Article contents

Yes! You can swap your Cash LISA for a Stocks and Shares LISA super easily. Hooray! However, not all LISA providers will be happy to let you make the switch, so you’ll need to find one that’s happy to sort you out.

A Lifetime ISA, known as a LISA, is a wonderful little thing that helps you save up to buy your first home, or to tide you over later on in life. It’s basically a special type of ISA (Individual Savings Account) where the government adds a 25% bonus to the money you put in, to help boost your savings. Kerching!

But to make matters a liiiiittle bit more complicated, there’s more than one type of LISA. Gasp! You’ll have to choose between a Cash LISA and a Stocks and Shares LISA. Here, we’ll look at what happens if you decide you want to swap your Cash LISA to a Stocks and Shares LISA, which is the better move for long-term savings (in other words it should make you lots more money!). But first…

Just like a Cash ISA, a Cash LISA is a type of ISA that lets you save cash and earn tax-free interest. In case you’re not sure, interest is a charge that you either pay when you borrow money, or earn when you lend money – with an ISA, you get to earn interest on the money you leave sitting in your account, and better yet, you also get to avoid paying any tax on it!

Cash LISAs have an added benefit over your average Cash ISA. The government will also add a 25% bonus to any money you put into your LISA. Yep, that’s right, as long as you don’t pay more than £4,000 per year into it, the government will add 25% to whatever you pay in. Nice!

This is because of something called tax relief. It means that you don’t have to pay any tax on the money you pay into your LISA – instead, the government refunds the tax you’ve paid straight into your LISA itself, boosting your savings.

The only catch is that you can’t take your money back out of your LISA unless you’ve turned 60, developed a terminal illness or you’re going to buy your first home. If you use it for anything else, you have to give back that 25% bonus. Doh!

If you thought that Cash LISAs sounded good, you’ll LOVE Stocks and Shares LISAs! With Stocks and Shares LISAs, you still get that juicy 25% government bonus on any money you put in. But if you’re saving for longer than a few years, you’ll also find it’s much easier to grow your money.

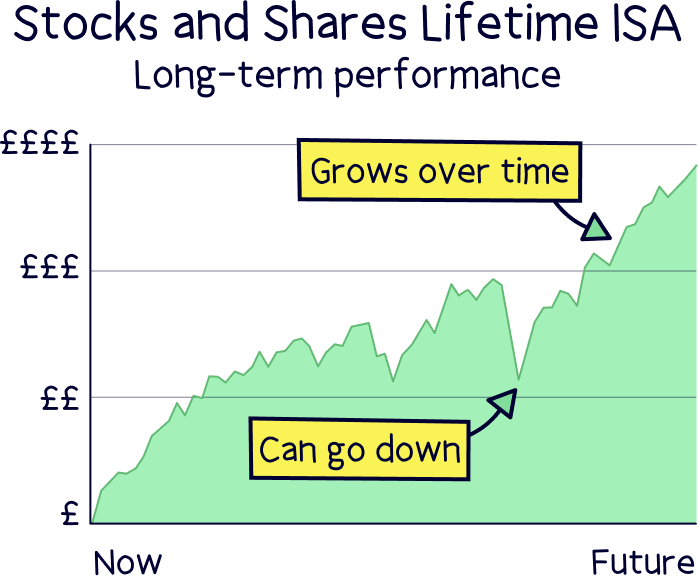

Remember how we said that Cash LISAs allow you to earn interest on the money you put into your account, but that interest rates are really low right now? Well, Stocks and Shares LISAs work differently. Instead of your cash just sitting in your LISA collecting dust, it’s invested in things like stocks and shares, which is basically owning small parts of companies. The idea is that as these companies (hopefully!) grow and increase in value, those stocks and shares will get more valuable and make you more money – money you won’t have to pay tax on!

As a general rule of thumb, you can expect a Stocks and Shares ISA (including LISAs!) to make you returns of around 8% per year. That’s a lot more than what you’d get from a Cash ISA!

If you’re nervous about investing, don’t worry – you don’t have to do a thing. Instead, your LISA provider (the company managing your ISA) will work with an investment fund who will invest your money for you. They’re experts, so your money is in safe hands!

In the medium-to-long term, your money can grow quite a lot, as it’s put to work trying to make more money for you (and, of course, you have the 25% government bonus to enjoy on top of that). Just remember that, like with a Cash LISA, you’ll still only be able to take your money out to buy your first home or later on in life.

Check out Moneybox, it's easy to use, low cost overall and the customer service is excellent.

