Article contents

The pension lifetime allowance was previously £1,037,000, however this has now been scrapped (April 2023), and there is no lifetime allowance.

Squirreling money away into a pension pot? Give yourself a pat on the back! Pensions are a sensible way to make sure you have enough money to live comfortably when you retire.

But is there such a thing as saving too much?! Well, you can technically save as much as you want into your pensions – there’s no maximum pension contribution. But if you save more than the lifetime allowance, you’ll have to pay a hefty extra tax charge. Here’s the lowdown.

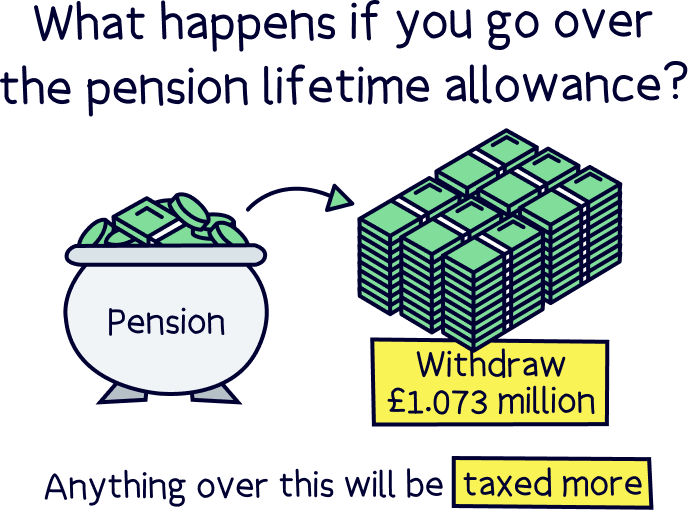

The pension lifetime allowance for 2022-23 is £1,073,000 million (that might sound like a lot but it’s easier to reach than you might think – more on that later!). Although the lifetime allowance can change from time to time, it’s currently set to stay the same until at least 2026.

But what exactly is it?

Well, the pension lifetime allowance is how big you can let your pensions grow over the course of your life, without having to pay a hefty tax charge.

Let’s rewind for a second.

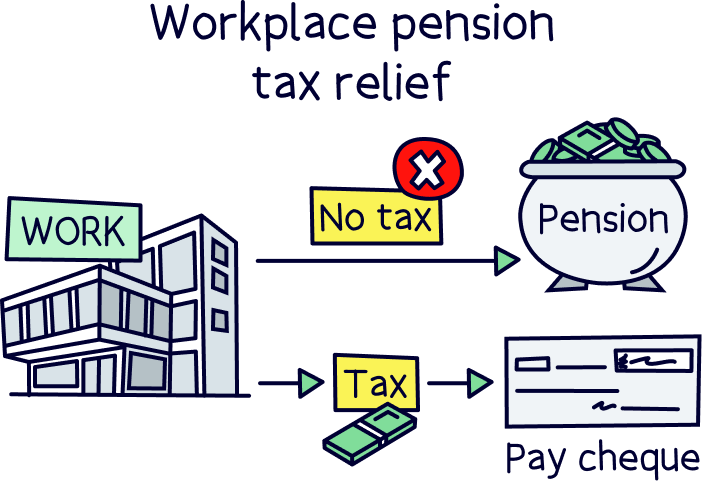

The government wants to encourage you to save up for retirement so they’re not left propping you up in your old age. To help, they give you this wonderful thing called tax relief whenever you pay into your pension pots. Tax relief means that you won’t have to pay tax on any income (like your salary) that you pay into your pension.

If you have a workplace pension (one that your employer sets up for you), your tax will be worked out and deducted before you get your payslip. So, you’ll simply end up paying the taxman (or woman) less.

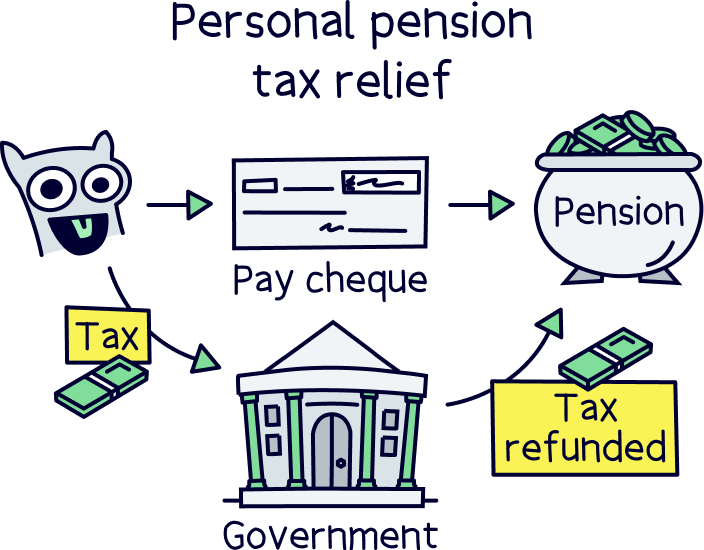

On the other hand, if you have a personal pension (one you set up yourself), you’ll get charged the same amount of tax you usually do. Your pension provider (the company that looks after your pension for you) will then let the government know how much you’ve paid into your pension pot, and any tax you’re owed back will be refunded straight into your pension. That means each time you pay into your pension, you’ll get a tasty bonus from the government (we’ll show you how that works in a bit).

Now, as much as the government wants to help you save for retirement, they also don’t want you taking the mickey. So, if the total amount you end up saving into your pensions goes over the lifetime allowance, they’ll want to claw back some of those tax benefits! Which brings us onto…

Find the best personal pension for you – you could be £1,000s better off.

If you go over the pension lifetime allowance, you’ll likely get taxed pretty heavily. Doh! This is the government’s way of limiting the tax benefits you can get.

Normally, you won’t get taxed until you actually come to take money out of your pensions. Technically, that means the lifetime allowance is a limit on how much you can withdraw from your pensions, rather than how much you can pay into them. But we still think it helps to think about it in terms of how big you can let your pensions grow (let’s face it, you’ll want to be able to withdraw all the money you’ve carefully stashed away!).

Anyway, you’ll pay taxes on your pension like normal on anything you withdraw up to the £1.073 million limit. This means you’ll be able to take the first 25% of this portion as a tax-free lump sum and then the rest will be taxed like any other form of income (in the UK, you have to pay income tax if you’re earning more than £12,570 per year, and that includes your pensions!).

But anything you withdraw beyond the allowance (known as the excess) will be taxed more heavily. Exactly how this works will depend on how you withdraw your money.

Want to take the excess in one go, as a lump sum? In that case, you’ll probably be taxed 55% on it. Eek!

You won’t normally have to worry about paying this bill yourself. Instead, your pension provider will take the tax off automatically and pay it to HMRC for you.

Just make sure that, if you’ve gone over the lifetime allowance, you get some professional advice before taking money out of your pension. Unbiased¹ can help you find the right financial advisor for you, to support you in making the best decisions when it comes to your pensions.

However, you’ll need to report the tax deductions by filling out a Self Assessment tax return (it’s easy to do, and all online).

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

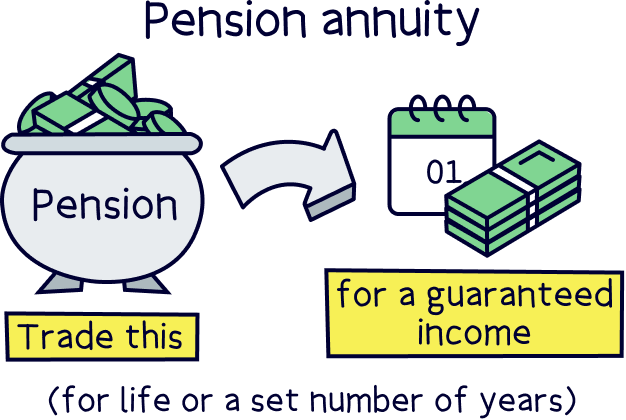

Alternatively, you can use your pension funds to pay yourself a regular income throughout retirement. You can either take a flexible income straight from your pension pot (known as pension drawdown) or you can use your pension funds to buy a guaranteed income (known as an annuity).

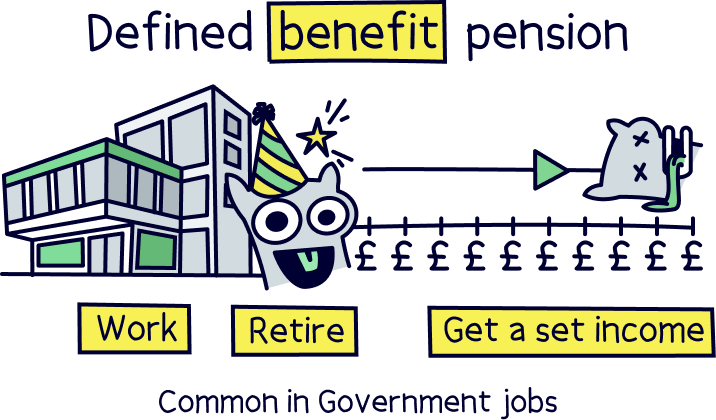

If you have an older-style pension, there’s also a small chance you have what’s known as a defined benefit pension – this is where your employer (or ex-employer) offers you a guaranteed income throughout retirement based on how long you worked for them, rather than contributing to a pot of money like how most pensions work.

