Article contents

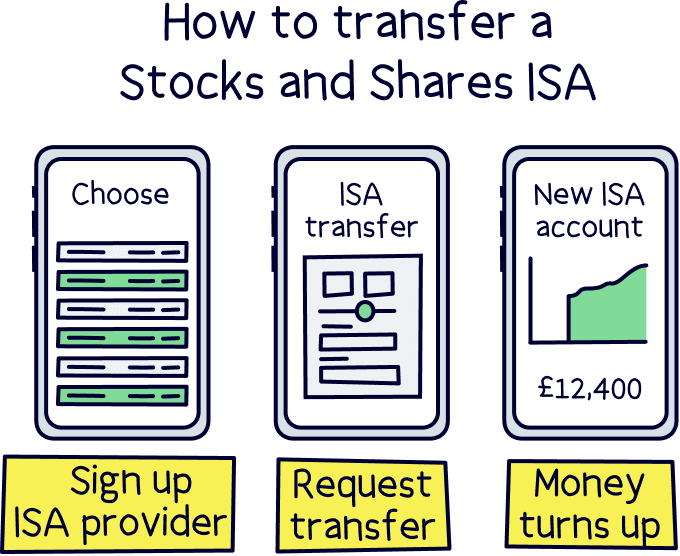

Transferring a Stocks and Shares ISA is super easy. Your new ISA provider will handle everything for you. All you need to do is sign up and fill out an ISA transfer form. After that, your money will turn up in your new ISA account (usually within 30 days).

Already have a Stocks and Shares ISA but want to move it to a new ISA provider? No problem. We'll explain all.

We’ll also run through the best Stocks and Shares ISAs, if you’re looking to compare and move to a better provider – with better investment performance, lower fees, or a bigger range of investment options.

You can also transfer your Stocks and Shares ISA to another type of ISA too, such as a Cash ISA or Lifetime ISA. We’ll cover what these are and how to do it below.

First things first, if you’re wondering if it’s possible to transfer your ISA to another provider, yes it is! In fact, the government has put processes in place to make sure it’s all handled smoothly and within a good time frame (30 days).

Everything will remain the same, except you'll be with your shiny new ISA provider. You’ll still have the same amount remaining of your ISA allowance remaining (more on that below).

And there’s even better news, it’s super easy to transfer a Stocks & Shares ISA too. All you need to do is find a great new provider if you haven’t already (we’ll cover the best Stocks & Shares ISAs below), and open an ISA account. After that, simply let your new provider know that you want to transfer your old ISA over and they’ll take care of all the paperwork.

You’ll have to fill out an official form called an ISA transfer form, which your new provider will give you, just to confirm you want to transfer the ISA officially, and how much you’d like to transfer (if not all of it).

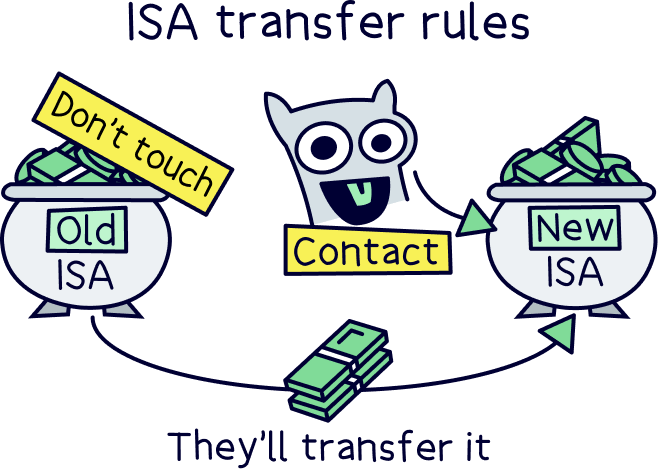

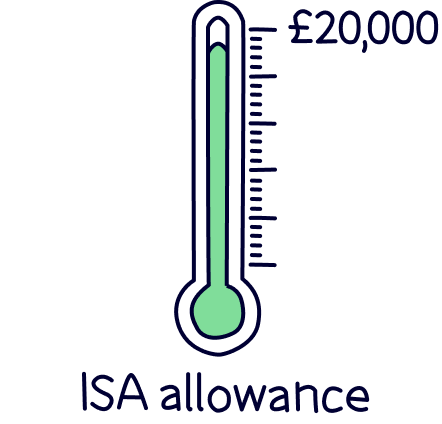

There’s only one rule! Don’t withdraw any money from your current provider and then deposit it into your new ISA – as the money you add this way will count towards your annual ISA allowance (the government allows you to save up to £20,000 tax-free every tax year). So, if you do this you might not be able to add as much as you'd like to within this tax current year.

Note: the tax year runs from April 6th to April 5th the following year.

If you have less than £20,000 in your ISA (and most of us do have less), and you’re not going to add more this current tax year to go over the limit, then it doesn’t actually matter too much if you withdraw your cash from your current ISA and deposit it into your new ISA. You’ll be below the contribution limit for the year anyway.

Nuts About Money tip: it’s often easier for your new ISA provider to transfer it for you.

Nope. You can transfer as little or as much as you like. Transferring just a bit of your cash or investments is called a 'partial transfer'.

Just let your new provider know how much you'd like to transfer and they'll sort it for you (don't worry, they will ask this when you apply for the transfer).

Not sure where to find the best ISA providers? Here's our recommendation for the best managed Stocks and Shares ISAs – that’s where the experts handle the investing and aim to grow your money over time.

Not found a great new ISA yet? Here’s the best options to help you pick.

Easy to use

A great and easy to use investing app. Add money from your bank or transfer your existing ISA, with the investments handled by experts. There’s a pension pot too.

The customer service is excellent, and has email and phone support based in the UK.

Beach is an easy to use investing app (and easy to set up), just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total savings whenever you like.

You’ll get an easy access pot (access money in around a week), which can be an ISA where all the money you make is tax-free (save up to £20,000 per tax year), and a standard account for those saving in addition to this (or who don’t want an ISA), where there’s no contribution limits (but also no tax-free benefits).

The investments are managed by experts from the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

There’s also an optional pension pot to save for retirement, so you can keep all your savings in one place, and if you’ve got lost or old pensions, Beach can also find them and move them over too.

Fees: a simple annual fee of up to 0.98% (minimum £4.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Not found a great new ISA yet? Here’s the best options to help you pick.

You can also make your own investments, rather than leaving it to the experts – but it’s only recommended for experienced investors. If you do want to do this, here’s the best self-select ISAs:

Not found a great new ISA yet? Here’s the best options to help you pick.

Get up to £100 free share

Lightyear is an awesome mobile app with very low cost investing.

There’s a decent range of investment options (over 4,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

There's no account fees and no trading fees. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

You can invest with a tax-free ISA, a regular account and a business account.

And if you’ve got cash savings, you’ll also get one of the best rates possible with their Cash ISA (it matches the Bank of England base rate).

Get fractional shares worth up to £100

Trading 212 is a platform built for everyone in mind – there's over 2,000,000 customers! It’s great for beginners to get started, and perfect for experienced traders looking for more advanced trading options, such as CFDs, meaning you can trade with leverage (borrowed money), and trade the price going down (go short). There's all the trading tools you’ll need too, such as stop-loss and limit orders.

It’s one of the cheapest platforms out there with low fees when buying foreign stocks (currency conversion fee).

Platform experience: good

Device options: website & phone app

Support: 24/7

Stocks & Shares ISA: yes

Pension (SIPP): no

Range of investments: large

Stocks: yes

ETFs: yes

Fractional shares: yes

Crypto: no

CFDs: yes

Forex: no

Account fee: free

Cost per trade: free

Spread fees: yes (low)

Currency conversion fee: 0.15% on stocks, 0.50% on CFDs

• Low cost trading

• Huge range of investment options

• Hold and trade in multiple currencies

• Very low foreign exchange fees (0.15%)

• Offers an ISA

• Great mobile app

• Lots of resources to learn

• Awesome customer service

• No minimum investment

• Fractional shares

• No personal pension (SIPP)

AJ Bell is well established, with a good reputation.

It's one of the cheapest traditional stock brokers out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is great too.

Overall, it's one of the best options.

Transferring a Stocks and Shares ISAs shouldn't take longer than 30 days to complete. This is an official guideline set by the government, and you should get in touch with your ISA provider if it’s taking longer than this (they are being naughty!).

You can also then complain to the Financial Ombudsman Service (the people who make sure financial customers are treating their customers fairly), who will look into the issue.

By the way, transferring Stocks and Shares ISAs is a bit longer than a Cash ISA to another Cash ISA. Transferring a Cash ISA should only take 15 days.

Just want to be 100% what a Stocks & Share ISA is? Let’s run through it.

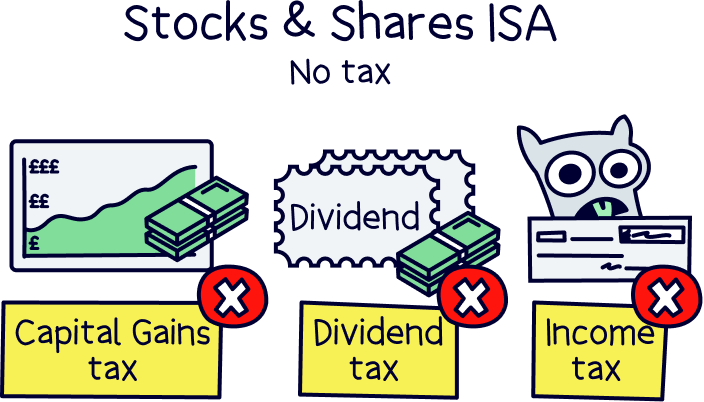

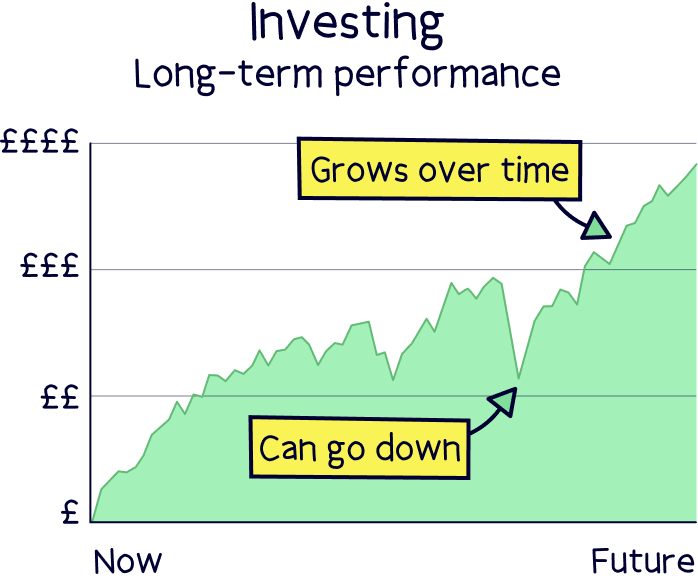

It’s an investment account that lets you save and invest (e.g. buying stocks and shares) completely tax-free! So, you won’t pay any Capital Gains Tax, Income Tax or Dividend Tax. This can be a massive saving when you are saving for the long-term (recommended). How great is that?!

They’re a great way to grow your money over the long-term, as long as you use a safe and sensible investment strategy (such as letting the experts handle things) and are considered much better than simply saving cash for long-term savings.

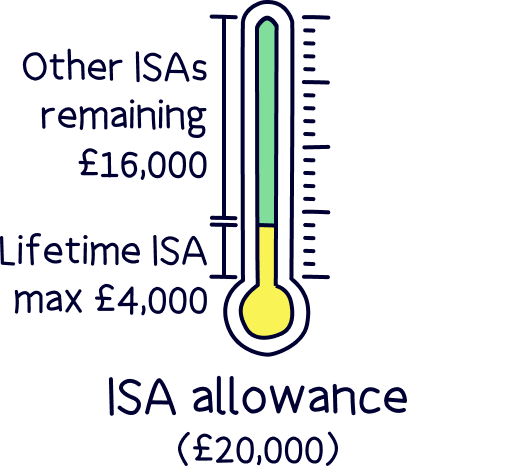

You can invest up to £20,000 per tax year (April 6th to April 5th the following year), called your annual ISA allowance, and is the total limit across of the different types of ISAs – so a Cash ISA (for cash savings), Lifetime ISA (to save for your first home), and an Innovative Finance ISA (for lending your money directly to other people via platform), all combined.

Note: Stocks and Shares ISAs are also commonly called investment ISAs.

You also have the option to transfer a Cash ISA to a Stocks and Shares ISA if you want to.

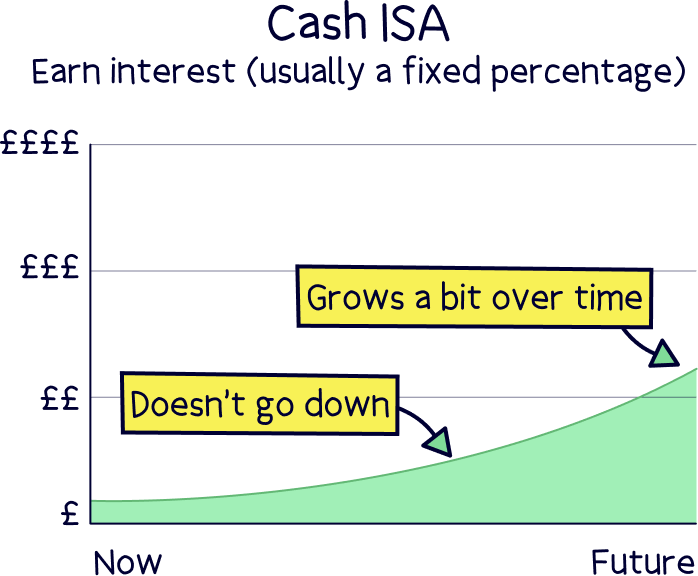

A Cash ISA is simply an ISA for your cash savings, where you’ll earn interest (usually a fixed percentage every year). You can do this in the same way as transferring a Stocks and Shares ISA, just let your new provider know you want to transfer your Cash ISA.

The same process goes for transferring an investment ISA to a Cash ISA – simply let your new provider know that you want to transfer your ISA across, and they’ll handle everything (after completing an ISA transfer form).

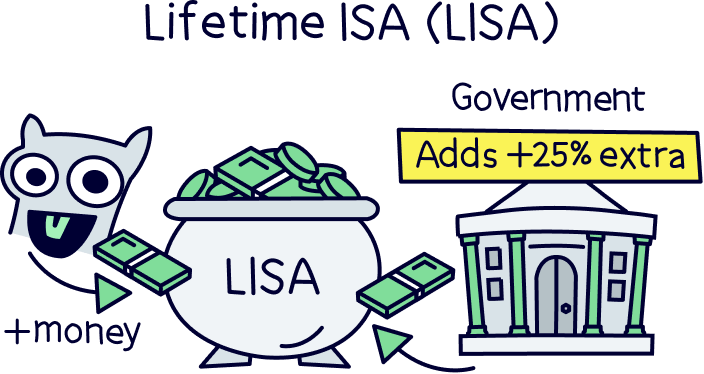

A Lifetime ISA is another type of government savings account where you can save completely tax-free, but you can only use it to buy your first home, or you’ll have to wait until you’re 60 to access the money. And, they have a great benefit, you’ll get a massive 25% bonus on your contributions. You can add up to £4,000 each year.

It’s often not a good idea to transfer a Lifetime ISA to a Stocks and Shares ISA as you’ll have to pay a hefty fee of 25% of the total balance. Which works out as more than the 25% bonus you get from the government on your contributions. But, it is possible, and works in exactly the same way, your new ISA provider will handle everything.

You can also transfer a Stocks and Shares ISA to a Lifetime ISA, and again, this works in the same way, your new provider will handle everything. However, your previous ISA balance will count towards your £4,000 annual allowance for a Lifetime ISA for this current year. So you won’t be able to transfer more than £4,000 until the next tax year.

There can be some fees involved with ISA transfers, and these depend on which ISA provider you are currently using, these vary across providers too.

Some may charge an ISA transfer fee, or an exit fee, but this is very uncommon – and if they do, it’s probably a sign that they’re not a great provider in the first place and transferring is a great idea.

The most common fees are transaction fees to sell your investments within your Stocks and Shares ISA account, and turn them into cash, if needed. This shouldn't be a huge amount – but it could be. Your provider should let you know about any cost involved.

So there we have it – how to transfer a Stocks and Shares ISA. Pretty straightforward really isn’t it? Simply sign up with a new ISA provider, and let them know you want to transfer your old ISA from your existing provider over to them, and they’ll take care of everything – you just need to complete an ISA transfer form.

If you’ve found a great new ISA provider, it’s often a good idea to transfer all your old ISAs to benefit from potentially lower fees, a wider range of investments and potentially better investment growth over time.

If you haven’t found a great new ISA provider yet, we’ve researched all the best out there. Here's all the best Stocks and Shares ISAs.

That’s it – your money will be with your new provider in no time!

Not found a great new ISA yet? Here’s the best options to help you pick.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Not found a great new ISA yet? Here’s the best options to help you pick.