Article contents

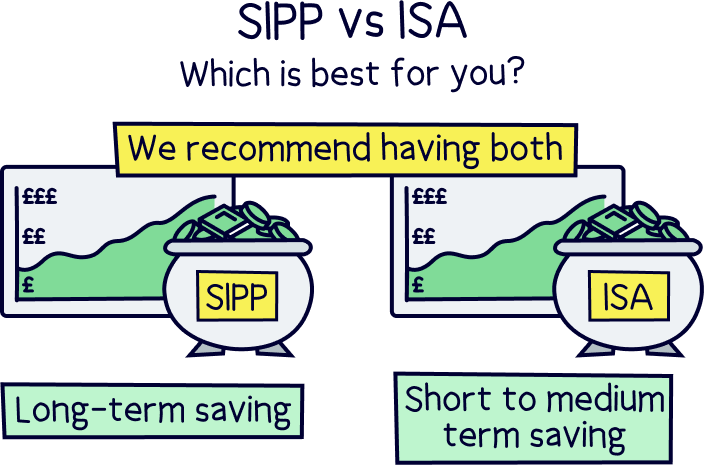

Both SIPP and ISA accounts are great for different reasons, and you don’t need to pick between them! Use a SIPP for long-term saving for retirement and an ISA for short-to-medium term saving. We recommend having both.

Saving and investing your money? Great decision. It’s the best way to grow your savings over time. But which type of investment account is the best way to invest your hard earned money, a self-invested personal pension (SIPP) or an ISA?

Let’s find out. Each account has different benefits and is suited to different types of saving goals – but they’re both great in their own right.

In a rush and want to know what the best SIPPs and ISAs are? Check out our top pensions and our top ISAs.

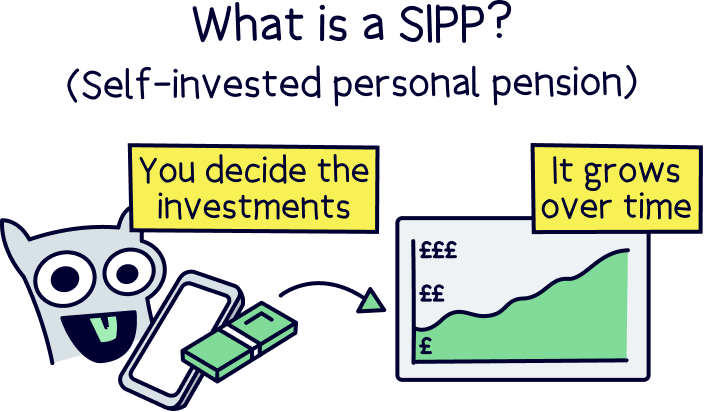

A SIPP, which stands for self-invested personal pension, gives you full control over your money in your pension for your retirement, you choose where and when your money is invested.

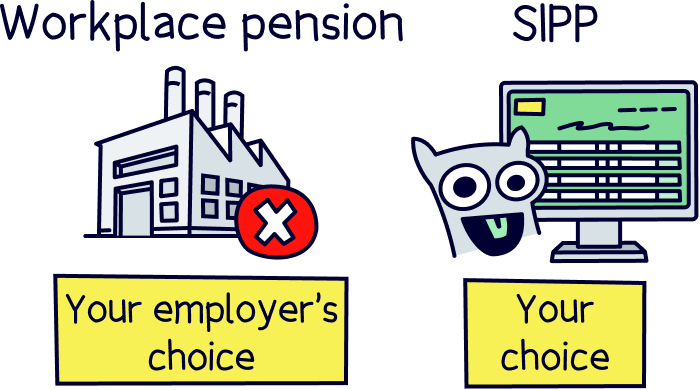

It’s a type of private pension, so similar to a pension you’ll get from your employer (called a workplace pension), except you don’t have to use your employer's pension provider – they can often be expensive with a poor track record of investing money. With a SIPP you get to choose!

A SIPP is a great addition to a workplace pension, and pretty essential if you are self-employed and don’t have a workplace pension. If you don’t have a pension you might run into financial trouble later in life if you’re going to rely on just the State Pension (it’s far lower than what you need to live comfortably on. At the moment, the full State Pension is £230.25 per week.).

