Article contents

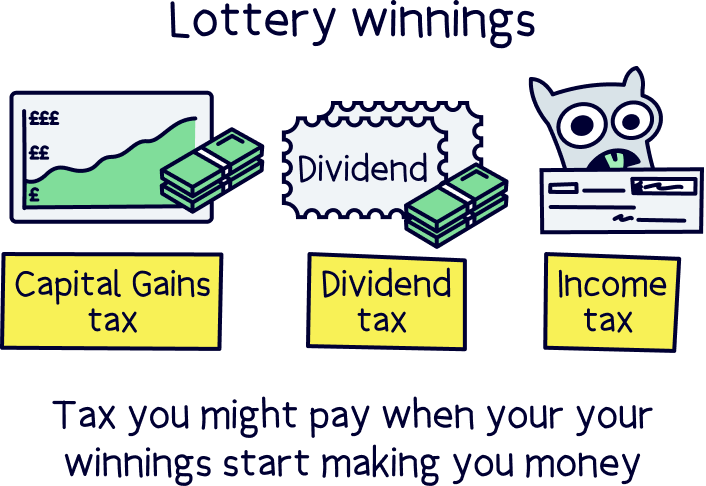

Lottery winnings are tax-free in the UK. However, any income or money generated from those winnings, such as through investments or interest, may be subject to taxes like Income Tax, Capital Gains Tax, or Dividend Tax.

Let’s get straight to it, nope! You don’t pay tax on lottery winnings in the UK.

You get to keep every single penny. But before you start celebrating you might have to pay some tax in the future if your winnings start making more money, such as interest payments.

In some countries, like America, you would have to pay tax, and it’s a lot – up to 45% depending on which state you live in. Crazy!

Let’s dive into the UK winnings a bit more and find out more about what taxes you might pay in future, and if you can legally avoid or reduce them a bit.

As gambling is free from tax in the UK, that means the lottery is also free from tax!

Technically playing the lottery is a form of gambling, and so it’s treated just the same as things like gambling in a casino.

Even things like sports betting are free from tax too, so you can bet on football at the weekend or any other sports you’re interested in and all your winnings are tax free – although gambling is not a wise investment strategy so we don’t recommend it!

Although the winnings itself is tax-free. There are some taxes to pay after you get the winnings. The tax people always get their cut, doh!

Let’s run through the types of tax you might pay, and how to reduce the amount if possible.

Find a financial advisor with Unbiased, and get help with your finances.

As soon as your winnings start making you more money, you might have to pay tax on the money you make.

So for instance, if you put your money in a savings account that pays interest, you might have to pay Income Tax on that interest.

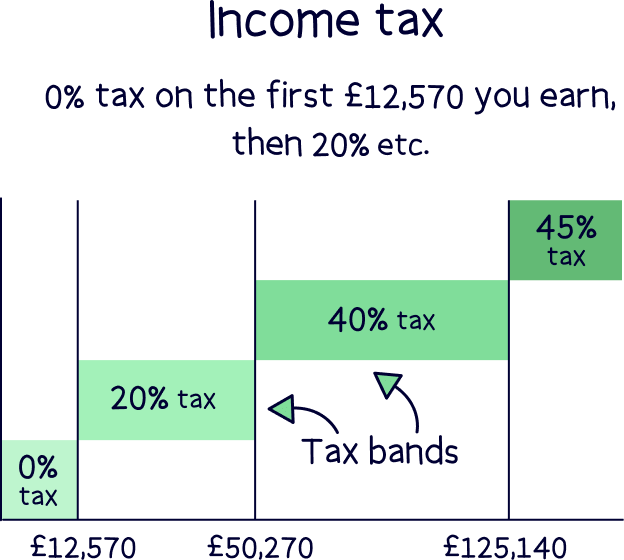

Income Tax is what you pay on quite simply your income, for instance your salary. You need to add up all of your income from everything (if you have more than one source), and then figure out how much you’ll pay with the table below:

Your income is based on a tax year, which runs from April 6th to April 5th the following year.

So, if you’re the lucky one and won millions of pounds on the lottery and put it in a bank account earning interest, you’ll probably have to pay 45% tax on most of your interest each year. Ouch!

If you didn’t quite win the jackpot but still a fair bit, you might have to pay Income Tax on your future savings interest.

