Article contents

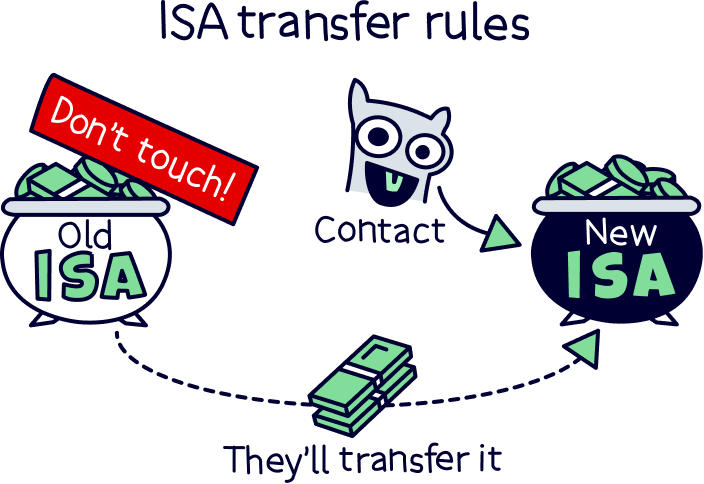

You can transfer your ISA to a different provider whenever you want. But whatever you do, don’t close your old ISA! Instead, contact the provider you want to move to, and they’ll sort out the transfer for you.

Got an ISA? Then you might be wondering if you can move it to a different provider. Maybe you’ve found a provider with cheaper fees elsewhere, or perhaps you have multiple ISAs and you want to gather them all in one place.

If that sounds familiar, we have some good news for you: you can transfer your ISA to a different provider whenever you want! Hooray! However, there are a few rules you’ll need to keep in mind.

An ISA transfer is when you move your ISA from one provider to another (your ISA provider is the company who gives you your ISA).

There are 2 main types of ISAs: Cash ISAs and Stocks & Shares ISAs. A Cash ISA is a savings account where you can earn tax-free interest (interest is a payment you get for leaving your money in the ISA). However, as interest rates are currently low, you’re unlikely to earn much, if anything at all, at the moment.

A Stocks & Shares ISA is a savings account where your money gets invested (meaning it’s used to buy stocks and shares, which are small stakes in companies). The idea is that your investments will (hopefully!) increase in value and make you more money over time. Better still, you won’t have to pay any tax on the returns (money) your ISA makes for you.

When you transfer your ISA, you’re essentially moving your cash or your investments to a new ISA with a different provider. You can switch your ISA type if you want, but you don’t have to. In other words, if you have a Cash ISA, you could transfer it to a Stocks & Shares ISA or to another Cash ISA.

Similarly, you could transfer your Stocks & Shares ISA to a Cash ISA or to another Stocks & Shares ISA. If you’re transferring it to another Stocks & Shares ISA, you can either transfer your investments without selling them (called an ‘in specie’ transfer). Or you can sell the investments and transfer the cash over (called a cash transfer). Simple!

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.

So, you now know what an ISA transfer is, but why would you want to do it? Well, there are a few different reasons why you might want to switch your ISA to a new provider, and it’s often a good shout!

You can technically transfer your ISA wherever you want, whenever you want. Woohoo! And it’s normally pretty easy. However, there are a few things to bear in mind.

If you have a Cash ISA, it will often be what’s called ‘fixed rate.’ A fixed-rate cash ISA is one that lasts for a set period of time and guarantees you a certain amount of interest. Sounds pretty good, right?

Well, they can be, but there’s a catch. If you want to take your savings out during this time, you’ll have to pay a hefty fee. That means that it might be wise to wait until the end of your fixed period before you transfer your ISA – that way, you can avoid the penalty.

Of course, if you can find a new provider that’s much cheaper than your current one, it may still be worth switching. But it’s important to take the penalty into account when you’re working out whether it’s a good idea.

Thanks to ISA transfer rules, all ISA providers have to allow you to transfer your money out of your ISA. However, they don’t have to accept transfers in!

That’s right, if you’re looking for a new ISA provider to transfer your ISA over to, you’ll need to check that they accept transfers. Sometimes, ISA providers that don’t accept transfers have better deals. This is especially the case with Cash ISAs, as often providers that accept transfers will have lower interest rates. Take all of this into account when you’re umming and ahhing about whether it’s worth going ahead with an ISA transfer.

Remember how we said that you might want to consolidate lots of different ISAs into 1 ISA to make it easier to manage? Well, we stand by the fact that this can be a good idea. But it can also be sensible to avoid letting 1 financial institution look after more than £85,000 of your money.