Nuts About Money tip: Our retirement income calculator can help you estimate how much money you will have in retirement and you can find out the average pension pot in the UK.

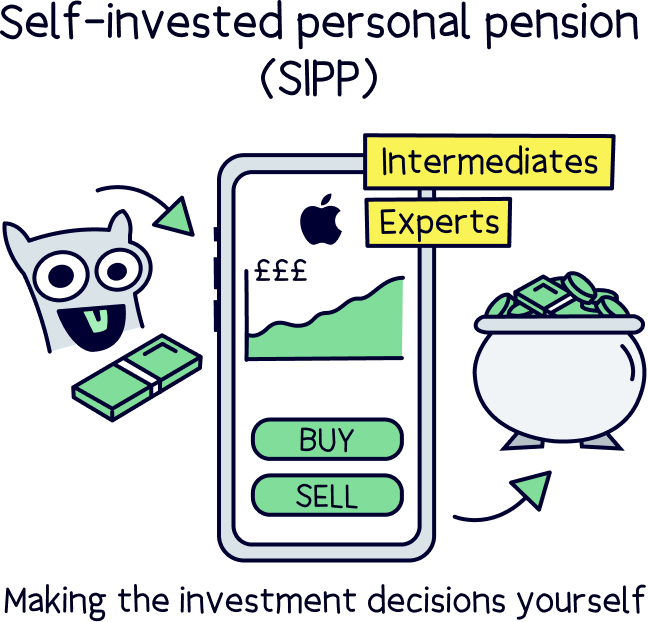

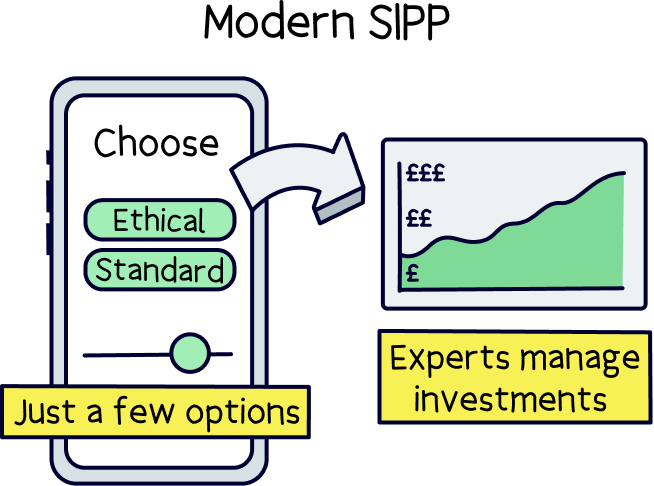

Traditionally a SIPP was solely to manage your own investments, such as you deciding which individual stocks and shares to buy (where you own a tiny portion of a company), or investment funds (groups of investments such as a group of different company’s shares) – so you needed to know what you were doing.

You can still do this, but more recently, you can also let the experts manage your investments through a SIPP too (it’s confusing right?). So you still get the flexibility and control over your pension, but with the support of professionals growing your money. It’s the best of both worlds.

If this sounds interesting check out Beach¹, they offer a tax-free Stocks & Shares ISA¹ managed by a team of experts and you can even set up a pension pot¹ too. It's also easy to use with a great app. Here’s our Beach review to learn more.

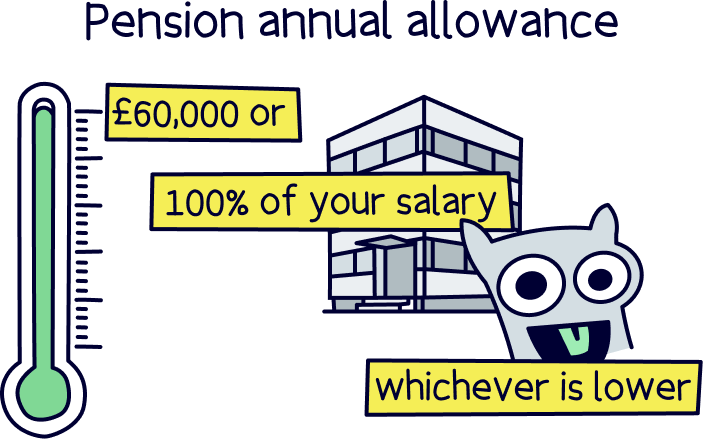

You are able to pay in £60,000 each year or 100% of your salary (whichever is lower). Well, we say pay in, we mean get tax benefits on, you can technically pay in as much as you like, but it’s not a good idea as you’ll then be paying tax on your contributions.

