Article contents

If you’re like most people, chances are you’re on something called a ‘term’ life insurance policy. If it runs out before you die, you’ll simply stop paying your monthly or yearly payments and your cover will end. You can take out a new policy, but it will normally be much more expensive!

Life insurance is a special kind of insurance that protects your loved ones financially if you die. In other words, you pay a set amount of money each month or year and in return, your loved ones will get money (usually one big payment) if you die while you’re covered.

But what happens if you don’t die? Well, it’ll all depend on what type of life insurance you have. Here’s the full lowdown.

Imagine you pay for a new bag or jacket, years pass, and you never end up using it. You wouldn’t go back to the store you bought it from to ask for a refund (at least, we hope you wouldn’t!).

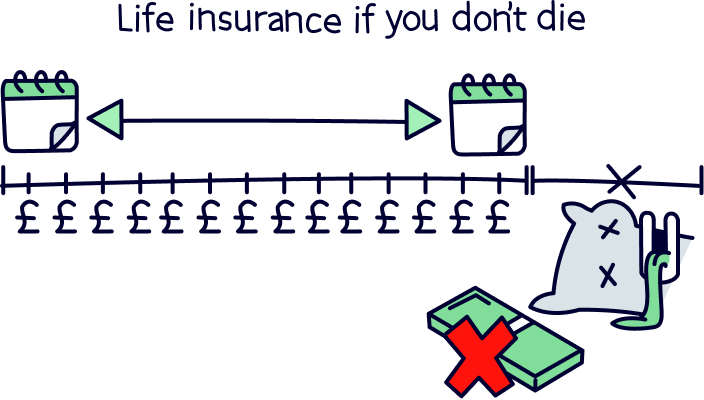

Life insurance normally works the same way. If your policy (a fancy word for your insurance contract) runs out before you die, you don’t get your money back. Instead, you simply stop your monthly or yearly payments (known as your premium) and your loved ones will no longer receive a payout if you die.

However, exactly what happens will depend on what kind of life insurance you have. There are 2 main groups.

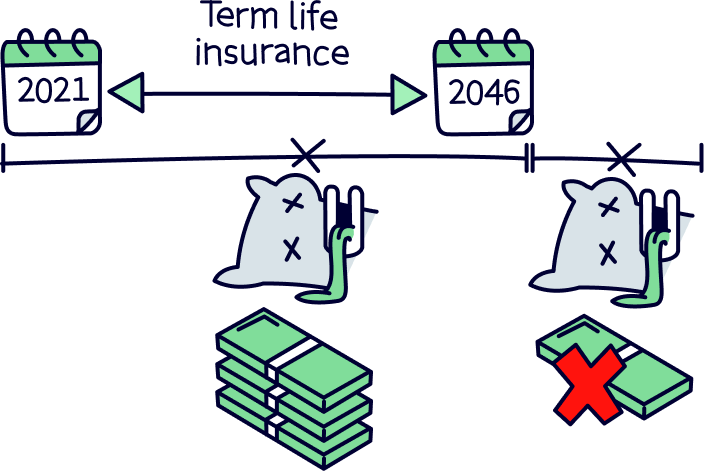

Term life insurance is the most popular kind of life insurance in the UK. It covers you for a set period of time, known as your ‘term.’ You can usually choose exactly how long this is. For instance, you could choose to be covered for 5, 10 or even 40 years (although you won’t be able to stay covered past a certain age, often around 80).

If you die during your policy term, your loved ones will get a payout. This will usually be one big payment that your loved ones will often use to cover things that they’d otherwise struggle to afford without your income. For instance, it could help them with mortgage repayments, rent, household bills or childcare costs.

However, what happens if you don’t die within this time? Well, aside from being a cause to celebrate the fact that you haven’t yet popped your clogs, nothing else much happens. Instead, your cover will just stop, and you’ll stop paying your insurance premiums accordingly.

As a general rule, you won’t get a refund. However, a few specialist insurance providers (people that give out insurance) offer a special kind of term life insurance called return-of-premium (or ROP). It’s pretty unusual, but if you have one of these policies and you’re still alive at the end of your insurance term, you will get a refund. In this case, you’d get all the monthly or yearly payments you made back, in one tax-free payment. Kerching!

There’s just one problem: these policies are hugely expensive. In fact, you’ll normally pay triple what you would on a standard term life insurance policy. Plus, they’re really hard to get your hands on as hardly any insurance providers offer them. So, as nice as they sound, we wouldn’t pin your hopes on one!

Whole-of-life insurance is a life insurance policy that won’t run out until you die. While a term life insurance policy only lasts a set amount of time, a whole-of-life policy will last your whole life, until you eventually pass away.

The good side? Your loved ones will get a guaranteed payout! That makes it really useful if you want to make sure your loved ones get a nice chunk of money when you die. It’s often used by people who want to contribute towards the cost of their funeral, or who want to help cover the inheritance tax bill for their loved ones (inheritance tax is a tax that’s charged on the money and possessions of someone who dies).

The bad side? It’s much more expensive than most term policies. However, if you hate the idea of paying for something you might never need, a whole-of-life policy is probably going to be a better option than one of those return-of-premium policies we told you about earlier (you know, those policies that refund your premiums at the end of your insurance term).

