Article contents

There’s lots of different types of mortgages out there, all suited to different types of people, with different circumstances. The most common is a fixed rate, repayment mortgage. That’s where your monthly repayments are the same (fixed) for a set amount of time, normally 2 or 5 years. These repayments would repay the interest, but also some of the mortgage. It’s best to speak to a mortgage broker to find the best mortgage for you.

Did you know there’s actually lots of different types of mortgages? There’s a whole range out there with different mortgages for different personal and financial circumstances.

That’s why we recommend using a mortgage broker to find the right mortgage for you – that way you can be sure you’re getting the best mortgage for you, they will find you the cheapest, potentially saving £100s per month.

If you’re not sure where to find a good mortgage broker, here’s the best mortgage brokers. As a spoiler, Tembo¹ tops the list – they’ve got great service and search every mortgage out there to find the right one for you.

Anyway, here’s an overview of all the different mortgage types, so you can get clued up on mortgages before you chat to a mortgage broker.

Firstly, there's different types of interest rates and then there’s different types of how you repay the mortgage.

Let’s run through them, it should all make sense after.

Let’s run through all the different ways to repay mortgages.

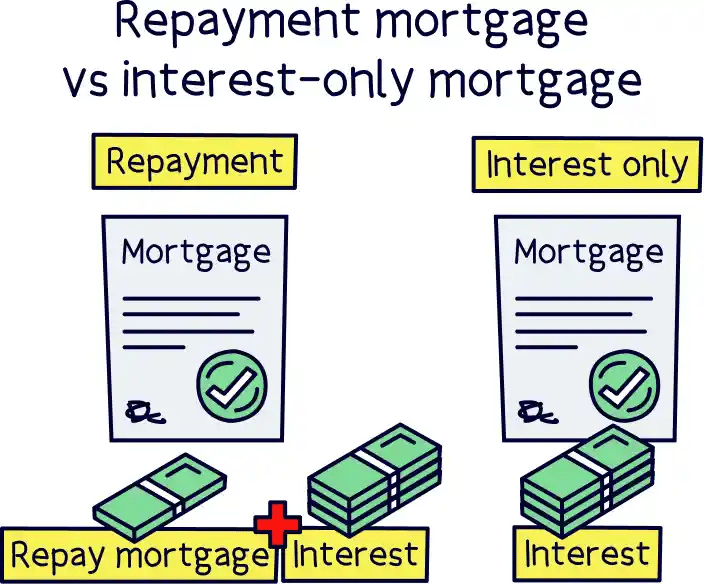

You might also hear repayment mortgages be called a capital and interest mortgage. It simply means paying back the mortgage loan itself and the interest each month.

Let's say you get a mortgage for £100,000 (this is also called the capital). If we take that figure and add on the interest that the mortgage lender (the people who give out mortgages) has set, we'll get an overall amount that needs to be repaid.

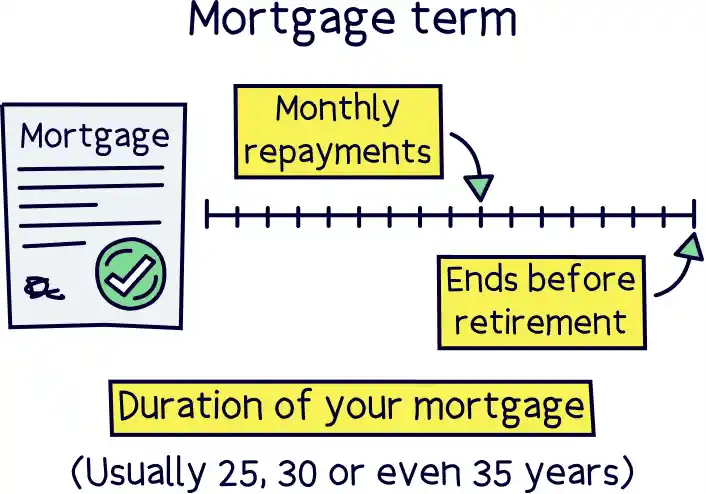

So let’s say the interest rate is 3.5% and doesn’t change over the whole mortgage term (length of the mortgage), for now, let’s say 25 years, then the total interest would be £50,000. (Let’s not worry about the maths for now).