Anyway, in any of these cases, you’ll face an immediate 25% tax charge on the excess (remember, that’s any savings over the £1.073 million limit).

You might be thinking ‘wow, that’s cheaper than if you take it as a lump sum!’ but sadly, you’ll also have to pay income tax on it. Depending on how much money you’re taking from your pension each year and if you have any other forms of income, you could end up getting taxed another 20% to 45%. So, it could add up to a lot!

Again, if you’re facing hefty tax charges like these, it’s best to seek advice before going ahead – Unbiased¹ is a great resource for finding a trusted financial advisor who can help you make the right financial decision for you.

You might well have been reading all this thinking: ‘£1.073 million sounds like a LOT of money. Surely I won’t have to worry about the pension lifetime allowance!’

Well, we have some news (both good and bad). It’s a lot easier to hit the lifetime allowance than you might think!

This is because the goal with pensions is to end up with more money than what you actually paid in. That’s right, your pension will normally get bigger without you having to lift a finger! This is thanks to a few different things:

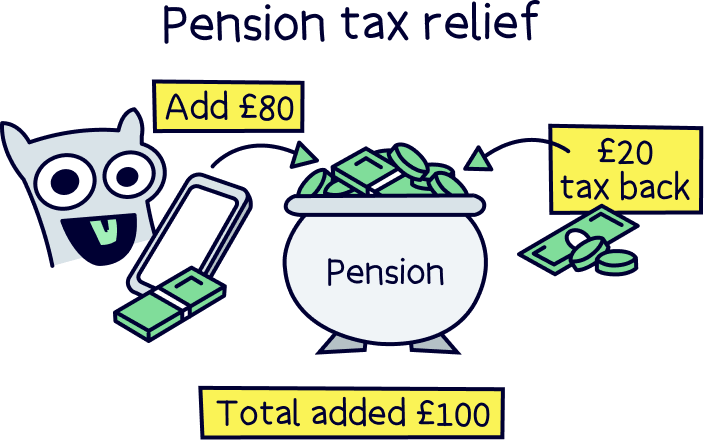

We’ve touched on tax relief already – remember how we said that you don’t have to pay any tax on the income (like your salary) that you pay into your pension?

Well, if you have a personal pension, tax relief means that each time you pay into it, the government will boost your savings by adding a bonus.

Exactly how big this bonus is will depend on how much you earn. Basic rate taxpayers (people who earn less than £50,270 per year and therefore pay 20% tax) will get 20% tax relief. That means if you pay £80 into your pension, the government will add £20 to turn it into £100 (£20 is 20% of £100). Kerching!

However, if you’re a higher earner and you pay more tax, things are even better. Higher rate taxpayers can get 40% tax relief on any income they’ve paid 40% tax on. And additional rate taxpayers can even get some tax relief at 45%. Get in!

All this means that you could end up with a lot more money in your pension pot than what you’ve actually paid in yourself. Thank you HMRC!

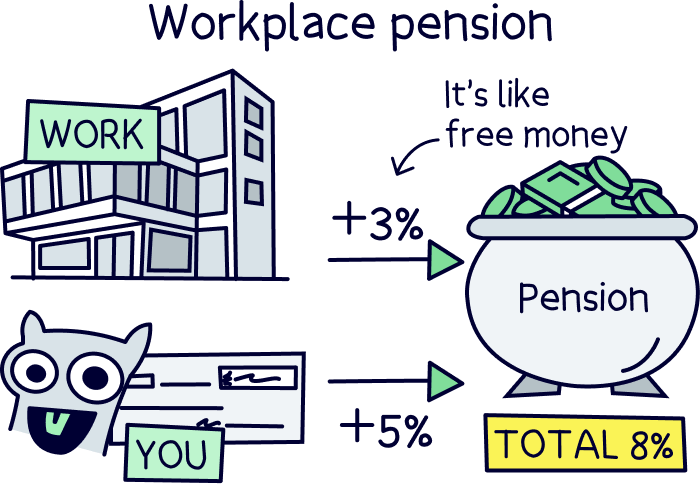

If you’re an employee, the chances are you have a workplace pension. Normally, your employer will be legally obliged to set one up for you. And, better still, they’ll be legally obliged to contribute to it alongside you!

