Article contents

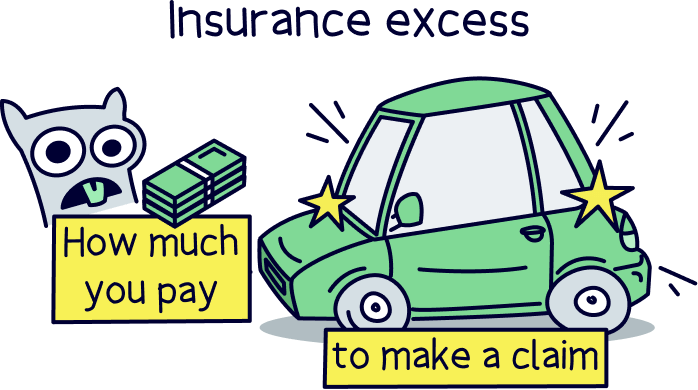

Insurance excess is how much you’ll pay yourself, should you ever have a successful claim on your insurance (the insurance company pays out and gives you money). It’s made up of compulsory excess (set by the insurer) and voluntary excess (set by you).

Insurance can be pretty complicated, especially when it comes to the excess. What even is insurance excess?! Don’t worry, you’re in the right place. Let’s run through it.

Note: insurance excess covers almost all types of insurance, e.g. home insurance, contents insurance, car insurance and travel insurance.

Insurance excess is how much you will have to pay yourself, when you make a successful claim on your insurance. A successful claim is when the insurance company gives you money as compensation, or pays bills on your behalf (e.g. medical costs). They’ll do this after something has happened that you were insured for, e.g. losing your luggage on a flight, or being involved in an accident.

The total amount of excess on your claim is made up of two parts, a compulsory excess, and a voluntary excess. Let’s run through those.

By the way, you might not actually have to pay any actual cash out yourself (depending on the insurance). The excess can be deducted from the total compensation you’d get. For instance, if you had your personal items insured for £1,000, with an excess of £200, and they were stolen, you’d actually get back £800 from the insurance company.

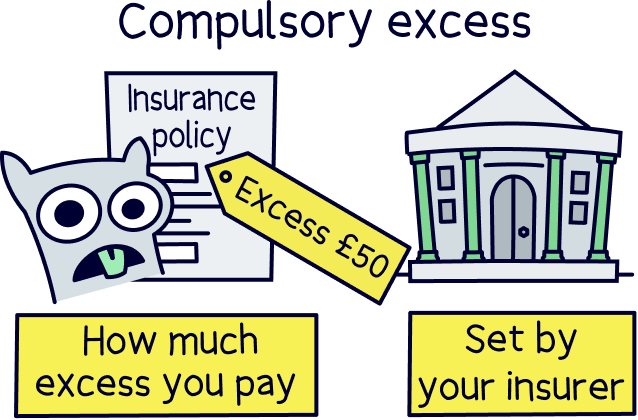

Compulsory excess is what the insurance company will decide the excess figure is, so you could think of it as the minimum excess. It’s determined by your personal circumstances (e.g. your age), and the type of insurance you want, so it can be different for everyone.

It can also be different for different parts of the same insurance cover. For instance, you could have a smaller excess for a claim that covers losing your items (such as a passport abroad), maybe £25, and a higher excess, maybe £250, for personal liability cover, which is cover for legal expenses if you get into an accident involving someone else or their property (legal expenses can get very expensive).

If you want to learn more about this, here’s our guide: what is compulsory excess?

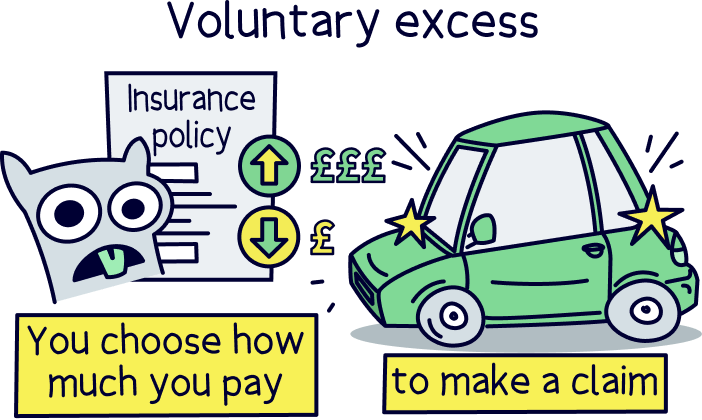

Voluntary excess is the part of the excess where you decide how much you set. Sounds great right?