So the total cost (overall cost) of the mortgage is £150,000.

A repayment mortgage would mean your monthly repayments would include paying back some of the interest (£50,000), as well as some of the capital, the actual mortgage loan (£100,000).

So eventually over 25 years, both are completely paid back and you are mortgage free!

Interest only mortgages are where you are only paying back the interest portion of the mortgage, when making monthly payments.

You will not be reducing the original loan amount at all. And at the end of the mortgage term, let’s again use a £100,000 mortgage over 25 years, you will be required to pay back the full amount of the loan, the £100,000.

The benefits of this are much lower monthly repayments, as you are just paying the interest. But they are expensive over time, as you’re never paying off the mortgage itself, and so the interest never reduces, like it does with a repayment mortgage (as you repay the mortgage, the amount of interest you pay will reduce).

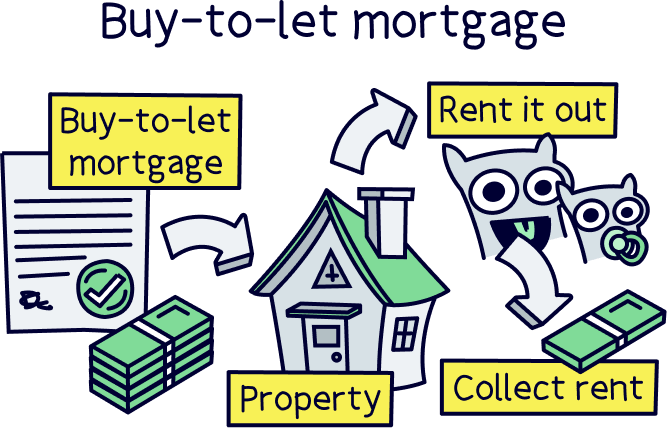

They’re typically not suitable for most people living in their own home. However, they are very common with a buy-to-let mortgage, as it helps increase cash flow for the investor (the amount of spare cash the owner receives). This means they can make more investments or simply increase their profit each month.

Plus, buy-to-let investors are relying on the house price increasing when they sell the property, at which point they will repay the mortgage loan, and walk away with a nice profit. Or, they could remortgage and get a new mortgage with a new mortgage term.

However, you need to prove you are able to repay the loan at the end of the mortgage term in order to get an interest-only mortgage – which is why it’s unlikely you’ll get one for your own home.

Interest-only mortgages can also have a higher interest rate than typical repayment mortgages. This is because the mortgage lender is taking on a bit more risk, as you won’t be paying back to the mortgage itself each month.

This is a combination of both a repayment mortgage and an interest-only mortgage.

So it’s part repayment, and part interest, or sometimes known as part capital and part interest mortgage.

It means at the end of the mortgage term, you will still have some capital left to repay.

Similar to an interest-only mortgage, at the end of the mortgage you will have to repay some of the capital, but not all of it (as you’ve been paying some off each month). So, some of the £100,000, if we use the same example as above).

There’s no set amount to how much you would have left to pay off at the end of your mortgage, this amount will be agreed when you get the mortgage.

You might get a part and part mortgage if you want lower monthly repayments (lower than a repayment mortgage), but also want a lower amount to repay at the end of the mortgage term (lower than a full interest-only mortgage).

Note: if you get this mortgage, you will need to prove that you can pay back the remaining loan amount at the end of the mortgage term. For instance some savings and investments elsewhere.

Tembo will find your best deal, and have award-winning service.