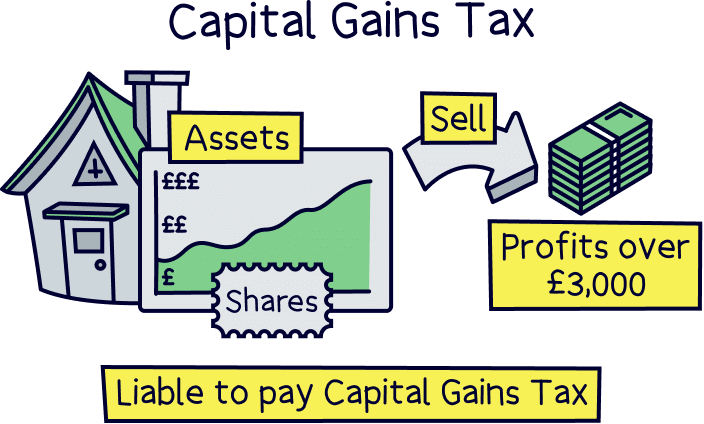

If you were to invest your winnings, rather than put them in a savings account, you might have to pay Capital Gains Tax too. This is where you buy something of value (called an asset), and that asset goes up in value and you then sell it. You might have to pay tax on your profit.

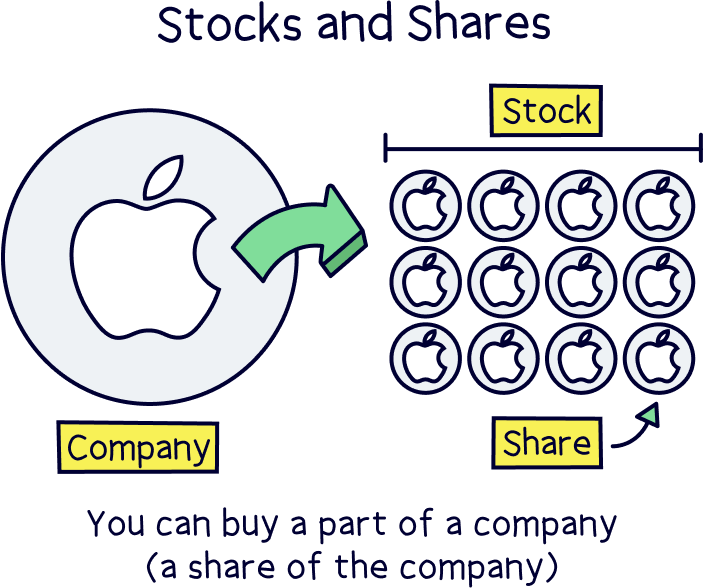

Typical investments are stocks and shares, which is where you own part of a company (a share of the company).

When you begin selling those investments and making profit, you might have to pay tax. The rate you’ll pay is either 18% or 24%. It’s 18% if you are a basic rate taxpayer when it comes to your income (see above), or 24% if you are a higher rate or additional rate taxpayer.

Presuming that your winnings are making you a large income from interest every year, you’ll be a higher rate or additional rate taxpayer and so you’ll pay 24% in Capital Gains Tax on your profits when you sell investments in the future.

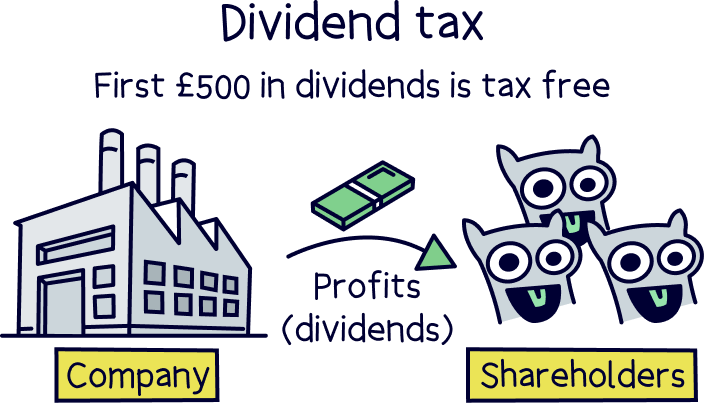

When you invest and buy shares in companies, you buy ownership of those companies. And when successful companies make lots of profit each year, they can give those profits back to their owners (called shareholders, the people who own the shares). These are called dividends.