An ISA transfer is where you switch your current ISA for a new one, often with a different provider. When you transfer an ISA, you’re basically just moving all the cash (if you have a Cash ISA) or the investments (if you have a Stocks and Shares ISA) in your account to a new ISA. Simple!

You can either transfer your ISA to another one of the same type (for example, swapping a cash ISA for another cash ISA). Or, you can change the type of ISA you have when you transfer it (for example, swapping a Stocks and Shares ISA for a Cash ISA, which would involve selling your investments and putting the cash value of them into a new Cash ISA).

Anyway, here’s some good news for you: transferring a LISA is exactly the same! So, it should be easy to swap your Cash LISA to a Stocks and Shares LISA or vice versa. You just have to find a new ISA provider you fancy switching to, and then ask them to transfer your ISA for you. As long as they accept ISA transfers, you can just sit back and let them handle it all for you.

There’s just one problem: not all providers are happy to accept ISA transfers. And even fewer will be happy to transfer a Cash LISA into a Stocks and Shares LISA.

Does that mean you should abandon the idea altogether? Absolutely not! It is doable, it just takes some digging to find a provider who’ll let you do it. However, we’ve done the hard work for you – Moneybox¹ is easy to use, low cost overall and the customer service is excellent. There's also AJ Bell¹ you can transfer an existing Cash LISA into one of their Stocks and Shares LISAs. Enjoy! (They're one of the best online stock brokers in the UK).

Firstly, it’s important to remember that everyone’s different. So, what’s best for someone else might not be best for you. However, in our opinion, when it comes to Cash ISAs vs Stocks and Shares ISAs, Stocks and Shares ISAs are by far the better option. At least, they are if you’re going to be saving up for more than a few years (which we’d always recommend).

A quick reminder: with Stocks and Shares LISAs, your money is used to invest in things like stocks and shares. This means it’s put to work making more money for you, which will hopefully result in far more money in the long-term!

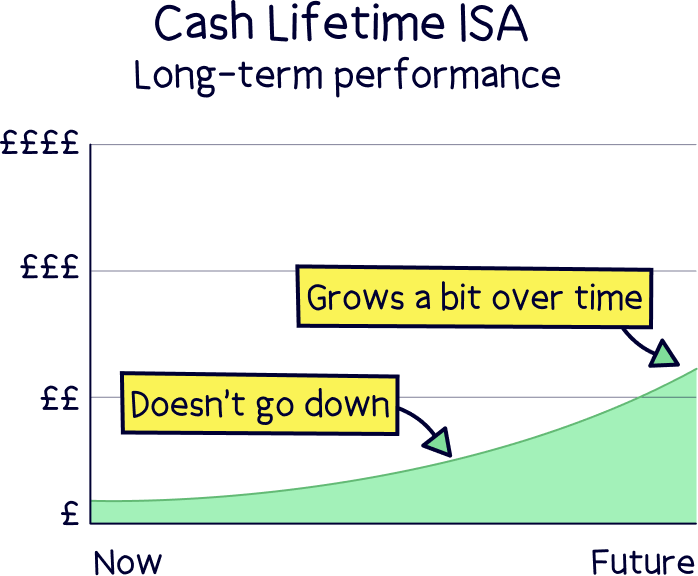

On the other hand, with a Cash LISA, your money just sits there in an account. Yes, it earns interest. But because interest rates are really low at the moment, it’s unlikely to earn you much if anything at all in the long run, especially once you take into account inflation (inflation refers to how goods and services get more expensive in an economy over time).

So, the main reason to transfer your Cash LISA to a Stocks and Shares LISA is to grow your money faster.

That said, Cash LISAs have their benefits, especially if you’re saving for the short-term. Let’s say you want to buy your first home in a couple of years. In this case, a Cash LISA may be the safer option. Stocks and Shares go up and down in value, so although a Stocks and Shares LISA is likely to make money for you in the long-term, there’s no guarantee that it will go up in the short-term.

A Cash LISA, on the other hand, will often be fixed-rate for a certain period of time, which means it will guarantee you a set amount of interest each year. That means you’ll know your money will at least hold its value and will be there ready and waiting for you to buy your first home.

Of course, as time goes by, your circumstances might change. Maybe you’ve now bought your first home, or maybe you’ve decided you’d rather save long-term. In this case, transferring your Cash LISA to a Stocks and Shares LISA can be a great way to make sure your LISA is evolving with your needs.

Yes! You can have both a Cash LISA and a Stocks and Shares LISA. So, if you already have a Cash LISA and you want to open a Stocks and Shares LISA, you don’t have to transfer it. You could just open a new one.