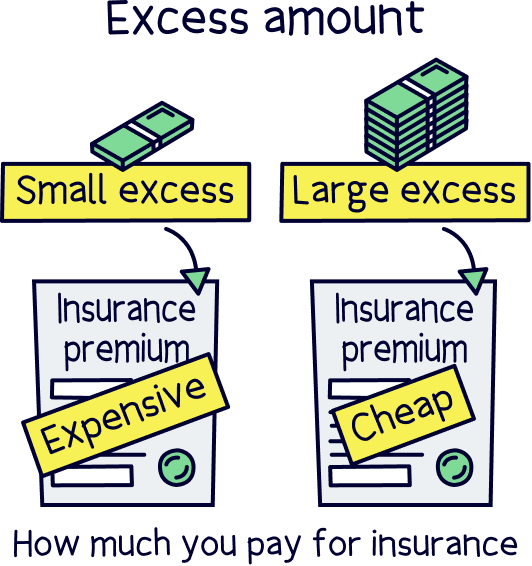

You get to decide how little or how much the excess is, from a set range. As the excess determines how much the insurance will cost (normally), this means you can actually increase or decrease the cost of the insurance by increasing or decreasing the voluntary excess. The higher the excess is, the lower the cost of the insurance.

And because you get to decide the figure, you can get the balance just right for you and your budget.

If you want to learn more about this, here’s our guide: what is voluntary excess?

Insurance providers have an excess for two main reasons:

To confuse things a little, you can in fact get insurance with no excess, and you guessed it, it’s called no-excess insurance. This can be a great idea if you think you would prefer to not have any excess at all, for peace of mind or any other reason.

The only downside is that you’ll have to pay a bit extra for the insurance (well, sometimes quite a bit more). And it doesn’t apply to all insurance policies, you’ll have to specifically get no-excess insurance.

Oh, and sometimes it doesn’t apply to everything on the policy. For instance, if there’s something that could cost the insurance company a lot of cash, such as emergency medical costs, you might still have to pay an excess.

With some insurance companies and policies, there’s also something extra you could get, called an insurance excess waiver. This effectively ‘waives’ the excess if there was ever to be a claim – this means the excess is effectively ignored, and you don’t have to pay it. It’s also called excess insurance.

However, nothing in life is free, and it's going to cost you. Normally, this is an extra fee when you take out the insurance, or shortly after. It’s down to you and your preferences if you want this or not, but it can be a good idea for bigger trips away (with a big excess), and things like car hire insurance (with a big excess).

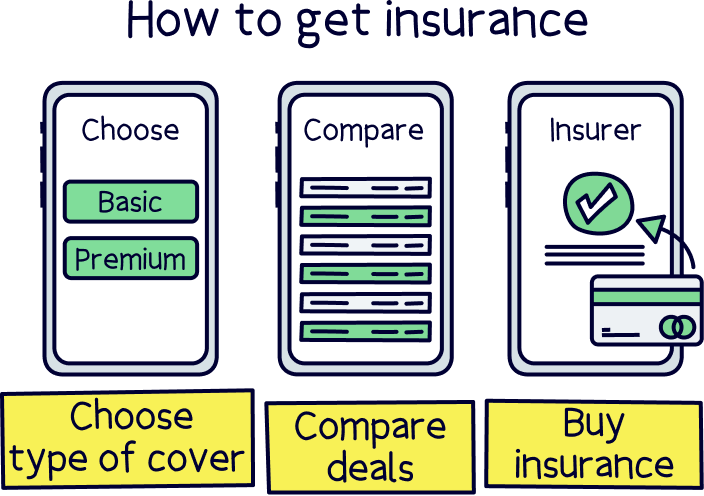

Although insurance can be a bit confusing, especially when it comes to the excess, the good news is that it’s easy and simple to find the best insurance deal for you. And that applies to all the different types of insurance you might be looking for (e.g. car insurance or travel insurance).

All you need to do is head over to an insurance comparison site, such as Confused.com¹. Add a few details about yourself and the insurance you’re looking for, and they’ll head off and search a wide range of insurance companies to find the right deal for you (in just a few seconds).

From the short list, simply find the right deal for you, which can often simply be the cheapest. After that, you’ll be taken to the insurance company’s website, which normally has all your details pre-filled – ready to be double-checked and then simply buy the insurance. As simple as that. It can take just 10 minutes overall.

Nuts About Money tip: looking for travel insurance? Here’s a great guide on how to get travel insurance.

Has that made insurance, and insurance excess a bit easier to understand? We hope so! As a recap, insurance excess is how much you’ll pay out yourself, if you make a claim on your insurance (and it’s successful).

It’s made up of two parts, compulsory excess and voluntary excess. Compulsory excess is set by the insurance company, and can’t be changed (it's the minimum amount you will have to pay). And voluntary excess is set by you, and can be changed.

You can adjust the voluntary excess either up or down (within a set range), and the lower the excess, the higher the cost to buy the insurance, and vice versa. Meaning you can get the balance just right for you.

And if you do ever make a claim, you might not actually have to pay any cash out directly, it could simply be deducted from how much you get back in compensation, it all depends on your insurance and your claim.

You can also get no-excess insurance if you prefer a bit of peace of mind, and even an insurance excess waiver, so you don’t have to worry about paying any excess if the time comes. However this will usually be more expensive to buy in the first place.

That’s all there is to it. All that’s left is to find the best deal for you.

Head over to Confused.com to find the best deal for you. They search almost every deal out there.

Head over to Confused.com to find the best deal for you. They search almost every deal out there.

Head over to Confused.com to find the best deal for you. They search almost every deal out there.

Head over to Confused.com to find the best deal for you. They search almost every deal out there.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible

Head over to Confused.com to find the best deal for you. They search almost every deal out there.