Access your money with 30 days notice. All available online and have FSCS protection. Interest rates are AER* variable.

32 days. Account is with Kroo Bank Ltd through Raisin. More top rates available via the platform.

32 days. Read Moneybox review.

Access your money with 45 days notice. All available online and have FSCS protection. Interest rates are AER* variable.

Access your money with 60 days notice. All available online and have FSCS protection. Interest rates are AER* variable.

Access your money with 65 days notice. All available online and have FSCS protection. Interest rates are AER* variable.

Account is with a leading bank through Raisin. More top rates available via the platform.

Access your money with 90 days notice. All available online and have FSCS protection. Interest rates are AER* variable.

Account is with a leading bank through Raisin. More top rates available via the platform.

Access your money with 95 days notice. All available online and have FSCS protection. Interest rates are AER* variable.

Account is with a leading bank through Raisin. More top rates available via the platform.

Access your money with 120 days notice. All available online and have FSCS protection. Interest rates are AER* variable.

Access your money with 180 days notice. All available online and have FSCS protection. Interest rates are AER* variable.

All data is sourced by Nuts About Money, or provided directly by the provider. Seen something inaccurate? Get in touch.

Finding a top interest rate for your hard earned cash can be quite challenging – there’s lots of providers (such as banks), but they don’t all offer great rates – in fact, often the bigger the bank, the lower the interest rate is!

We’ve tracked down all the top accounts we could find to put together our best buys for notice savings accounts.

Here’s the criteria we looked at:

For this table of best buys, we’ve just looked at notice accounts (where you give ‘notice’ to get your cash back after a set number of days). But we’ve also looked at:

All the savings accounts we’ve featured are available nationwide, and can be opened online, via a website or mobile app. And, they’re all protected by FSCS, where your money is protected up to £85,000 (we’ll cover that more below).

So, whichever one you choose from our list – you can be sure your money is safe, and with one of the best options available.

Interested in learning more? Here’s our full review methodology and how we test.

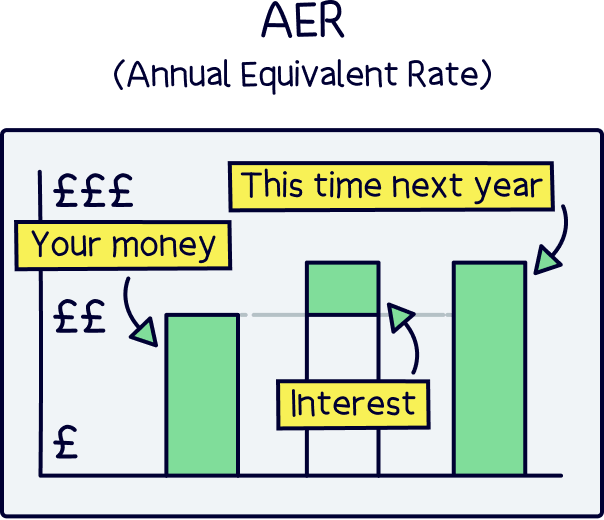

AER stands for Annual Equivalent Rate, and is how much you’ll earn in interest from your savings account at this point in a year's time (12 months).

It includes any interest you earn as time goes on (e.g. if interest paid monthly), and the interest that the interest makes (technically this is called compound interest) – to summarise, it's the total you’ll have after 1 year.

So, if the AER is 3%, you’ll have earned 3% in a year’s time.

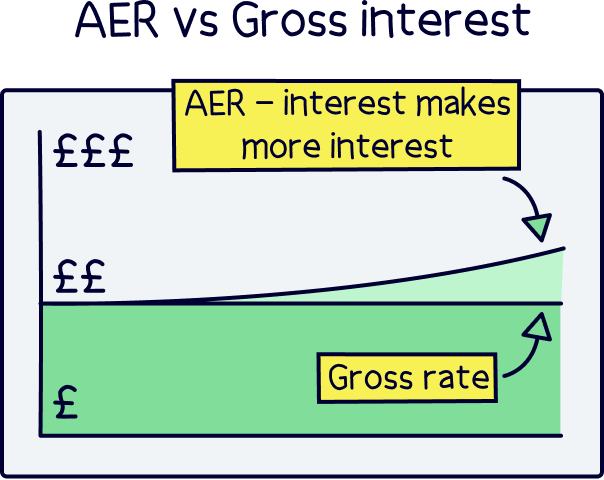

The gross rate doesn’t include any interest that your interest makes (the compound interest side of things). It’s technically how much the account pays in interest, rather than how much you’ll make (which is the AER). So it’s slightly less than the AER.

That’s why it’s not a good idea to compare the gross rate with AER – it’s better to pick one to compare different savings accounts with each other (and most likely AER).

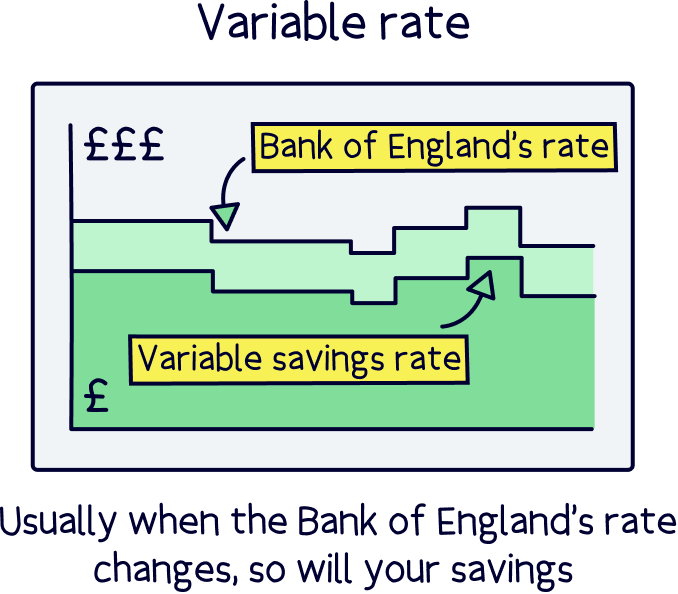

Variable rate means the interest rate can change over time (the account provider (company) will decide when it changes).