If you’ve already decided a SIPP is for you, check out our best private pension providers UK. But if you want to get an ISA check our top ISA recommendations.

Still want to know more about a SIPP? Read on…

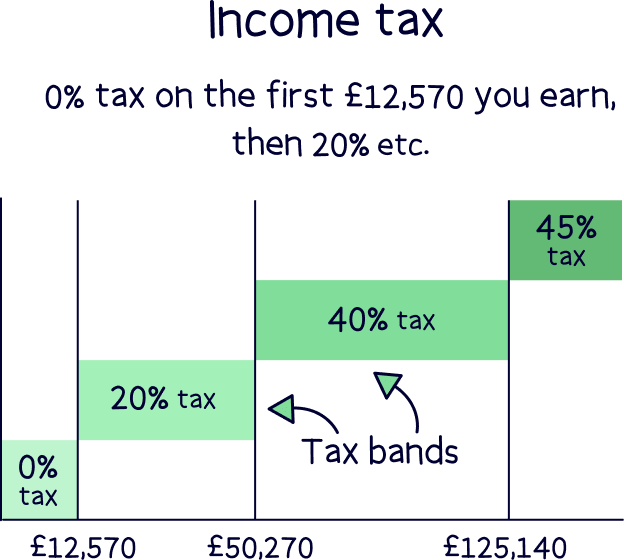

Let’s rewind for a second, with pensions, the government wants you to have a nice big pension pot by the time you come to retire (so you don’t have to rely on the government too much) – so they let you save your money within a pension before you pay income tax (that’s a tax on your earnings).

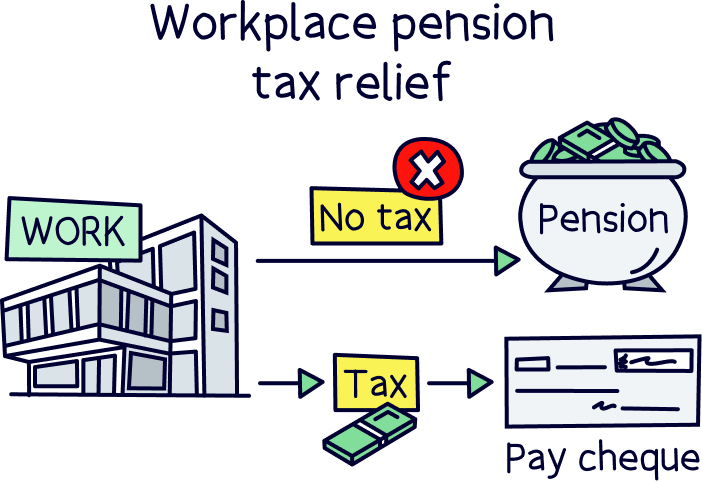

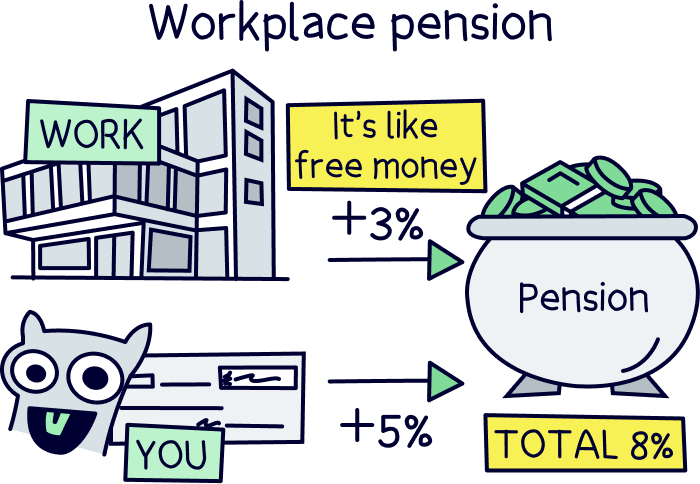

With a workplace pension (a pension through work), your money goes into your pension before paying tax, and this is all handled by your employer.

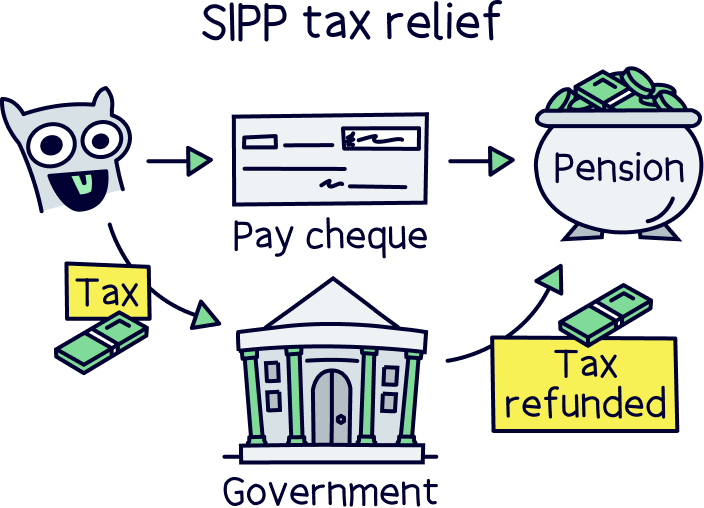

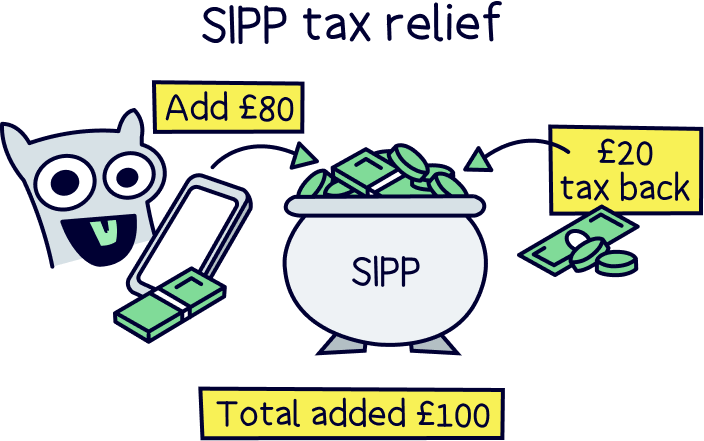

With a SIPP you’ll get the same tax free saving benefits as a workplace pension. Except instead of your money going into your pension before you pay tax, you’ll get taxed as normal through your pay cheque (salary) and then the government will refund the tax you’ve paid back into your SIPP, which is all automatically handled by your SIPP provider.

Let’s say you pay £80 into your SIPP, the government will automatically add £20 into your pension too. It’s a 25% bonus, which works out the same as if you had paid £100 into your pension before you paid tax (as you’d have paid 20% tax on your salary, which gives you £80).

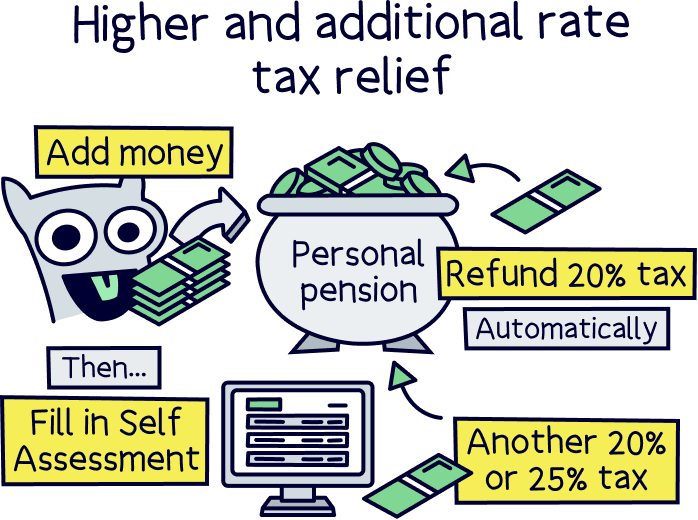

Now it gets even better. If you’re a higher-rate tax payer, (pay 40% tax), or an additional rate tax-payer (pay 45% tax), you’ll get the tax you paid at that rate too!

However, you’ll have to claim this back yourself on your Self Assessment tax return (it’s pretty easy to do but if you want help try Taxfix¹, their service is quick, low cost and 5* rated).

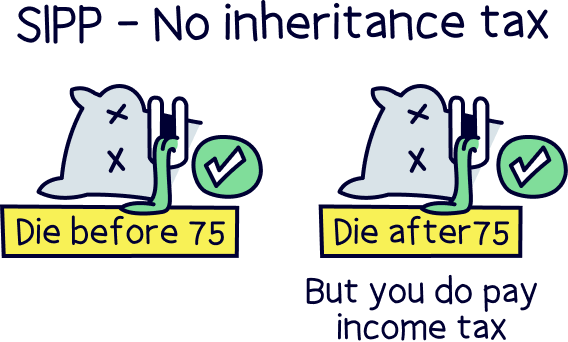

A SIPP is not subject to inheritance tax – so you can pass it down to your family completely as it is when you die. If you die before 75, it’s completely tax free for your family to receive too, but after 75, they’ll have to pay income tax on the amount.

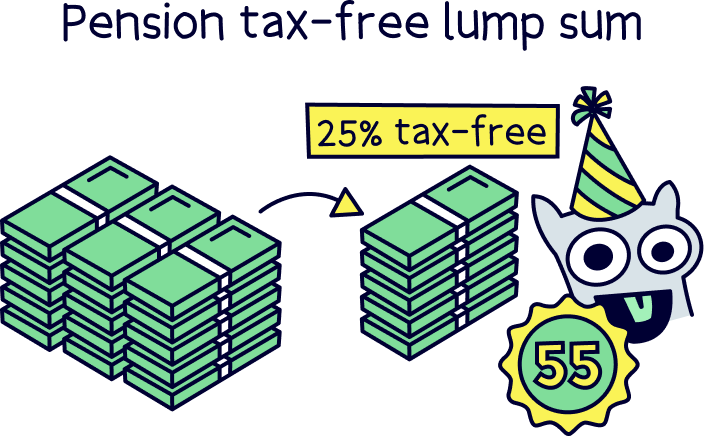

When it comes to taking your money out of your pension, the first 25% of withdrawals are tax-free, the rest you might pay income tax (it depends on your salary at the time).

The amount of tax you’ll actually pay depends on how much you withdraw each year (and any other money you earn), you may not pay any tax because of your personal allowance. You can earn £12,570 each year and not pay any tax at all. (it’s similar to how your salary works now).

However, don’t let this put you off a SIPP, despite paying income tax, you may still have made more money because of that lovely government bonus that offsets any tax paid.

We’ve researched, reviewed, and rated all the top SIPPs to help you choose.

If you’re saving for retirement, then a personal pension is probably the best option for you.

However, there’s one caveat, it’s often better to pay more into your workplace pension if your employer is willing to match your contributions and pay more in themselves – we mean more than the legal minimum, which is when you pay in 5%, your employer must pay in 3%.

For instance, if your employer matched contributions up to 10%, then you should aim to pay in 10% too – as you’re getting a lot of free cash. However, employer contributions above the legal minimum are quite rare.

So, that’s where personal pensions come in – you can keep saving for retirement all by yourself, without the need for an employer, and still benefit from those tax-free savings – with the lovely bonus from the government.

Plus, you can decide exactly how and where your money is invested.

So what about an ISA then? By an ISA, we mean a Stocks and Shares ISA (ISA stands for Individual Savings Account). It’s an awesome account where everything you put into it, is completely tax-free, forever!

However you would have already paid tax on the money you put into your account (as income tax from your earnings, such as a salary). Whereas with a pension you are saving money before you pay tax (so you don't get the 25% bonus we mentioned above).

