Review contents

Aviva is a well established pension provider (company) for work pensions (called workplace pensions). However, it might not be the best option for a personal pension (ones you set up yourself), or if you’re considering transferring old work pensions over. The customer service is often pretty poor, the pension plans are fairly confusing to understand, and the range of investments for experienced investors is limited. There’s better options out there.

Aviva is a massive company in the UK – they cover a lot of financial and insurance services, such as car insurance, home insurance, pensions, and investing. In fact, they’re even in Ireland and Canada.

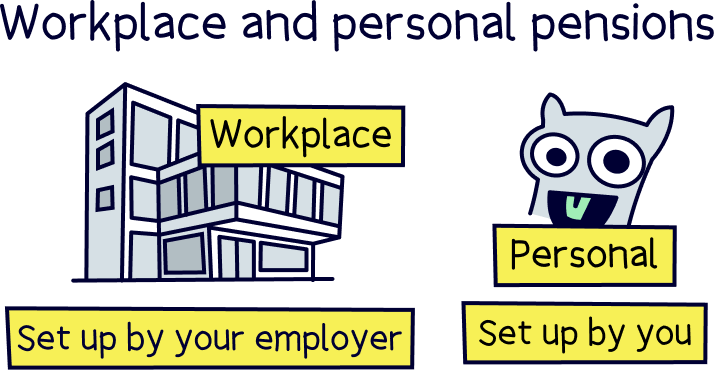

We’re going to be focusing on pensions – Aviva are one the biggest workplace pension providers in the UK – that’s a pension that your employer sets up for you if you’re employed.

You don’t have a choice which pension provider you get with your job, and you aren’t able to transfer it until you get a new job (if you didn’t know, you’re able to move your old work pension to a new provider when you change jobs, and it’s a popular thing to do).

Ultimately, Aviva focuses on workplace pension, but you can also choose to open a pension with Aviva outside of your work, called a personal pension (often a great idea to help boost your pension pot).

Or, if you leave your job with your work, your Aviva pension will automatically turn into a personal pension, that you can then move to another pension provider (company), or keep it where it is – we’ll run through all your options and benefits below.

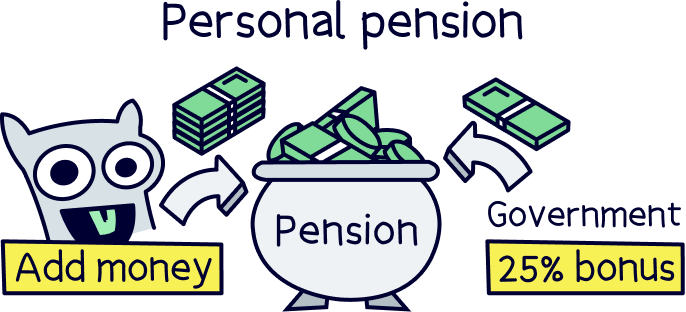

If you’re self-employed, a personal pension is your only option, but a great one. (With a personal pension you’ll get a 25% bonus from the Government on everything you save.)

Also, you might be considering moving an old pension over to your new Aviva pension that you’ve got with your new job – this can be a good idea if you want to combine them all together, but they’ll then be stuck with Aviva until you get another new job.

As a spoiler, we don’t rate Aviva too highly. It’s complicated to use, the customer service is pretty poor (think waiting on hold for a long time), and the investment options (choices) aren’t the best.

If you're looking to open a pension, or thinking of transferring any old pensions to Aviva, we recommend checking out PensionBee¹ – it’s easy to use, low cost, and has a great record of growing pensions over time. Plus you get a dedicated account manager to help you whenever you need it.

We've also secured a deal where you'll get £50 added to your pension when you sign up through Nuts About Money. Here’s our PensionBee review to learn more.

There's also Beach¹, which is an easy to use app, where you can open and manage a pension, and they'll find lost pensions too.

