the companies themselves (shares are small bits of ownership). They’re significantly more fruitful than Cash ISAs, because your money grows when your investments do well.

As a rule of thumb, you could expect around an 8% per year increase on average. Which means that if you put away £10,000 at 8% growth, on average you’d make £800 per year.

The best bit is you don’t even have to lift a finger. Experts handle everything for you. Just sit back, relax and watch your money grow.

An Innovative Finance ISA is somewhat similar to a Stocks and Shares ISA, but you do something called ‘peer-to-peer’ lending instead. This is where you lend money via your ISA to companies or people who need it. You get more money back because the people who borrow it pay interest on the loan.

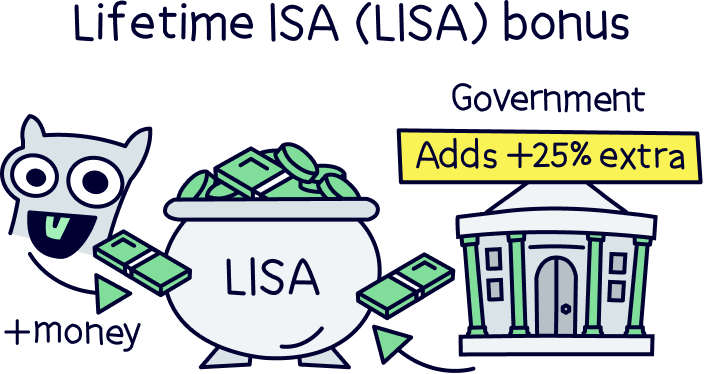

Lifetime ISAs are designed for you to save for your first home or for later in life. You can save up to £4,000 every tax year (from 6th April to 5th April) and the government will top it up by 25%.

So, if you manage to save that £4,000, you get £1,000 extra! Amazing. And, these can either be a Stocks & Shares Lifetime ISA or a Cash Lifetime ISA, which act in the same way as their ‘normal’ version.

The downside is that you have to pay 25% to withdraw your money if you don’t use it for your first home or before you’re 60. So make sure you don’t need the money for anything else.

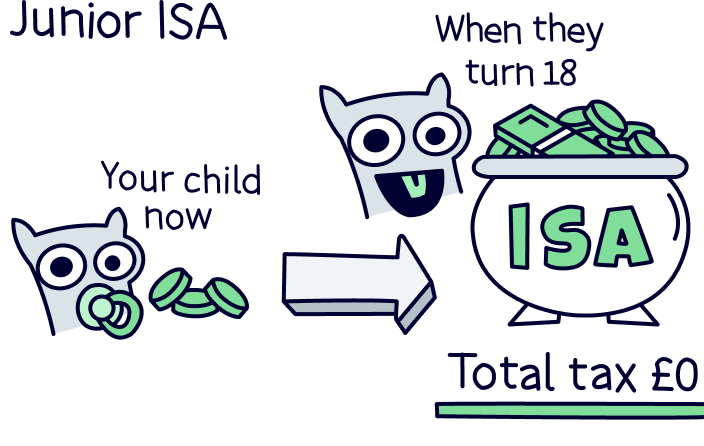

Junior ISAs are designed for you to save money for your kids' future. You can get a Cash Junior ISA or a Stocks and Shares Junior ISA, and add up to £9,000 per year per child. This will then become their money and they can do what they want with it when they turn 18.

The biggest benefit? You guessed it – no tax! And that goes for all types of ISAs.

The government gives you an ISA allowance of £20,000 every tax year. (The tax year runs from 6th April to 5th April.) This means you can save £20,000 every year across all of your ISAs – except if you have a Junior ISA, which has a separate allowance of £9,000.

So, put simply: you can spread your allowance across your Cash ISA, Stocks and Shares ISA, Innovative Finance ISA, and Lifetime ISA. Everything you earn on the money you save or invest is totally tax-free. ISAs are the only savings accounts that offer this benefit.

You can earn a lot from certain types of ISA. Namely a Stocks and Shares ISA and a Lifetime ISA, which will likely outpace inflation and grow your money much more than a savings account.

And the best bit, you don’t even have to do anything! Experts can handle everything for you.

A Stocks & Shares ISA is your best option for long-term savings. It's simple and easy to get started.

If you’re thinking about growing your money over the long-term, a Stocks and Shares ISA is a must-do, and your best option.

You’ll make lots more money over time than a savings account or a Cash ISA.

With a Stocks & Share ISA, instead of earning interest each year, like a savings account, your money grows based on how well businesses are doing, such as increasing sales, and therefore becoming more valuable.

This works because your money buys shares in these companies – bought on the stock market (a place to buy and sell shares), and these shares represent ownership of those companies, meaning when you own shares, you own part of the company.

And when these companies grow in value, so does the value of their shares! And there’s no limit to how big a company can grow, or how many companies your money can be invested in.

The best bit, you don’t need to do any of this yourself. You can simply open a Stocks & Shares ISA and the experts will handle everything for you. They’ll know which shares to buy and which investments to make, all while using the safest investment strategies.

This is why over time you can make a lot more money than a savings account – your money is linked to businesses and essentially the economy as a whole, which tends to grow over time. Rather than a set interest rate that's below inflation, where your money would actually be losing value over time.

Learn more about Stocks & Shares ISA, and how to get started with our guide to investing for beginners (UK).

Currently, most savings accounts have insanely low interest rates, meaning you’re actually losing money over time as inflation (the cost of goods and services) increases – your cash balance won’t go down, but what you can buy with your cash goes down, so over time your money can buy less things.

Cash ISAs have the same issue, as they are effectively a savings account, but with tax-free benefits.

Stocks and Shares ISAs stand high above the rest in terms of the money you can make. And this is your best option when it comes to long term saving. If you’re ready to get saving, learn more about Stocks & Shares ISAs and the best investment apps in the UK.

Here’s a quick recap:

Note: Stocks & Shares Lifetime ISAs are also awesome—that sweet 25% top-up from the government. But they’re only useful if you’re saving for your first home or later in life.

Happy saving!

A Stocks & Shares ISA is your best option for long-term savings. It's simple and easy to get started.

A Stocks & Shares ISA is your best option for long-term savings. It's simple and easy to get started.

A Stocks & Shares ISA is your best option for long-term savings. It's simple and easy to get started.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

A Stocks & Shares ISA is your best option for long-term savings. It's simple and easy to get started.