And you might have to pay tax on dividends. Initially you get a £500 allowance per year where no tax is paid, but after that you’ll pay tax, and it can be fairly hefty.

It’s again linked to your income, and here's what you’ll pay:

So, presuming you’re a higher rate taxpayer you’ll pay 33.75% and if you’re an additional rate taxpayer you’ll pay 39.35%. That's a lot of tax, so how do you reduce this tax bill? Let’s run through it.

The best way to avoid Capital Gains Tax (well all taxes on your investments) is to open a Stocks and Shares ISA. That’s an account where quite simply, you can save tax-free.

However, there’s a limit of saving £20,000 per year (your ISA allowance). If you've won the jackpot this allowance might be a small amount of your winnings (however, it's still worth using).

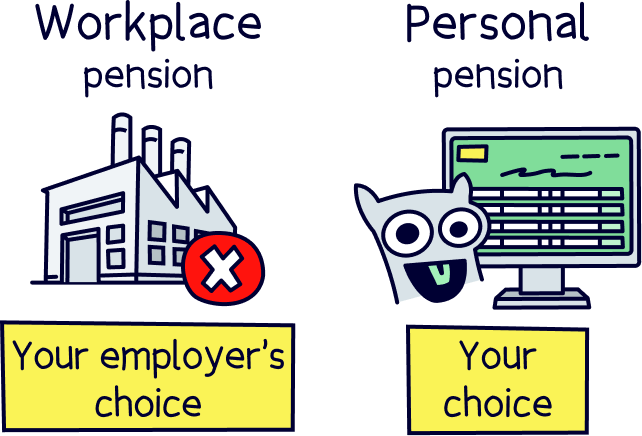

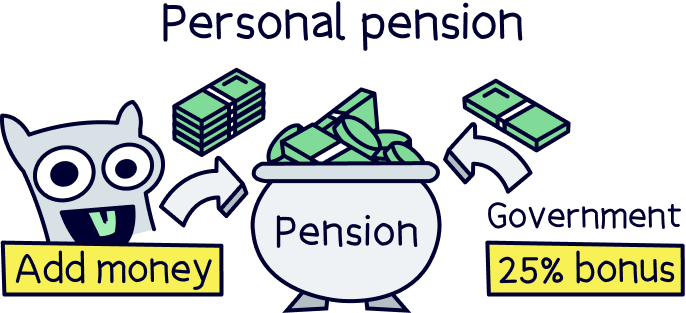

You could also pay money into a personal pension, in addition to an ISA. These are also tax-free.

A personal pension is similar to a pension you might have from work if you’re employed. Which is called a workplace pension. Except it’s set up by you instead of your employer. It’s easy to do, all you need to do is pick a pension provider (someone who looks after your pension).

They’ll invest your money in a responsible way to grow it over time. Just the same as a workplace pension.

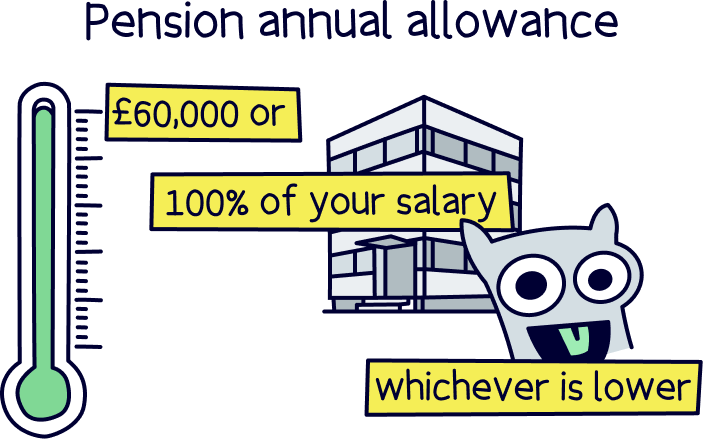

However in order to pay into a personal pension, you will need to be generating an income each year (hopefully from your new savings and investments). You are only allowed to pay in as much as your income into your pension(s), or up to £60,000, whichever is lower.

A personal pension also has the added benefit that it doesn’t count towards Inheritance Tax (more on that below). Plus, you actually get your Income Tax automatically refunded back into your pension in the form of a government bonus (25%), so you save even more money! Plus if you pay tax at a higher rate (40% or 45%), you can claim this tax back too via a Self Assessment.

