Article contents

Life insurance is a special kind of insurance that protects your loved ones financially if you die. You pay every month or year and in return, your insurance provider will give your loved ones cash (usually one big payment) after you pass away.

Thinking about what’ll happen if you die probably isn’t at the top of your to-do list. Let’s be honest, there are a million and one more cheerful things you’d rather be thinking about right now. But planning ahead is oh-so-important, especially if you have loved ones who depend on you financially.

Life insurance can give you peace of mind that your loved ones will cope financially if you pass away. Our life insurance guide will answer all your questions about it, from how it works to how much it costs.

Life insurance is a special kind of insurance that protects your loved ones financially if you die.

It’s basically a contract where you agree to pay a set amount of money every month or year. In return, your insurance provider (the organisation that gives you your insurance) agrees to pay a lump sum or regular monthly payments to your loved ones after you pass away.

Normally, your loved ones (known as your beneficiaries) will use the money to cover things like household bills, mortgage payments or childcare costs that they might otherwise struggle to pay without your income. Really, it’s there to ease their financial worries and make what’s always going to be a distressing time that little bit easier.

There are a few different types of life insurance in the UK. Which one you choose will affect lots of different things, like how much money your loved ones will get if you die, how much your insurance costs per month or year (known as your premium) and how long your policy is valid for (your policy is what the contract is called).

Here are the main types.

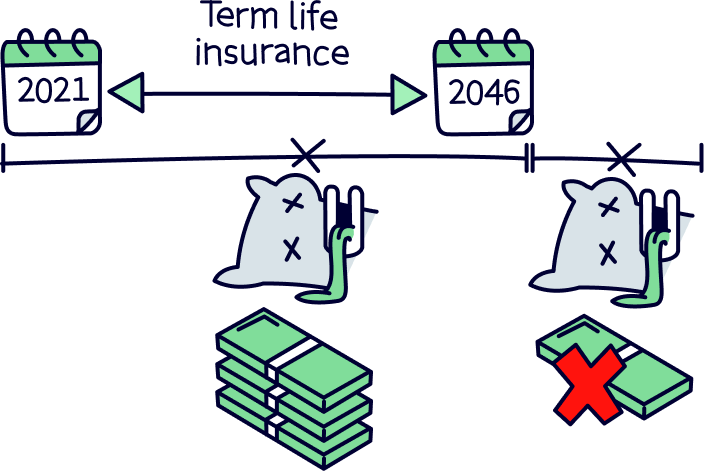

Term insurance is a life insurance policy that lasts for a fixed period of time.

You can choose how long you want your policy to last, known as its ‘term.’ For instance, you might want to be covered for 5, 10 or 25 years. Your insurance provider will only pay out if you die during this time.

Just bear in mind that with a term insurance policy, you can’t normally stay covered past a certain age. This is usually age 80, but it can vary depending on which insurance provider you’re with.

Anyway, there are a few different kinds of term insurance policies…

A life assurance policy, also known as a whole-of-life insurance policy, is one that gives your loved ones a fixed lump sum whenever you die. In other words, while term insurance will only pay out if you die during a certain timeframe, a life assurance policy won’t run out until you die – whenever that may be.

This kind of policy is normally a lot more expensive than a term policy and tends to be a lot less common in the UK. They’re often used by people who want to contribute towards the cost of their funeral, or who want to cover the cost of the inheritance tax bill for their loved ones (inheritance tax is a tax that’s charged on the money or property of someone who dies).

An over-50s life insurance policy is one that’s guaranteed to accept you until you’re a certain age (usually 80 or 85).

Basically, most insurance providers will decide whether to give you life insurance based on lots of different things, including your age and health. That means it can be harder to get a generic life insurance policy as you get older or start to have health complications. On the other hand, an over-50s policy will accept you regardless.

That might sound like a done deal, but watch out. These policies are a lot more expensive and you’re not usually allowed to claim in the first 1 or 2 years after you get one (making a claim is when you ask your insurance provider to pay out). Even though these policies last until you die, you could end up paying in more than what your loved ones get out.

Aside from deciding what type of life insurance you want, you’ll also have to choose whether you want a joint life insurance policy or a single one. A single life insurance policy is one for just you, whereas a joint policy will cover both you and your partner.

So, if you have a partner, which should you choose?

Well, we’d recommend getting 2 single policies rather than 1 joint one. It’s true that a joint policy will normally be cheaper than getting 2 single ones. BUT it will only provide one payout, normally when the first of you dies.

You might think that this wouldn’t be a problem, especially if your partner is your only dependant and vice versa. But if you decide you want your own policy later down the line (perhaps you split up or you have children later), you could end up paying a lot more as your price would be calculated based on your new age and health.

Yes, taking out 2 single policies may be more expensive. But it will mean there’ll be 2 payouts if you both die during the policy terms. Plus, they’ll work independently of one another, so it’s a good way of making sure you stay covered, no matter what happens.

Life insurance quite literally covers your life. In other words, it pays out when you die.

If you have a term life insurance policy, you’ll be covered if you die during your policy’s term (that’s a fancy word for its duration). Or, if you have a whole-of-life policy, it’ll cover you for your whole lifetime, only running out once you’ve passed away.

However, life insurance does not cover any income you lose due to illness – even if you’re terminally ill. It’ll only pay out once you’ve died.

You can get cover for serious illness, known as critical or serious illness cover. This is a popular extra that a lot of insurance providers will encourage you to add to your life insurance and it will cover you if you can’t work due to a serious illness.

However, be warned. A lot of people assume that critical illness insurance will cover you if you get any illness that stops you from working. Sadly, that’s not the case. Your insurance provider will only pay out if you get an illness that’s listed in the policy.

For instance, you might think you’re covered for cancer, but most policies will only pay out if you develop certain types of cancer. Or you might think you’re covered if you lose a leg, but your policy might only pay out if you lose both.

If you want to protect your income, it might be easier to get a normal life insurance policy (like level term cover) and then a separate income protection policy, which protects your income in many different scenarios. Alternatively, if you do want critical illness cover, make sure to read what’s covered really carefully.

If you want to be super safe, you could speak to a financial advisor (a professional who can give you advice). Or, we’d recommend looking into one of the newer insurance providers that are trying to make the world of life insurance a lot more straightforward and easy to understand, like Dead Happy. These companies aim to make it really clear what’s included in critical illness cover (which Dead Happy calls ‘Near Death Insurance!) and it can be pretty cheap. Read our review of Dead Happy to find out more.

Okay, so first things first, you don’t actually need life insurance – by which we mean it’s not a legal requirement. But it’s definitely worth considering as there are tons of life insurance benefits. Things like…

In a nutshell, most people get life insurance to help loved ones who would struggle financially without them around. However, life insurance can also be useful for wealthy people who want to pass money to their loved ones after their death in a tax-efficient way, with the help of a trust. Which bring us onto...

Although your loved ones won’t normally have to pay income or capital gains tax on the payout from your life insurance when you pass, they may well have to pay inheritance tax.

Inheritance tax is a tax that’s charged on your money or property when you die. If everything you own is worth more than £325,000, your heirs (the people that get left your belongings) will need to pay a tax of 40% on anything over that threshold – unless they’re married to you or in a civil partnership with you.

So, let’s say the value of your money and property is over £325,000 when you die. In this case, the money your loved ones receive from your insurance payout will be taxed at a rate of 40%. That means if your life insurance payout is £200,000, your loved ones would receive £120,000 (200,000 minus 40% is 120,000).

That said, inheritance tax can be a bit complicated and if you’re passing everything onto your children, the tax-free threshold will be a bit higher.

Anyway, there’s some good news! Your loved ones can legally avoid having to pay any inheritance tax at all on the insurance payout if you put it ‘in trust.’ A trust is a legal way of storing money for safekeeping for a loved one. It’s essentially a pot of money that’s looked after by people you appoint, known as ‘trustees’ (usually a solicitor or a family friend).

When your money is in a trust, it doesn’t count as part of your estate (that’s what all your belongings grouped together are called). And that means that your loved ones won’t have to pay inheritance tax on it. Happy days! Most insurance providers will be happy to help you put your life insurance in trust for free.

Just be aware that writing your insurance policy in trust is really hard to reverse. So, you’ll need to be absolutely sure you want the payout to go to a particular loved one before you set it up!

You might think that life insurance is just for people who have children, but that’s not the case at all. Anyone can get life insurance and it can be a great (and often cost-effective) way to provide financial support to anyone who relies on you and your income – or anyone who you just fancy helping out with a gift once you’re gone. That could be your parents, children, partner or friends.

That said, it’s not right for everyone. Here are some things you’ll need to consider when you’re working out whether or not to get it.

Do you have anyone relying on your income? Would they struggle financially if you died?

If the answer’s yes to either of these questions, life insurance could be a great shout. It could allow them to do little things, like paying the bills and doing the food shop, that they might otherwise find difficult without your income.

For instance, imagine you and your partner have a joint mortgage on your home. If you were to die unexpectedly, would your partner be earning enough to be able to take on the mortgage by themselves? If not, life insurance could allow your partner to pay off (at least part of) the mortgage so that they can carry on living at home.

On the other hand, if you don’t have any dependants and there’s nobody you’d want the money to go to particularly, there’s probably no point.

Life insurance might sound like something that only older people need, but don’t be fooled. Yes, there’s less chance of passing away while you’re young, but there’s always a risk of developing an illness or being in an accident.

Not only that, but insurance will normally be cheaper the younger (and healthier!) you are. It’s true that you’ll probably need to pay for life insurance over a longer duration if you get it while you’re young, but the yearly or monthly cost will tend to be vastly less.

Some super nice employers offer this lovely thing called death-in-service cover. In a nutshell, it pays out if you die while you’re an employee of that company (don’t worry, your death doesn’t need to be work-related for you to qualify!). Normally, the payout will be around 4 x your salary.

If your employer offers this as an employee benefit, you might think there’s no point in getting your own life insurance on top. And in some ways, you have a point! But remember, if you get made redundant or change jobs, your next employer might not offer it.

If you end up needing your own life insurance later on, you might find it harder to get a good deal as you’ll be older and may even have significant health problems at this point. So, although death-in-service cover is a really lovely benefit, it’s best not to rely on it completely. Instead, we’d recommend simply using it to top up your own life insurance policy.

You should get life insurance as early as possible once you need it.

Firstly, the younger you are when you get life insurance, the cheaper your premiums will normally be (your premium is your monthly or yearly cost). To give you some idea, the average premium for 30 to 39-year-olds on MoneySuperMarket is £21.03 per month. For 50 to 59-year olds, however, that cost leaps up to £34.10 per month.

Plus, as time goes on, there’s more chance that you could be diagnosed with a health condition. Depending on what the health condition is, this could make it hard to get approved for life insurance – and, even if you do find an insurance provider who’s happy to insure you, you’ll usually find that costs are much higher accordingly. This is all because as you get older and start to develop health problems, the chances of you making a claim (and specifically, of making a claim before you’ve made many of your monthly or yearly payments) goes up.

It can be tempting to play down any health problems to try and get a good deal on your insurance, but watch out! If you lie, your insurance provider might refuse to pay out once you’re gone. So, it’s really important that you tell the truth!

By getting life insurance with a long term while you’re still young, you can lock in a low rate that you’ll carry on paying long into the future. For instance, if you’re 30 years old, you could get a level term policy with a 50-year term. This way, you’ll be covered until you’re 80, and your prices will be fixed until then too.

Yes, longer terms tend to cost more than shorter ones. But with a shorter term, you’d need to look for cover again once your policy ended, and would likely face higher prices at this point. By taking out a long-term life insurance policy while you’re young, you’ll benefit from continuous cover and avoid those price hikes (just make sure that you don’t stop paying or pause your cover at any point!).

The average cost of life insurance in the UK is between around £15.85 and £30.40 per month, according to industry research by our friends at Unbiased.

However, how much you pay for life insurance can vary massively based on lots of different things. These include…

Congrats! You now know everything there is to know about life insurance! But there’s just one thing missing… you’ll need to know how to actually go ahead and get it!

If you’re ready and raring to get yourself insured, just follow these simple steps.

First things first, you’ll need to decide how much money you want your loved ones to get if you pass away (known as your policy’s death benefit). The bigger the payout, the more you’ll need to pay on a monthly or yearly basis, but the better off your loved ones will be if you sadly pop your clogs.

When deciding how much you need, make sure to factor in outgoings like your mortgage or rent, food shopping, bills and childcare. One general rule of thumb is to take your yearly salary and multiply it by 10. That way, your loved ones should be able to maintain their current lifestyle for a decent period of time.

However, everyone is different and will have different priorities. For instance, if you have kids, you might want to make sure they’re going to be well provided for until they hit at least the age of 18. Ultimately, it’s a careful balancing act between how much you can afford to pay now each month or year, and how much your loved ones are going to need later when you’re not around anymore.

Most Brits opt for level term insurance, which covers you for a fixed period of time. If you die during this time, your insurance provider will pay out a set lump sum to your beneficiaries.

However, everyone’s different and this may not be the best option for you – as we showed you earlier, there are other types of life insurance too. A decreasing term life insurance policy means the payout your loved ones get will become smaller as you become older, but it’ll usually be cheaper. So it might be a good option if you’re on a limited budget.

At the other end of the scale, a life assurance (or whole-of-life) policy will cost you more now but will remain valid until you die (whenever that may be) as long as you carry on making the payments. So, it could be a great shout if your aim is to contribute towards your funeral costs or to find a tax-efficient way of passing your money onto your family members after your death.

Now that you know what you’re looking for, check the top few comparison sites to get an idea of what insurance policies are available and how much they cost. They’ll let you sort and filter results based on what you’re looking for (including price and life insurance type) to make it really easy to compare quotes.

In an ideal world, we’d recommend using all 4 of the sites below, as not every deal will be on every comparison site. But if you’re in a rush, you could just check the first 1 or 2. We’ve listed them in order of how good we think they are.

Ready to get life insurance to protect your loved ones financially when you’re gone?

Searches most of the leading insurers. Get a quote in just 3 minutes.

Good range of providers, and get Meerkat Meals – discount on takeaways and eating out. Plus an Amazon gift card.

Searches over 13 of the leading providers. Quotes show guaranteed prices.

Searches the top insurers – and get free Bupa Healthy Minds and Wellbeing cover.

Ready to get life insurance to protect your loved ones financially when you’re gone?

There are a few insurance providers that won’t show up on comparison sites at all because they’d rather you went direct to them. It can be a bit annoying, but it’s worth checking direct-only deals as sometimes, they’ll be able to beat the deals you find on comparison sites.

The biggest direct-only provider that we’d recommend checking is Direct Line. They often have good deals available, so head to their website, put your details in and see what they can offer you.

An insurance broker is a professional who specialises in helping people to find the right insurance for them. Most people do without an insurance broker as it’s pretty easy to find good deals on comparison sites or direct with providers. But if your situation is a bit more complex and you want some advice, an insurance broker can help.

Just make sure to go with an independent, whole-of-market insurance broker. These can compare and advise you on deals from lots of different insurance providers, rather than just a select few, so you’ll know you’re getting impartial advice about what’s best for you. You can use Unbiased¹ or the British Insurance Brokers’ Association to find the right insurance broker for your needs.

Finally, once you’ve found a deal you like, spend some time double, triple-checking you’re happy with it. That means reading through the policy carefully to check whether there are any exclusions you didn’t spot before (an exclusion is something that’s not included). And it also means making sure that you actually need any extras your insurance provider has persuaded you to add.

Insurance providers are very skilled at making you feel like you need extra levels of cover, but you don’t want to end up paying more than you have to for cover you don’t need. As we mentioned before, serious or critical illness cover is a common add-on that may not be as great as you initially think.

While it might sound good to be covered in case you get ill and can’t work, these policies generally only cover very specific illnesses, so they’re often not as useful as they look. If you do want to protect yourself and your loved ones against loss of income, a separate income protection policy, which protects your income in lots of different eventualities, might be safer and more straightforward.

Anyway, assuming you’ve checked the terms carefully and are happy, great news! You can simply go ahead and tell your insurance provider when you want the policy to start (or just start it straight away).

Getting life insurance might sound like a chore, but protecting your loved ones financially when you pass is one of the kindest things you can do.

If that sounds appealing, then we’d recommend getting yourself insured sooner rather than later. After all, the earlier you get life insurance, the cheaper it will be – and the sooner you’ll get that all-important peace of mind that things won’t fall apart once you’ve gone.

Ready to get life insurance to protect your loved ones financially when you’re gone?

Ready to get life insurance to protect your loved ones financially when you’re gone?

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible

Ready to get life insurance to protect your loved ones financially when you’re gone?