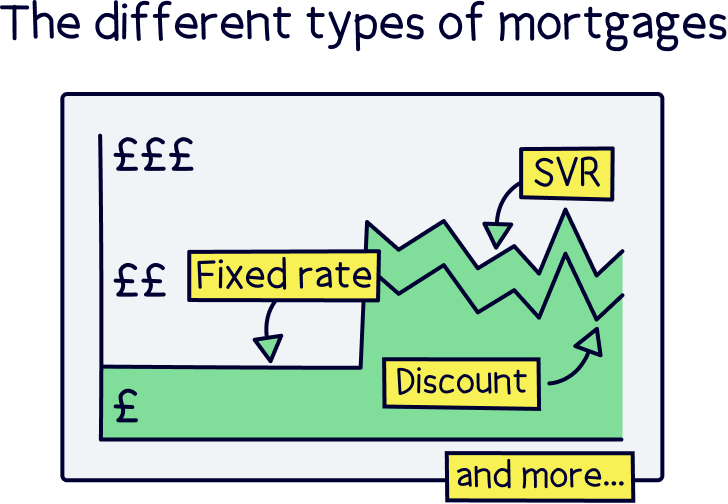

So, the above was the different types of mortgages, and how to repay it, but there’s also different types of mortgage rates – that’s the interest rate you’ll actually be paying. Let’s run through them.

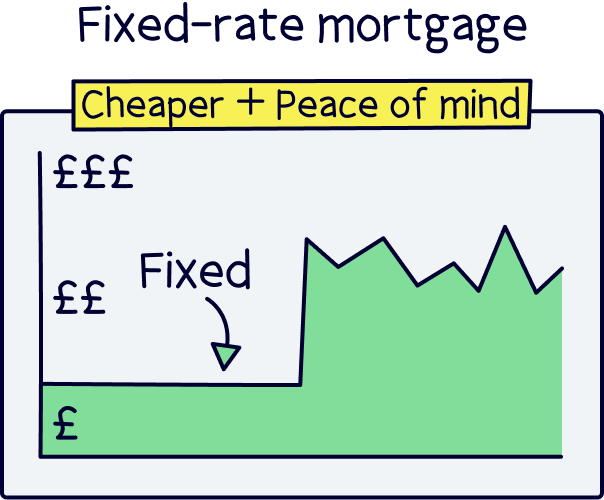

These are the most common types of mortgages in the UK – fixed rate mortgages.

Imagine a total mortgage term of 25 years. As part of that, there will be a length of time where the interest rate stays the same (fixed), and is usually for either 2, 3, 5, 7 or 10 years. With 2 and 5 years the more common ones.

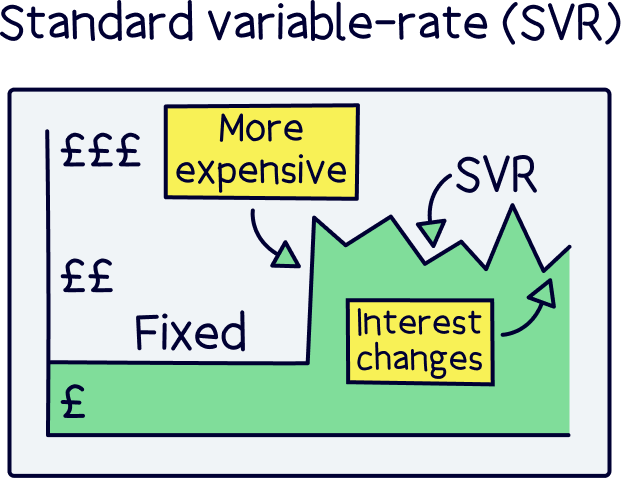

After this fixed rate ends, also called the introductory or incentive period, the interest rate changes to a variable rate that can go up or down, (often their standard variable rate (SVR)). This rate is normally a lot higher than the fixed rate. More on those below.

The fixed rate is essentially used as a sales tactic to make it look like the mortgage has a lower rate and compete with other mortgage lenders. This low rate can make it appear higher in comparison tables.

A standard variable rate is the ‘normal’ rate of your mortgage lender, or their standard rate. The rate varies across different lenders, and they can change it whenever they like.

