Review contents

St. James’s Place (SJP) is the largest financial advice business in the UK. It’s got great financial advisors up and down the country providing excellent customer service. They’ll determine the best investment strategy for you and manage everything too. They have a good record of growing your money over time, and the fees are reasonable. 4 stars from us.

Keen to invest and grow your money, but have no idea where to start? That’s where St. James’s Place and financial advisors come in – and the good ones are worth their weight in gold.

As an overview, St. James’s Place is the largest wealth manager (financial advisor) in the UK by far, and the most popular, with nearly 1,000,000 customers.

We’ll cover them in detail just below. First, let’s cover the basics of financial advice so we’re all on the same page.

Just here to learn about the SJP fee changes happening in 2025? Scroll down, we’ve run through all the changes and how they might benefit you (jump ahead to the fee changes).

Nuts About Money tip: if you're looking for a place to invest easily (in either an ISA or a pension) check out Beach¹, it's easy to use, a great app, with investments managed by experts.

Financial advisors will work with you to determine the best investment strategy for you – it’s all completely personalised. They do this by getting to know you, your family and your financial circumstances. Most importantly, they will listen and understand what it is you want to achieve in the future and your goals.

Your financial goals are often things like a safe and secure retirement with a decent income, for both you and your partner (if you have one). And, things like how your money might be passed down to your family in the most tax-efficient way.

You might want to grow your money as fast as possible while you’re young, and retire early (who wouldn’t?). Or maybe you want a nice consistent income while you’re still working. The possibilities are quite endless. And that’s what a financial advisor is for – to understand you and your goals, and then build a financial strategy to achieve them.

These days, financial advice can be hugely beneficial to everyone, even those who are just starting out with savings – financial advisors can put you on the right path to grow your savings over time (e.g. the right investment accounts and investments themselves).

Plus, some financial advisors can help with things such as life insurance and mortgages.

What’s key here is that you’re prepared to build up your savings, perhaps saving a bit each month (if you’re not starting out with a lot), with the view to building up your savings over many years, potentially long into retirement – a financial advisor can take care of everything.

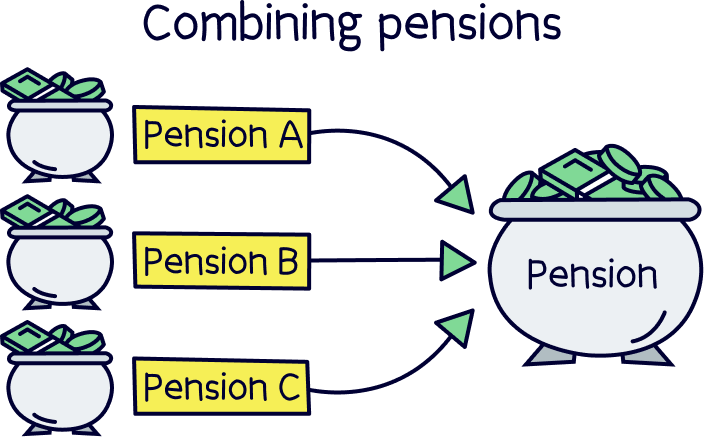

If you’ve got any old pensions from old jobs, you can transfer these over to a financial advisor too, so they can make sure your pension is continuing to grow in the best way possible.

By the way, if you’re not sure financial advisors are for you just yet, you could also consider an app where the investments are managed by experts, such as the easy to use Beach¹.

And, if you’re only looking to save within a pension, check out PensionBee¹, it’s 5* rated, and super easy to use. Here’s our PensionBee review to learn more.

If you want to consider more options for financial advisors, check out Unbiased¹, who can match you with great advisors local to you.

Nuts About Money tip: get an indication of how much you might need in retirement, and how much to save, with our quick and easy pension calculator.

St. James’s Place is the largest financial advice firm in the UK. They have nearly 5,000 fully qualified advisors and they help nearly 1,000,000 people. That’s a lot.

St. James’s Place looks after a staggering £168 billion – that's all their customers' money added together. This puts it as one of the top 100 companies in the UK (together these companies are called the FTSE 100), and it’s been there for over 8 years – and well established overall (33 years old).

The good thing about (very) large firms like this is the advice and customer service is a pretty consistent standard, and with St. James’s Place, the standard is very high. You can trust you’ll be looked after by a true professional. There’s a reason why they’re so popular.

Alongside your advisor, you’ll also be able to track your investments whenever you like too. You can do this on their website, and on their mobile app (both on Apple and Android devices). We’ll cover the app in detail below.

Let’s dive into the details to see if St. James’s Place is the right place for you and your hard earned money.

St. James’s Place is very trustworthy, it’s the UK’s largest financial advice firm, and looks after a staggering amount of money, from a huge number of clients up and down the UK and overseas, and has been doing so for a long time.

Your money is perfectly safe when investing with St. James’s Place (although the investments can go down in value as well as up). They follow all the rules and regulations set out by the Financial Conduct Authority (FCA) to ensure your money is safe (more than later), and you are protected by their compensation scheme too.

Combining that with the high level of service it provides, based on reviews from customers on both, Trustpilot (4.5 out of 5), and VouchedFor (4.9 out of 5), it comes out as one of, if not the most reputable wealth manager in the UK.

You may hear stories about St. James’s Place high fees, which we’ll cover in detail below (these are changing in 2025), but what the stories are typically comparing is investing by yourself vs with a large financial advice firm – but in reality, St. James’s Place comes in as one of the lowest cost large financial advisors overall (results below too).

Check out Beach, an easy to use app to invest sensibly with investments managed by experts. There’s a tax-free ISA and a pension pot (combine old pensions too).

On the surface, it’s simple: you speak to a financial advisor, and they’ll determine the best place to put your money to help you achieve your financial goals. Your advisor will be in regular contact while they’re working on growing your money over the long-term.

There’s many benefits to financial advice – it can ‘pay dividends’ over the long term with the right advisor, rather than investing yourself, and especially when compared to not investing at all.

The key benefits are that a financial advisor has the knowledge, skills and experience in investing that most people simply do not have – it’s a very complicated topic. That means your money can grow more quickly, but it also means you don’t have to spend the time or energy learning or managing your own money, for potentially less return (how much your money grows) – so you can spend more time living life.

Let’s run through the main areas of what St. James’s Place offers…

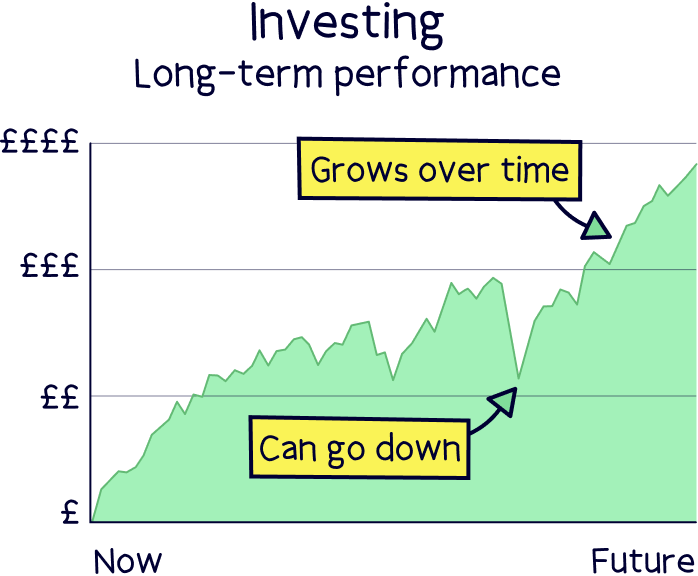

Using a financial advisor is for achieving your financial goals in the future. It’s long-term investing, using tried and tested investment strategies to grow your money over time – and they are very good at it. You just put your feet up, relax and watch your money grow over time (there will be ups-and-downs along the way).

In the UK, there’s quite a range of investment accounts on offer (all with different advantages, like being tax-free). Your advisor will create the right mix of accounts and determine how much to invest into each of them to fully benefit from all the tax benefits, for both you and your family (now and in the future). These are things like an ISA (Individual Savings Account) and a pension.

Although most people like to think of themselves as smart and could never be fooled, investment scams do happen, and to very smart people – even experienced investors can get fooled.

Millions of pounds are lost every year to scams – often because the investment looks exactly the same as a genuine investment. However, with St. James’s Place, they manage their own investments, so your money is perfectly safe (more on that below).

Investing is complicated, hard, and quite frankly, scary! There’s a lot to learn, and a lot of ‘jargon’ out there too. Many of us in the UK aren’t taught about finances or money in general, and our confidence to invest is pretty low – even though it’s seen as one of the best way to grow your money over time.

