Article contents

Yes! You don’t legally need life insurance to get a mortgage. However, it is a good idea as, if you share your home with loved ones, it will help them to pay the mortgage if you pass away.

Keen to buy a home? Wondering if you need life insurance to get a mortgage?

You’re in the right place. Here, we’ll look at everything to do with mortgages and life insurance.

Lots of people think they legally have to get life insurance to get a mortgage. But this simply isn’t true! Contrary to what you might think, you don’t actually need life insurance for a mortgage in the UK.

That said, life insurance is a very good idea, especially when you’re making a big financial commitment like buying a home. We’ll look at why it’s so useful when you have a mortgage in a second. But first, you might be wondering what life insurance even is!

Life insurance is a special kind of insurance that protects your loved ones financially if you die. It’s a bit of a morbid topic, but an important one!

Basically, you pay a set amount of money every month or year (known as your premium). In return, your insurance provider (the organisation that gives you your insurance) agrees to pay your loved ones cash (usually one big lump sum) if you die while you’re covered.

It’s there to make things that little bit easier for your loved ones in what’s sure to be a really distressing time for them. Normally, they’ll use it to cover things that they might otherwise struggle to pay without your income, like household bills, childcare costs or mortgage payments. Which brings us onto…

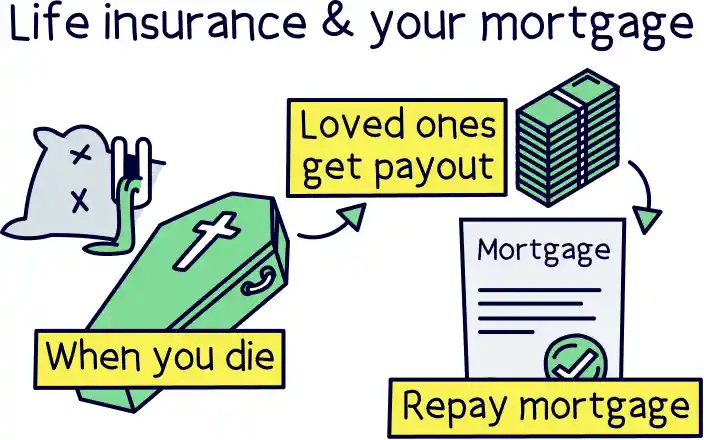

So, what has life insurance actually got to do with mortgages? Well, if you’re sharing your home with other people, like a partner or your family, they might struggle to pay the mortgage by themselves if you died.

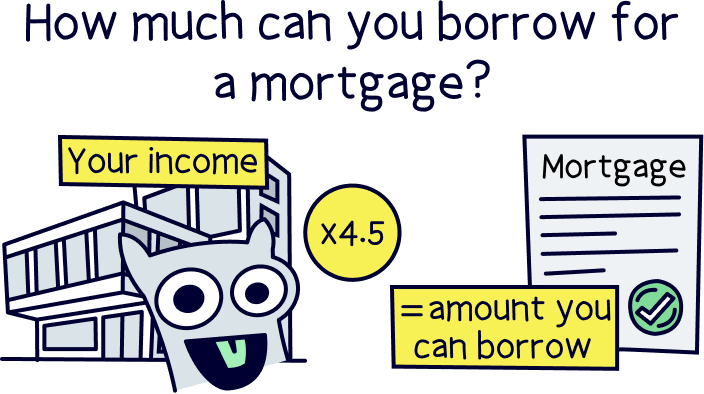

In fact, even if your loved ones felt they could scrape the money together, your mortgage lender may not be happy to transfer the mortgage into their name alone. Normally, lenders will only let you borrow around 4.5 x your yearly income, so if your family’s salary isn’t high enough, your lender might refuse to let them have the mortgage by themselves.

Life insurance means that your loved ones will get a payout when you die, which they can use to pay off the mortgage. That way, they can carry on living at home if you pass away, rather than having to sell the property and move out.

In short, life insurance gives you peace of mind that your loved ones can stay at home if you sadly pass away. Simple!

Some life insurance policies are only designed to contribute towards funeral costs, while others are designed especially for paying off the mortgage (your policy is your insurance agreement, which is essentially a contract). Others still can be used for just about anything your loved ones want.

So, what type of life insurance is best if you want to help your loved ones pay off the mortgage when you’re gone? Here are the main types.

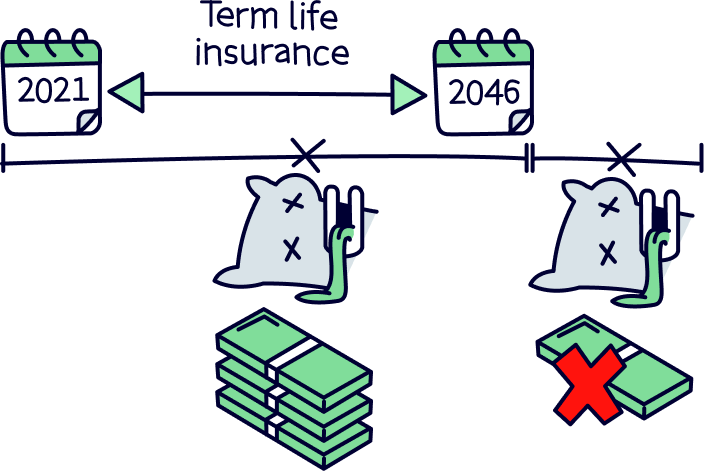

Term life insurance is a life insurance policy that lasts for a set period of time. You can choose how long you want the policy to last for, which is known as your insurance term. For example, you might want to be covered for 5, 10, 25 or even 50 years.

Your loved ones will only get a payout if you die during that time. Just bear in mind that you can’t normally stay covered on a term policy after a certain age (often around 80).

Sounds simple enough, right? However, there are a few different types of term policies.

Any of these types will work if you want to help your family with the mortgage when you’re gone. So, which one should you get?

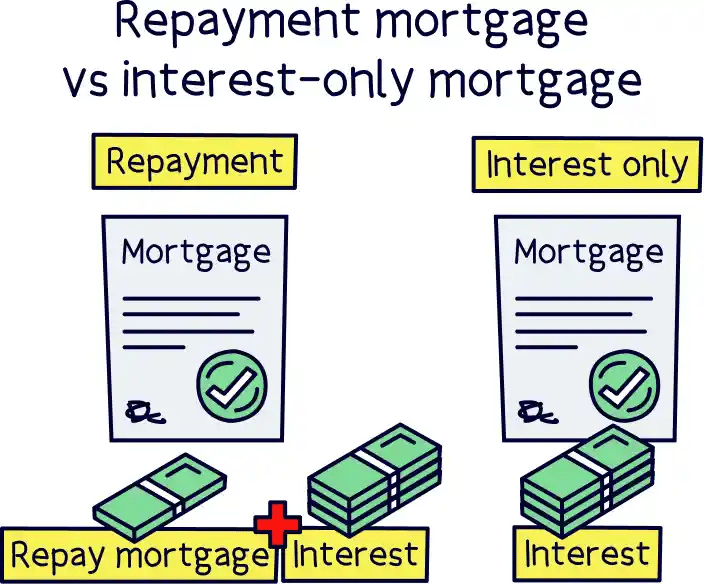

Well, if all you want to help them with is the mortgage, then decreasing term life insurance may be all you need – as long as you’re on a repayment mortgage like most people (one where your monthly repayments are designed to pay off the loan itself as well as the interest).

Normally, these policies are designed so that the payout hits zero at roughly the same time that your mortgage gets paid off completely (although the payout amounts are agreed in advance so even if you pay off the mortgage early, your loved ones will still receive the payout that’s outlined in your policy). Plus, decreasing term life insurance is normally cheaper than other types.

However, don’t forget that your mortgage isn’t the only cost your loved ones might struggle with if you die. The payout might also be handy for them to cover other costs like household bills or childcare. Plus, even if they don’t specifically need the money for anything, an insurance payout can be a great way to provide your loved ones with some security and support when you’re gone – even if you just view it as a gift.

The payouts from other term life insurance policies, like level term or increasing term, won’t decrease with time. So, your loved ones have more chance of ending up with some leftover cash even after the mortgage has been paid off. As far as we’re concerned, that can only be a good thing – but remember, these types of insurance will normally be more expensive!

Whole-of-life insurance, also known as life assurance, is a policy that gives your loved ones a lump payment whenever you die. Remember how we said that term policies only last a set amount of time and they usually won’t cover you past the age of 80? Well, with whole-of-life insurance, you’ll know your loved ones will inevitably get a payout, as your policy won’t run out until your death.

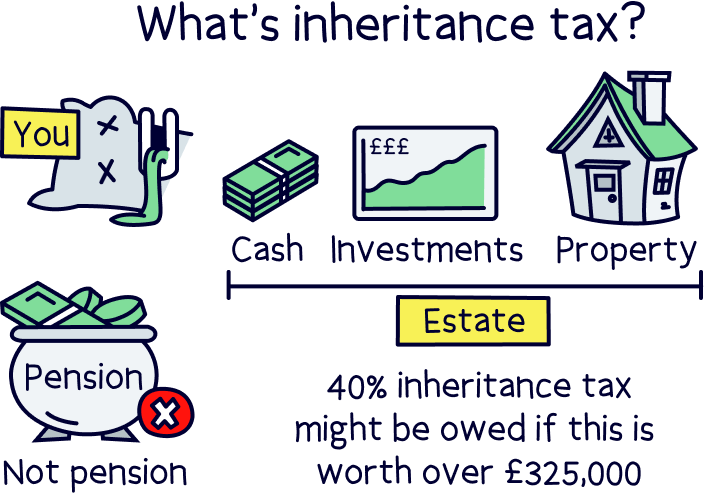

These policies tend to be much more expensive than term policies and they’re also less common. Mostly, they’re used by people who want to contribute towards the cost of their funeral or who want to cover the cost of the inheritance tax bill for their loved ones (that’s a tax that’s charged on the money and belongings of someone who dies).

Anyway, are whole-of-life insurance policies useful for helping your loved ones with the mortgage? Absolutely!

Whole-of-life insurance can offer the most protection out of all the policies as it will guarantee your beneficiaries will eventually get a payout – hence the hefty price tag! Depending on how big you want the payout to be, your loved ones can use it to pay off the mortgage if it’s still outstanding when you die. Or, they can use it for any other purpose they choose.

An over-50s life insurance policy is one that’s guaranteed to accept you if you’re over the age of 50 (although you’ll still need to be under a certain age – normally 80 or 85). Once you have one of these policies, you’ll be covered until you die, as long as you keep up with the payments.

Wondering why you’d need over-50s life insurance instead of just getting a standard life insurance policy? It’s because most insurance providers will decide whether to give you life insurance (and how much to charge you) based on a number of factors including your age and health.

As you get older or you develop health complications, it becomes harder to get life insurance – and more expensive! An over-50s life insurance policy won’t ask you any questions about your health so you’ll know you can get accepted regardless.

That all sounds very good until you realise that these policies tend to be much more expensive than other kinds of life insurance. Not only that, but you’re often not allowed to make a claim in the first 1 or 2 years (making a claim is when you ask your insurance provider to pay out)!

This means that even though you’re covered until you die, you could end up paying in more than what your loved ones get out.

Although your loved ones could theoretically use the payout to pay off the mortgage, the amount of cover you can get will normally be quite low – typically between £1,000 and £25,000. For that reason, these policies are often just used to contribute towards funeral costs. After all, if you have a big mortgage, the payout isn’t likely to stretch very far!

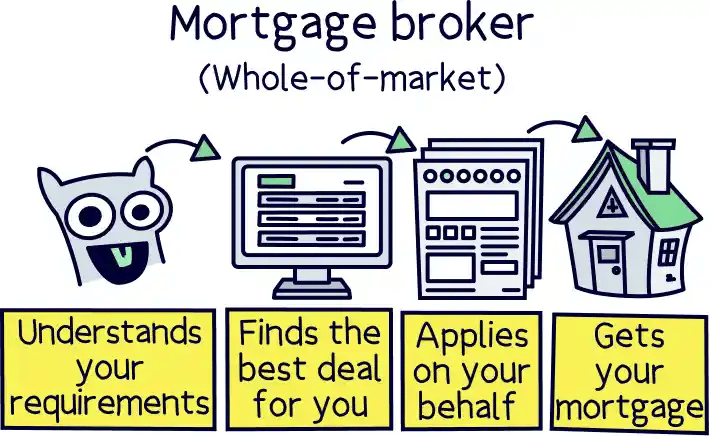

A mortgage broker – also known as a mortgage advisor – is a professional who helps you get a mortgage. They’ll normally save you a ton of time and money as they’ll advise you on the best mortgage lenders and deals for you, and they’ll even sort out your mortgage application. But anyway, we digress!

Some mortgage brokers will also recommend you a life insurance provider, as they’ll know that lots of people who get mortgages will also be looking for life insurance. It can be tempting to just go with the insurance provider they recommend. After all, buying a home is a stressful process and going off a recommendation can make life easier. BUT don’t fall into the trap of blindly opting for the provider recommended by your mortgage broker!

Firstly, you have no obligation to use the provider they recommend. And secondly, you’ll normally be able to save money by comparing insurance deals and providers yourself – your mortgage broker will normally get paid for referring you, so their recommendation will probably be what’s best for their pockets and not necessarily what’s best (or cheapest!) for you.

In a similar vein, if your mortgage broker tells you that you have to get life insurance, this is a red flag and if we were you, we’d find another broker.

If you’re not sure where to start, check out Tembo¹, they've got award-winning service and will guarantee to get you the best mortgage. You'll also get 50% off their fee with Nuts About Money.

Ultimately, we’d recommend finding your own life insurance using a reputable company who searches every insurance deal out there, like Anorak insurance.

Even if you do eventually decide to use your mortgage lender’s recommended provider, it’s worth at least checking what else is out there first as it could save you hundreds of pounds per year.

If your situation is a bit more complex and you want some help, you could also look at using an insurance broker. These are professionals who can help advise you on the best insurance type and deal for you. Just make sure to use one who can compare lots of different insurance providers, rather than just a few – you can find one using the British Insurance Brokers’ Association.

Although life insurance isn’t a legal requirement, we’d strongly recommend it. Life insurance will allow you to make sure that your partner or family can carry on living at home if you sadly pass away before you’ve paid off your mortgage. Even if you don’t have a mortgage to pay, it will give you that peace of mind that your loved ones will be able to get by financially without you around.

Does protecting your loved ones financially sound appealing to you? Then check out our life insurance guide where we break down everything you need to know about it. Or, are you ready to jump straight in? In which case, head over to a comparison site like MoneySuperMarket, Confused.com, Compare the Market or GoCompare to start comparing deals or just use Anorak insurance and they'll sort it all for you. You’ll have that all-important peace of mind before you know it!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.