Article contents

Yes! You can (and should!) remortgage when self-employed. If you’re newly self-employed, you may need to remortgage with your current lender. Or, if you’ve been self-employed for 2 years or more, you can choose between many lenders to access the best deals.

Self-employed? Worried about what happens when it comes to remortgaging?

Relax! Remortgaging when self-employed is totally doable. In fact, it’s a must if you haven’t remortgaged in the last few years.

Here, we’ll tell you all you need to know. But first...

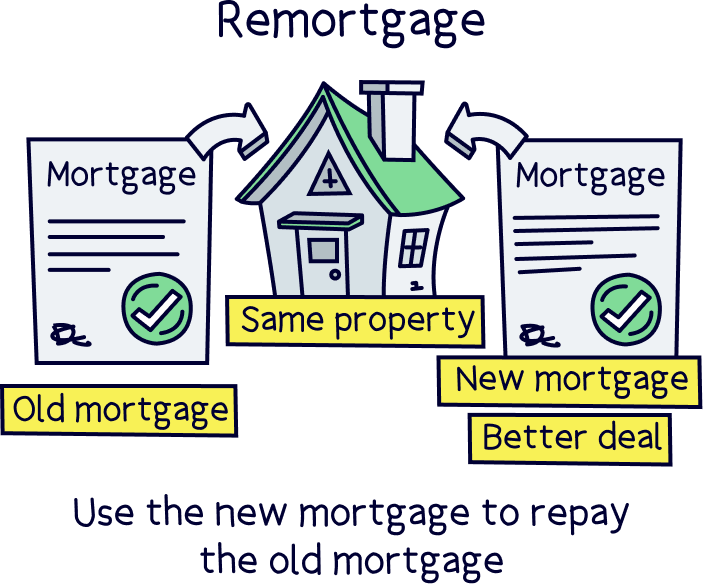

Remortgaging is when you swap your current mortgage for a new one, either with your existing mortgage lender or with a different lender altogether (lenders are the guys that give out mortgages). You should do it every time your current mortgage deal comes to an end. Let us explain.

