Article contents

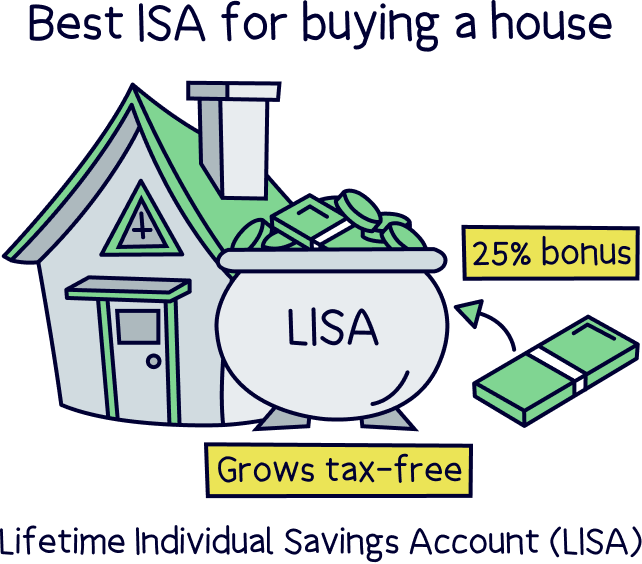

The best ISA account to use to save to buy a house is a Lifetime ISA (LISA). You’ll get a massive 25% bonus from the government on everything you save (you can add up to £4,000 per year), and your money will grow tax-free. The best interest rates are below.

Planning to start saving for your first home? Great, the sooner you start, the bigger your deposit will be!

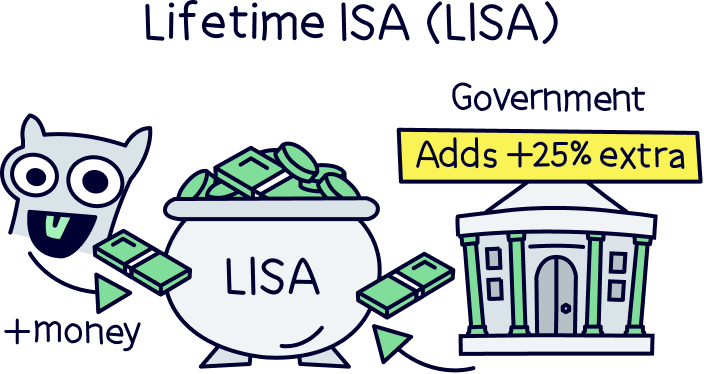

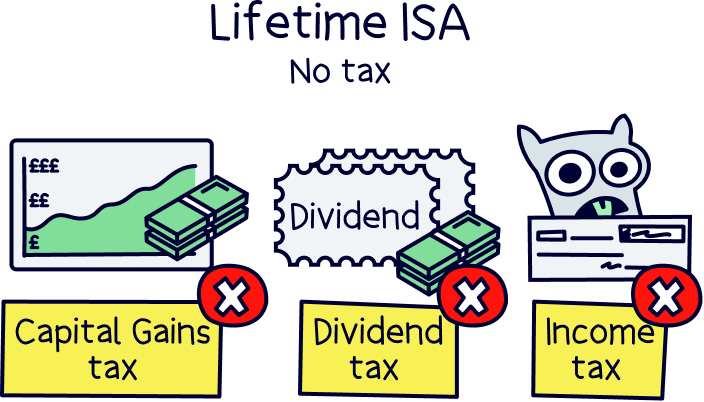

In the UK, there’s some pretty great savings accounts to help you boost your house deposit – and one designed for specifically that, a Lifetime ISA (LISA), where not only can you save tax-free (so no tax paid as it grows or when you withdraw), but you’ll also get a massive 25% bonus from the government on everything you save.

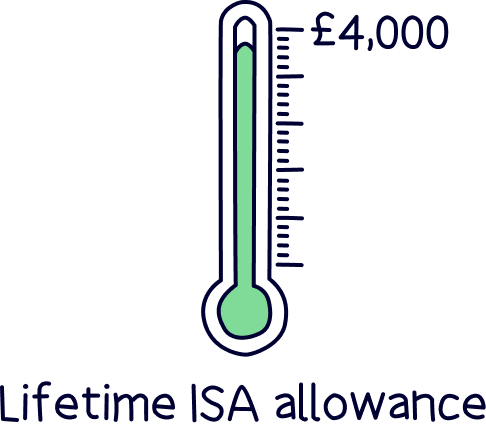

You can save up to £4,000 per tax year (April 6th to April 5th the following year), meaning you could get a juicy £1,000 free each year (if you’re able to save that much).

