Review contents

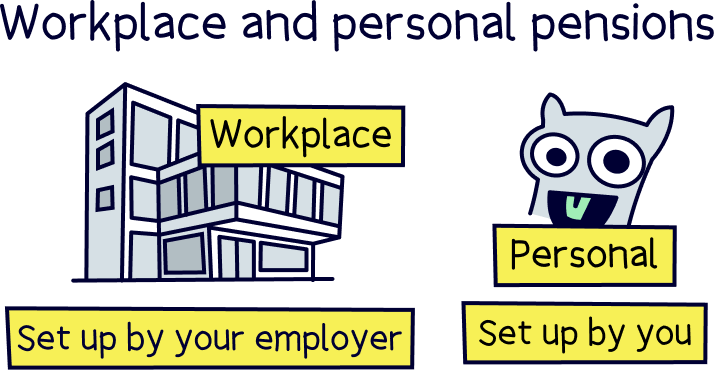

Penfold is a great new workplace pension provider – that’s a pension for employees, set up by their employer. Penfold is easy to set up for your team, and free for employers (employees will pay fees). There’s a good range of pension plans, but the support lets them down.

If you own or manage a company and want to set up pensions for your employees, Penfold could be for you…

However, if you’re looking to set up your own pension (called a personal pension), or if you’re self-employed, you can use Penfold, but it’s not really what they do (they used to, but now they’re focusing on pensions for companies). But don't worry, we have some alternatives for you to consider…

We recommend 5* rated PensionBee¹ – it’s easy to use, low cost and has a great track record of growing pensions. The customer service is awesome too (and you’ll get £50 added to your pension for free with Nuts About Money). Check out the best personal pensions for other great options too.

Penfold then, is a pension you could get if you’re employed, called a workplace pension, and it’s set up by your employer (if they choose to use Penfold). There’s lots of options to choose from, such as Nest (a Government pension scheme), and Aviva (a large pension company).

Penfold is the new kid on the block when it comes to workplace pensions, but they’re pretty great – being technology focused, it’s a breath of fresh air in the pretty boring, and old school industry of workplace pensions…

It’s free to use for an employer, there’s a pretty great app for employees to manage their pension, there’s a good range of pension plans (where your money is invested), which are managed by large investment companies such as HSBC and BlackRock, and their customer support for employers is great (not so great for employees unfortunately).

We’ll cover all those in detail below, but as a quick recap, Penfold is primarily for employer pensions – there’s better options for you if you’re looking to set up your own pension, check out the best personal pensions if you are.

If your employer has decided to use Penfold for your workplace pension, and you’ve got old pension(s) from old jobs lying around collecting dust, you might be considering moving them to your new Penfold pension.

This can be a great idea as you’ll have all your pensions in one place. However, the drawback is you won’t be able to move them again until you change jobs – so you need to be sure Penfold is the best option for you.

Often, we recommend moving your old pensions to a personal pension – that’s one that you choose, open and look after yourself, meaning you can contribute to it whenever you like, and transfer old pensions over too. You can move it to another provider whenever you like, so you can always be with the best provider – one that’s easy to use, low cost and a great track record of growing pensions.

There's no reason to just use your employer's default pension when you have a choice. If you were looking at renewing your phone contract, you would have a look at your options right? With pensions you can do the same!

Our top recommendation for a personal pension is the 5* rated PensionBee, for all of those reasons above, and they’ll handle everything to do with your pension transfer – with a dedicated customer service person just for you (Penfold don’t offer this, only for employers).

You’ll also get £50 added to your pension if you sign up with Nuts About Money, just get started on the PensionBee website¹.

You can also check out all the top options with our guide to the best pension providers.