If you’re wondering why, it’s because of this great scheme called the Financial Services Compensation Scheme (FSCS). Basically, the FSCS will protect up to £85,000 of your money with each financial institution you use. Get in! However, if you go over this, your savings won’t be protected in the same way anymore.

Let’s be honest: nobody wants to put their money at unnecessary risk. So, you may as well do the sensible thing and spread your savings out across more than 1 financial institution if it looks like you’re going to go over that £85,000 threshold (as long as they’ve got the investments you want and the fees are good). Just make sure to remember where you’ve stashed all that cash though – the last thing you want is to forget about it!

Each tax year, you’re only allowed to pay a certain amount of money into ISAs, known as your ISA allowance. This can change from year to year, but at the moment, it’s £20,000.

The good news is that ISA transfers don’t count towards your ISA allowance. Hooray!

Let’s say you want to transfer an old ISA that you haven’t contributed to this tax year. And let’s say that that ISA is worth £10,000. In this case, you can just transfer it to a new provider and you’ll still have your full £20,000 allowance to play with.

Now let’s imagine you have a £10,000 ISA you want to transfer but you paid in that £10,000 this tax year. In this case, you can transfer it over to a new provider (as long as you transfer the whole thing, remember). Then, you’ll still be able to add up to another £10,000 this tax year (£10,000 + £10,000 = £20,000).

This bit’s really important. If you want to do an ISA transfer, DON’T close your old ISA or withdraw any money yourself.

Why? Well, the great thing about ISAs is that any money or investments you have in them are tax-free! In other words, your ISA is like a magic forcefield protecting your savings from the taxman.

If you take those savings out, they won’t be protected in the same way anymore and the taxman will come for them. Aaahhh! Plus, if you want to put that money back into a new ISA, it will be treated like a whole new deposit (in other words, it will count towards that £20,000 ISA allowance). Urgh.

To stop all that from happening, here’s what you need to do.

First, you’ll need to pick a new ISA provider to transfer your current ISA to. Remember, this will have to be an ISA provider that accepts ISA transfers.

To compare deals and find the best one for you, you can use our comparison table of best investment platforms UK.

As long as your new provider accepts ISA transfers, they’ll be able to sort the whole thing out for you. It’s normally super quick and easy to start the process off.

You’ll just need to fill out an ISA transfer form giving your old ISA provider’s details and letting your new provider know what you want to transfer over. Just have the details of your old account to hand.

Some providers will let you set up an ISA transfer over the phone, but it can also be done really easily online.

Now all that’s left to do is put your feet up and stick on your favourite Netflix series while your ISA providers sort everything out between them. Exactly how long it takes for the ISA transfer to go through will depend on what kind of ISA you’re transferring.

If you’re transferring a cash ISA to another cash ISA, you shouldn’t have to wait longer than 15 days, so it’ll all be sorted in a jiffy. You’ll get paid interest by your old ISA provider right up until the moment your ISA gets transferred. Plus, your new provider has to start paying you interest within 15 days of receiving your transfer request, even if the transfer hasn’t finished at that point. How cool is that?!

If you’re switching a cash ISA to a Stocks & Shares ISA or vice versa, it could take more like 30 days. And it can take even longer if you’re transferring a Stocks & Shares ISA to another Stocks & Shares ISA, depending on the way it’s done. In some cases, you could end up waiting for as long as 3 months.

However, don’t let that put you off. Your providers will handle everything for you, so hopefully, it shouldn’t be a hardship!

Now you’ve seen how easy ISA transfers are, you might be wondering if you could transfer your ISA to someone else. Sadly though, the answer is no! Your ISA can only be owned by one person and you can’t share it or give it to anyone else.

Well, there is 1 exception, but it’s not a very cheerful one! If you die, you can leave your ISA to whoever you want in your will and they can then inherit it (sorry to bring the mood down!).

In this case, your spouse or partner can apply for an extra ISA allowance called the inherited ISA allowance or additional permitted subscription (APS). That means they can transfer the contents of your ISA over to theirs without it counting towards the standard £20,000 ISA allowance.

Weirdly enough, only your spouse or partner can get this extra allowance. So, if you leave your ISA to somebody else, your spouse will still get the extra allowance and not the person you leave your ISA to. It’s just one of those strange rules!

You can transfer your ISA over to a new provider whenever you want. Hooray!

Just make sure that you let your new provider handle the ISA transfer for you. Please, please, please don’t close your old ISA or take your money out as you won’t be able to pay it into your new ISA if it’s over the ISA allowance. You can’t say we didn’t warn you!

If you’re looking for a new ISA provider to transfer over to, check out our best investment platforms to find the best one for you.

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Beach is an easy to use app allowing you to invest sensibly with the help of experts in a tax-free ISA.