Article contents

Yes! Lots of lenders will be willing to offer you a mortgage as a foreign national. You’ll still need to meet certain criteria though!

Are you a foreign national living in the UK? Are you dying to get a mortgage so you can buy the house of your dreams here? Well, we have some good news for you: it’s totally possible. Here’s all you need to know about mortgages for non-UK citizens.

Let’s start at the very beginning. When we talk about foreign national mortgages, we’re talking about mortgages for non-UK citizens. And when we talk about non-UK citizens, we’re basically talking about anyone who doesn’t have a UK passport (or the right to one).

Sound like you? If the answer’s yes, chances are you fall into one of these three groups:

We’ll take a look at what that means for you when it comes to getting a mortgage in just one moment. But first, let’s be totally clear about one thing: getting a foreign national mortgage has nothing to do with whether you’re actually allowed to buy a house in the UK. Anyone can buy a house no matter where they’re from! Getting a mortgage is just about how you fund it.

Tembo will find your best deal, fast, all with award-winning service.

Yes, most lenders will be happy to offer mortgages to foreign nationals. Woohoo!

However, depending on your circumstances, there might be more hoops to jump through than there would be for a UK citizen. We’ll look at some of these below, but before you get out your notebook and pen, bear in mind that every lender is different. And, to make things even more complicated, there are over 100 lenders in the UK!

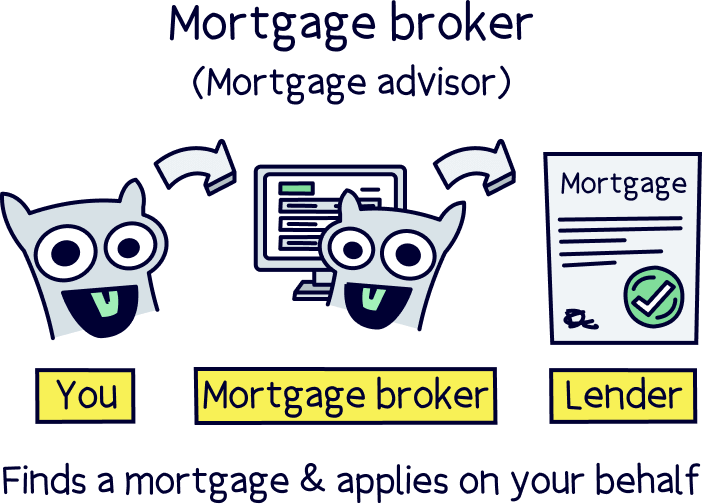

All this is to say that if you don’t fit the standard criteria, don’t panic. There may well be a lender out there that would still be willing to give you a mortgage. Just get in touch with an independent mortgage broker (also known as a lifesaver!) and they’ll be able to point you in the right direction!

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

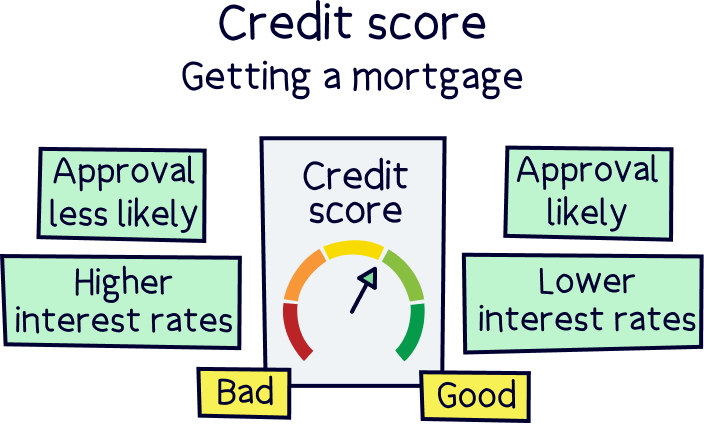

If you have the right to live in the UK permanently, that’s great news for you! It will make things a whole lot easier when it comes to getting accepted for a mortgage. Here are the main things that lenders will usually look at...

Don’t have permanent residency in the UK? All is not lost.

You might still be able to apply for a mortgage if you’re on one of these visas...

If this sounds like you then hopefully, you’ll be able to get a mortgage before you know it. Just bear in mind that you’ll still need to tick all the boxes that a non-UK citizen with permanent residency will need to tick. That means opening a bank account in the UK, living here for a while as you build up your credit score and preferably putting down a decent deposit. Good luck!

Are you an EU citizen? If so, you’re probably tired of hearing the word ‘Brexit.’ But we’re going to need to use it here anyway (sorry!).

Historically, EU citizens have found it super easy to get a mortgage in the UK. That’s for a mix of reasons, including the fact that EU citizens were able to live in the UK without a visa. And the fact that UK lenders could trace their credit histories without too much trouble.

Most EU citizens were able to get a regular UK mortgage just by:

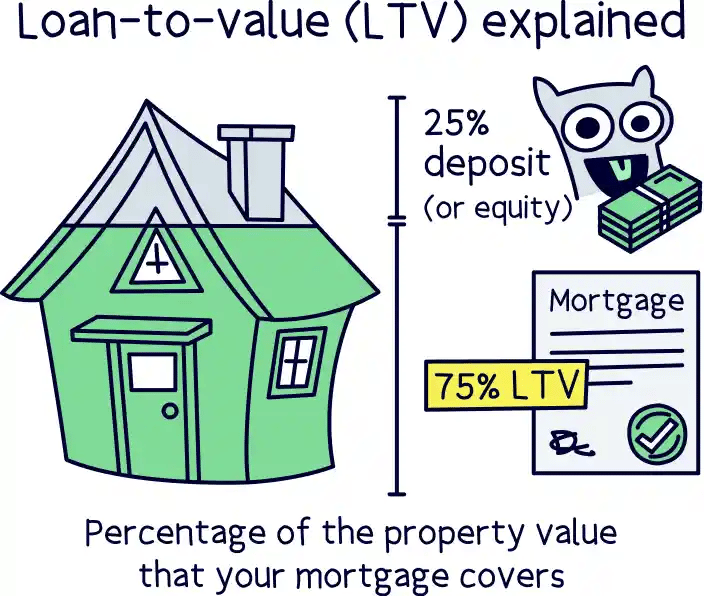

The chances are it’s not going to be quite as easy now that the UK is no longer a part of the EU. For example, mortgage lender Santander has already announced that it will only give out mortgages of over 75% LTV to citizens of the European Economic Area if they can prove they’re permanent residents of the UK (check out the full article in the Financial Reporter).

But don’t worry. At the end of the day, even though things might not be as easy as they would have been in the past, you can still get a mortgage. Worst comes to worst, you’d just need to meet the same criteria as non-EU nationals. So, it’s not the end of the world!

Yep! Getting a buy-to-let mortgage as a foreign national is pretty similar to getting a standard mortgage – and totally possible!

It’s generally easiest to get a buy-to-let mortgage if you have a UK work permit or permanent residency. But even if you’re not a current UK resident, you may still be able to get approved for one. It helps if you’ve lived in the UK for a couple of years in the past (as this allows mortgage lenders to at least check some of your credit history). And it helps if you can put forward a deposit of 20% or more too (as this helps to minimise the risk for your mortgage lender).

If you’re a non-UK resident, you can also expect a mortgage lender’s checks to be even stricter than usual, especially when it comes to anti-money laundering and identity checks. But let’s be honest: for such an upstanding citizen as yourself, we’re sure you’ll have nothing to worry about!

As you can see, getting a foreign national mortgage in the UK can look very different depending on your personal situation and your mortgage lender’s requirements. So, even though it’s absolutely doable, it can be a bit of a minefield!

That’s why we’d always recommend using an independent mortgage broker. They’ll take the time to get to know your situation and your needs. Then, they’ll be able to search the whole market for the right lender (and the best deal!) for you. They’ll even sort out the whole application process for you from start to finish. What more could you ask for?!

Ready to conquer that mortgage application once and for all?!

Just get in touch with a mortgage broker to start making your home-owning dreams come true. Before you know it, you’ll have a gorgeous little patch of the UK to call your own. Enjoy!

If you're not sure where to find a great broker, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Plus, get 50% off their fee with Nuts About Money.

Yes! Most lenders will be happy to offer a mortgage for tier 2 visa holders (now known as a Skilled Worker visa). This visa type will allow you to give proof to mortgage lenders of your right to work in the UK, which can be used in place of permanent residency.

To give you the best possible chance of getting approved for a mortgage, it helps if you have at least 2 years left on your visa when you apply. If you don’t, then don’t worry. There are things you can do to strengthen your application, like putting in a larger deposit (we’re talking in the region of 25%). Ultimately, you have options! Chat to a mortgage broker for some tailored advice.

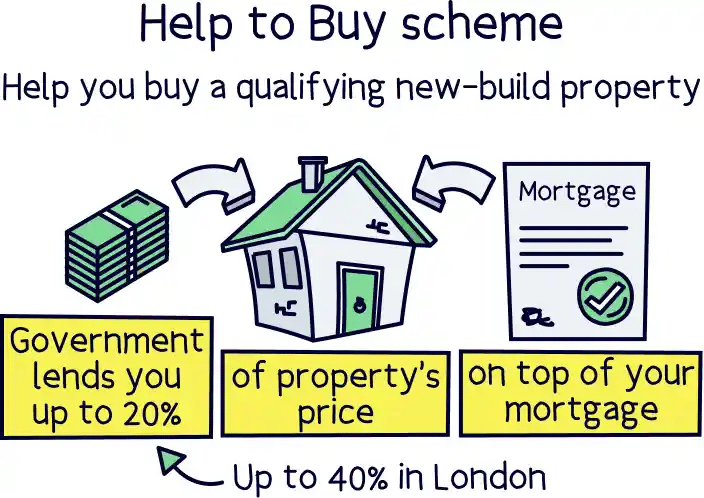

Technically, yes! You have to be a UK resident to be eligible for the government’s Help to Buy scheme. So, if you can prove that you’re a UK resident based on how much of your time you spend in the UK (credit to your tier 2 visa, now known as a Skilled Worker visa), then there’s no reason why you shouldn’t apply.

The only difficulty is this: there aren’t many mortgage lenders who offer the scheme. That could make it more difficult to get hold of one of these mortgages, especially because you may already be choosing from a smaller pool of lenders because of your status as a foreign national. Urgh!

Not in the UK. A non-status mortgage, also known as a self-certification mortgage, is one where you don’t have to show a mortgage lender any proof of income. Sounds pretty great, right?!

It was mainly designed for self-employed workers who don’t necessarily have any payslips to show or who may even get paid in cash. However, regulations have since been tightened, and non-status mortgages are no longer available in the UK. There are similar mortgage types in other countries though!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.