It’s normally linked to the Bank of England base rate, which is a rate used by the Bank of England to control the economy (it’s the rate at which they lend out money to banks and the government).

We won’t go into exactly what the base rate is, but all you need to know is that if the base rate goes up, the lender's standard variable rate normally goes up too. And if the base rate goes down, lenders' standard variable rates normally go down too. But it is up to the lender to choose to do it, they have no obligation to, and sometimes don’t.

Nuts About Money tip: you often don’t want to be on a lender’s SVR, it's normally very expensive.

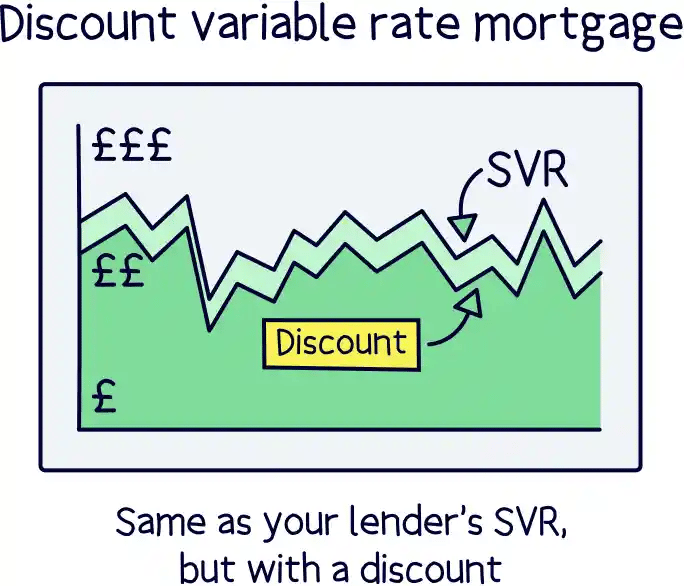

Similar to a lender’s standard variable rate (SVR). A discount variable rate mortgage is where, for a period of time, you get a discount from the standard variable rate. It’s as simple as that.

You need to be careful however, as the standard variable rate can change at any time, meaning your mortgage interest rate can change too.

A tracker rate mortgage is linked to a specific interest rate, and it tracks that rate and then adds a fixed amount on top.

This is normally linked to the Bank of England base rate, with an added fixed amount on top.

For instance, a mortgage might be linked to the Bank of England base rate, plus 1%. So if the base rate is 3%, you simply add 1% and your mortgage rate will be 4%.

It’s great when the base rate is low or falling, but it could change at any point and if it rises, your repayments will increase too.

A capped rate is a variable rate mortgage, so a standard variable rate, discount variable or tracker rate, but has a maximum amount of interest that can be charged, or put simply, a cap on the interest rate.

You might get this if you think the interest rates are due to go up soon, but you pay a premium (higher initial rate) than an uncapped mortgage.

This means that your mortgage payments can change month to month (are flexible). You can pay more than your set monthly payment amount if you want to, or less than your set monthly payment. This is called overpaying or underpaying.

By paying more than you need to, you’ll be reducing the mortgage term (how long you have the mortgage for), and also reduce the total amount of interest you’ll pay over the life of the mortgage (so saving a lot of money).

You can also take what’s called a payment ‘holiday’ which is a break from making any payments at all (for a set period of time).

Some flexible mortgages also allow you to build up a ‘reserve’ of money – a collection of overpayments you’ve made, and withdraw it later if you need to.

If you have savings with the same lender, or sometimes a current account (bank account), and you’re on a flexible mortgage, you can ‘offset’ the money in your account against your mortgage. This helps to reduce the amount of overall interest you pay.

That sounded complicated, but it means you can still keep your savings in a savings account, but then deduct the savings amount from your mortgage amount, and only pay interest on that.

For instance if you have £20,000 in savings, and £100,000 remaining to pay on your mortgage, you would only pay interest on £80,000. You can add or withdraw money from your savings at any time, and the mortgage would adjust accordingly.