Why? Well, they’re a lot easier to get your hands on as lots of the big providers offer them. Plus, since there are more providers to choose from, there’s a better chance of getting a good deal!

On top of that, a whole-of-life insurance policy will cover you all the way up until your death. While a return-on-premium policy might sound appealing, once you get that lovely refund, you won’t be covered anymore. Which might not be ideal if you still want to protect your loved ones financially!

Okay, so if your term life insurance policy is due to expire and you’re (luckily!) still alive, what should you do? Here are your options.

Do you still want to protect your loved ones financially if you die? In this case, your current insurance provider might be happy to simply extend your policy term.

Extending your existing policy will normally be cheaper than starting from scratch and getting a new life insurance policy with a different insurance provider. That’s because when you apply for life insurance, providers will look at your age and health before deciding whether to approve you and how much to charge you. The older you are, and the more health conditions you develop, the harder it will be to get a good deal – and let’s be honest, the chances are some time has passed since you first got life insurance!

On the other hand, you can sometimes make changes to your existing policy – like extending your insurance term – without having to give your provider any extra medical information (although it’s important to check your policy documents as there’ll often be some exceptions). Even though your premiums will probably still go up, you’ll often find you save money this way as your costs will be calculated based on the information you gave your provider when you first got your policy – back when you were younger and (potentially!) healthier.

If your insurance provider won’t extend your policy, you could look at getting a new one, either with your existing provider or a different provider altogether. In fact, even if your existing provider is happy to extend your policy, it will still be worth looking at other options to see if you can get a cheaper deal elsewhere (especially if they want to take into account extra medical information).

We’d recommend using a comparison site to see what deals are available to you, and how much they cost. You could use MoneySuperMarket, Confused.com, Compare the Market or GoCompare. Or, better yet, use all 4 as they’ll all show slightly different deals.

Just bear in mind that, if some time has passed since you got your last life insurance policy, you might find it harder to get approved (or it may just be more expensive!). That’s all to do with the fact that, as you get older and develop health conditions, you’re more likely to make a claim before you’ve made many payments to your provider (making a claim is when your insurance provider is asked to pay up).

If you’re over 50 and you’re struggling to get approved for a standard life insurance policy, you might be tempted to look at over-50s policies.

These are life insurance policies that are guaranteed to accept you if you’re over the age of 50 (although you will still need to be under a certain age, often 80 or 85). However, they tend to be really expensive and a lot of the time, you’re not allowed to make a claim in the first 1 or 2 years. So, often, they’re not really worth it. Which brings us onto...

Depending on your circumstances, you might decide that you don’t need to be covered anymore. Don’t get us wrong, we think life insurance is important, especially if you have loved ones who depend on your income. And especially if you have large financial commitments that your loved ones would struggle to afford if you passed away (like a mortgage).

But there are times where you might not feel you need life insurance anymore, or where it stops being worth it.

The main one is to do with your age. As you get older, you might find the need for life insurance gets smaller. For example, your children might be earning their own income, or you may have paid off your mortgage so your partner wouldn’t have to worry about the repayments if you passed away.

On a term policy, you won’t normally be able to stay covered past around the age of 80. But unless you’re keen to help your family out with a contribution towards funeral costs or the inheritance tax bill, this won’t normally be a problem – you’ll likely no longer be working at this point, so your passing won’t result in a loss of income for your loved ones.

On the other side of the coin, you might decide you want to remain covered but then struggle to get approved for a new life insurance policy. For instance, you may have developed a serious health condition. If this is the case, it could be a good idea to put aside whatever money you would usually pay your insurance provider each month or year to help support your loved ones later on.

For instance, you could save it to help pay for funeral costs. Or you could invest it, for instance putting it in a Stocks & Shares ISA for your family to benefit from later (remember though, investing always comes with a risk!).

Ultimately, everyone’s different. So, think carefully about your loved ones and how they’d cope financially after you’re gone. If you want some bespoke advice, we’d recommend speaking to an independent insurance broker whose job it is to help you find the right insurance for your needs. You can find one using the British Insurance Brokers’ Association.

As you can see, life insurance is a great way of protecting your loved ones financially in case you die. But if you’re on a term life insurance policy like most people, it won’t last forever!

If you’re young and getting term life insurance for the first time, we’d recommend getting a policy that lasts as long as possible. That way, you’re very likely to get approved and you’ll be able to lock in a nice, low rate for a long time to come.

However, if your life insurance is due to expire and you’d like to remain covered, don’t panic. First things first, ask your insurance provider if they can extend your policy. Or, if that doesn’t work, head to a comparison site like MoneySuperMarket, Confused.com, Compare the Market or GoCompare to compare what’s available and to see if you can find a decent deal.

Fingers crossed you’ll get that all-important peace of mind that your loved ones could cope financially without you before you know it!

Check out our life insurance guide to learn more about how it can protect your loved ones financially after you pass away.

Check out our life insurance guide to learn more about how it can protect your loved ones financially after you pass away.

Check out our life insurance guide to learn more about how it can protect your loved ones financially after you pass away.

Check out our life insurance guide to learn more about how it can protect your loved ones financially after you pass away.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible