Article contents

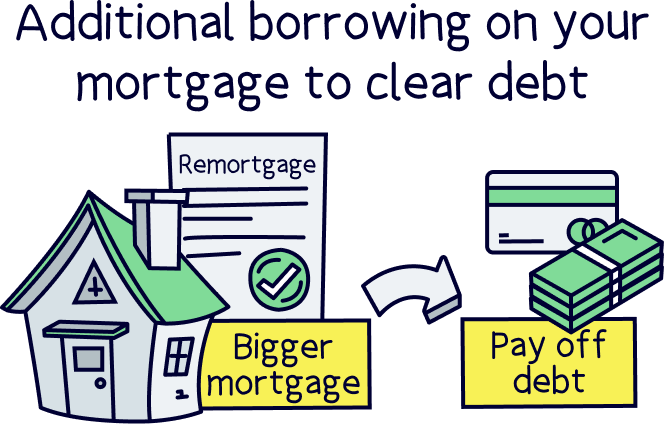

When you take on additional borrowing on your mortgage to clear debt, you’re essentially getting a bigger mortgage on your property so you can free up equity (cash). You then just use this cash to pay off your other debts and get yourself back on track.

Are you finding it hard to keep up with your debts? Or just want to manage your debts more efficiently by swapping many for one easy monthly payment?

If you’ve got lots of individual debts you’re paying off in lots of different places, it’s easy to feel like you’ll never be rid of them. But don’t worry – there are solutions out there to help you clear those debts and start again afresh. One possible solution is to take on additional borrowing on your mortgage.

Here, we’ll look at how it all works and why it might help.

Additional borrowing on a mortgage to clear debts basically just involves taking out a bigger mortgage to release equity. Let us explain.

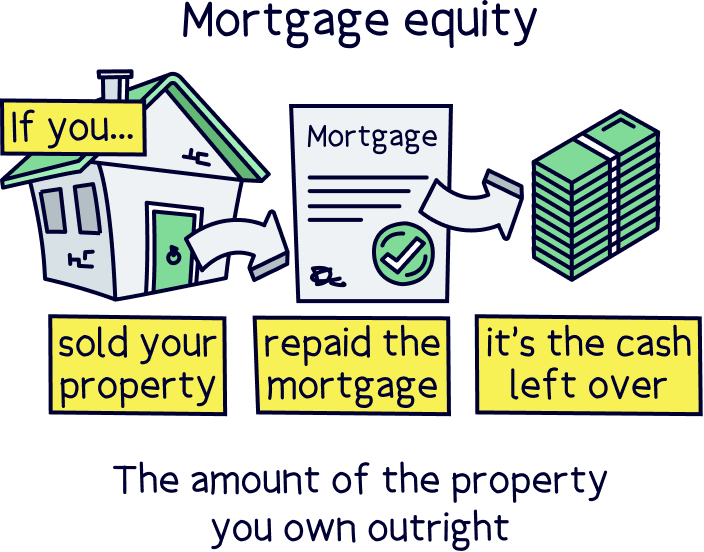

Equity is the amount of your property that you own outright, as opposed to the value of your property that you’ve borrowed and still owe your mortgage lender (mortgage lenders are the people that give out mortgages and are usually banks). In other words, your equity is the amount of your home’s worth that would go straight into your pocket as cash if you sold your property.

When you take out a bigger mortgage, you’ll be taking on additional borrowing and therefore reducing your equity. This could involve swapping your current mortgage for a new one or getting a second mortgage (we’ll explain how this all works in a bit). Either way, you get the difference back in cash, known as ‘releasing equity.’ Kerching!

You can use this cash for whatever you fancy (although your lender might ask you why you are doing it and the reason might affect whether you’re approved). It might be to cover your child’s uni fees, to pay for a broken boiler… or, you guessed it, to pay off existing debts. This could be a great solution if you’re struggling to keep spiralling debts under control (or you just fancy paying off expensive debts to get a better deal – we’ll reveal all shortly).

Getting additional borrowing on your mortgage to clear debt is commonly known as a debt consolidation mortgage or remortgage.

Tembo will find your best deal, fast, all with award-winning service.

Okay, okay, we know what you’re probably thinking. Why the hell would you take on more debt to clear your current debts?! A mortgage is a debt in itself, after all!

Well, there is a good reason (although it’s not going to be right for everybody!). Basically, mortgages tend to have much lower interest rates than most other kinds of loans. Interest is a charge that lenders make you pay for the pleasure of borrowing their money and is normally a percentage of the amount you owe them.

Let’s look at some examples.

An arranged overdraft is a loan that allows you to keep spending when you run out of money in your bank account. Normally, this kind of loan comes with interest rates that are between 19% and 40% APR. In other words, you’ll be charged between 19% and 40% of the amount you owe your lender each year.

Now let’s compare that to a mortgage. Current mortgage rates are often between 2% and 6%. So, much, much lower!

That means if you borrowed the same amount of money with a mortgage as opposed to an overdraft, you’d be charged a lot less interest each year. And that means lower monthly repayments that are easier to keep on top of. Winning!

But there’s one thing you’ll need to bear in mind. Just because you’ll be paying less each month with a mortgage, that doesn’t necessarily mean you’ll end up paying less overall.

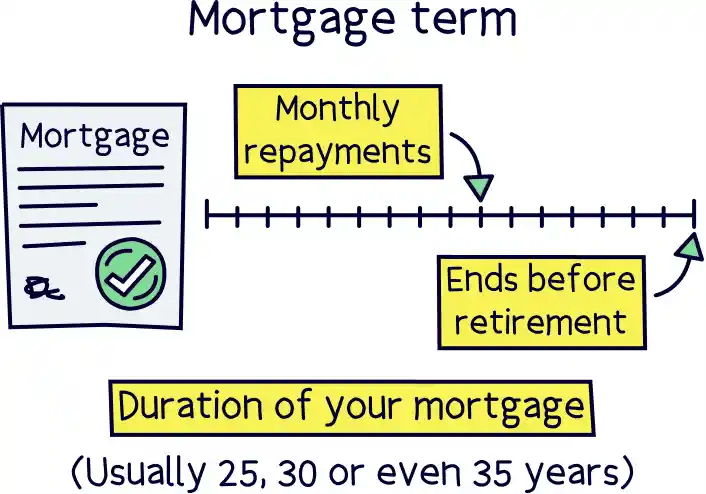

Mortgages tend to last a lot longer than other kinds of borrowing such as overdrafts. Often, you’ll pay off a mortgage over 25 or even 35 years (known as your mortgage term), while you’d normally aim to pay off an overdraft a lot quicker – say, over a matter of months.

This means that, even though you’ll pay less per month with a mortgage, you’ll be paying it every month for years to come, therefore paying more in total.

You’re going to hate us for saying this, but there isn’t really an easy answer. Everyone is different so it’ll all depend on your personal situation and how well you’re currently handling your debts.

Adding additional borrowing to your mortgage can be a lifesaver if you’re struggling to keep on top of spiralling debts or you just generally want to move your debts over to a loan that has a better interest rate. But it’s not all rosy, as normally you’ll spend years paying off the additional borrowing which means paying more in the long run. So, if you’re currently handling your debts easily, you might want to think twice. Tricky, huh?

Here are the main pros and cons of additional borrowing on a mortgage to clear debt, to help you work things out.

Want a little tip? You can take on additional borrowing on your mortgage to save on interest rates and then overpay on your new mortgage.

Overpaying is when you pay your lender more than what you owe, to pay your mortgage off quicker (although most mortgage types will charge you a fee if you overpay by more than a certain amount). That way, you get to reduce your interest and you won’t pay more overall because you’ll still be paying your mortgage off (relatively!) quickly. Just be careful as a lot of people have the good intention of making over payments but then don’t do it!

Okay, so we keep going on about additional borrowing on your mortgage and how it can help you to clear debts. But what exactly does it look like?!

Well, there are three main ways that it can work.

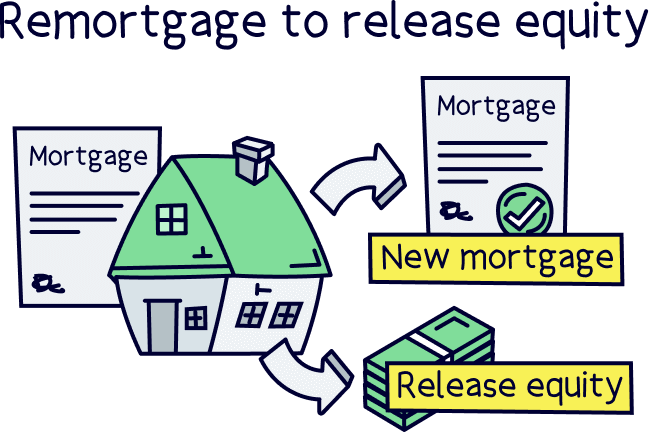

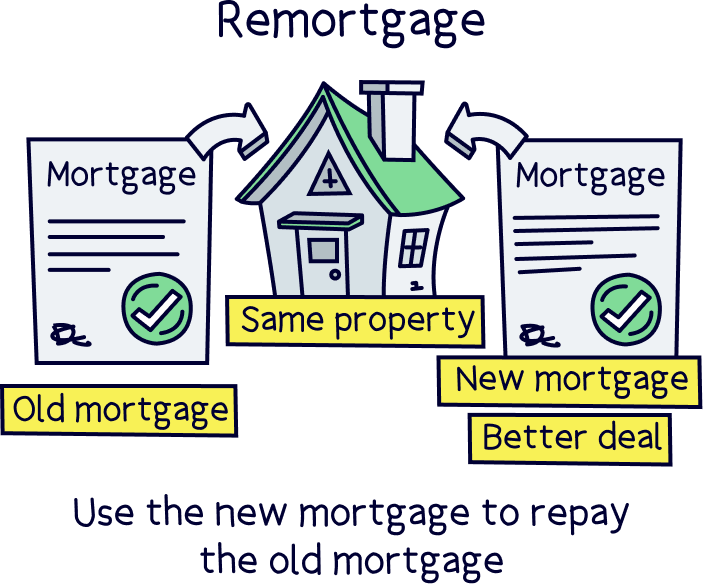

This is the most common way of getting additional borrowing on your mortgage. Remortgaging is when you swap your current mortgage for a new one, either with your existing lender or with a different lender altogether.

If you want to pay off debts, you can do something called remortgaging to release equity. This is when you swap your current mortgage for a new, bigger one. That way, you reduce the equity you have in your property and get the difference back in cash. Simple!

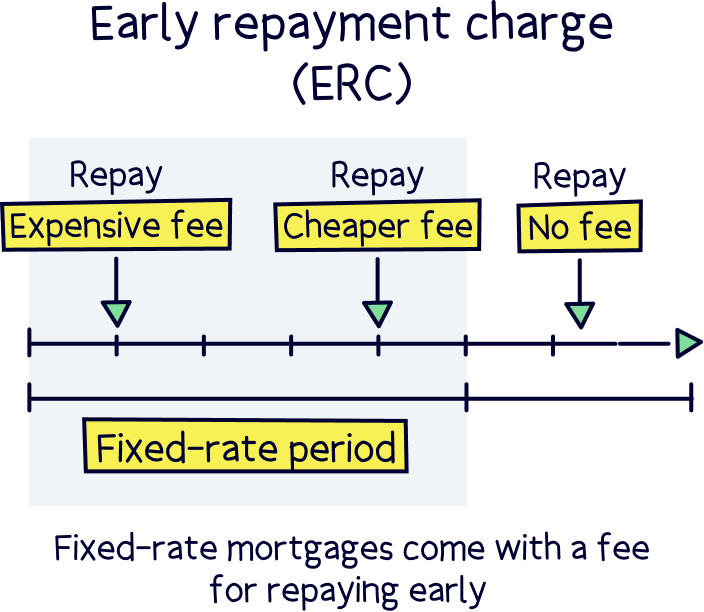

Just be careful that you take into account early repayment charges. An early repayment charge is a fee lenders often charge if you want to pay your mortgage back early. Basically, when you first get a mortgage, you’ll usually get access to a discounted deal that lasts for a set period of time. This period is known as your incentive or introductory period as your lender is essentially giving you a good deal to ‘incentivise’ you to choose them!

If you want to leave your lender before this period runs out, you’ll need to pay an early repayment charge, which could be pretty hefty. It’s usually a percentage of the amount you owe, so it could add up to thousands of pounds!