By the way, you don’t have to win the lottery or be super rich to open a personal pension, it’s highly recommended for everyone. Paying no tax is a wonderful thing, it means you can save so much more money by putting it in a pension!

Not sure which pension provider to choose? Check out the best personal pensions to learn more and get started.

Now after winning your millions you'll probably want to share your money and ultimately pass it down to your family when you sadly pass away. Here’s where it can get very expensive.

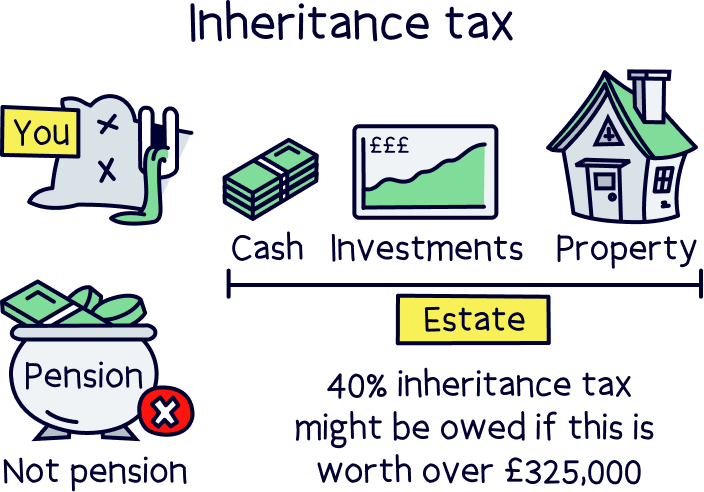

When you pass away, all of your money, property, and any other assets you have (except your pension), are all grouped together and added up. This is called your estate. And this is what counts towards tax (if it’s over £325,000).

If you die before your partner (spouse or civil partner), and they inherit all of your estate, then there’s no tax to pay. Phew.

However, if you pass on your estate to your kids or anybody else that’s not your partner, they’ll have to pay a huge 40% tax on it.

Well, first they’ll get an allowance of £325,000 where no tax is paid, but after that, it’s 40% on everything. Ouch!

There’s one exception, which is passing on your home to your kids (and only your kids), then the threshold (the tax free figure) increases to £500,000 in total.

A gift is simply when you give money or something nice (like jewellery or a house), to someone without any expectation of anything in return.

If you give away your winnings to your friends and family, you will of course become very popular, and if you live for a long time your friends and family will have nothing to worry about tax wise. Well, 7 years to be precise!

If you live for another 7 years after you’ve given a gift, there’s no inheritance tax to pay (on the gift).

However, if you pass away during the 7 years after giving the gift, there will be inheritance tax to pay. Although you can give away £3,000 per year in total tax-free. Anything above this, the receiver may have to pay inheritance tax on.

What they’ll pay depends on how long ago the gift was given after you pass away, and works like a sliding scale (called taper relief). Here’s what they’ll pay:

Quite a bit right?! It’s worth keeping in mind when giving gifts.

It might become fairly stressful and expensive if your gift is used for something like buying a house, but then you pass away and they have to pay 40% tax on the amount you gave them. (They would probably have to sell the house). Maybe let them know about this!

And there we have it, great news for you, no tax on your lottery winnings! If you won big you can stay super rich for life providing you don’t spend it all on fancy cars and champagne parties! (well, maybe just a few).

However once your money starts making you even more money, that’s when you’ll pay tax, and that’s Income Tax, Capital Gains Tax and Dividend Tax.

However, if you pass away, your loved ones may have to pay inheritance tax on all of your estate (the total amount of money you would have if you sold everything). Plus, tax on any gifts you’ve given them if you pass away within 7 years. Let’s hope that doesn’t happen!

Nuts About Money tip: If you have won the lottery, you could also speak to a financial advisor. You can find the best advisor for you with Unbiased¹.

And that's it, paying tax might be a nice problem to have, just imagine what you could do with all of your winnings! Good luck, we hope you win the lottery soon!

Find a financial advisor with Unbiased, and get help with your finances.

Find a financial advisor with Unbiased, and get help with your finances.

Find a financial advisor with Unbiased, and get help with your finances.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find a financial advisor with Unbiased, and get help with your finances.