Most of the time, you’ll need to contribute at least 5% of your earnings to your pension each month. But the really good news is that your employer will need to contribute at least 3% on top of that, straight from their own pocket. Nice!

Again, this means you’ll end up with more money in your pension pot than what you actually pay in yourself – meaning your savings can add up quicker than you might think!

If you have a pension, you’ll also have a pension provider – that’s a company whose job it is to look after your savings for you. But they’re not just there to keep your pension safe (although that is an important part of the job!). They’re also there to help grow your money.

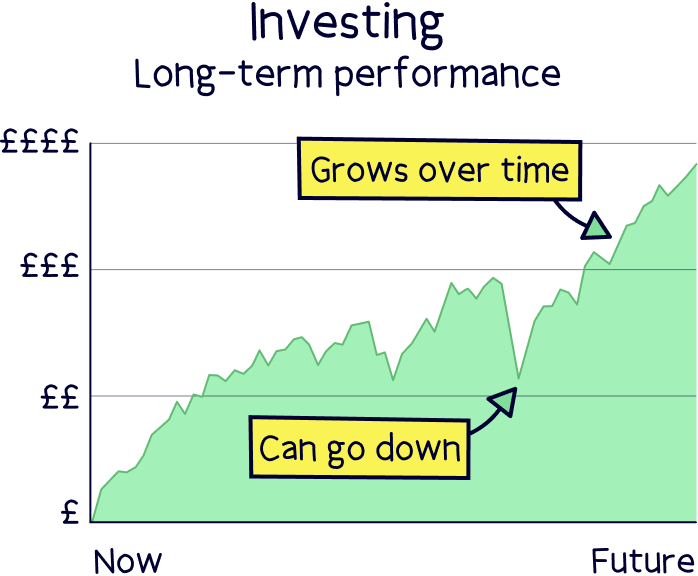

Normally, they’ll grow your money by doing something called investing it. That’s when they use your savings to buy things like stocks and shares (those are ownership stakes in companies). The idea is that as your investments increase in value, your savings do too! In investing, this is known as making a ‘return.’

We know what you might be thinking: ‘Ahh investing sounds like a scary thing!’ We promise, it’s not as scary as you might think and it can actually be a really sensible thing to do – especially when you let experts like pension providers take care of it for you.

Yes, it’s true that investments can go down in value as well as up in the short term. But pensions are about saving for the long term. And your investments are almost guaranteed to go up in value over time if you give them long enough.

Ultimately, all the rich people use investing to turn their money into more money. So why shouldn’t you? Pensions are a great way to get in on the action.

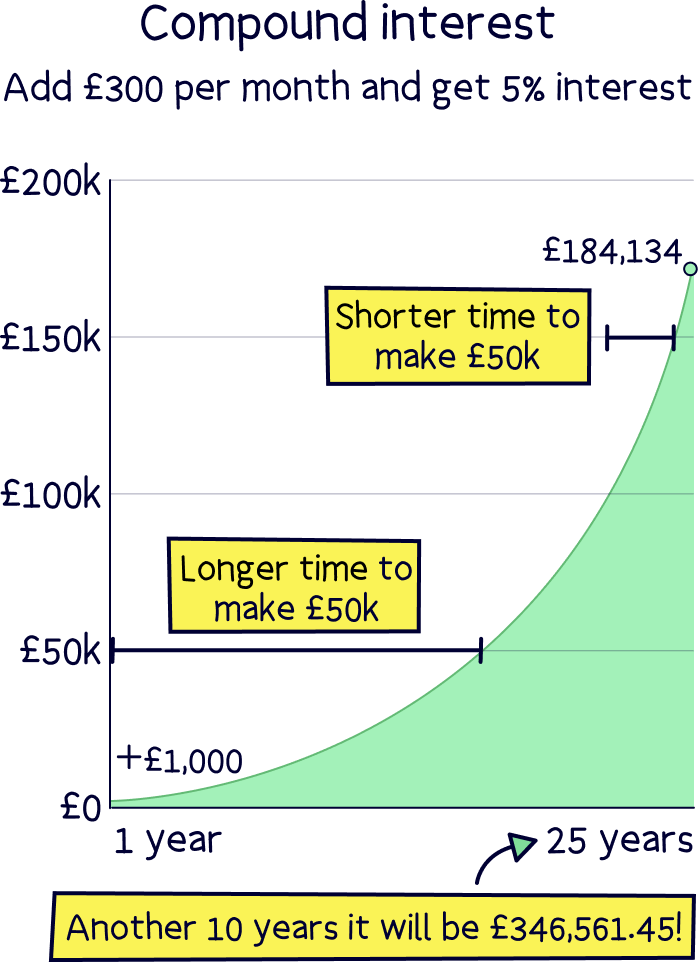

Finally, you know the phrase every little helps? Well, it’s incredibly true when it comes to pensions, all thanks to something called compound interest (or you might also see it referred to as compounding interest).

Compound interest refers to the fact that the returns your pension makes will also grow and make returns (don’t forget, a return is a fancy word for profit!). It’s like a snowball effect where the more your money grows, the quicker it will grow in future.

Let’s look at an example.

Say you pay £1,000 into your pension pot in your first year, and you make a 5% return. This means you’ll have £1,050 by the end of the year.

Now let’s say you make a 5% return again in the second year (without adding any more money). By the end of year two, you’ll then have £1,102.50 (because 5% of £1,050 is £1,102.50).

On average and over time, your savings will continue to grow in this way every year. So, after a while, you should end up with much more than what you started with. In fact, if your money keeps growing like this for 25 years and you also add £300 per month, you’ll end up with £184,134.20. Give it another 10 years and you’ll have almost double – £346,561.45!

This means if you pay a decent amount into your pension each year and you make decent returns, you could feasibly go over your lifetime allowance without meaning to. Yes, hitting the lifetime allowance is annoying in some ways, but it’s also a nice problem to have!

There’s 2 types of pensions in the UK:

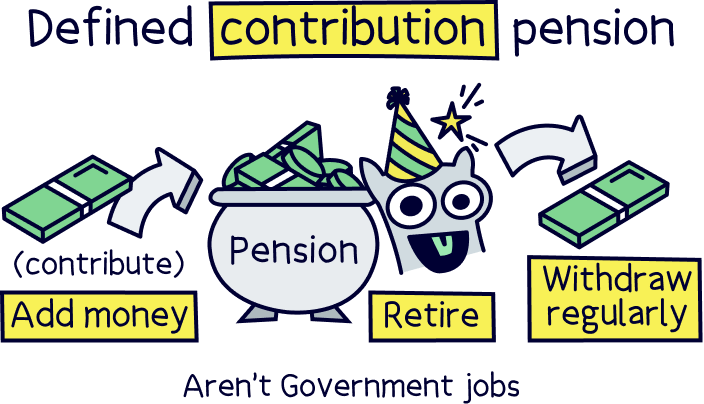

We’ve been talking about defined contribution pension pots in this article as that’s what most people have. And all of your money within your pension pot counts towards your lifetime allowance.

However with defined benefit pension pots, there is also the same lifetime allowance, but as you don’t know how much is in your pension pot, you won’t be able to work out how close you are.

So, to work this out, it’s usually 20 times what you would get from your pension within the first year you take it. Plus any lump sum. However, it’s best to check with your pension provider about this if you are concerned.

It might seem like you could never save enough money to hit the pension lifetime allowance, but your pension could grow quicker than you think – especially if you start saving early and pay into it regularly. If you do end up hitting your lifetime allowance, there’s both good and bad news.

The good news is that you’ve done an amazing job of saving up for retirement (hooray!). Your pension savings are over £1,073,100!

The bad news is that you’ll be hit with an extra tax charge when you come to take your pension savings (not that you’ll be able to withdraw your pension before 55 anyway). Which will be 55% if you take it as a lump sum, or 25% if you take it as a pension income (on top of Income Tax).

If you have exceeded the lifetime allowance and are set to be hit with a hefty tax bill, it’s important to get professional advice first – you can use Unbiased¹ to find a trusted financial advisor to help you make the best financial decisions for you.

Don’t yet have a personal pension? Whether you already have a workplace pension or not, starting a personal pension is really easy and can be a great way of boosting your savings for retirement – particularly if you choose a pension provider with cheap fees and a great track record for growing your savings. We’ve created a list of the best personal pensions to make it even easier for you.

Remember, whether you hit the pension lifetime allowance or not, the most important thing is to save, save, save – that way, you can ensure you have enough financial stability to enjoy your golden years to the full. Cruise around the Caribbean, anyone?!

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.