Enough about that, let’s get down to the details of Aviva…

As mentioned, Aviva is mostly known for being a workplace pension provider, which is a pension you’ll get from work, and you’ll typically be automatically enrolled when you start a new job, unless you ‘opt out’ (not recommended).

By law, most companies have to offer their employees a pension, and the employer decides who the pension provider is – often they just want to get the box ticked, rather than finding the best one for their employees, and so most companies opt for Nest pensions or Aviva, two of the largest and well-known companies.

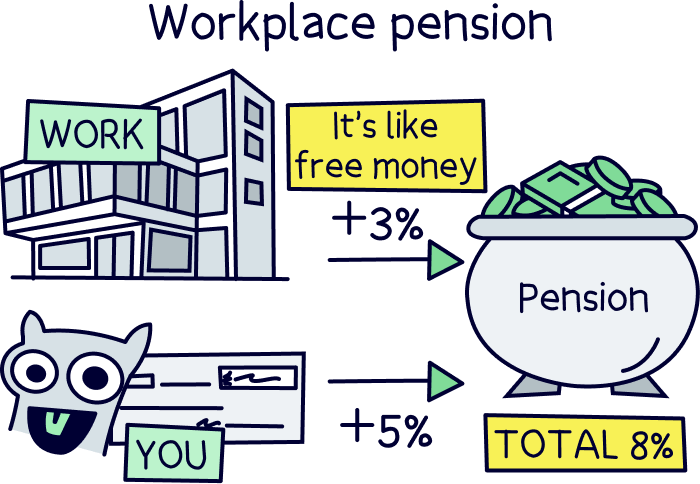

The great thing with workplace pensions is that your pension contributions are taken directly out of your pay before any tax is paid (so you won’t pay tax on them), and if you add 5% of your salary into your pension, your employer has to add 3% (by law). Pretty great right? It’s like a free pay rise!

Once it's set up, it’s all over to Aviva (or the pension provider you choose) to grow your money over time – and typically, you’d choose how your pension is invested from a range of different options (we’ll cover these below).

Nuts About Money tip: these days, you’ll need a lot of money in your pension to give yourself a comfortable retirement – likely a lot more than you are currently saving (sorry to put a downer on things). That’s where personal pensions can come in (a pension separate to your workplace pension). To find out how much you might want to be saving, check out our guide to how much you should be paying into your pension.

Beach is easy to use, with a great app. They can find and combine lost pensions too.

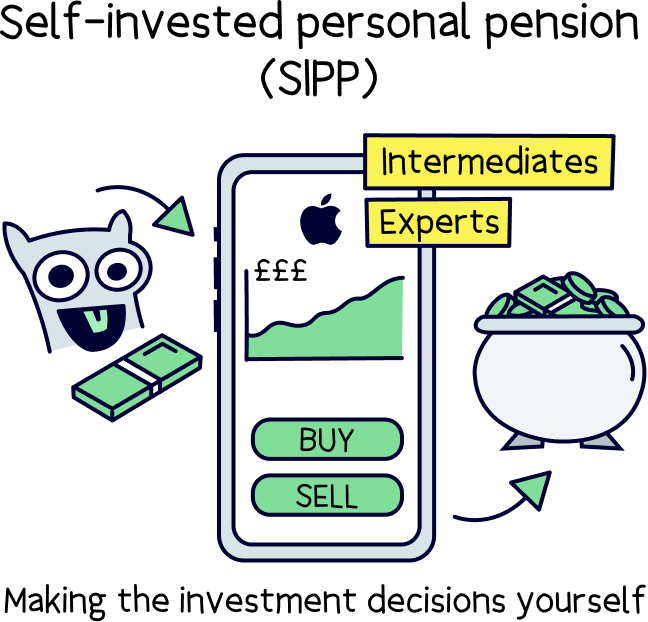

Aviva is predominantly a workplace pension provider for employees, and that’s their core focus, rather than self-employed people. However, you can sign up for a pension with Aviva if you want to – you’ll need to open a ‘self-invested personal pension’ (SIPP)...