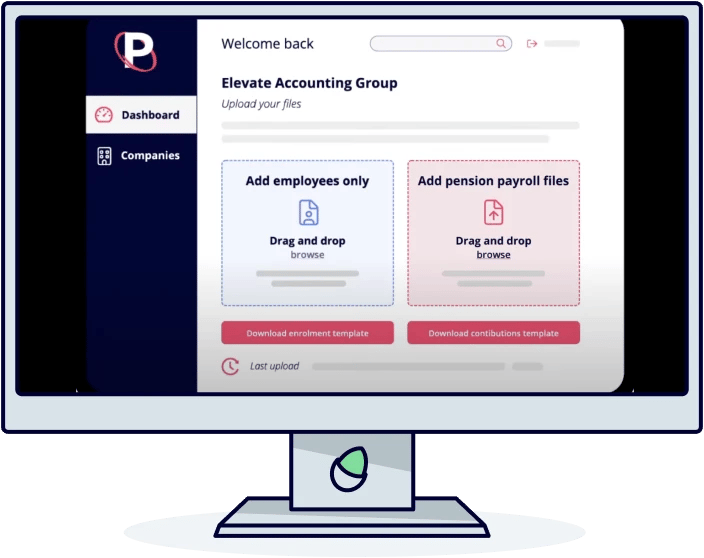

For employers, Penfold is great – you can handle everything you need to, all within an easy to understand platform (their website).

You’ll be able to manage payroll pension contributions (so all the admin to do with employees pay and their pension contributions), including keeping track of all payments, manage employees who want to opt-out (not receive the pension) and view the total contributions from the employer too.

You’ll be able to upload all the necessary documents, and this will be checked to make sure it’s accurate before any actions are taken (e.g. making payments). For instance uploading all of your employees data in one go, rather than one by one!

You’ll also get reminders when you’ll need to do things, such as making payments and re-enrolment.

Plus, it’s not just the tech and pension you get, you’ll get a dedicated customer service rep to help you with any questions or issues (9am to 6pm on weekdays).

You’ll also be able to opt for salary sacrifice for your employees. That’s where your employees salary is reduced to account for the pension payments, and therefore both employees, and you as an employer, can benefit from lower National Insurance contributions.

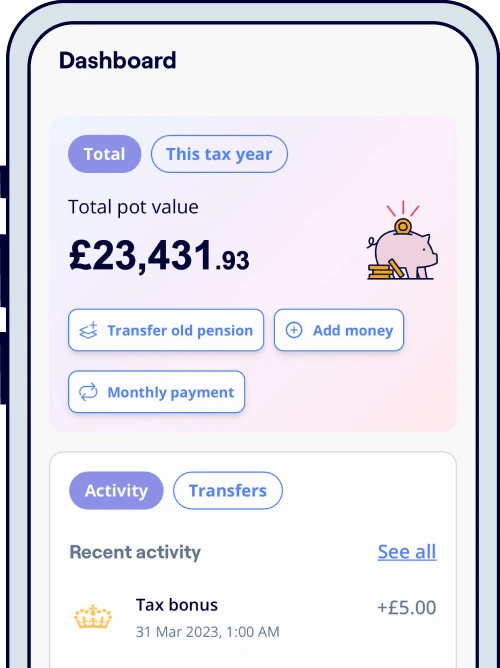

As an employee, you’ll be able to manage everything on the phone app and website – it’s pretty easy to use, and you’ll be able to see all of your pension contributions and how much is in your pension (whenever you like too).

On the app, you’ll be able to pick which pension plan you want to use – that’s where your money will be invested, there’s a range of different options which should suit most people. We’ll cover those just below.

Penfold is typically for companies that give their employees a pension. If you want your own pension, here’s some great options…

A pension plan isn’t complicated, don’t worry! It’s just how and where your money should be invested, based on your preferences.

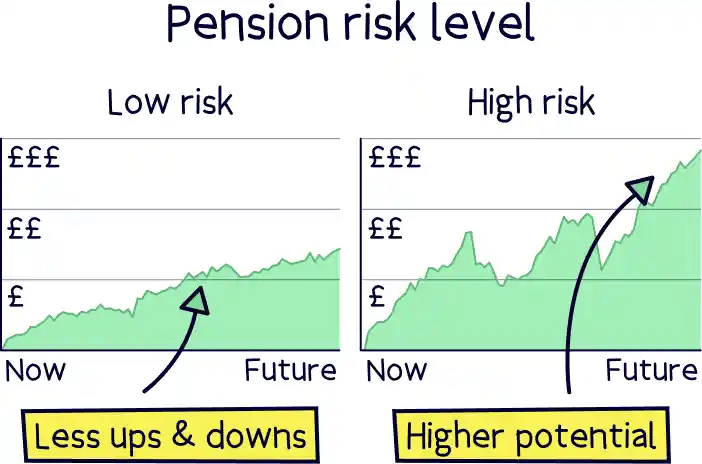

For example, what type of investments you’d like, for example, only investing in ethical companies. And, a risk level…

A higher risk level means your money will have bigger ups and downs over time, but has the potential to grow more, whereas a lower risk option has smaller ups and downs, but isn’t as likely to grow as much over time.

Typically, if you’re young(ish), you might opt for a higher risk option, and when nearing retirement, opt for a lower risk option – but it’s completely up to you.

The 3 plans are:

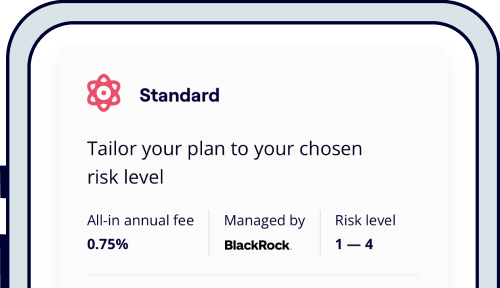

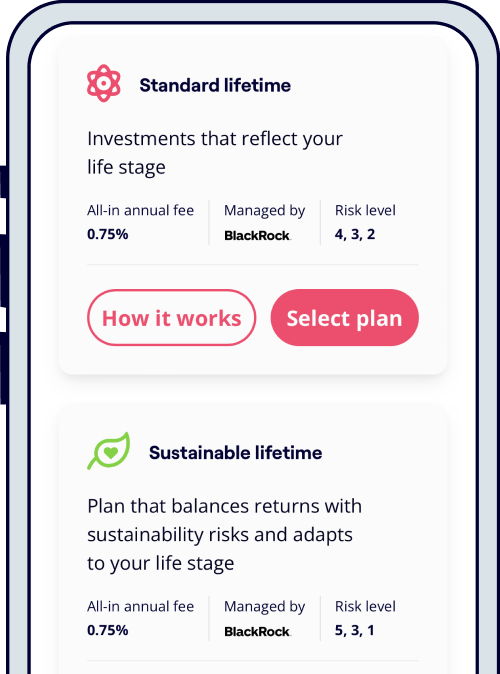

The most popular plan, choose a level of risk from 1 to 4, and that’s it.

Your money is invested in companies that make a positive impact on the world. So no harmful companies increasing global warming or affecting people's health.

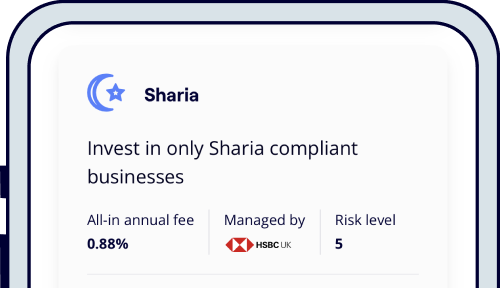

This means your money will only be invested into companies that adhere to Islamic principles. For example, no gambling, alcohol, and tobacco companies.

The Standard and Sustainable plans can be lifetime plans. This automatically adjusts the investments as you age, moving from higher risk (young people) to lower risk (older people) over time.

Ok, we know what you are thinking, this all sounds great but how much does it cost? Good question!

For employers, it’s completely free – that’s great news for you, but there are fees for your employees…

For employees, depending on what pension plan you choose, they charge a fee of 0.75% or 0.88% per year of your total pension.

If you’re lucky enough to have over £100,000 saved, any figure above this is charged at 0.40% or 0.53% (Shariah plan).

There’s no fees to transfer an old pension to Penfold either, or for making any extra payments into your pension.

That’s a pretty reasonable fee for a pension – pensions can range anywhere from 0.30% per year to 1.5%+, it all depends on the company.

Fees are important, but so are the investments on offer (the pension plans), how good the service is, and how easy it is to use (for instance being able to manage everything on a mobile app).

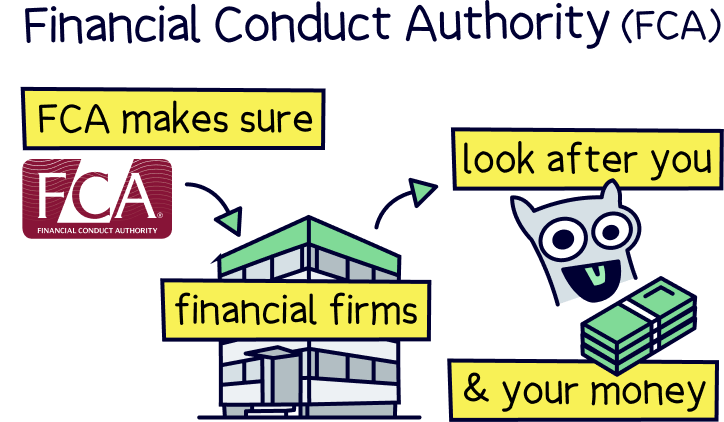

Yep. Penfold is completely safe to use as a pension provider. Pension companies have to be regulated by the Financial Conduct Authority (FCA), they’re the people who oversee financial services firms and make sure you are treated fairly and correctly.

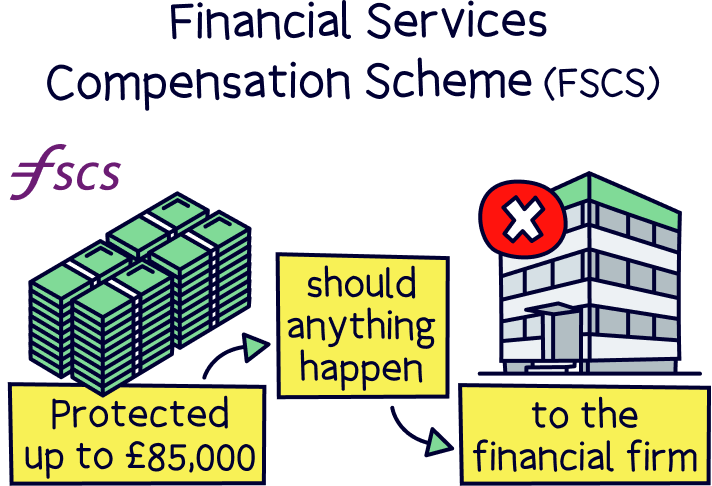

That also means your pension is protected by the Financial Services Compensation Scheme (FSCS) – which means you’ll get up to £85,000 in compensation should Penfold go out of business.

However, even if Penfold were to stop operating, your pension would still exist. Penfold are effectively the middle-man between you and where your money is invested, called funds, which are managed by some of the biggest players in investing – BlackRock and HSBC. That means your money would still be within those investments, all in your name, and can only be returned to you.

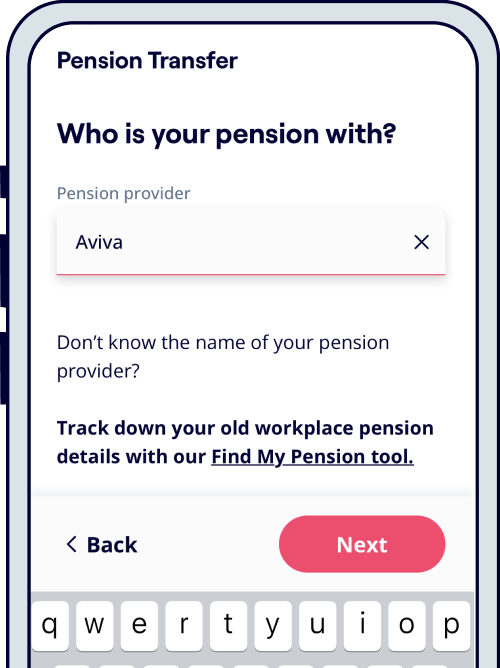

If you’re lucky enough to already have a pension(s) you can transfer it to Penfold by using their Pension Finder tool so that all your pension money is in one place (this is called pension consolidation).