When you use an advisor like St. James’s Place, you can feel confident that your money is in safe hands. Each advisor is fully qualified and has many years of experience.

Your investment portfolio is what type of investments you actually have, and this is where advisors really earn their money. An advisor will look at your long-term goals (such as having a nice big retirement income), and work out the optimal investment portfolio to achieve them.

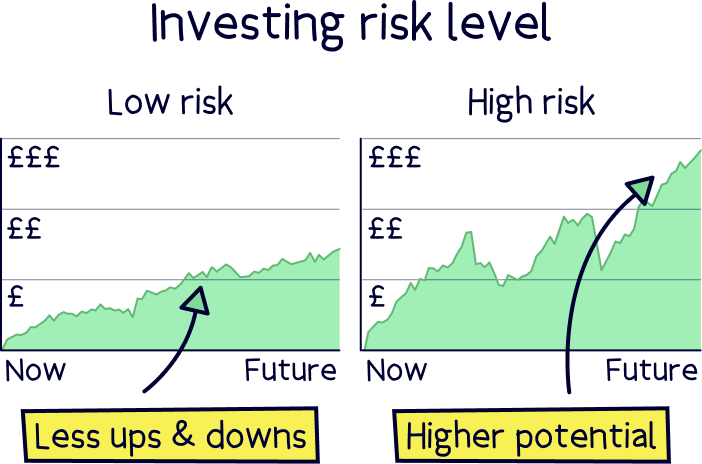

This is often determined by levels of risk within the portfolio and the range of investment (don’t let the word risk put you off).

With higher risk, you’ll likely have bigger ups and downs in the short-term, but the aim is more growth in the long term. With lower risk, the aim is slow and steady growth over time but you probably won’t make as much money over the long-term. Ultimately, it’s about finding the right balance between risk and return for you.

Let’s dive into the advice St. James’s Place offers, their advisors and their customer service.

First of all, let’s quickly define what an independent financial advisor is. They’re someone who helps with your long-term financial goals but often works for themselves (they are independent of any one investment company).

They have a duty to provide 'a comprehensive and fair analysis of the market'. Which means they have to look at pretty much every investment opportunity that exists (or at least a wide range) before they can make recommendations.

They don’t manage these investments themselves, they just provide advice, and then buy the investments on your behalf.

With St. James’s Place, the advisors all work for St. James’s Place. This means they do not have the same ‘duty’ to search every investment option out there, they are not independent (as they work for an investment firm), and this is called ‘restricted’ advice.

They will make recommendations from the range of investment options that St. James’s Place manages itself (more on this later).

This doesn’t impact any of the investment strategies they recommend (how they choose the investments to buy and what investment accounts to set up for you). Everything is the same, and you could even expect better service as it’s a larger firm. Ultimately, whether it’s an investment that St. James’s Place manages or not, it will be suited to achieving your long term goals.

All advisors are local to you, up and down the country, there’s nearly 5,000. And being a large firm, their standards for service are very high, in fact 80% of their own customers rated them as excellent or good (more on customer reviews later).

The way St. James’s Place works is that they’re your partner when it comes to investing. When your investments grow, so do their charges (more on that later), and so making you more money also makes them more money, plus they want you to stay with them for a long time!

This means you get the 5 star treatment that’s all tailored to you – if you like regular catch ups, you’ll have regular catch ups, if you don’t, you won’t. They’re available to chat and provide advice whenever you like – they’re there for you. As an added bonus, St. James’s Place has a budget for little treats, things like golf days (if you play) or other things suited to your interests.

Alongside financial advice for how best to invest, St. James’s Place will also provide advice on the best way to make the most out of your money, and more importantly, how to pay less tax. Legally, of course!

For instance, they’ll advise how best to structure your pension payments to make the most out of all of your tax-free allowances across the years.

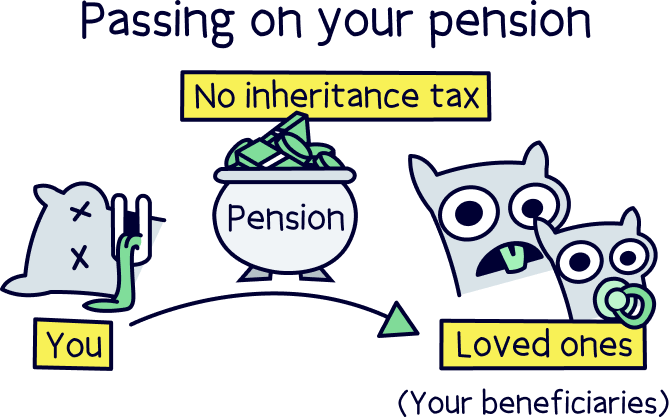

St. James’s Place will also recommend other tax-free accounts that can help your money grow quicker, and they'll also help your loved ones pay less Inheritance Tax when you pass away (sorry to put a downer on things).

That’s as well as things like how to save tax if you get a bonus from work, or shares and share options in a company (we won’t explain what these are right now). And, if you own your own business, how best to pay yourself. And of course, how best to take money out of your pension when you retire. This list goes on!

Tax is a complicated area in general, and there’s huge value in advice – potentially saving you and your family a significant amount of cash.

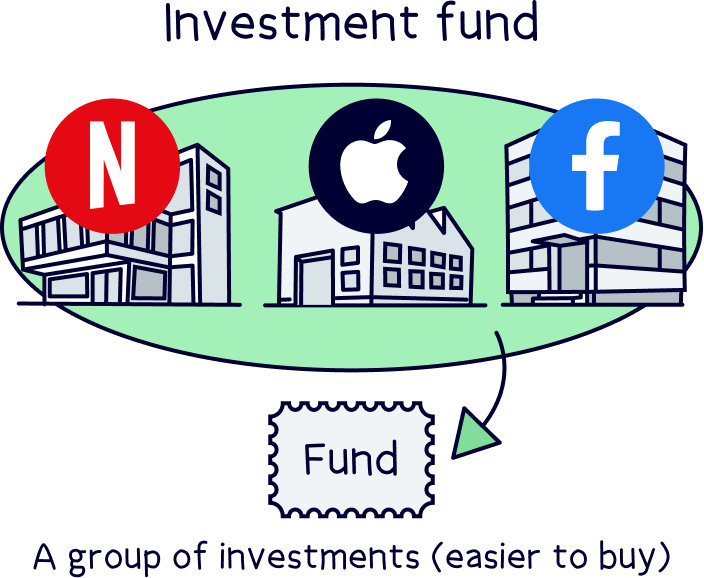

When investing for the long-term, you’ll most likely invest in investment funds, these are groups of investments all packaged together into one easy to buy and understand investment (funds are also much cheaper than buying all the investments in them individually).

Investment funds are super popular across the world, whichever financial advisor you use. If you have any investments at all, they’ll most likely be in investment funds.

The type of investments (assets) included in them are things like:

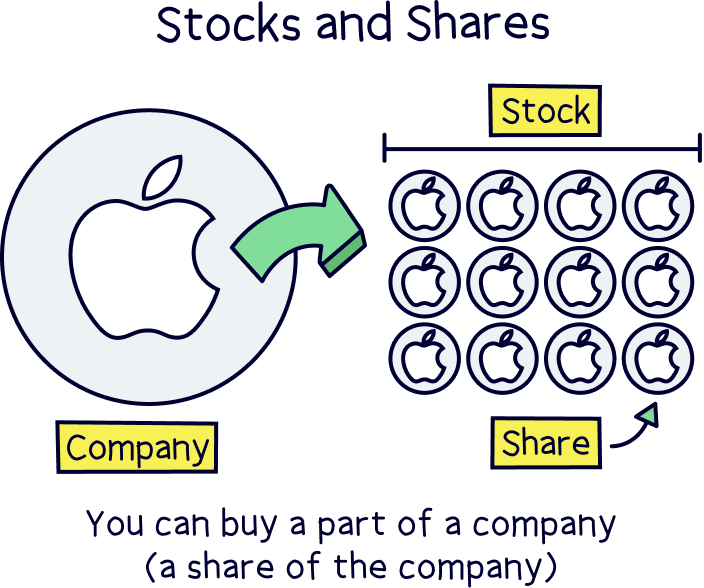

Stocks and shares (equities): where you buy a small part (a share) of a company, that can increase in value and can pay out its profits (called dividends) to the owners (the shareholders).

Bonds: where you effectively loan money to large businesses and governments in return for interest.

Property: often commercial property that pays regular income (rent).

Commodities: real things like gold and silver.

Note: these categories of investments are also called asset classes.

With St. James’s Place, they have a wide range of investment funds all tailored to achieve different investment goals. Your advisor will determine which is best for you.

The funds available with St. James’s Place are all managed by experts, and they’ll decide which investments go into the fund, for instance which stocks and shares or bonds to buy.

