Article contents

Yes, you can use cryptocurrencies to pay your mortgage deposit, but you’ll need to convert them into pound sterling first. You’ll also need to prove that there’s no evidence of money laundering, which can be a little tricky!

Have you made money from cryptocurrencies like Bitcoin, Ethereum or Dogecoin? Congrats!

Bitcoin and other cryptocurrencies have made lots of people millionaires. But whether you’ve made millions or just a few hundred from them, you’re going to want to spend your profits at one point or another. If now’s the time, a new pad is likely to be at the top of your wishlist.

Here, we’ll reveal whether you can use cryptocurrencies as a mortgage deposit, evidence of income, or to simply pay your mortgage off. Here goes!

Tembo will find your best deal, fast, all with award-winning service.

Okay, so first things first, can you use a cryptocurrency such as Bitcoin for your mortgage deposit or downpayment?

Well, you can’t pay the deposit in actual cryptocurrency. Sorry! But if you convert it into pound sterling by selling it then yes (by using a crypto exchange), you can use your cryptocurrency profits to put down a deposit for a home. Woohoo!

However, before you get too excited, there’s some less good news too. Because cryptocurrency is so new, a lot of lenders haven’t yet decided where they stand with it (lenders are the people who give out mortgages). Many will turn you away point blank if you want to pay your deposit using cryptocurrency profits. Urgh.

If you’re wondering ‘Why would a lender care where I got the deposit money from?!’ then we don’t blame you. To cut a long story short, it’s all to do with money laundering (that’s what it’s called when someone hides money that’s been gained illegally).

Basically, lenders need to be able to confirm where the funds you’re using for your mortgage deposit have come from, to make sure you’ve got them legally. This can be really hard if you’re using cryptocurrency, especially because this kind of money is unregulated (not controlled by laws or regulations) and therefore in the riskiest category for money laundering.

Don’t get us wrong, we trust that your Bitcoin is squeaky clean. But mortgage lenders need to be absolutely sure. So, there are fewer lenders out there who’ll be happy to let you pay your deposit this way. And even the ones who are happy will have to do some very strict checks on your money first. Which brings us onto…

If you want to stand a chance of paying your mortgage deposit out of cryptocurrency profits, you’ll need to be able to show your lender how you got your cryptocurrency, how you sold it and that you’ve paid any necessary tax on it.

This might involve giving them bank statements and statements from the cryptocurrency platform. It might also mean getting a forensic accountant involved if you’re dealing with large amounts that are particularly hard to trace (forensic accountants are people who specialise in finding out whether any dodgy financial reporting has taken place).

Often, lenders will even refer you to their financial crime unit (a unit whose job it is to prevent money laundering) so that they can do even stricter checks on your money. It sounds scary but don’t worry, as long as your cryptocurrency is above board, you should be absolutely fine!

That said, because this cryptocurrency malarky is so new, most lenders don’t yet have a set criteria for approving or rejecting mortgage applications. Instead, most will make a decision on a case-by-case basis.

To give yourself the best possible chance of being accepted, we’d strongly recommend working with a ‘whole of market’ mortgage broker (also known as a mortgage adviser) who can compare mortgage deals from lots of different lenders and advise you on which would be best for you.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best deal. You'll also get 50% off with Nuts About Money. How great is that?

To tell you the truth, we always recommend working with a mortgage broker, even if you aren’t using cryptocurrencies. But it’s even more important if you are, because they’ll know from experience which lenders are most likely to accept your cryptocurrency profits and what they’re looking for. This will help you avoid getting rejected, which could negatively affect your credit score and make it harder for you to get a mortgage in the future (your credit score is a number that shows lenders how good you are with money).

In summary, mortgage brokers are the superheroes of mortgages and, if we were you, we wouldn’t want to be without one. Just saying!

We hate to be the bearers of bad news, but at the moment, lenders won’t take cryptocurrency into account when they’re assessing your income and affordability. Sorry!

If you’re wondering what we’re going on about, then let’s rewind a little.

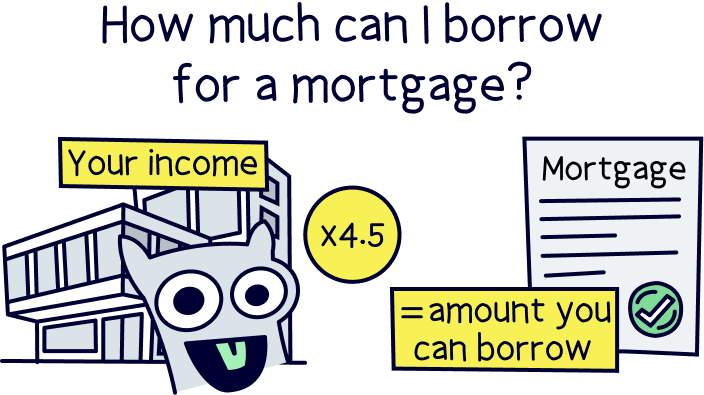

Basically, when lenders are deciding whether to give you a mortgage (and how big a mortgage to give you), they’ll carry out affordability checks. This pretty much just involves looking at your yearly income and expenses to decide whether or not they think you’re going to be able to afford your monthly mortgage repayments.

Normally, lenders will be happy to lend you around 4.5x your yearly income. In other words, if you’re earning £20,000 a year, they’ll probably let you borrow around £90,000 (20,000 x 4.5 = 90,000).

If you’re trading in cryptocurrencies, it makes sense that you’d want to declare your cryptocurrency balance as income so that you can get a bigger mortgage. However, sadly, this isn’t possible right now.

Why? Well, not only is it hard for lenders to trace where your money’s come from. But cryptocurrencies like Bitcoin are also really volatile. In other words, lenders are worried that the value of your cryptocurrency could drop and cause you to struggle to pay your mortgage. Exactly what they don’t want!

As cryptocurrencies become older, the market might become more stable and then, who knows, mortgage lenders might be happy to include them in their affordability assessments. But for now, it’s just not meant to be.

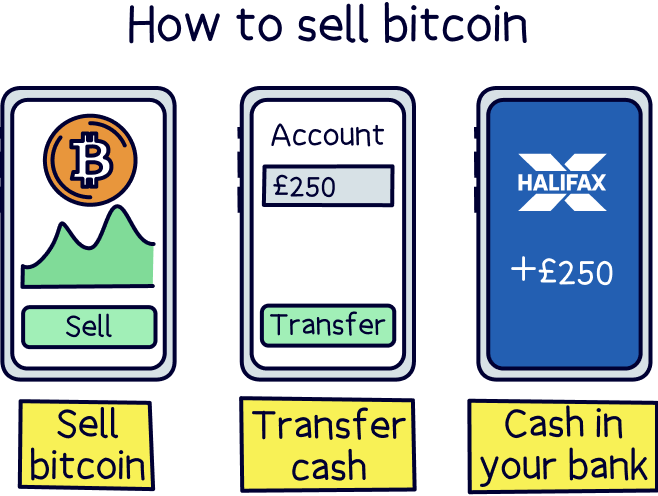

Yes! We mean, you can’t actually pay your mortgage lender in Bitcoin, but if you sold it to convert it into pound sterling then yes! You could use your Bitcoin to pay your mortgage.

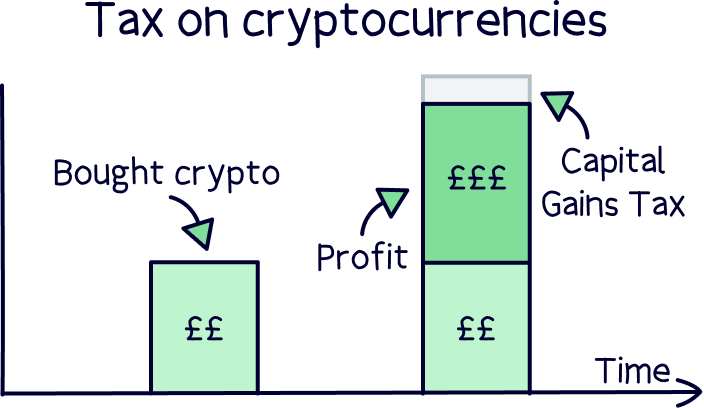

Just bear in mind that you’ll need to declare any profits you make from Bitcoin (and any other cryptocurrencies) to HMRC (the guys at the government who deal with taxes). Otherwise, you won’t be doing so legally and if your lender gets wind of it, they could file a Suspicious Activity Report which could put you in a bit of a pickle.

Paying the right amount of tax on cryptocurrency can actually be pretty complicated because trading it can trigger income tax but selling it as an investment comes under capital gains tax (a tax you have to pay when you sell an asset).

Ultimately, if you’re not sure whether you’re paying the right amount of tax, we’d recommend getting an accountant to help you out. That way, you can rest safe in the knowledge that you’re paying your mortgage legally.

Theoretically, yes, you can pay off your mortgage using Bitcoin (again though, you’ll have to sell it to convert it into pound sterling first!).

We say theoretically because, if you’ve got enough money to pay off your mortgage in one big lump sum, your mortgage lender is going to want to check where your money has come from before they accept it. This is all about making sure that no money laundering has taken place (we know, we know, we’ve gone on about this a lot. But they do need to be careful!).

If they see that your money has come from selling cryptocurrency like Bitcoin, they’ll need to be even more careful because of all the things we’ve mentioned before (you know, the fact that cryptocurrencies are unregulated and hard to trace). So, you’ll need to be able to show them a clear trail of your cryptocurrency trading and that you’ve paid all the right taxes on it. Otherwise, they’re just not going to want to take your money.

Assuming you can do all that then yes, you should be able to pay off your mortgage with Bitcoin and enjoy life mortgage-free. Well done you!

At the end of the day, there’s not much point in making £££s from cryptocurrencies if you’re never going to spend your profits.

If you’re keen to use your cryptocurrency profits to put down a deposit on a new pad, the first step is to find a mortgage advisor. They’ll be able to show you which mortgage lenders are most likely to approve you, which deals are the best-value, and what you need to do to pass all those anti-money laundering checks.

Getting approved for a mortgage with cryptocurrencies isn’t easy, but a mortgage broker will make it a whole lot easier. And we promise: when you’re sat on the floor of your brand new home with a takeaway in your lap and a glass of bubbly in your hand, it’ll be oh-so-worth it!

As a reminder, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Get 50% off their fee with Nuts About Money too.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.