So what this means for you then, is two options:

1. You can keep your monthly mortgage payments the same, and because you are now paying less interest per month (the mortgage interest has been reduced from your savings), you will pay more towards the capital part of your mortgage and therefore reduce the loan faster – meaning you will be paying off your mortgage quicker.

2. Or, you could use the reduced interest payments to reduce your monthly mortgage payments and keep the same total mortgage length – the number of years of your mortgage.

Better yet, you may be able to switch between the two options if your lender allows it. Check with your lender to see if this is possible.

This does come at a cost however, which is normally a higher interest rate overall, and you normally won’t be earning interest on the savings. So be careful when considering these types of mortgages – make sure you get expert advice from a mortgage advisor or financial advisor. If you’re unsure where to find a financial advisor, check out Unbiased¹.

When comparing mortgages, it’s important you don’t just look at the interest rate. Look at the overall cost of the fixed rate period, which is the interest rate, plus any fees the mortgage lender might charge for taking out the mortgage.

A mortgage broker can really help here with the sums here. If you’re not sure where to find a good one, here’s the best mortgage brokers, we’ve rated them all. Tembo¹ comes out top – they’ve got great service and you’re guaranteed to get the best deal.

Nuts About Money tip: don’t look at the average rate of the mortgage over the whole mortgage term, just look at the overall cost over the fixed-rated period.

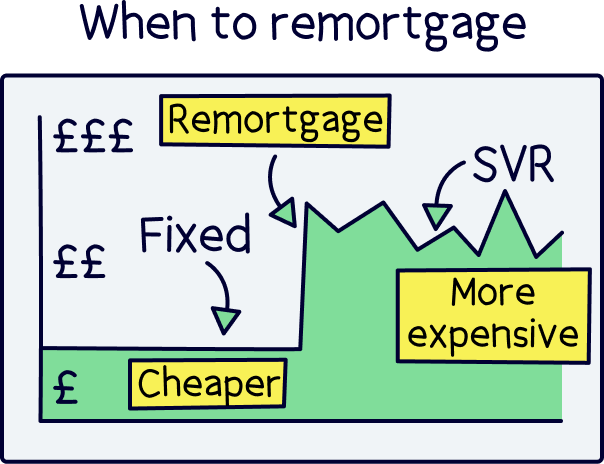

Why? Because with most mortgages, there’s a low interest rate at the start, and when it’s time for you to pay the higher rate (the standard variable rate), when the fixed rate period ends, you can remortgage. That means you can replace your current mortgage on the same property with another mortgage.

So you can go searching again for a new fixed rate mortgage with a much lower rate than your now variable rate, and save quite a lot of money (potentially £100s per month).

Keep on doing this until your mortgage is paid off, it's a bit of work but can save you so much money. Remember, a mortgage broker can do most of the heavy lifting.

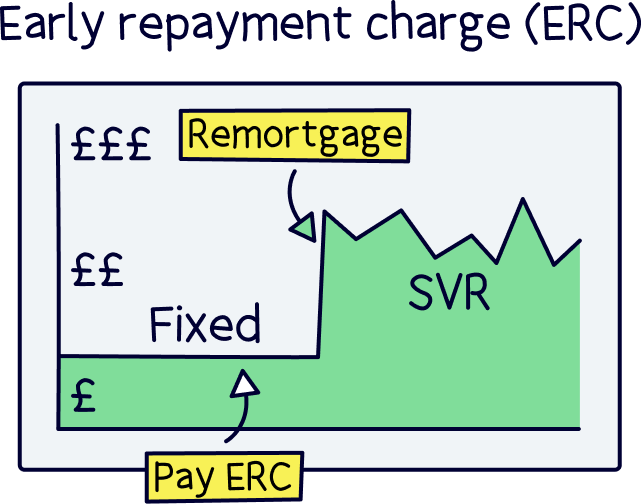

Note: if you remortgage during the fixed rate period, you’ll often have to pay a hefty early repayment charge (ERC). Which can be as much as 5% of your total mortgage.