That’s a pension that you manage yourself, and you decide which investments you want to make within your pension (e.g. what shares, or investment funds you want to buy). They’re typically for more experienced investors (explained below).

But don't worry, if you are self-employed, you’ve got lots of pensions to choose from. You'll need to open a 'personal pension', and the best ones have experts to handle everything, all you need to do is add your money (ideally monthly), and you’ll benefit from all the great tax advantages personal pensions have, such as a 25% government bonus on all the money you add (we’re not joking!).

Of course, letting the experts handle everything is probably a sensible idea, and the top option for that is PensionBee¹ – it’s easy to use, low cost and has a great track record of growing pensions over time.

And getting technical, if you are self-employed, you can pay in directly from a limited company bank account (to save even more tax).

If you’re keen to learn more about pensions while being self-employed, here’s our guide to the best private pensions for the self-employed.

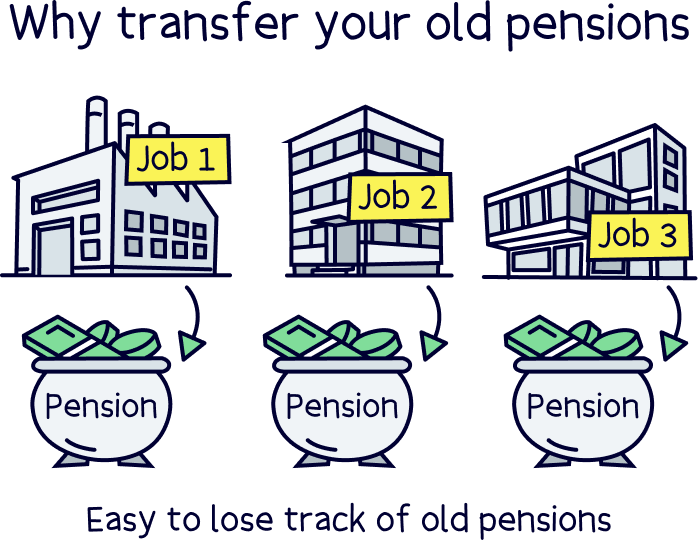

If you’ve now got a brand new pension with Aviva, perhaps from starting a new job, you have the option to transfer any old pensions over to it.

Keeping all your pension together is usually a good idea, however as soon as you move them over to your new workplace pension, you won’t be able to move them again until you get a new job.

It’s not necessarily that being stuck with Aviva is a bad thing, but there might be better pension providers out there that suit you better – and this could change over time.

So, having the flexibility to move your pension in future is a great idea. For instance, your pension with Aviva might not be performing well (not making much money), or you might find their website is hard to use, and customer service not great. There’s all sorts of reasons why you might want to change it.

Imagine your pension a bit like your mobile phone contract, or broadband deal, it’s best to shop around to find the best one for you, and not sign up to the default package.

With that in mind, ideally, you want to transfer old pensions to a personal pension, so you can retain full control of which pension provider to use. You can pick one that suits you, perhaps easy to use, low cost, with experts on hand to help… You get the idea.

Sorry to go on about them, but they really are great, we recommend PensionBee¹ as the top personal pension provider. There’s alsBeach¹, which is an easy to use app, great customer service, and can find lost pensions.

With both, they’ll handle the whole pension transfer process too. All you need to do is let them know who your old pension is with.

Check out the best pension providers to find all the top options.

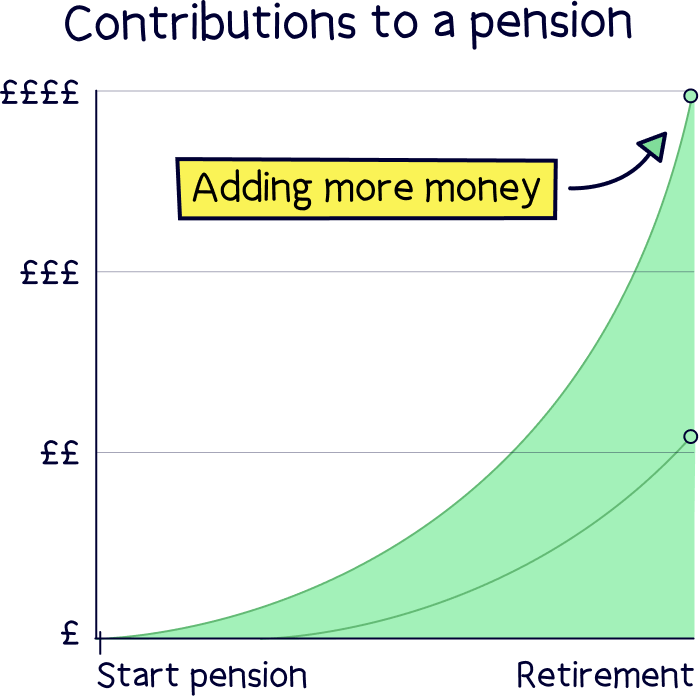

Okay, one last thing about personal pensions, before we dive into Aviva. It’s a sensible idea to pay as much as you reasonably can into your pension, to help build a big pension pot for later-in-life, or even retire early.

If you want to pay in more than 5% of your salary (which is the minimum amount for a workplace pension, to get the free 3% from your employer) – it’s often a good idea to pay anything above this into a personal pension separate to your workplace pension.

Why? Well, for the same reasons we’ve mentioned above, once it’s in a workplace pension, it’s stuck there until you change jobs, and it might not be with the best provider. With a personal pension, you can pick the best one for you (and change it in the future if you want to).

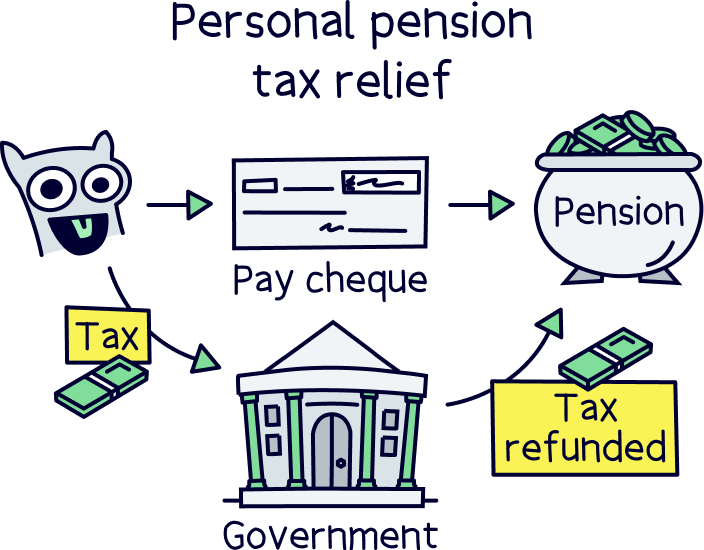

By paying the extra into a personal pension, you’ll still benefit from all the same tax-free benefits – it just comes in the form of a 25% bonus from the Government, automatically added to your pension pot when you add money…

As pensions are intended to be tax-free, when you pay into a personal pension, you’ll have actually already paid tax on your income. So, the Government refunds you the tax paid straight back into your pension pot. Make sense?

As a recap, here’s our guide to the best personal pensions.

Aviva has a range of options for you to invest your money within your pension. You’ll select one, or a combination of options when you get started.

If you’ve got a workplace pension with Aviva, your options are fairly limited, you won’t be able to invest in anything and everything you like. You’ll have to pick from a limited range of investment options they provide for you.

These include some of the options below (but not all of them).