Often, you’ll find the interest rate is linked to the Bank of England’s base rate (which is the interest rate the Bank of England gives the banks for saving cash), and so when that goes up or down, usually so does the interest on savings accounts.

A fixed rate is where the interest rate doesn’t change – it is set for however long is agreed (for instance 1 year). These are often called fixed rate accounts (rather than notice accounts, which are typically variable rates).

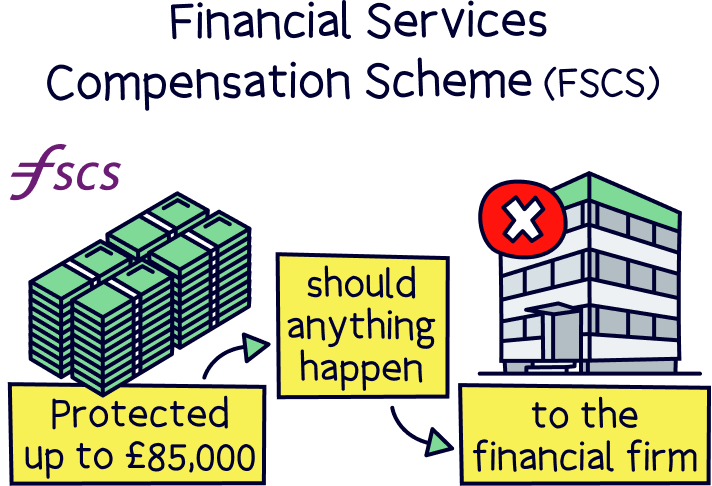

The Financial Services Compensation Scheme (FSCS) is like insurance on your savings – if something went wrong, such as the account provider going out of business and didn’t return your money, the FSCS would step in, and give you your money back.

There’s a limit of up to £85,000 per account provider – so those with more could spread this out with different providers to ensure all their cash is protected.

Although it’s very unlikely you wouldn’t get your money back if a provider did go out of business anyway, as your money is typically held entirely separate from the business’s money, held in your name, and can only be returned to you.

A notice account isn’t your standard savings account, where you add cash and take it back out whenever you like (often called an easy access account).

Instead, when you open the account, you agree to save your money in the account, and only access it after giving ‘notice’, which is a notification that you want some or all of your money back – and this is typically a set number of days (e.g. 30 days notice).

That means it’s also different to a fixed-rate savings account, which is where your money is locked away for the whole period (e.g. 3 years), and you typically can’t access your money until the end of the period.

So, you can keep your money in a notice account indefinitely, and make the most of the (hopefully) high savings rate, and get your money back by giving notice.

Are notice accounts for you? Let’s run through the pros and cons.

Saving into a notice account might mean you’ll pay tax on your interest – if it’s not in a tax-free ISA (e.g. a Cash ISA), where everything will be tax-free.

Instead, you’ll pay tax on your interest based on how much interest you make, and your income (e.g. your salary from your job). It’s taxed just the same as your income.

However, before you pay any tax, you’ll get a Personal Savings Allowance (PSA), which is an annual limit of how much interest you can make before paying tax (on your interest) – and the limit depends on how much you earn.

The limit runs for the tax year, which is from April 6th to April 5th the following year.

Here’s the income levels and allowances:

That means that if you earn (from your income such as a job) below £50,270, you’re able to earn £1,000 in interest each tax year, tax-free.

If you earn over £50,270, but less than £125,140, you’ll be able to earn £500 in interest before paying tax, and if you’re fortunate to earn over £125,140, you’ll unfortunately pay tax on all the interest you earn (from a savings account that isn't a tax-free ISA).

If you earn less than £17,570 per year, there’s something called the ‘starting rate for savings’ which will apply to you. It’s where all the interest you’ll earn is tax-free – until the interest pushes your income above £17,570.

It’s an additional £5,000 allowance for earning interest tax-free, which is in addition to your Personal Allowance of £12,570 (how much you can earn in general without paying any tax on your income).

It’s a bit confusing, but for every £1 you earn above £12,570, your tax-free allowance for interest will reduce by £1, all the way up to £17,570 (so up to £5,000 tax-free).

There we have it for notice accounts – not too complicated are they?

They’re more flexible than a fixed-rate savings account, where you lock your money away for a set period of time, and you can keep saving for as long as you like (rather than the end date of a fixed-rate account). But they're not as flexible as an easy access account, where you can get your money back whenever you like.

With a notice account, you’ll have to give ‘notice’ to the savings provider to get your money back out – which is a set number of days you agree to when you open the account, and it’s typically from 30 days to 180 days.

We’ve reviewed all the top notice accounts we could find, to make things easy for you, and they’re all in the table above – with some of the very best savings rates out there. Plus, you can open them all online (via a website or app).

And that’s it. Happy saving!

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things savings, with many years of combined experience writing and talking about savings (and ISAs). Some of our team were top financial advisors. We understand the ins and outs of planning your finances well, how to communicate savings in an easy to understand way (we hope you agree), and of course, how to get the best savings rate for you.

More than 20 years of combined experience researching and writing about savings

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of savings companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Raisin makes it simple to compare and open savings accounts in one place, helping you secure the best rates.