Keen to get a mortgage? There’s a lot of different types of mortgages available, but don’t panic, you don’t need to know the ins-and-outs of them. There's a super easy way to get the right type of mortgage for you, and the best mortgage deal too.

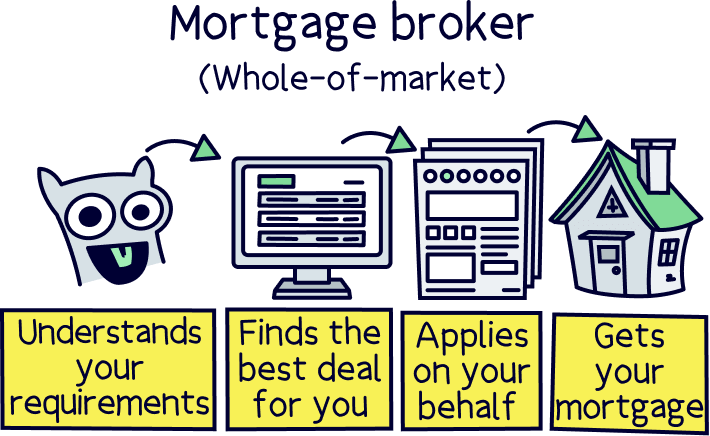

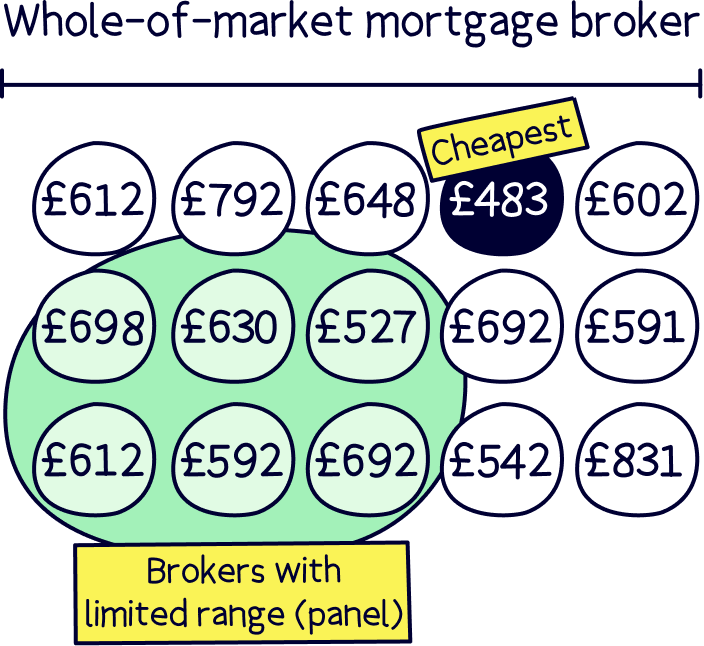

Use a mortgage broker! They’re experts in mortgages and have the tools and knowledge to find the right mortgage for you. There’s over 20,000 mortgages out there, from over 100 mortgage lenders – so it’s quite a feat to try and do this all yourself.

Mortgage brokers (also called mortgage advisors) will also handle all of the paperwork and mortgage application for you too. How great is that? You don’t really need to do much at all.

There’s just one rule when it comes to mortgage brokers – use one that can search the whole market. That means they have access to search all the deals out there for the right one, if they can’t, you can’t be confident you’ll be getting the best deal, and that could mean paying much more than you need to each month (potentially £100s).

If you’re not sure where to find a great mortgage broker, here’s the best mortgage brokers. As a spoiler, the top is Tembo¹ – they’ve got great service and you’ll be guaranteed to get the best mortgage.

And that’s all there is to mortgages and mortgage brokers. Good luck getting the best deal for you and a lovely new home if you’re house hunting!

Tembo will find your best deal, and have award-winning service.

Tembo will find your best deal, and have award-winning service.

Tembo will find your best deal, and have award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, and have award-winning service.