You can either open a Cash Lifetime ISA, and earn interest on your cash, or opt for a Stocks and Shares Lifetime ISA, where you can invest your money (we’ll cover those more below).

Note: there used to be a different ISA called a Help to Buy ISA, which also had a 25% bonus, but was limited to £200 per month in savings. This has now been replaced with the Lifetime ISA. If you do have a Help to Buy ISA, you can transfer it to a LISA, or still use it.

Anyway, if you’ve heard enough and keen to get started, here’s the top 3 of our top 10 Lifetime ISA providers:

Check out Moneybox, it has one of the highest interest rates, and it’s easy to use.

Top rate

Saving for your first home? Moneybox could be for you.

Moneybox is the go-to place for Lifetime ISAs – it’s easy to use, and you’ll be able to manage everything on a great mobile app.

You can either pick from saving cash (Cash Lifetime ISA), and benefit from a great savings rate. And there’s no fee for saving cash.

Or, you can make your own investments (Stocks and Shares Lifetime ISA), and pick from a range of investment options (including individual US shares such as Apple and Amazon). Fees will apply.

Moneybox will handle everything behind the scenes, and collect your 25% government bonus and automatically add it to your account.

Overall, it’s low cost overall, and the customer service is excellent.

Note: don’t wait to get started, as you’ll need to wait 12 months before you can use your LISA to buy a home – all you need to do is add £1.

Top rate

Tembo is one of the best Lifetime ISAs out there – it’s got one of the best interest rates out there, and it’s easy to use, with a great app on your phone, packed with tools to help you save more.

They’ll also transfer your existing Lifetime ISA over if you have one too (they’ll handle everything).

There’s two options, a Cash LISA (with the top interest rate), or a Stocks and Shares LISA, where you can simply let the experts handle things, and aim to grow your money more over time).

They'll also be able to help you with the mortgage when the time comes to buy your first home – and help you borrow more if you need to.

The customer service is top notch too.

Cheapest Stocks and Shares Lifetime ISA

Lifetime ISAs: fees are reduced to 0.25% per year, and free to buy investment funds

Hargreaves Lansdown (HL) is the most popular investment platform in the UK, it’s used by over 1.8 million people, saving over £130 billion. It’s very trustworthy, and safe to use.

They offer a great Stocks and Shares Lifetime ISA – which offers the full range of investment options, but also has reduced costs just for the LISA (compared to other types of investment accounts), making it one of the best LISA options out there (fees are reduced to 0.25% per year, and free to buy investment funds).

It’s great for making your own investments, or you can pick ready-made choices where you can leave it to the experts.

Check out Moneybox, it has one of the highest interest rates, and it’s easy to use.

It’s pretty difficult to save for a home these days right? Actually, make that incredibly difficult!

A Lifetime ISA (Individual Savings Account) can provide some welcomed help, and is perfect to help you save for your first home.

That’s thanks to the massive 25% government bonus on all the cash you’re able to put away into it. Plus, your money will grow tax-free, so you get to keep all the money you make, helping you to save that little bit more.

You can save up to £4,000 per tax year, which runs from April 6th to April 5th the following year, so the total bonus you can get free is £1,000 each year (which means you’ll have a total of £5,000 each tax year, plus interest).

You can open a LISA aged between 18 and 39, and keep paying into it until you’re 50.

However, there are some limitations…

You can only buy a home worth up to £450,000 – which can be too low for some people these days (as house prices have gone through the roof).

You’ll also need to be a first time buyer, which is someone who hasn’t bought property before.

If you’re buying a house with a partner, you can both use a LISA, however you both need to be first time buyers, otherwise just the first time buyer can use theirs.

You also need to have your LISA open for at least 12 months (with cash in it too), before you can use it. (So don’t delay, get started today. Check out Moneybox¹, it’s one of the best interest rates out there.)

And, if you want to withdraw cash from it, instead of using it to buy your first home, you’ll have to pay a penalty of 25% (called a government withdrawal charge) – which actually works out as more than the 25% government bonus (it sounds odd, but the maths works out).

Nuts About Money tip: if you think a LISA isn’t for you, a normal ‘ISA’ is a great option to save tax-free – we’ll cover it in more detail below, but here’s our guide to ISAs.

Let’s recap all that to make it a bit easier to understand. To open and later use a Lifetime ISA, you’ll need to:

If you don’t use it for your first home, you’ll need to wait until you’re 60 to withdraw the cash, or pay a 25% penalty. However, if you become terminally ill, you’ll be able to withdraw your money without a penalty.