If you have a personal pension with Aviva, you can choose from all of the following options…

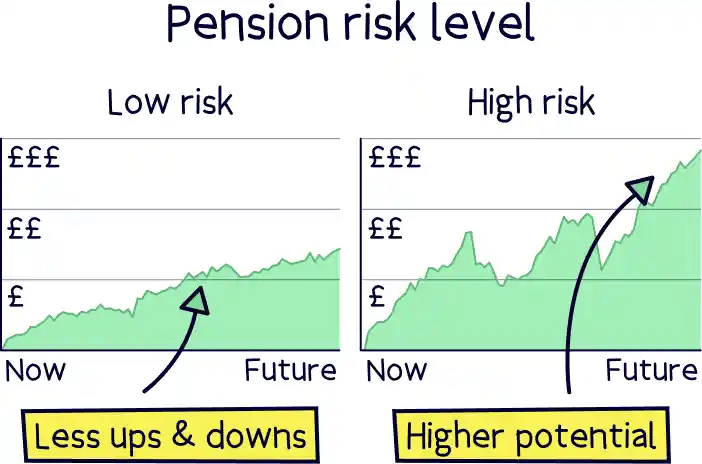

This great option will adjust the mix of investments within your pension based on your age, and will gradually change over time throughout your life, from higher risk investments to lower risk investments…

Higher risk means that your money could grow a lot over time, but there will likely be bigger ups-and-downs along the way, whereas lower risk means less ups-and-downs, but likely to grow slower over time.

When you’re younger, it’s generally considers okay to take on a larger amount of higher risk investments as you have time to ride out the ups-and-downs – but it’s totally up to you.

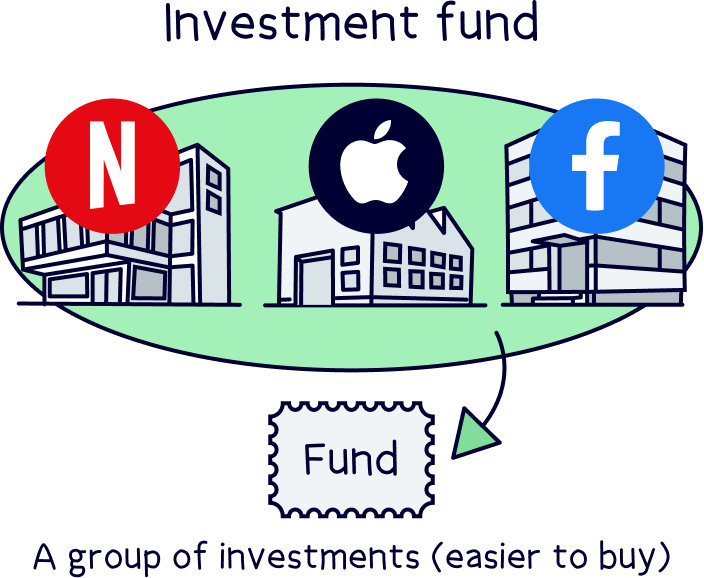

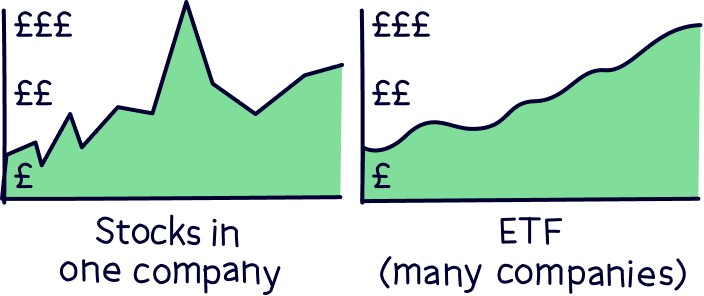

These are groups of investments all packaged together, and well, ready to go (called investment funds).

You’ll pick from a range of investment goals, such as growing your money over time, or providing a regular income. And then the level of risk you’d like to take – more risk means a higher expectation of growth over time, but with bigger ups-and-downs along the way.

These options might seem a bit complicated if you’re not too familiar with investing, as you’ll have to make a few decisions about the risk levels yourself.

Note: a ‘fund’ is a collection of lots of different investments (such as shares in companies, which themselves represent ownership of the company, you own a share of the company), all pooled together into a single investment.

The investment experts at Aviva have put together a shortlist of investment funds they recommend, which you can pick from.

Note: this doesn’t mean the investments are guaranteed to make more money, or perform well in the future.

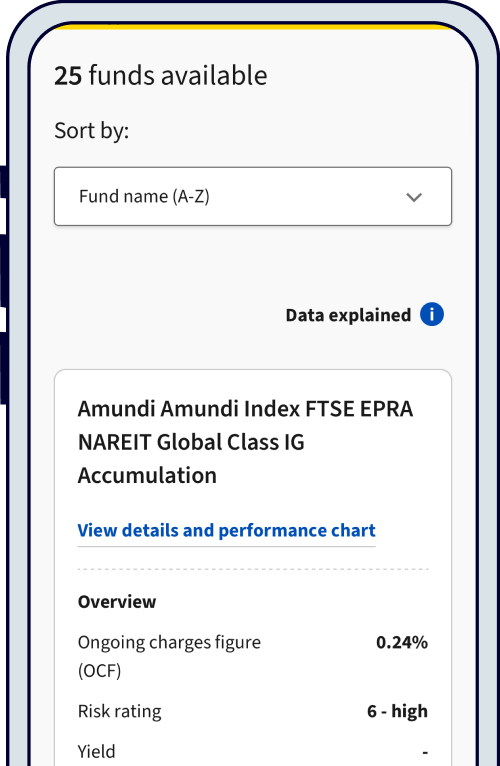

You also have the option of choosing from a wide range of investment funds and individual shares to build your own portfolio (mix of investments). This is only recommended for experienced investors.

If you are interested in choosing your own investments, you might be better off using a larger investment company such as AJ Bell¹ or Interactive Investor¹ – they’re both easy to use, low cost, and have a huge range of investment options (all within a personal pensions called a SIPP).

Right, let’s get into the fees – they're fairly reasonable for a workplace pension provider. There’s no surprises, it’s not super expensive, but it’s not super cheap either.

The fees will be taken out of your pension pot directly, rather than you paying anything up-front yourself.

The main fee you’ll pay is the annual management fee, called the ‘Annual Aviva Charge’. This is a percentage of the money you have within your pension and is:

You’ll then pay a fee within the investment fund itself, and this varies depending on which investment fund you choose. They can range anywhere from 0.35% to 1.5%+. The majority of the funds managed by Aviva themselves are 0.35% (e.g. ready-made funds).

So, that gives a total of 0.75% to 1.9% per year (if you have less than £50,000), which will reduce as your pension pot grows into large amounts.

For comparison, PensionBee¹ (sorry to keep mentioning them, but they’re pretty great), has an overall cost starting at 0.50%, and depending on your pension plan, can go up to 0.95% (in total), and reduces the more you save.

If you want to make your own investments outside of one of the suggested funds, there are some extra fees to pay.

For example, this would apply if you want to buy shares of individual companies directly, or investment funds that are traded on stock exchanges (called exchange-traded funds (ETFs)).

This is 0.40% per year of the total amount that you hold. And is capped at £120 per year in total.

On top of that, you’ll also pay £7.50 every time you buy and sell an investment.

You’ll also pay Stamp Duty when you buy shares in UK companies, which is 0.50%, and paid to the Government.

It all starts adding up isn't it? If you’re looking to make lots of investments yourself, check out InvestEngine¹, AJ Bell¹ and Interactive Investor¹ – all have a wider range of investments and are low cost.

The customer support is pretty poor. Aviva is a huge old fashioned company, with not much appreciation for the little guy, their customers…

So, if you call them up, expect things like a long wait on hold.

You won’t get any expert advice either. The support is mostly about how to use their website and app to make things like one-off payments, and view your balance (the website and app aren’t user friendly).

On top of that, they make it really hard to actually speak to a real person, and try to direct you to their online ‘chatbot’ first, or send them a message first for them to reply when it suits them.

