Article contents

Investing your company’s spare cash is a great idea to increase your profit in the long-term. That’s providing you don’t need the cash and can’t invest it in the business itself. Here's all our top picks for investing with a business account.

Is business booming and you’ve got lots of spare cash you want to invest and make even more money? Or perhaps you want to invest through a limited company rather than investing personally in your own name. It’s a good idea, let’s look at the pros and cons and which are the best share dealing accounts for limited companies.

Get up to £100 free share

Lightyear is a great, low cost investing and stock trading platform. There’s a good range of investment options (over 3,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

There's no account fees and no trading fees. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

Company accounts: you can also invest as a business (e.g. limited company), and benefit from all the same low fees and great experience. Just select 'business' in the top of their website after you click through.

A corporate share dealing account, or sometimes called a business share dealing account, is great for a company with lots of spare cash but can’t invest in their own business to grow the business further.

When excess cash begins to pile up in the business bank account it could be invested in the stock market for the potential to make a much larger return than the little bit of interest it makes from just sitting there in the bank account.

It’s a great position to be in, so congratulations on building a successful business that generates lots of profit and positive cash flow!

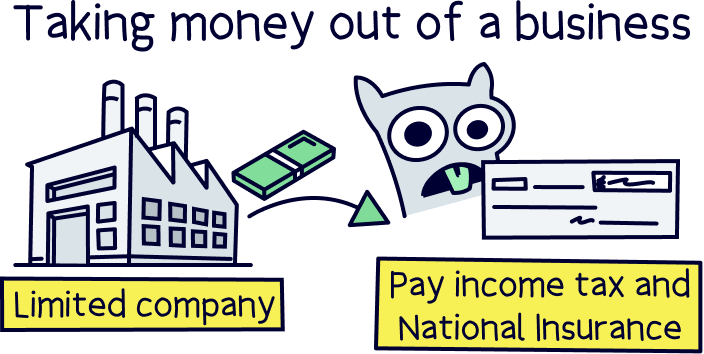

You might be thinking, why don’t I take the money out of the business and invest the money personally? It’s a great question, and you can definitely do that!

The drawback is you’ll have to pay income tax if you take the money out as a salary, and then pay National Insurance Contributions too, both as an employer and an employee.

If you take money out of your business as dividends (which is giving your profits back to the owners of the business), you have an allowance of £500 where no tax is paid, but then you’ll have to pay income tax on the rest (that’s a tax on your earnings, that everyone pays).

So effectively, you’ll be paying at least 20% of whatever you take out of the business in tax (the basic rate level of tax). That’s presuming you are already paying yourself a salary, and so have used up your personal allowance (that’s the bit where you don’t need to pay tax, currently £12,570).

If you begin paying yourself over £50,270, you’ll have to pay 40% tax (higher rate tax), and over £125,140, it’s 45% (additional rate tax). That’s quite a lot of your profit gone on tax if so!

To avoid paying income tax, at least immediately, you can invest your company’s profits before you have to pay income tax yourself – which can mean your money grows much faster, thanks to compound interest – that’s when the money you make, begins making you money too. So that 20% tax (or even 40/45%) can have a big impact.

Your business would still pay Corporation Tax, which is a tax on profits, and 19% - 25%

When you take money out of the business (and pay tax), and then invest in your own name, it’s a good idea to invest using a Stocks and Shares ISA – an account where everything you make is tax-free! (an ISA stands for Individual Savings Account).

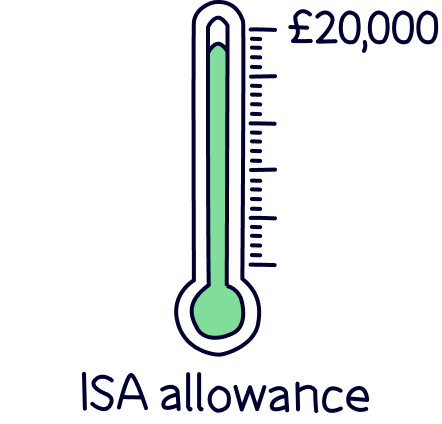

However, you might have saved as much as you are allowed each year into your ISA (your £20,000 ISA allowance). And so, if you wanted to invest more than this, you’d have to invest inside a General Investment Account (GIA). This means you’d be liable to pay Capital Gains Tax, which is 18% or 24% depending on how much you earn, if you made a profit of over £3,000 within a tax year (April 6th to April 5th) from your investments (when you sell the investments).

Keeping cash inside your limited company would mean you can avoid paying Capital Gains Tax yourself in the future. Although it’s often a good idea to use your Stocks & Shares ISA first, as you won’t be paying Capital Gains Tax anyway.

If you're keen to invest in your own name, here's the best share dealing accounts in the UK.

Investing in your own pension is a great idea – you’ll benefit from tax-free saving when you add money into your pension, and benefit from not paying Capital Gains Tax when your pension grows.

If you’re self-employed as a company director (the owner of a company), you’ll have to arrange your own pension, rather than your employer arranging this for you if you were employed.