Ideally, this means you want to wait until the end of your incentive period before remortgaging to pay off debts. But of course, if you’re in desperate need of equity to pay those debts off, you might decide it’s worth biting the bullet and remortgaging immediately anyway. Ultimately, the choice is yours!

A further advance is when your current mortgage lender agrees to lend you more money on top of your existing mortgage. In other words, you can stay on the mortgage you’re currently on, and then borrow more from them on top. Sounds easy, right?!

The good thing about opting for a further advance is that, if you’re currently on a good mortgage deal, you can keep it as it is. Plus, if you’re in the middle of your incentive period, you won’t have to worry about paying an early repayment charge to leave early.

The less good side? Well, this extra borrowing will normally come with its own separate agreement. So, you won’t necessarily get to access the same deal you have on your current mortgage. Instead, the additional borrowing could have higher interest rates (although you might also find you get the same rate or sometimes even better!). You’ll normally have to pay an arrangement fee for your lender to sort the whole thing out too.

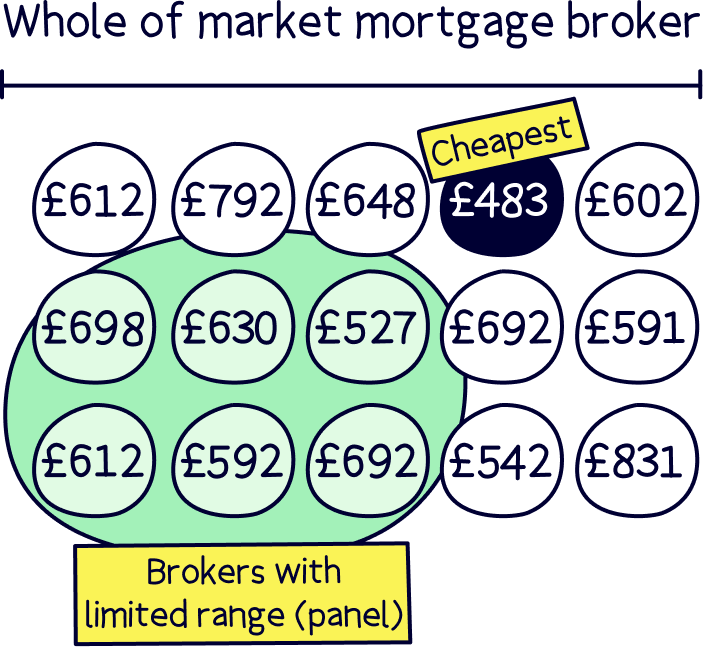

On top of that, you can only get a further advance with your current lender. While that’s not a bad thing in itself, the chances are they won’t have the cheapest mortgage deal for you. After all, there are over 100 mortgage lenders in the UK alone, all offering different rates and deals!

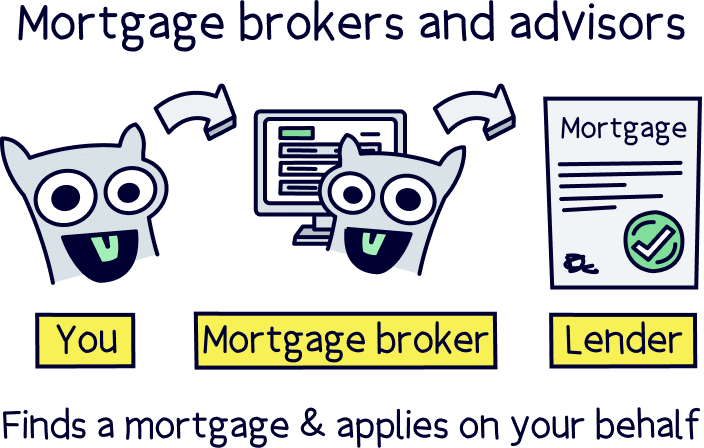

To find out whether it’s the right route for you, it’s best to use a mortgage broker (also known as a mortgage advisor). Here's how to find the best mortgage broker for you.

Whole-of-market mortgage brokers are experts who can compare all the different deals and lenders available to find you the best one for your circumstances.

Not sure where to find a good broker? Check out Tembo¹ they've got award-winning service, and will guarantee to find you the best mortgage. You'll also get 50% off their fee with Nuts About Money.

Last but definitely not least, a second charge mortgage is where you get a second mortgage on your current property. Yep, it’s exactly what you’re thinking: you end up with 2 mortgages on 1 home!

Just like a further advance, your current mortgage gets to stay exactly as it is (meaning you don’t have to worry about any early repayment charges!) and you just borrow extra money on top. But this time, rather than getting the extra borrowing from your current lender, you actually use the equity you’ve built up in your home to get a whole other mortgage with a second lender.

The great thing about this is that you don’t have to settle for whatever rate your current lender is happy to give you. Instead, you can compare lots of different lenders to find the best deal out there on your additional borrowing (don’t worry, a mortgage broker can give you a hand with that!).

Just remember that any mortgage is a big commitment. And 2 mortgages means double!

Think about it: you’ll need to keep up with 2 lots of monthly mortgage repayments. And your home will be used as security by 2 different lenders. In other words, if you stop paying either of your mortgages, your property could get taken away from you. It’s an absolute last resort (we promise!) but it’s important that you know what you’re signing up for!

You’re probably wondering whether you can add enough borrowing to your mortgage to clear your debts.

Ultimately, a lot of it comes down to how much equity you have in your property (although they’ll also look at things like your age, income, expenses and credit score). Without enough equity, you won’t be able to borrow more in order to release it and get that all-important cash in your pocket. Here’s how to work out how much equity you own.

Now, you won’t be able to take on additional borrowing that covers all of your equity. Instead, you’ll need to keep some equity in your property.

Why? Well, firstly, it’s the sensible thing to do so you don’t fall into that dreaded negative equity we told you about earlier. And secondly, most mortgage lenders will only let you borrow a maximum of 95% of your property’s value (known as a 95% LTV). That means you’ll need to keep at least 5% equity.

For example, let’s say your property is worth £200,000. You’ll need to keep at least £10,000 of equity in your property (5% of 200,000 = 10,000). Any equity you have on top of that, you could, theoretically, release.

Just be aware that your lender will do a whole load of other checks to work out how much extra they’re willing to let you borrow, like checks on your age, income, expenses and credit score. Plus, the more equity you keep in your property, the better the deal you’ll normally be able to get. So, it’s normally best not to release more equity than you really need!

Ready and raring to get some additional borrowing on your mortgage to clear your debts? Then you’ll probably want to know how to get started!

First of all, we’d recommend getting in touch with a whole-of-market mortgage broker. You don’t have to (you can just go straight to individual mortgage lenders). But a broker will take the time to learn about your individual circumstances before helping you to understand whether you’re best off remortgaging with a new mortgage lender, getting a further advance with your existing lender or even getting one of those second charge mortgages we told you about.

By comparing all the different lenders and mortgages out there to help you find the best deal, they’ll normally end up saving you a ton of time and money. Oh, and they’ll even sort out your whole mortgage application for you too. Our free find a mortgage advisor service can help you to find a mortgage broker that’s right for you.

If you have a good credit score and you’ve built up a decent amount of equity in your property, fingers crossed, it will be fairly easy to get approved for that extra borrowing and it’s only a matter of time before you’ll have that cash in your pocket ready to clear those debts. However, if your debts are spiralling out of control and you’ve missed some payments, then chances are your credit score won’t be in great shape.

It’s kind of a vicious circle because the more your debts spiral, the worse your credit score is likely to be. And the worse your credit score is, the harder it will be to find a lender who’s happy to let you borrow more money to pay off those debts. Urgh!

This is all because if you’ve missed payments before, your lender is likely to be worried that you’ll miss them again. And, at the end of the day, all they really care about is getting their money back.

Anyway, if you have a bad credit score and you feel like you’re stuck in that vicious cycle, don’t panic. It’s totally possible to get a mortgage with bad credit and there are even some lenders who specialise in lending to people who’ve found themselves in your position. A mortgage broker will be familiar with the ins and outs of different mortgage lenders and will be well-placed to help you find a lender who can work with your circumstances.

Itching to get those debts paid off? Think that getting additional borrowing on your mortgage is the way to do it? In which case, now’s the time to find a mortgage advisor.

They’ll be able to guide you through the whole process to make your life a whole lot easier (and, hopefully, cheaper!). Fingers crossed, you’ll be able to get those debts under control and start rebuilding your credit score before you know it. Good luck!

To recap, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will find you the best deal. You'll also get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.