This can take a few months but don’t worry, Penfold will handle everything and keep you updated and let you know when it’s all been transferred over.

However, it’s not necessarily a good idea to move old pensions over to a workplace pension, as even though your pension would be in the same place, you can’t move it until you change jobs – and you may find your new workplace pension isn’t the best, with high fees, and bad investment performance.

As mentioned, we typically recommend moving your old workplace pensions to a new personal pension, that’s a pension you set up yourself, rather than your employer. That way, you can pick the best provider for you, one that’s easy to use, has low fees and a great record of growing pensions, it also means you can move it again whenever you like.

Our top recommendations are PensionBee¹ (get £50 added to your pension for free with Nuts About Money), and Beach¹, they offer a tax-free Stocks & Shares ISA¹ managed by a team of experts and a pension pot¹. It's also easy to use with a great app. Here’s our Beach review to learn more.

Your pension is locked away until you’re at least 55 years old (57 from 2028), after that you can start withdrawing from it if you like, or wait until you retire (although the amount you can still pay in each year will reduce to £10,000).

We recommend letting it grow as much as possible until you retire. When you do decide to retire, you can keep your pension with Penfold, and start withdrawing from it directly, this is called pension drawdown.

Typically, you might opt to buy an annuity, which is a guaranteed income for the rest of your life, or a set period of time (e.g. 10 years). Or withdraw from your pension directly as and when you like. The choice is yours – but it’s always good to speak to a financial advisor before making a decision.

You also don’t have to keep your pension with Penfold when you retire, you can move it to any pension provider you choose. To find out more, visit the best pension drawdown providers.

The customer support for employers is good, but unfortunately not quite as good for employees.

As an employer, you’ll get a dedicated account manager who can help with any issues you might have – and guide you through the whole process to get set up. You’ll be able to phone them 9am to 6pm during the week.

For employees, there’s an online help centre, with lots of common questions answered. And if you need a bit more support, there’s a live-chat function on the app, or on the website, and you can chat with the support team after a while. They’re available during the week, from 9am to 6pm. Unfortunately, you can’t speak over the phone with anyone.

Typically the reviews around customer service aren’t great, with reviews mentioning slow responses, and messages unanswered. Common issues include long wait times to transfer pensions away from Penfold when changing jobs (taking several months).

When looking at customer service, we like to use Trustpilot, a popular reviews website.

On Trustpilot, Penfold has a rating of 4.2 out of 5, that’s good, but not the best.

There’s many reviews about the customer service being fairly poor for employees and those who have transferred pensions, or self-employed people. Although there’s lots of great reviews too, mentioning how easy it is to use, and the great phone app.

Let’s run through the pros and cons of Penfold.

We think Penfold is a great option for employers looking to set up a workplace pension scheme, and it’s modernising workplace pensions too – with a great app for employees to use and track their pension, rather than old school paperwork once a year.

It’s easy for employers to get set up, and they get an account manager to handle any questions and issues, and guide them through the process.

The pension plans for employees are good, and easy to understand, and the app itself is great to track the investments and the total pension pot size.

If you’re self-employed, or want to set up your own personal pension, it could be a good option, but you may want to consider a dedicated personal pension provider, such as PensionBee¹, who can provide you with better service (a dedicated customer service person), alongside a great app, and a great record of growing pensions over time.

For all the top options, check out the best personal pensions.

If you’re considering moving an old workplace pension(s) over to your new pension with Penfold, it could also be a good idea, but bear in mind, your money would have to stay with Penfold until you change jobs…

We recommend transferring old pensions to a personal pension, where you have full control over which provider you use, so you can pick one with low fees and easy to use, and then you have the option to switch pension provider whenever you like too.

Overall, we like Penfold, the app and website is good, but the personal service for employees lets it down. 3 stars from us. If you want to learn more and get started, here's the Penfold website.

Penfold is typically for companies that give their employees a pension. If you want your own pension, here’s some great options…

Penfold is typically for companies that give their employees a pension. If you want your own pension, here’s some great options…

Penfold is typically for companies that give their employees a pension. If you want your own pension, here’s some great options…

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Penfold is typically for companies that give their employees a pension. If you want your own pension, here’s some great options…