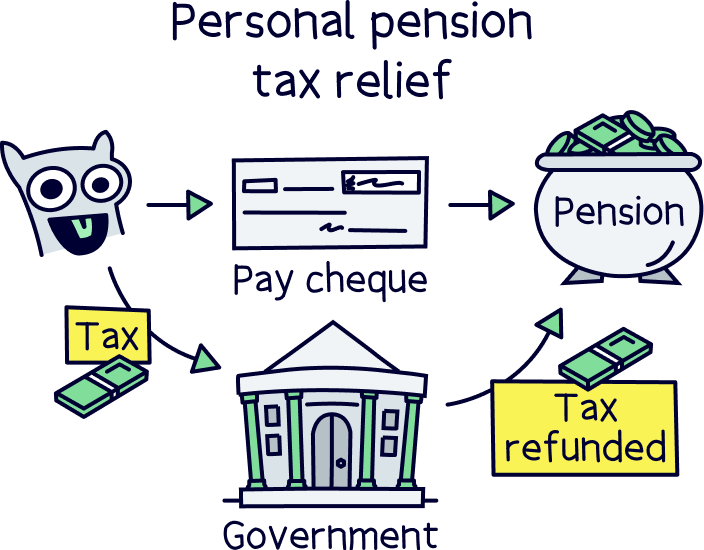

Everytime you contribute money to your pension, the government will top it up by 25% (which is effectively a refund of the amount of income tax you’ve paid). And if you are a higher rate tax payer, or additional rate taxpayer, you can claim the amount back you’ve paid at those rates on your Self Assessment tax return (it’s easy to do but if you want help try Taxfix¹, their service is low cost, quick and 5* rated).

Your pension can act exactly the same way as an ISA or a share dealing accounts for limited companies. You just need to open a self-investment personal pension (SIPP) if you want to make your own investment decisions. Or you could even let experts just handle everything for you – such as with PensionBee).

If you haven’t got a pension yet, it’s easy to do, and we’ve got the best private pension providers in the UK, to find the best one for you. You could also check out the best investment platforms UK.

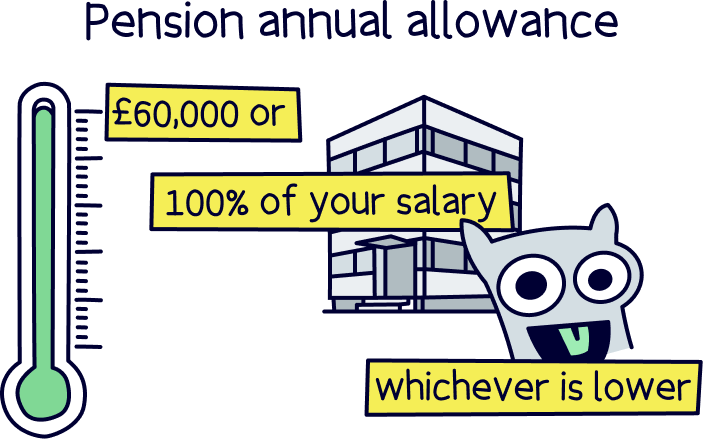

You can invest as much as your earnings into your pension, so a maximum of your salary if you are employed by your business, plus however much you take out of the business for yourself (e.g. dividends). There’s an upper limit of £60,000 however. Well, you can add more, but you’ll have to pay extra taxes, so it’s normally not worth it.

If you haven’t got a pension at all, it’s probably worth considering taking money out of your business and investing the money in your own pension before investing the cash within the business name – the tax-free benefits are pretty great!

When a business begins operating (which is called trading), there are a few options for how the official structure of the business works in law.

The owner could run it entirely in their own name, which is called a sole trader, or if there’s multiple owners that are effectively offering their services rather than trading, like a law firm, they could form a partnership and be recognised legally as such.

Or, the owner(s) could register as an official company – and the company would be recognised legally, rather than the owners themselves. This is called a limited company.

It has the word ‘limited’ in it because it has ‘limited liability’ status, which means that the company, not the owners, is responsible for any financial losses (if the business makes any). In effect, it is completely separate from the owners – in fact, many companies go on to thrive after the person who set it up leaves or retires.

When you want to buy and sell investments with your limited company, you’ll need an LEI number. This is a unique code for your business, which is public, and it’s 20 characters long made up of letters and numbers.

The code contains information about your company’s ownership, such as who owns it – and so makes financial transactions (such as buying investments) completely transparent. It works globally too. You can learn more on the GLEIF website.

To clarify, you’ll need one to make investments, whatever company you decide to use to make investments. Expect to pay around £70 per year if you were to arrange it directly yourself (sometimes investment platforms will do it for you).

It’s pretty straightforward investing with your limited company in a share dealing account – in fact, it’s exactly the same as investing personally. The only difference is you’ll have to jump through a few more hoops when you first get started and open your account (such as getting an LEI number).

As a reminder, scroll up or click top share dealing accounts for limited companies to see our recommendations.

Good luck investing! And if you’re looking for a new investment platform, here’s the best platforms in the UK.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible