Article contents

Yes! There’s nothing to stop you from getting multiple life insurance policies. That said, it’s not always the best move. It all depends on your circumstances.

Getting more than 1 life insurance policy might sound like a fantastic idea. After all, the more protection the better, right??

Well, you can get multiple life insurance policies and there are times when it can be a good move. But things are a little more complicated and it’s not always the best course of action. Here’s the full lowdown!

First things first, you can have as many life insurance policies as you want. There’s no rule stopping you!

In case you’re not sure, a life insurance policy is an agreement between you and an insurance provider. It’s basically a contract that lays out how much you have to pay and what you get in return – a bit like a mobile phone contract or an agreement with your energy supplier. Except in this case, instead of 4G or energy, you get financial protection for your family if you die (yep, it’s not the cheeriest of topics!).

You have to pay a set amount of money each month or year for your policy to stay valid. Then, if you die during this time, your insurance provider will give your loved ones cash – usually one big payment. They’ll often use it to cover things they’d otherwise struggle to afford without your income, like household bills, mortgage payments, rent or childcare costs.

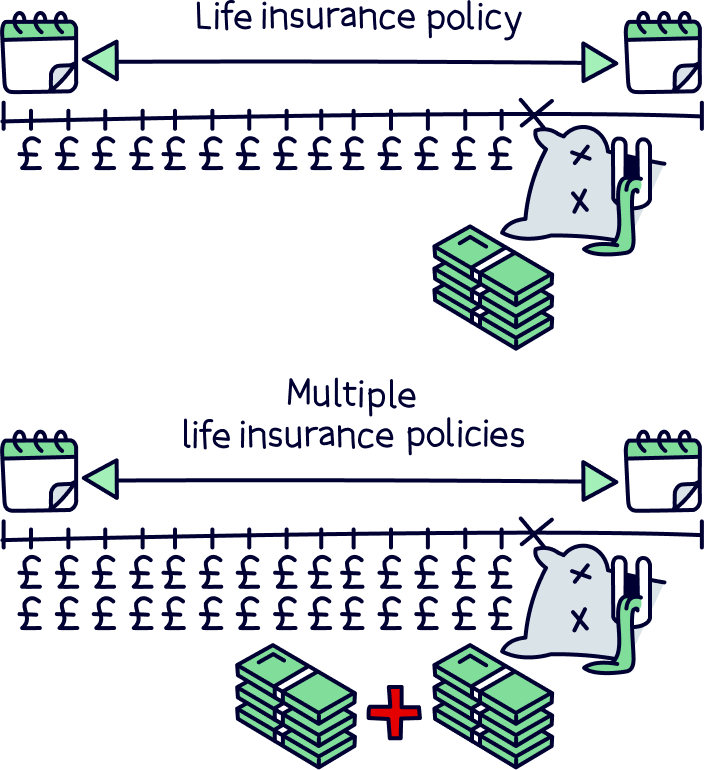

With several life insurance policies, your loved ones will get multiple payouts if you die (as long as your policies are still valid, of course!). But you’ll also have to pay multiple premiums (that’s a fancy word for the monthly or yearly payment you give your insurance provider to stay covered).

There are a few different situations that might have you umming and ahhing about a second (or third or fourth!) life insurance policy. Here are the main ones:

When you get life insurance, you can choose how much cover to get. Your cover is the amount that your loved ones will get paid if you die and is known as your insurance death benefit.

Usually, you’ll work out how much cover you want based on your outgoings – things like your mortgage or rent, food shopping, bills and childcare. A general rule of thumb is to take your salary and multiply it by 10 so that your loved ones will have enough money to last them for a while.

However, if your circumstances change and your outgoings go up (maybe you get a bigger mortgage or you have children) then you might want to get more cover.

Let’s say you’ve already got a life insurance policy with £200,000 of cover but you decide you want to increase it to £400,000. One way of achieving this could be to get a second policy that also has £200,000 worth of cover. Then, with both policies added together, your loved ones would get £400,000 if you died.

There are 2 main groups of life insurance: term policies and whole-of-life policies (also known as life assurance).

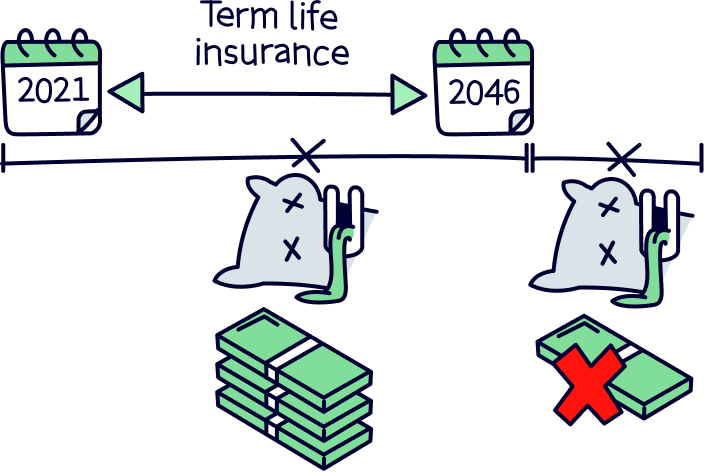

Term policies are ones that only last for a set period of time, known as your term. You can choose how long this is – for instance, you might want to be covered for 5, 10, 25 or even 50 years (although you can’t normally be covered past a certain age, often around 80). Your loved ones will only get a payout if you die during this time.

Term policies are the most popular kind in the UK.

Whole-of-life policies, on the other hand, cover you until you die, whenever that may be. In other words, while term policies run out after a set period of time, whole-of-life policies only end when you pop your clogs. As you can imagine, these are more expensive – your loved ones are guaranteed a payout as you will inevitably die at some point (sorry!).