Opening a new Stocks and Shares LISA instead of doing a LISA transfer has its benefits. It will likely give you a bigger choice of LISA providers, which means you’ll often be able to get a better deal (Stocks and Shares LISAs come with fees to have your money managed by an expert and these fees vary depending on which provider you go with).

It also means you’ll have one LISA that’s better-suited for saving for the short-term and one that’s better-suited for saving for the long-term. Just remember that, unless you’re saving to buy your first home or you become terminally ill, you won’t actually be able to access your money until you turn 60 (unless you pay 25% of it back to the government, but we doubt you want to do that!).

On the downside, opening a new Stocks and Shares LISA instead of doing a transfer means that all those lovely savings sitting in your Cash LISA will do just that – carry on sitting there doing… well… not a lot for you. Transferring those savings into a Stocks and Shares LISA means they can be put to work generating more money for you. Kerching!

Oh and there’s something really important that we should mention. Even though you can have both a Cash ISA and a Stocks and Shares ISA, you can only open or pay into one LISA per tax year (a tax year goes from the 6th April to the 5th April, unlike a calendar year which goes from the 1st January to the 31st December). That means you could open and pay into a Cash LISA this tax year if you want to, but then you can’t open or pay into another one until next tax year. So, it requires patience!

First things first, if you want to transfer your Cash LISA to a Stocks and Shares LISA (or you want to transfer any other kind of ISA), one thing’s really important. You must NOT close your LISA.

Why? Well, if you close your LISA (or any other kind of ISA), you’ll be taking your money out of its tax-free wrapper (remember how you don’t have to pay any tax on the money your ISA generates?). Basically, your money or investments are protected from the taxman, but only while they’re in your ISA. As soon as you take those savings out, they won’t be protected anymore and the taxman can come for them. Yikes!

Not only that, but with a LISA, you also get that lovely 25% government bonus on the money you put in there. But again, as soon as you take out your money or you cash in those investments, you’ll face a hefty 25% charge.

Now, you might be thinking ‘I’ll just be giving the government back their bonus, so it’s not that big a deal.’ But you’ll actually have to pay 25% on the whole amount you withdraw, so you’ll end up with less than what you initially put in. We know, we know, it sounds complicated, you can find out more about withdrawing money from your Lifetime ISA here.

Anyway, now you know all about what not to do, we should probably tell you what you should do. Luckily, transferring your LISA is really easy.

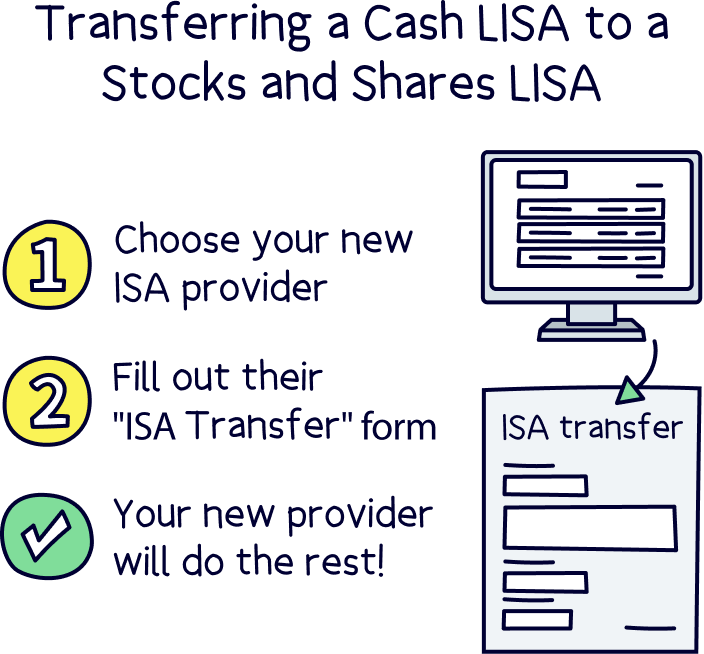

First things first, you’ll need to decide which LISA provider you want your new Stocks and Shares LISA to be with. You can compare deals and find the best one for you with our guide to Lifetime ISAs.

Remember, not all providers will let you transfer a Cash LISA to a Stocks and Shares LISA, so you’ll need to choose one that is. If you’re not sure where to start, check out our recommendations below. They will happily transfer a Cash LISA to a Stocks and Shares LISA.

Top rate

Saving for your first home? Moneybox could be for you.

Moneybox is the go-to place for Lifetime ISAs – it’s easy to use, and you’ll be able to manage everything on a great mobile app.

You can either pick from saving cash (Cash Lifetime ISA), and benefit from a great savings rate. And there’s no fee for saving cash.

Or, you can make your own investments (Stocks and Shares Lifetime ISA), and pick from a range of investment options (including individual US shares such as Apple and Amazon). Fees will apply.

Moneybox will handle everything behind the scenes, and collect your 25% government bonus and automatically add it to your account.

Overall, it’s low cost overall, and the customer service is excellent.

Note: don’t wait to get started, as you’ll need to wait 12 months before you can use your LISA to buy a home – all you need to do is add £1.

AJ Bell is well established, with a good reputation.

It's one of the cheapest traditional stock brokers out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is great too.

Overall, it's one of the best options.

Check out Moneybox, it's easy to use, low cost overall and the customer service is excellent.

Check out Moneybox, it's easy to use, low cost overall and the customer service is excellent.

As long as your new provider accepts LISA transfers, they’ll be able to sort out the whole transfer for you! Normally, you just need to give them your old LISA provider’s details and let your new provider know what you want to transfer over. You may also need your old account details to hand.

It’s usually super easy to do this online, by filling out an ISA transfer form. Alternatively, some providers will also let you do it over the phone if you’d rather chat to a human. Either way, it shouldn’t take more than a few minutes. You won’t even break a sweat!

Now all that’s left is to sit back, relax and leave the hard work to your new provider. That’s right, you shouldn’t have to do a thing more!

It can take up to 30 days to switch a Cash ISA to a Stocks and Shares ISA. So, you can just forget all about it until the transfer completes (your new provider should tell you when it’s all done). Then, enjoy watching your cash get invested and, hopefully, grow before your eyes!

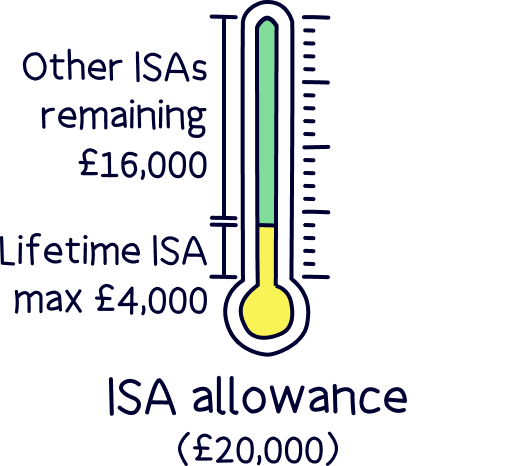

Now, there’s one thing we haven’t yet touched upon. Each tax year (remember, between 6th April and 5th April), you’re only allowed to pay up to a certain amount of money into ISAs. This is known as your ISA allowance.

The ISA allowance can change from year to year, but at the moment, the maximum you’re allowed to pay into ISAs in one tax year is £20,000. And only £4,000 of this allowance is allowed to go into your Lifetime ISA (remember, you can have more than 1 LISA, but you can only pay into 1 each tax year).

But now for the good news: ISA transfers (and therefore LISA transfers!) don’t count towards your ISA allowance. Hoorah!

So, say you haven’t yet contributed to your Cash LISA this tax year. And say there’s £10,000 in there. If you want to transfer it to a Stocks and Shares LISA, you can move the full £10,000 to your new LISA and then still pay £4,000 into your new LISA before the tax year ends.

Now let’s say that this tax year, you’ve already paid £4,000 into your Cash LISA and now you want to transfer it to a Stocks and Shares LISA. In this case, you can still do the transfer, as long as you transfer the whole thing. But you won’t be able to add any more money into your Stocks and Shares LISA until next tax year, as you’ve already used up your £4,000 allowance. Makes sense, right?

Transferring your Cash LISA to a Stocks and Shares LISA is totally doable. In fact, other than finding a new provider, you won’t have to worry about anything at all as they’ll handle the whole transfer for you. Winning!

However, if you have a Cash LISA and you want to open a Stocks and Shares LISA, don’t forget that a transfer isn’t your only option. Not all LISA providers will accept transfers, so you may be able to find a better deal by leaving your Cash LISA as is and opening a completely separate Stocks and Shares LISA with a provider of your choice. Just remember that you can only open and pay into 1 LISA each tax year, so depending on when you opened your Cash LISA, you may need to be patient!

To recap, our recommended LISA providers are above, click best LISA providers to see them again.

To learn more about LISAs (and why we love them so much!), check out our dedicated Lifetime ISA guide, and learn more about investing with our guide to investing for beginners (UK).

Check out Moneybox, it's easy to use, low cost overall and the customer service is excellent.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out Moneybox, it's easy to use, low cost overall and the customer service is excellent.