All of the money you make from investing within the account is all yours – there’s no tax to pay on your profits, such as Capital Gains Tax or tax on dividends (profits paid out to shareholders). Pretty great right?!

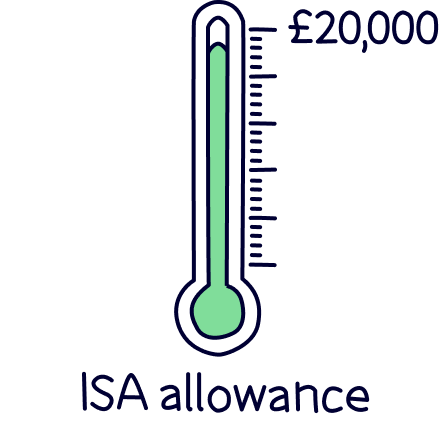

You are allowed to save up to £20,000 per year across all of your ISAs (called your ISA allowance) – so that’s a Stocks & Shares ISA, Lifetime ISA and a Cash ISA.

Although, unless you are saving for your first home, you’ll probably only want a Stocks & Shares ISA.

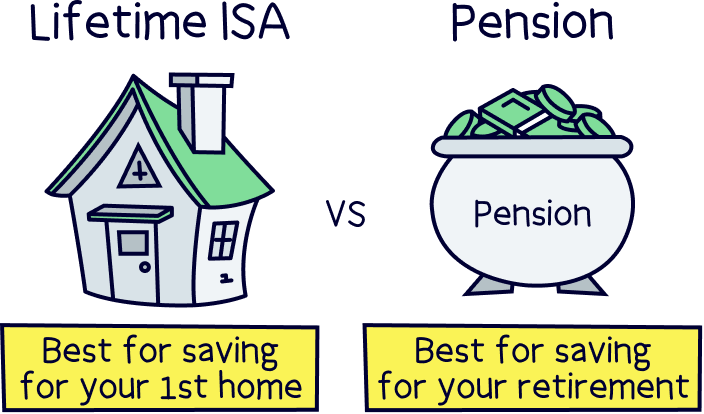

If you are saving for your first home, a Lifetime ISA lets you save up to £4,000 per year and gives you a 25% bonus, but it can only be used to buy your first home or accessed after the age of 60. It isn't a replacement for a pension. Learn more with our guide: Lifetime ISA vs pension.

To get an ISA you'll have to open one through a high street bank, investment platform (a website or app) or a stock broker. Most will offer an ISA in the UK but not all.

You can find the best ISA for you with our investment platforms comparison tool. Simply select ISA from the settings.

An ISA is great to use for savings goals that aren’t retirement or very long term, as you can withdraw your cash whenever you like. So, perhaps you’re saving for something else like a nice car (we don't recommend buying an expensive car, keep investing if you can and make more money!), or are sensibly letting your savings grow over time by investing them, but still want access if you need it.

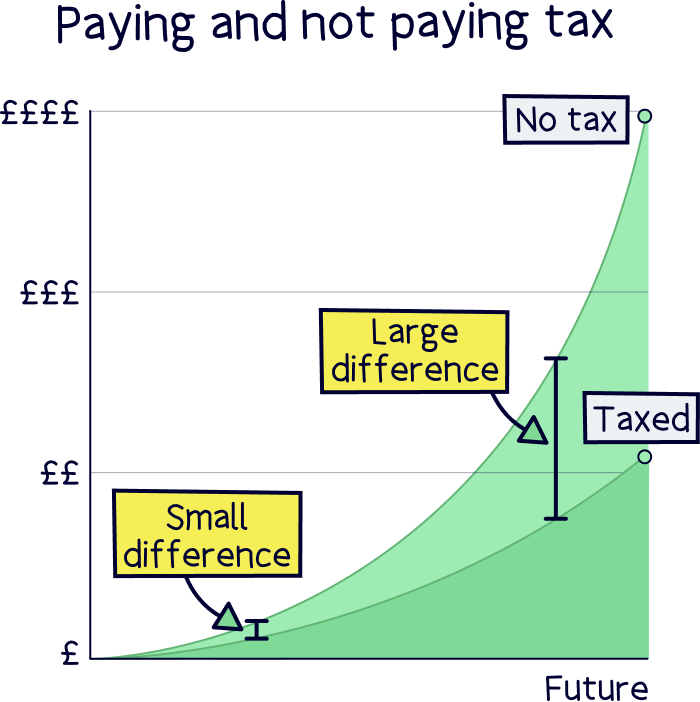

Not paying tax on the money you make can make a big difference, especially when your savings start growing to large amounts – you’ll end up paying a big chunk in tax if it’s not inside an ISA (or pension), when you sell an investment.

Outside of an ISA, you’ll have to pay Capital Gains Tax on all profits you make above £3,000 per tax year (April 6th to April 5th the following year). Capital Gains Tax is 18% if you’re a basic rate taxpayer (earn less than £50,270 per year in income, e.g. your salary), and 24% if you’re a higher rate taxpayer (earn more than £50,270 per year).

Note: accounts that aren’t an ISA are called a General Investment Account (GIA).

So which is best for you?

They’re two different accounts, both with a massive benefit – growing your money over time without paying any taxes!

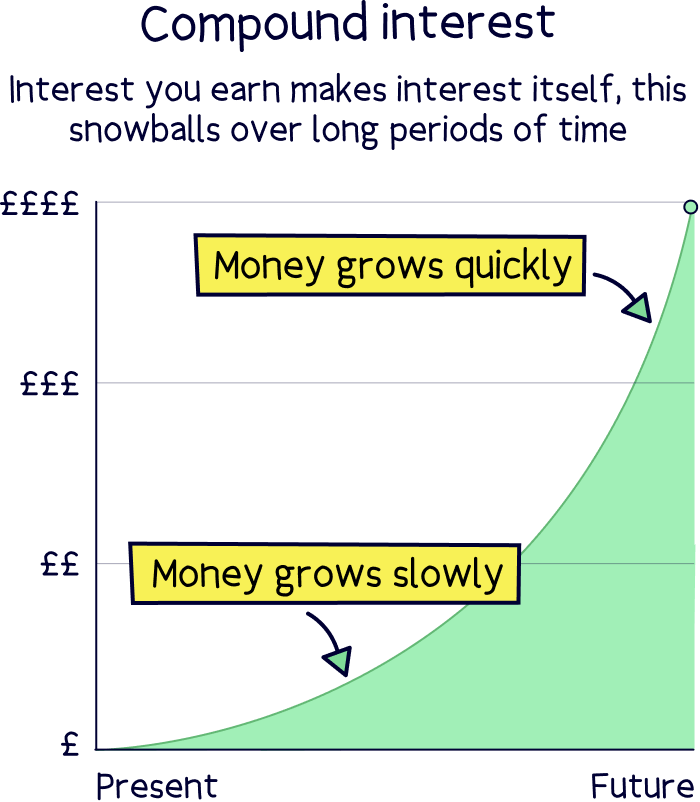

Not paying tax makes a huge difference on how fast your money can grow due to something called compound interest – which is where the money you make starts making you money too, and so on and so on, and this cycle continues over time, making you a lot more money.

However, you don’t need to think which one is better, they’re both suited for different types of saving.

A personal pension is far better for long term saving. You’ll get a 25% bonus on everything you put in, which can increase to 40% or 45% if you’re a higher rate or additional rate tax-payer. That’s a very big deal!

Just make sure you are prepared to lock your money away until you’re at least 55 (57 from 2028).

If you’re not happy to lock your money away for a long time, that’s when an ISA comes in.

An ISA is great for short-to-medium term saving, as you can withdraw it whenever you like, and everything you make is tax-free! We recommend having both so you can have the best of both worlds.

So to recap, SIPP for long-term saving, and an ISA for short-to-medium term saving. And you can have both!

Here’s where to find the best self-invested personal pensions and the best investment platforms for ISAs.

We’ve researched, reviewed, and rated all the top SIPPs to help you choose.

We’ve researched, reviewed, and rated all the top SIPPs to help you choose.

We’ve researched, reviewed, and rated all the top SIPPs to help you choose.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

We’ve researched, reviewed, and rated all the top SIPPs to help you choose.