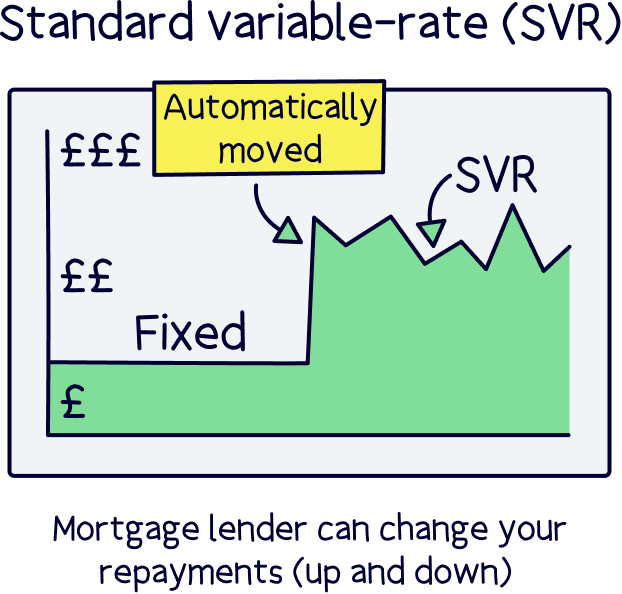

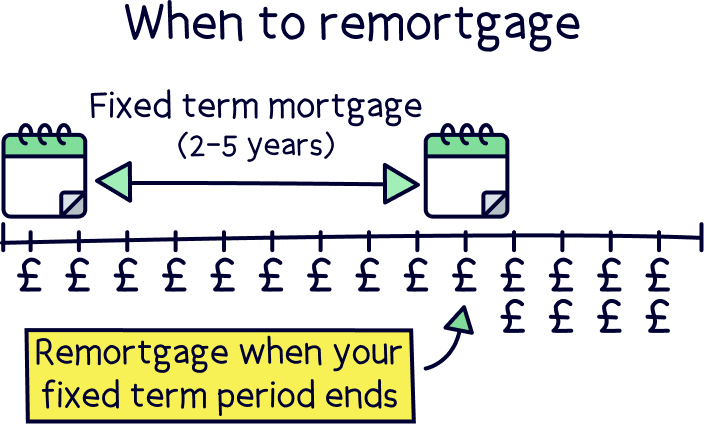

When you first get a mortgage, your lender will normally give you a discounted deal that lasts for a set period of time, known as your incentive period or introductory period. They do this to encourage you to choose them, hence the word ‘incentive’!

This period can last for any length of time, but normally it lasts for 2, 3 or 5 years. Sounds good so far, right?

The problem? As soon as your incentive period ends, your lender will suddenly hike up your prices!

Yep, they’ll automatically put you onto a really rubbish rate called their standard variable rate (SVR). Not only is it a lot more expensive, but your lender can also put your monthly payments up (or down) when they want. Sadly, loyalty doesn’t pay!

Your lender is basically just hoping that you either can’t be bothered to switch to a new mortgage, or that you don’t know how. In fact, a study by Experian showed that as of September 2020, a whopping 46% of mortgage holders were on their lender’s SVR and paying more than they needed to. We know, it’s super cheeky from the lenders. But fear not!

By remortgaging when your incentive period ends, you can avoid falling onto your lender’s pesky SVR and benefit from a lovely new incentive period all over again, often saving hundreds of pounds a month (thousands over a year!).

If you’ve been on the same mortgage for a few years, then chances are you’re on your lender’s SVR. Our tip? Get yourself a remortgage asap so you can start saving!

Tembo will find your best deal, fast, all with award-winning service.

Yes, yes and yes again. You can absolutely remortgage if you’re self-employed. And, if you’ve come to the end of your incentive period, you should remortgage as soon as possible.

However, things might be a bit different for you depending on how long you’ve been self-employed. There are three main groups.

Were you already self-employed when you first got your mortgage? Then you’re in luck!

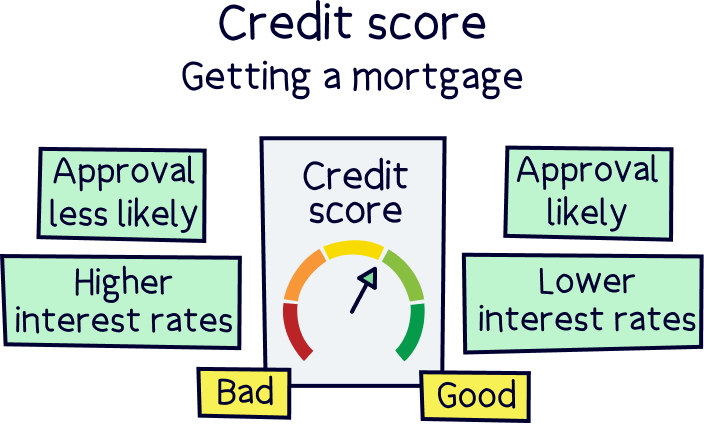

When you remortgage with a new lender, they’ll carry out all the same checks that you had done when you first applied for a mortgage. That means they’ll take a peek at your credit score (a score that shows how good you’ve been with money in the past), your expenses and your income.

Since you’ve already been approved for a self-employed mortgage once, there’s no reason why you shouldn’t pass all those checks again. At least, as long as nothing drastic has changed!

In other words, you’re in a great position and you’ll probably have loads of lenders to choose from. And the more lenders you have to choose from, the more likely you are to find a good deal. Hooray!

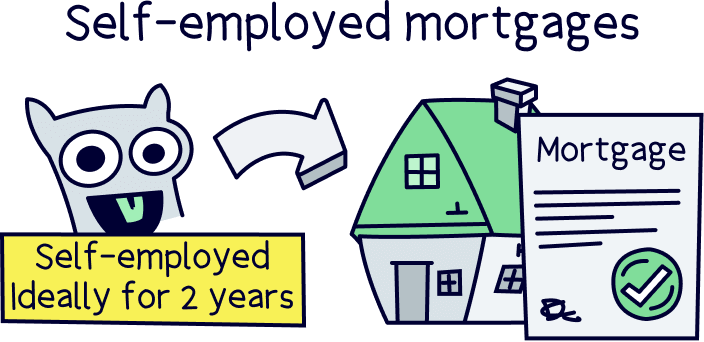

If you’ve turned self-employed since you last got your mortgage, that’s no problem. However, it really helps if you’ve been self-employed for at least 2 years.

Basically, as a self-employed person, it can be harder to prove how much you’re earning (you won’t have an employer who can confirm your salary and you may also be receiving different amounts of money into your account each month). That means most mortgage lenders will want to look at your accounts from the last 2 or 3 years to work out what you’re earning.

If you’ve been self-employed for 2 or 3 years then happy days! You should have all the info you need and most lenders will be happy to consider you for a new mortgage. Even if you’ve only been self-employed for 1 year, you might get lucky and find a lender who’s willing to consider you.

There’s just one thing to bear in mind: if you’re earning a lot less than what you were when you first got your mortgage, you might not be able to borrow as much. Which could make things a bit tricky! But if you’re earning a similar amount to when you were an employee (or you’re earning more!) then you should have lots of lenders to choose from and you should be able to get a great deal as a result!

Finally, what happens if you’ve just turned self-employed and you don’t have 2 to 3 years worth of self-employed income like we keep banging on about?

Well, you can still remortgage. Yay! However, you might struggle to switch to a new lender. That’s because a new lender will want to carry out all those checks we told you about on your income and expenses before approving you for a mortgage, which means they won’t be thrilled if you can’t show them your accounts from the last few years.

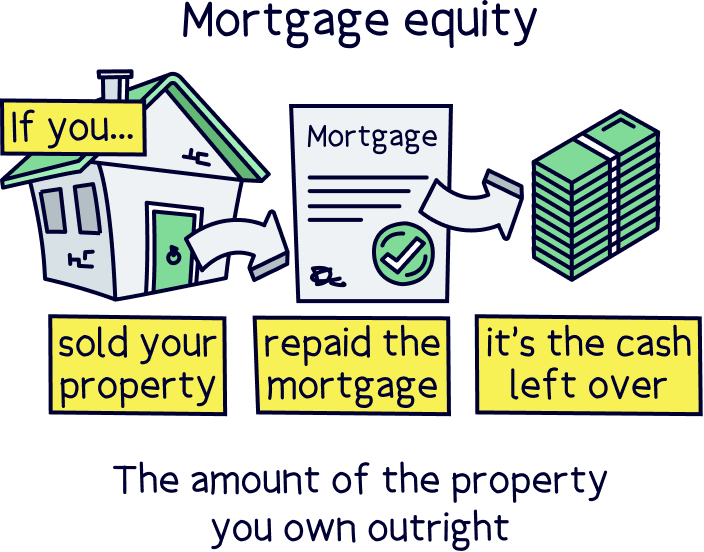

If you’ve built up a lot of equity in your property then some new lenders may be happy to let you switch to them. Equity is the amount of your home that you own outright, instead of the value of your home that you’ve borrowed and still owe your mortgage lender.

However, usually, you’ll need to remortgage with the same lender your current mortgage is with instead. They’ve already carried out checks on you, so they won’t need to carry out many checks on you again. Plus, they’ve seen first-hand that you can keep up with the mortgage repayments (as long as you’ve been paying them on time, of course!).

This is known as a ‘product transfer’ as they’re effectively ‘transferring’ you from one mortgage to another.

Okay, so it’s not the dream situation – normally, you’ll be able to access the cheapest deals by switching lenders as you’ll have more choice. However, remortgaging with your current lender is still a LOT better than falling onto your lender’s expensive SVR.

Once you’ve been self-employed for a bit longer and your next mortgage deal comes to an end, you can remortgage again. And this time, you can look at switching to a different lender to get an even better deal. Simple!

Most mortgage lenders will see you as self-employed if you own more than 20% or 25% of the business that gives you your main income. That means you could be a sole trader (someone who runs their own business as an individual). Or, you could be the partner or director of a limited company (someone who owns and runs their own business as a company, either on their own or with other people).

Whichever way you choose to run your business, lenders will normally ask to see your full accounts from the last few years (which means full details of all your income and outgoings) or your last 2 or 3 SA302s (that’s a yearly document that summarises how much tax you’ve paid if you’re self-employed). Hence why you ideally need to have been self-employed for the last few years before you remortgage with a new lender!

If you’re the director of a limited company, you might also need to show proof of dividends (that’s what it’s called when you pay yourself a share of your company’s profits) and proof of retained profits (retained profits is the money that’s left in your company account, which you haven’t paid yourself).

Things can be a little bit more complicated if you’re the director of a limited company because, if you’re like most directors, you might keep your salary deliberately low to avoid having to pay large amounts of National Insurance and tax, leaving a good proportion of your earnings in your company account.

In other words, your income might look a lot lower than what it is in reality! Not all mortgage lenders will take retained profits into account when they’re calculating your earnings, but if you tend to leave a lot of money in your company account, it could be really helpful to find one who does. They’ll have a better idea of how much you’re actually bringing in and would hopefully be happy to give you a bigger mortgage as a result.

Don’t worry, a mortgage broker (also known as a mortgage advisor) will be able to help you find the right lender for you. We’ll explain why these people are so great in a moment!

Coming to the end of your incentive period? Or already on your lender’s dreaded SVR? Then it’s time to think about remortgaging! But what do you need to do?

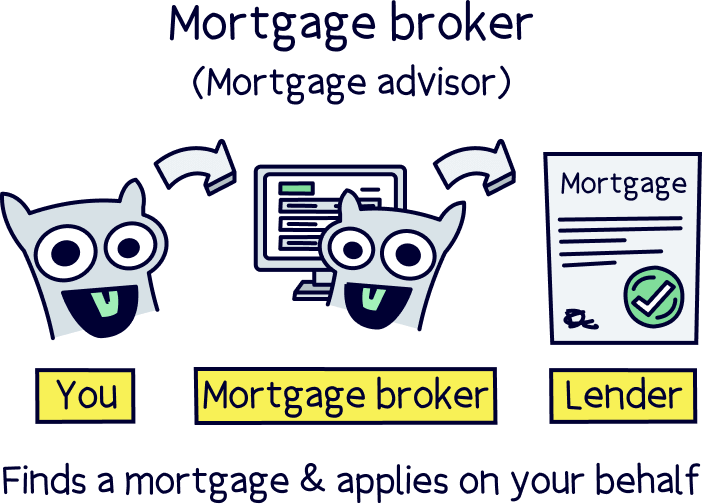

Well, we’d recommend getting in touch with a mortgage broker as your first port of call. Don’t get us wrong, you don’t have to use a mortgage broker – you can just go straight to individual lenders to ask them for a mortgage if you prefer. However, a broker can be really useful.

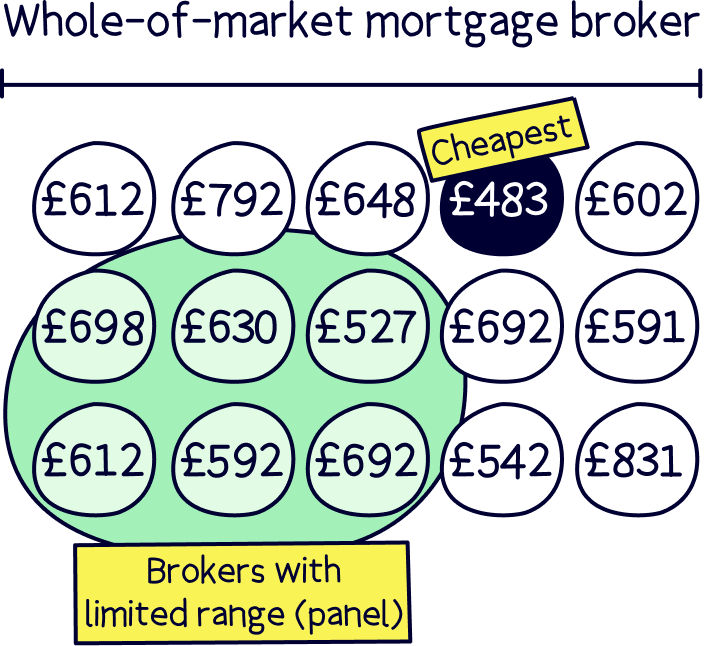

Basically, a mortgage broker is a professional whose job it is to help you find a mortgage. If you choose a whole-of-market mortgage broker, they’ll be able to compare all the mortgages available to find the best deal for you. And they’ll even sort out your whole remortgage application to make your life a lot easier and give you the best possible chance of getting approved.

Now, we think a mortgage broker is a great shout for anyone who wants to remortgage. But they’re even more useful if you’re self-employed.

That’s because every mortgage lender will have different rules and requirements around giving mortgages to self-employed people, which you might not be aware of. Your broker will take the time to find out about your own unique circumstances and will know all the ins and outs of individual mortgage lenders, so they’re in a great position to point you in the direction of the best lender for your needs.

Need help finding one of these awesome people? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best deal. You'll also get 50% off their standard fee with Nuts About Money. How great is that?

If you’re self-employed and the time to remortgage is slowly creeping nearer, there are a few things you can do to give yourself the best chance of getting a really great deal.

If you remortgage with a new lender, they’ll want to see your SA302s (documents that give evidence of your earnings) or your accounts from the last couple of years. So, make sure you keep up with your paperwork and keep clear records. That includes registering with HMRC when you turn self-employed.

Don’t worry if you’re feeling a bit overwhelmed by it all. An accountant can help. If you’re not sure where to find one, we’d recommend comparing accountants near you using Unbiased¹.

A new lender will check your credit score to see how good you’ve been with money in the past. Improving your credit score is a great way to make yourself seem less risky to lenders as it will help them feel more confident that you’re going to keep up with your monthly mortgage repayments.

That means paying off any outstanding debts. And, it also means that now’s probably not the best time to take out a new loan. That swanky car you were hoping to get on finance might just have to wait – sorry!

This doesn’t exactly replace the need for those accounts or SA302s. But if you can give lenders proof of upcoming work, it can definitely help. Especially if lenders are torn about whether or not to offer you a mortgage.

Proof of future work might include signed contracts if you’re a fixed-term contractor, or a letter from a client who’s offering you a big chunk of work. Either way, it just might help to seal the deal!

If you have those 2 to 3 years of accounts, then we’d definitely recommend looking into switching lenders. By comparing deals from multiple lenders (especially with the help of a whole-of-market mortgage broker), you’ll normally end up with the best deal.

However, if you’re newly self-employed, new lenders might not yet be willing to consider you for a mortgage. In this case, you’ll still be able to remortgage with your current lender, known as a product transfer.

Yes, you might not be accessing the very best deals. But it will still prevent you from falling onto your lender’s SVR. And if it means saving money (which it does!) then we’d say it’s oh-so-worth-it!

If your current mortgage deal is coming to an end – or you’re already paying through the roof on your lender’s SVR – it’s time to remortgage. And yes, that includes if you’re self-employed!

Not only will remortgaging help you avoid your lender’s pesky price hikes, but if you find a mortgage advisor who can help you to compare all your options, it will also mean getting yourself on the very best deal and hopefully, saving hundreds of pounds a month. Just think what you could spend that money on… a new TV? A fancy holiday? We’ll leave it to you!

As a reminder, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.