Anyway, if you want to guarantee your family a payout but you’re on a budget, you could decide to get just a small amount of cover on your whole-of-life policy (maybe just enough to pay for your funeral or to contribute towards the inheritance tax bill for your loved ones). Meanwhile, you could also get a larger term policy so that if you die earlier while you have higher outgoings (such as young kids), your family will get a bigger payout. They could use that payout to cover immediate costs like childcare or uni fees.

Some lovely employers offer an employee benefit called death-in-service cover. This is a kind of life insurance policy that will pay your loved ones if you die while you’re an employee of that company. Usually, the payout will be around 4 x your yearly salary.

This is a great bonus as your loved ones will get a level of financial protection for free. Hooray! However, in this case, we’d always recommend getting your own life insurance policy on top.

Why? Well, firstly, the payout from your employer’s policy might not be high enough to cover your loved ones’ needs. And secondly, what happens if you get made redundant or switch jobs? These policies often can’t be moved elsewhere (and even if yours can, you’ll normally get charged more if you want to move it).

If you end up without life insurance and you need to get cover later in life, you might struggle to get accepted – or, if you do get accepted, you could end up being charged a lot. That’s because when providers are deciding whether they’re happy to give you life insurance (and how much to charge you), they’ll look at your health and age.

As you get older and potentially start to develop health conditions, it can be much harder to get decent life insurance in place, as insurance providers will see you as more likely to make a claim before you’ve had a chance to pay them much. There are policies where you’re guaranteed to get accepted if you’re over a certain age, known as an over-50s policy, but they tend to be very pricey.

By getting your own life insurance policy nice and early (instead of relying on your employer’s death-in-service cover), you’re likely to get accepted and to lock in a nice low rate long-term.

Let’s put it this way: having multiple life insurance policies isn’t necessarily a bad idea and there are definitely scenarios where it makes sense. For example, if you want 2 types of life insurance cover, or you want to supplement your employer’s death-in-service cover, getting a second policy will generally be the only way to do that.

However, if your reason for getting another policy is that your needs have changed (for example, you want to increase your level of cover or you want to extend your insurance term), getting a second life insurance policy often isn’t the best idea. Why? Well, a lot of insurance providers will be happy to let you make changes to your existing policy – and that’ll usually be cheaper than having to pay 2 insurance premiums (the monthly or yearly cost of getting life insurance).

Things that insurance providers will often be happy to change for you include the level of cover, your insurance term, and whether you want to pay monthly or yearly. Just bear in mind that your premiums will normally go up or down depending on what changes you make!

But aside from avoiding 2 premiums, there’s another good reason for adapting your current policy instead of getting a second one. Remember how we said that as you get older or develop health conditions, your life insurance cost will normally go up (or you may even get rejected)?!

If you’re considering a second policy, some time may have passed since you got your first one. Meaning, you may be older and you may well have developed a health condition during that time. If that’s the case, you might struggle to get approved for a second policy (unless you go for an over-50s policy with guaranteed acceptance, but these are very expensive). And, if you do get approved, your premium is likely to be much higher on your second policy than on your first.

On the other hand, you can sometimes make changes to your existing policy without having to give your provider any extra medical information – although it’s important to check your policy documents to see if there are any terms and conditions that apply. So, you could be charged based on the information you gave your provider when you first got your policy, keeping your costs down.

Finally, another drawback of getting multiple life insurance policies is that it could be harder for you to keep track of them all. Don’t get us wrong, you might be super organised in which case this might not be an issue. But if you miss a payment, your insurance policy will become invalid. And that means you’ll have to start all over again, likely facing higher costs (or even struggling to get approved) as time will have passed. Urgh!

If you have a partner, you can get a life insurance policy that covers both of you, known as a joint life insurance policy. Or you can get 2 separate ones, so you each have your own. The choice is yours!

So, which is better?

Well, getting a joint policy will normally be cheaper. But it will only provide 1 payout, usually when the first of you dies. That might not be a problem if you don’t have any other dependants. But if you have kids or elderly parents relying on you, it could cause issues – how would they cope if you both died within a short period of time?

Not only that, but a joint policy gives you a lot less flexibility. Imagine you split up later down the line and you suddenly need your own single life insurance policy. This could be expensive or hard to achieve if time has passed and you’ve developed health problems.

Ultimately, getting 2 life insurance policies as a couple might mean spending a bit more money to start off with, but we think it’s the better way to go. If you both die while you’re covered, your loved ones will get 2 payouts. Plus, your policies will work independently of each other so if your situation changes later down the line, you’ll both have peace of mind that you’re still covered.

Umming and ahhing about whether to get a second (or third or fourth!) life insurance policy? We’d recommend checking with your existing provider to see whether they can simply amend your current life insurance policy first. Or, if you’re after some bespoke advice, why not use an independent insurance broker (a professional whose job it is to help you get the right insurance for your needs)? You can use the British Insurance Brokers’ Association to find one.

Alternatively, if you’ve done your thinking and you’ve decided to get multiple life insurance policies, head over to a comparison site – like MoneySuperMarket, Confused.com, Compare the Market or GoCompare – to start comparing deals. You’ll have that all-important peace of mind that your loved ones are as protected financially as they can be in no time!

Check out our guide to life insurance to learn all about how best to protect your loved ones financially after you pass away.

Check out our guide to life insurance to learn all about how best to protect your loved ones financially after you pass away.

Check out our guide to life insurance to learn all about how best to protect your loved ones financially after you pass away.

Check out our guide to life insurance to learn all about how best to protect your loved ones financially after you pass away.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible