Article contents

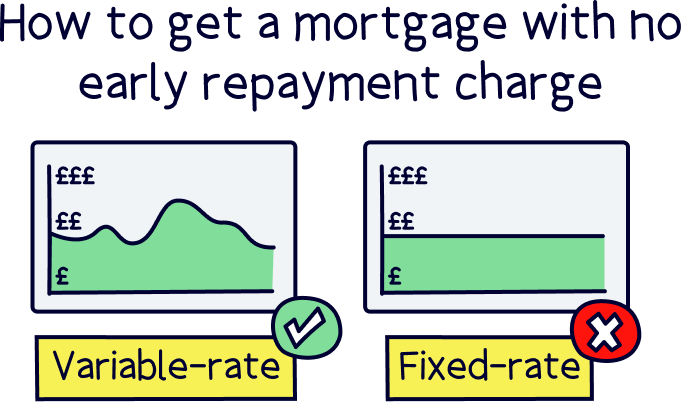

Most mortgages with no early repayment charge are variable-rate mortgages, rather than traditional fixed-rate deals. However, they can be hard to find. If you want a mortgage with no early repayment charge, it’s best to get a mortgage broker to help.

Don’t want to be tied into your mortgage? Want to be able to leave whenever you want without having to pay hefty fees? You’re in the right place.

Here, we’ll look at how to get a mortgage with no early repayment charge and whether it’s worth it. But first...

An early repayment charge, also known as an ERC, is a fee for paying your mortgage back early.

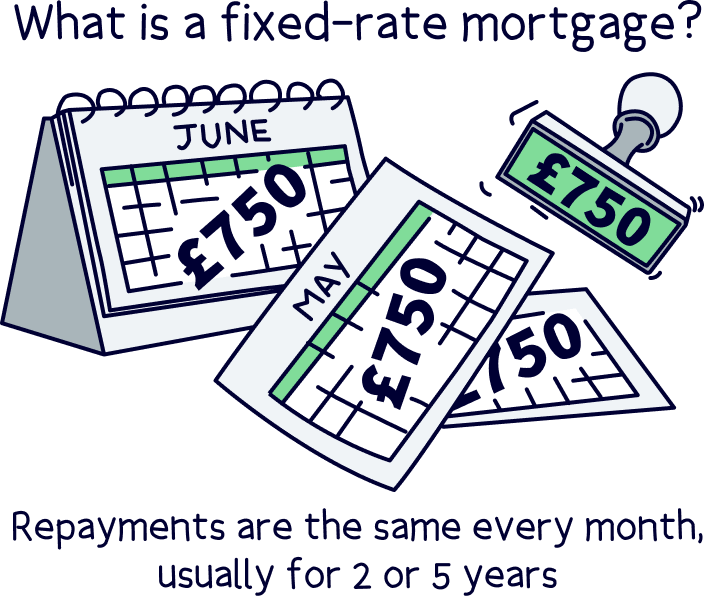

When you get a mortgage, you’ll normally sign up for a deal that lasts a set amount of time. For example, you might get a fixed-rate mortgage, which is where your monthly repayments are set at a fixed cost each month, often for 2, 3 or 5 years. This period is called your incentive period, as your lender will usually give you a cheaper rate to incentivise you to choose them (lenders are the people who give out mortgages).

There’s just one problem. In exchange for these lower rates, you have to agree to stick around until your incentive period is over. If you leave before that, you’ll get charged a hefty fee called an early repayment charge.

Your early repayment charge will normally be a percentage of the amount you owe your lender. Usually, the percentage you have to pay will go down the closer you get to the end of your deal and will be roughly equal to the number of years you have left.

For example, if you have 2 years left of your incentive period, you might have to pay 2% of the amount you still owe your lender. But if you only have 1 year left, you might only have to pay 1%.

Often, people think of early repayment charges as something that only comes with fixed-rate mortgages (remember, that mortgage type where your monthly repayments are set at a fixed cost for a specific amount of time). However, in reality, most mortgage types come with early repayment charges. So, finding a (good) deal without one can be tricky.

Tembo will find your best deal, fast, all with award-winning service.

The best way to avoid the early repayment charge is simply to wait until your incentive period ends before leaving!

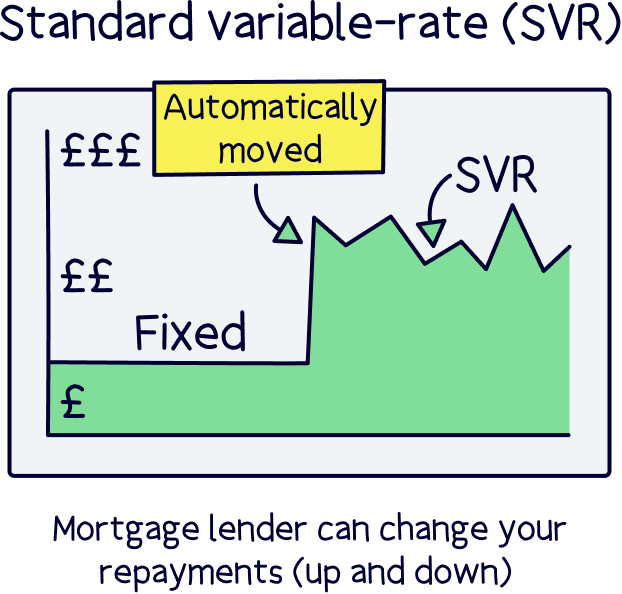

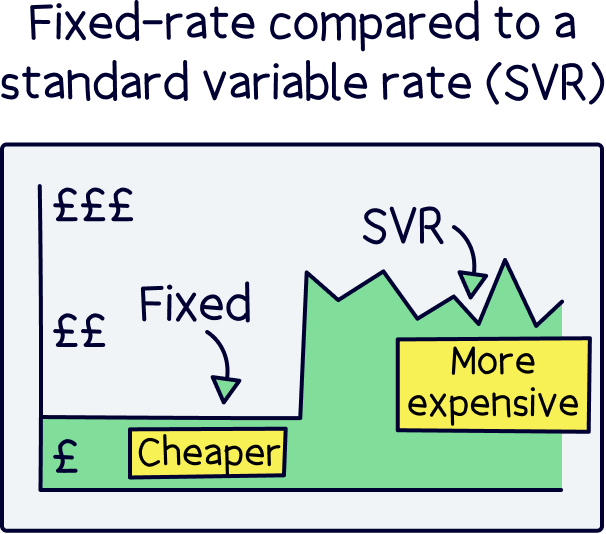

Once your incentive period ends, you’ll automatically be moved onto something called your lender’s standard variable rate (SVR). This is essentially just your lender’s default mortgage rate and once you’re on it, you can leave whenever you want without having to pay any early repayment charge. Hooray!

Just watch out because your lender’s SVR is really expensive! It can also move up and down unexpectedly. Normally, it will move at roughly the same time as the Bank of England’s base rate (that’s the official UK interest rate) but technically, your lender can move it whenever they want.

Basically, your lender will draw you in with a nice juicy deal during your incentive period and then, once it’s over, they move you onto a pretty horrible rate hoping that you either don’t notice or can’t be bothered to switch to a new mortgage deal. Cheeky! In fact, as of September 2020, 46% of mortgage holders were on their lender’s SVR and therefore paying more than they needed to (according to Experian).

If you’re on your lender’s SVR, we’d recommend switching to a new mortgage deal ASAP. You won’t have to pay an early repayment charge and, better still, you could save yourself potentially hundreds of pounds each month by moving to a cheaper mortgage deal.

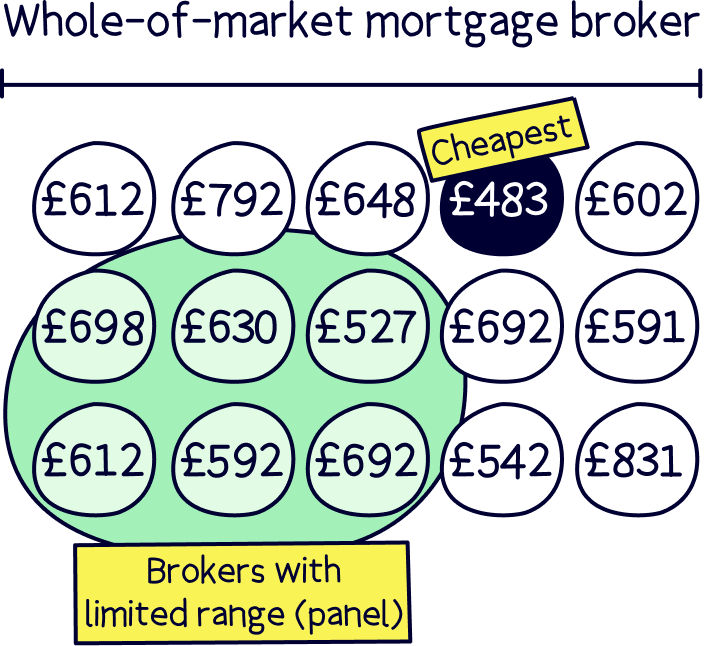

The best way to find a cheaper deal is to use a whole-of-market mortgage broker (also known as a mortgage advisor). They’ll be able to compare all the deals from all the different lenders to find you the cheapest option.

We highly recommend using a mortgage advisor. Check out Tembo¹, they've got award-winning service, and have will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Okay, so we know what you’re thinking. What if you want a mortgage where you can leave whenever you want without having to worry about an early repayment charge? What if you don’t want to be tied in for the duration of an incentive period?

Well, you can get mortgages that don’t come with any kind of early repayment charge. However, if you want a ‘no early repayment charge’ mortgage that’s not your lender’s pricey SVR, it might be difficult. Here, we’ll look at the main mortgage types and whether they come with ‘no early repayment charge’ options.

A fixed-rate mortgage is a mortgage where your interest rate, and therefore your monthly repayments, are set at a fixed cost for a given amount of time (interest is a fee that lenders charge you for the pleasure of borrowing their money).

This is handy because, while your deal lasts, you’ll know exactly what you’re going to be paying each month. In other words, you can rest safe in the knowledge that your lender can’t put your price up. Phew!

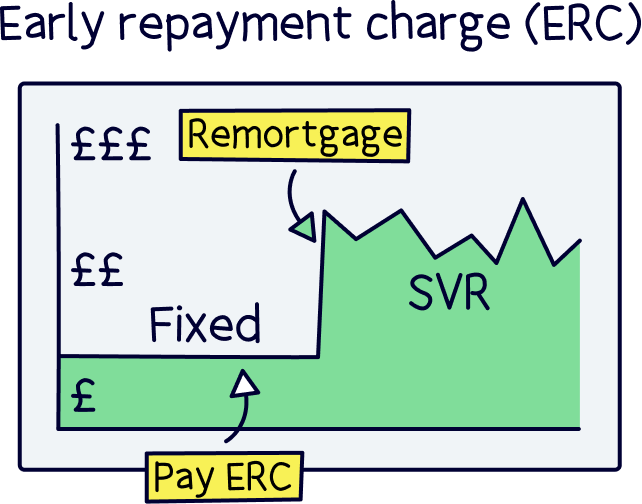

Normally, fixed-rate deals have an incentive period that lasts for 2, 3 or 5 years. This is also known as your fixed-rate period. If you leave during this time, you’ll have to pay the early repayment charge.

After your fixed-rate period comes to an end, you’ll get moved onto that dreaded SVR we told you about. At this point, you can leave whenever you want without penalty (and should leave as soon as possible to avoid having to pay more than you have to!).

It’s really rare to find a fixed-rate mortgage that doesn’t come with an early repayment charge. But there are a few lenders who offer them.

The problem? They tend to be a lot more expensive than other fixed-rate deals and they often come with a ton of other fees. So, to be honest, they’re usually not worth it. The exception is if you have a specific reason for wanting the extra flexibility, for instance, if you’re moving in the next few months. More on this later!

If you’re keen to explore ‘no early repayment charge’ fixed-rate mortgages, a whole-of-market mortgage broker will be able to help. Check out Tembo¹, they've got award-winning service and will find you the best deal. Plus, get 50% off their fee with Nuts About Money.

Your lender’s SVR is your lender’s default mortgage rate. In other words, it’s the rate you automatically get moved to when your mortgage deal runs out.

The good news? It’s the only mortgage type where you’re guaranteed to be able to leave whenever you want without having to pay any kind of early repayment charge. Yay!

The bad news? It’s really expensive and your lender can put your rate up and down whenever they want (okay okay, so normally they tend to move it when the Bank of England’s base rate moves, but they don’t actually have to)! Basically, it’s not a rate you want to end up on if you can help it. Normally we’d recommend taking out a new mortgage deal when your incentive period ends. That way, you can avoid the price hikes and uncertainty that comes with the SVR.

However, if you have a reason for not wanting to be tied into a deal, you could stay on your lender’s SVR for a little while.

For example, what if you’re planning on selling your property in the near future? In this case, taking out a new mortgage that comes with a tie-in might not be a good idea as it will mean you’re hit with an early repayment charge when you leave early. Even though the SVR is expensive, it might be worth paying it for a few months to avoid the early repayment charge when you leave.

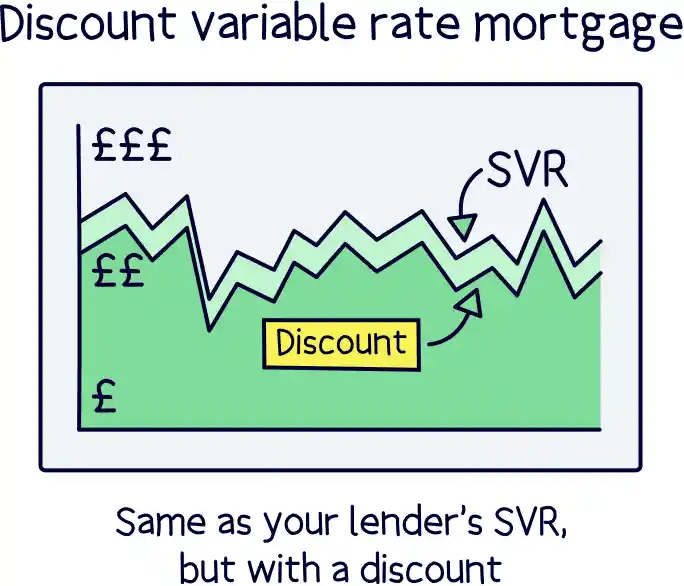

A discount variable rate mortgage is similar to your lender’s standard variable rate, but cheaper. In a nutshell, you just take your lender’s boring (and expensive) old SVR and get a nice juicy discount on it for a set period of time.

Discount variable rate mortgages are often the cheapest mortgages out there. However, they’re riskier than fixed-rate mortgages as your monthly repayments can still go up or down. Yes, you’ll be getting a discount on your lender’s SVR. But if your lender suddenly hikes their SVR up, your rates (and therefore your monthly repayments) will go up too.

Anyway, if you want to leave your deal during your incentive period, you’ll normally have to pay an early repayment charge – just like you would if you were on a fixed-rate mortgage. After your incentive period ends, you’ll automatically be moved onto your lender’s SVR, at which point you can (and should!) remortgage without having to pay those hefty charges (remortgaging is when you switch to a new mortgage, either with your current lender or with a new one).

That said, there are a few lenders out there who do offer discount variable rate mortgages with no early repayment charge. This would allow you to leave during your incentive period with no penalty. The main issue is price.

Just like with fixed-rate mortgages, getting a discount variable rate mortgage that doesn’t come with an early repayment charge is likely to be a lot more expensive. So, it’s a case of balancing up whether low monthly repayments or flexibility is your priority.

If you want a discount variable rate mortgage with no early repayment charge, get in touch with one of those awesome mortgage brokers we told you about earlier. They’ll be able to find the best lender and mortgage for you and your needs.

Tracker mortgages are another type of variable rate mortgage where your monthly repayments can go up or down. However, this time, your lender can’t move your rate around whenever they fancy it. Instead, your rate will be linked to a specific interest rate – usually, the Bank of England’s base rate (remember, that official borrowing rate we told you about earlier?). Although your payments can still go up or down unexpectedly, at least with a tracker mortgage you won’t be subject to the whims of your lender. Always a plus!

Just bear in mind that your rate won’t be the same as the base rate. Instead, it’ll usually be a bit higher. For example, it might be the base rate plus 1%, meaning that if the base rate is 0.25%, your interest rate will be 1.25%.

Most tracker mortgage deals last for an agreed period of time. After this, you’ll be moved onto that expensive SVR we keep banging on about. That means you’ll usually be tied in and will have to pay an early repayment charge if you want to leave early.

However, there are a few tracker mortgages that don’t come with early repayment charges. So, if you’re looking for a mortgage with no early repayment charge, this is where you’re likely to find the best deal.

One kind of tracker mortgage where early repayment charges don’t apply is a lifetime tracker mortgage. This is where your deal lasts for the whole duration of your mortgage, known as your mortgage term. Usually, your deal simply ends either when you reach the end of your mortgage term, or when you sell your house.

If you’re interested in a lifetime tracker mortgage, or any other kind of tracker mortgage with no early repayment charge, we’d always recommend talking to a mortgage broker. They’ll be able to help you decide whether it’s the right option given your circumstances.

As you can see, there aren’t too many options if you want to get a mortgage with no early repayment charge. And, to make matters even more confusing, these options are going to look pretty different depending on what kind of mortgage you want!

Don’t worry though. There are some pros and cons that might be handy if you’re umming and ahhing about whether a ‘no early repayment charge’ mortgage is right for you.

At the end of the day, when you’re making your decision, a lot of it is probably going to be about how likely you are to leave your deal early.

Are you planning on selling your property soon? Or are you expecting a windfall that will allow you to pay your mortgage off early? Then a mortgage with no early repayment charge could be worth it. Yes, it’ll be more expensive in the short term with higher fees and monthly repayments. But it’ll be cheaper in the long run as you’ll avoid having to pay that hefty early repayment charge when you inevitably leave.

Alternatively, is there a good chance you’ll still be in your home in another couple of years? Then you probably don’t need a ‘no early repayment charge’ mortgage. By getting a mortgage that does have an early repayment charge, you’ll be able to benefit from those lovely lower repayments while your deal lasts. And then, once it ends, you can leave without having to pay the penalty. In many ways, it’s the best of both worlds!

If you know that you’re going to be moving house soon, it’s probably not worth tying yourself into a new incentive period. After all, you want to avoid paying that early repayment charge if you can help it!

However, sometimes plans change and there’s always a chance that you end up having to move house when you’re right in the middle of your incentive period. If that’s the case, don’t panic! It doesn’t necessarily mean you have to leave your mortgage or pay that hefty fee.

Instead, most mortgage lenders will let you do something called ‘porting your mortgage.’ This is where, instead of leaving your deal, you can just move it over to your new house.

Don’t get us wrong, this isn’t foolproof. Your lender will want to do some checks on your new home and, if it’s more expensive, they’ll also have to agree to lend you the difference. But it’s still nice to know that it doesn’t have to be a case of staying put or facing the early repayment charge. There is an in-between!

‘No early repayment charge’ mortgages are few and far between and can be expensive. But if you want the flexibility of being able to leave your mortgage whenever you want without having to pay a penalty, they just might be worth it!

If you’re umming and ahhing about what kind of mortgage to get, the first step is to find a mortgage advisor. Not only will they be able to help you choose the best deal. They’ll even sort out your whole mortgage application for you so that you don’t have to lift a finger. You’re welcome!

To recap, if you need to find a decent mortgage broker, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.