Nope. The government no longer offers Help to Buy ISAs. These savings accounts were to help you buy a home too, but worked a bit differently, where you could save up to £200 per month, and the government would top up your total savings by 25% when you were ready to get on the property ladder and buy your first home.

They were a bit complicated when actually buying the house too, because of the process of actually claiming that 25% bonus when you needed it (when you were exchanging contracts (officially buying the house)).

But lucky you, Lifetime ISAs are much better – you can save even more cash each year, and you don’t have to save monthly if you don’t want to. Plus, you’ll get the bonus directly within your LISA account, rather than when you buy the home – so it’s a simpler process, but also you can earn interest on the bonus too!

You can also use a LISA for retirement saving, as it’s tax-free, and you get the 25% government bonus – but we won’t run through all the details of that here, we’re focusing on saving up your for your first home.

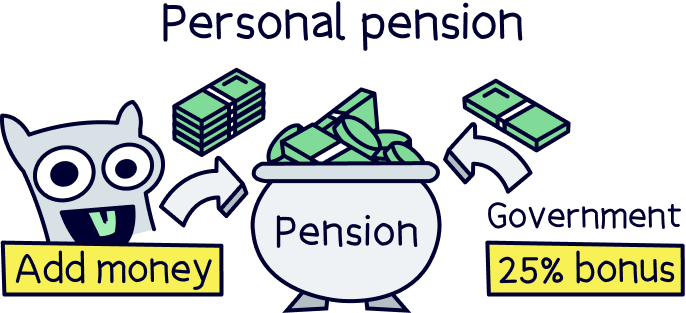

And although a Lifetime ISA can be for retirement, for a lot of people, a personal pension is typically better – you also get a 25% bonus, and your money grows tax-free, but you can also save a lot more in it each year and claim back more tax if you pay 40% tax, plus lots of other advantages.

Note: you might pay tax when you withdraw your money when you retire, it depends on your total income at the time.

Learn lots more about that with our guide to a Lifetime ISA vs pension.

There’s two types of LISAs, a Cash LISA, and a Stocks and Shares LISA. Let’s run through each.

This is just like a savings account from your bank, you add money, it earns interest and your money grows over time. The 25% government bonus will be added automatically by your provider (LISA company), either when you add money, or each year (depending on the provider).

Here’s where to learn more about the best Cash Lifetime LISAs.

A Stocks and Shares LISA is where you can invest your money, rather than earning interest on it (like a Cash LISA).

Investing your money is typically seen as a better option for long term savings, as it has the potential to grow more than earning interest, and this is typically over 5 years or more.

Depending on the LISA provider you opt for, you can either let the experts handle things (recommended), or if you’re experienced with investing, make your own investments.

You’ll be able to invest in things like stocks and shares (where you own parts of companies), and investment funds, which are groups of lots of different investments all pooled together into a single investment, and typically managed by experts.

Your money can go up and down over time however, but with a sensible investment strategy it will likely grow, given enough time.

Here’s where to learn more about the best Stocks and Shares LISAs.

If a LISA isn’t for you, perhaps you want to buy a home worth more than £450,000, or if you’re planning to save more than £4,000 within a tax year and so need two accounts, you’ve got some more options too.

This works like a Cash Lifetime ISA and a savings account with your bank, where you simply add money, and earn interest in return (more money). The money you make will be completely tax-free. However, you won’t get the 25% government bonus.

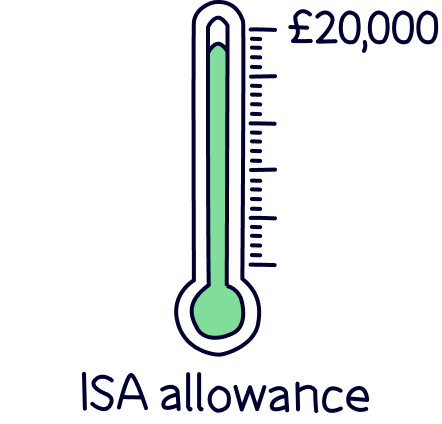

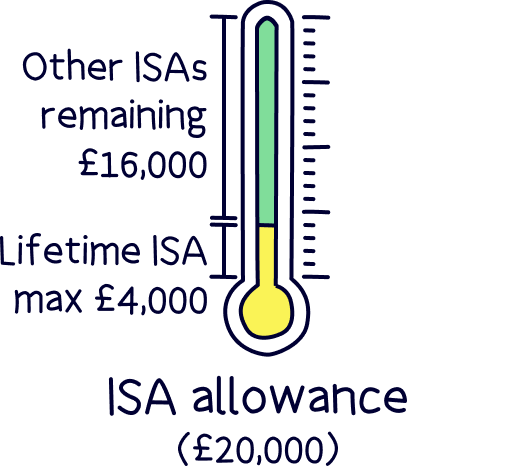

You can save up to £20,000 per tax year (your ISA allowance), which is a total across all your ISAs (if you have more than one).

Learn more with our guide to Cash ISAs.

You guessed it, these work like a Stocks and Shares Lifetime ISA, where you can make investments rather than saving cash. And depending on the provider, you can either let the experts handle things, or make your own investment decisions.

You can save and invest up to £20,000 per tax year, which counts as a total across all of your ISAs.

There’s a lot more Stocks and Shares ISA providers out there than Lifetime ISA providers, so you’ve got a lot more options when it comes to picking which experts you’d like to use, or which investment platform (app or website) to use for your own investments.

Check out the best investment platforms for all of our top picks, and learn more with our guide to Stocks and Shares ISAs.

Yep! You can have two or more ISAs, as many as you like in fact – as long as you don’t save more than £20,000 per tax year, and of that, £4,000 into a LISA.

However, you can’t save into more than one LISA each tax year. But, you can open another one in the next tax year if you want to, as long as you don’t then save into your old one – but you can transfer a LISA to a new provider if you want to, instead of opening a new account.

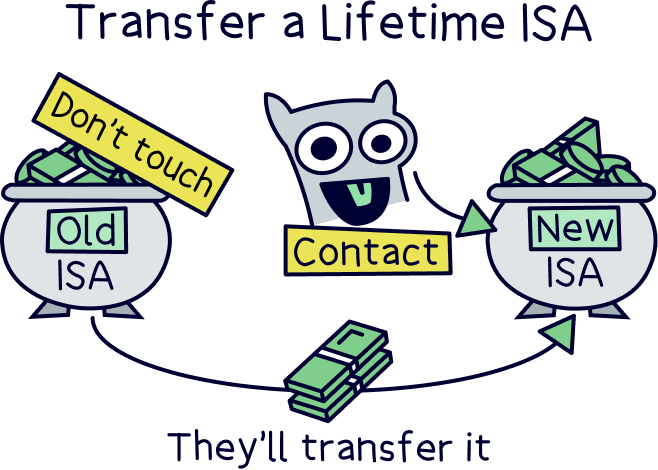

If you’ve already got a Lifetime ISA account, great. You can transfer your LISA to another provider if you like – perhaps one you prefer, or has a higher interest rate. Check out the best Lifetime ISAs to make sure you’re making the most of your LISA and getting a top interest rate.

If you’ve got an ISA already, which can be either a Cash ISA or a Stocks and Shares ISA (which are both the same as the two types of LISAs, just without the 25% government bonus), you can transfer these to a LISA too.

However, you can only transfer £4,000 each tax year as that’s the limit on how much you can save into a LISA. You can save up to £20,000 across all your ISAs, which also includes the £4,000 allowance for your Lifetime ISA savings.

All you need to do is get in touch with your new LISA provider and they’ll take care of everything. If you haven’t got one yet, let them know when you’re registering and they’ll handle it straight away.

That’s it for the right ISA for buying a house, a Lifetime ISA!

Lifetime ISAs are really great at boosting your house deposit and getting on the housing ladder quicker. You’ll get a massive 25% bonus from the government on everything you save, up to a maximum of £4,000 per tax year – so up to £1,000 free each year. Plus they grow tax-free.

You can either choose to save via a Cash Lifetime ISA, where you simply earn interest on your money, or invest your cash via a Stocks and Shares LISA (can work out better when saving for a number of years (typically over 5 years), but there’s no guarantees).

To recap, scroll up our click our recommended best Lifetime ISAs.

And remember, you’ll need to have your LISA open for at least 12 months before you can use it, so don’t delay, open yours now to start the timer – you only need to add £1.

All the best saving for your first home!

Check out Moneybox, it has one of the highest interest rates, and it’s easy to use.

Check out Moneybox, it has one of the highest interest rates, and it’s easy to use.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things savings, with many years of combined experience writing and talking about savings (and ISAs). Some of our team were top financial advisors. We understand the ins and outs of planning your finances well, how to communicate savings in an easy to understand way (we hope you agree), and of course, how to get the best savings rate for you.

More than 20 years of combined experience researching and writing about savings

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of savings companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out Moneybox, it has one of the highest interest rates, and it’s easy to use.