Yep. It’s perfectly safe to use Aviva for your pension, or for any other financial service.

Aviva is authorised by the Financial Conduct Authority (FCA), which means they have been approved and are trusted to look after and protect your money.

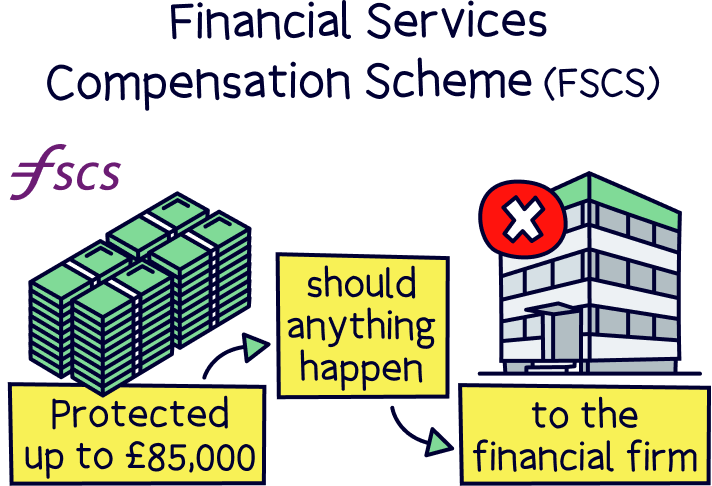

That also means your money is protected by the Financial Services Compensation Scheme (FSCS). Which gives you protection up to £85,000 should anything happen to Aviva, such as going out of business (unlikely).

Although saying that, your pension and investments are actually held entirely separate from Aviva’s own money, all in your own name, and can only be returned to you. So there's extra security.

As Aviva is a large company offering lots of different services, unfortunately that means all their reviews are merged together too – so it’s not possible to look at just the reviews for the pensions service.

Typically, to get an idea of the service, we like to look at the popular reviews website, Trustpilot. On Trustpilot, Aviva has a great score of 4 out of 5, and from a lot of reviews.

That is great overall, but looking into the reviews a bit closer, lots of the 5 star reviews are about the cost of car insurance being good value (only when using a comparison website first, not going direct). And lots of the 1 star reviews are about the poor customer service. So, we’ll let you make your own mind up on that one.

Here’s a quick recap and the pros and cons of Aviva pensions:

We’re big fans of helping people save for their future, especially for retirement, where these days, we’ll all need a pretty hefty pension pot in order to have a comfortable retirement.

With that in mind, Aviva is doing a good job by providing a workplace pension for employers to use – and it is pretty popular.

However, for those who are able to make their decisions with their pension, for instance if you’re considering opening a personal pension, or transferring old pensions over to Aviva, it’s likely not going to be the best option for you – the customer service is pretty poor, the investment options aren’t great, and are complicated to understand and to round it off, the website and app are hard to use.

If you’re a more experienced investor wanting to make your own investment choices, the investment options are very limited compared to the larger pension providers such as AJ Bell¹ and Interactive Investor¹, and they’re much cheaper too.

If you’re just looking for the experts to handle your pension, you’ve also got better options – ones with great customer service, have experts on hand to help, are easy to use and understand, and are low cost.

And if you hadn’t guessed yet, we recommend PensionBee¹ as our top option, for all of those reasons. And, if you sign up with Nuts About Money, you’ll also get £50 added to your pension for free.

Another great alternative is Beach¹,where you can also save and invest outside of a pension (for instance in a tax-free ISA).

So, overall, we’re giving Aviva 2 stars. It’s an okay service for a workplace pension, but it’s likely not the best option for a personal pension. If you’re keen to learn more, here’s the Aviva website.

Beach is easy to use, with a great app. They can find and combine lost pensions too.

Beach is easy to use, with a great app. They can find and combine lost pensions too.

Beach is easy to use, with a great app. They can find and combine lost pensions too.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Beach is easy to use, with a great app. They can find and combine lost pensions too.