And, they’ll constantly review the performance of the investments and adjust them to make sure the investments are achieving the goals of the fund (which is often long-term growth).

The experts managing the funds are some of the best in the world. They are invited to manage an investment fund exclusively for St. James’s Place. This means they don’t technically work for St. James’s Place, they are external fund managers.

This has huge benefits for St. James’s Place, as it gives them the freedom to choose the best fund managers suitable for each fund, wherever in the world they might be. And, this means the funds can benefit from a wide range of different investment styles based on the fund manager's expertise.

The experts themselves are reviewed and monitored by The St. James’s Place Investment Committee – which is an independent group of more investment experts, who’s job is simply to make sure the experts handling customers' money are at the top of their game. It's another reason why your money is in safe hands!

And just to be clear, the experts managing the investment funds are completely different from your financial advisor, their only job is to manage the funds and grow their value over time. Your advisor's job is to decide which type of investment funds are right for you.

The investment funds are all designed to suit specific types of customers and their financial goals. These funds are grouped into core investment themes, which are selected for you based on your short and long-term objectives (to grow your money over time, and to ensure you don’t pay any more tax than you need to).

Just to recap, an investment fund is where lots of investors' money is pooled together, and investments are bought within the fund itself. This makes it super easy to invest in a wide range of assets, or a specific set of assets, by just investing in the fund itself (don't worry if this doesn't make complete sense, your advisor will handle everything).

The funds are also built around different levels of risk to suit different investors, and then held within one of the core investment themes (e.g. long-term growth). We’ll cover the investment performance of the funds later.

Let’s run through the types of investment options (don’t worry, your advisor will actually decide the best options for you):

This is a simple option for long-term financial planning, particularly when it comes to managing tax (not paying more than you have to). It provides the ability to invest in a wide range of investments, across different types of asset classes (e.g. stocks and shares, and property etc.).

You have the option for your investments to rise in value, or produce a regular income, or a mix of both.

How much tax you’ll save (if any) depends on your personal circumstances, and your total balance will fluctuate up and down over time depending on the investment performance. Which is the same for all investment options. (More on the performance below.)

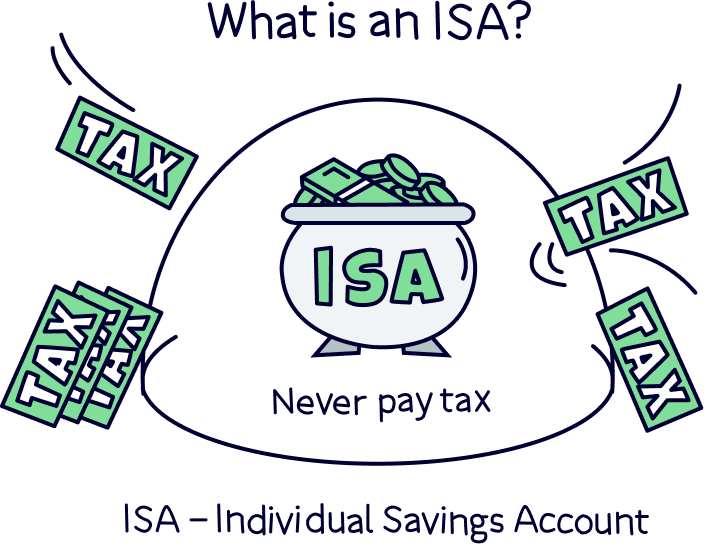

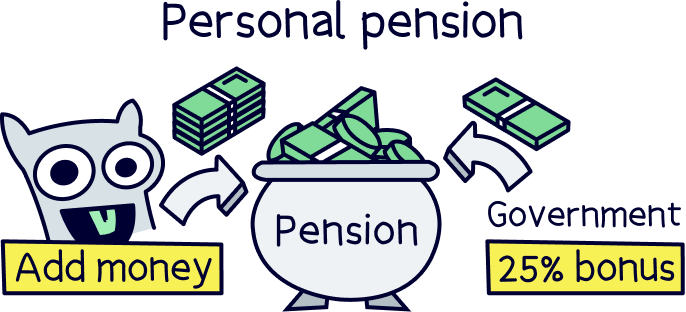

These are a great option to save for the future, where everything you make is completely tax-free. This will likely form the core of your investment portfolio, and you can invest in a wide range of investments. There’s a limit on how much you can save per tax year however (£20,000).

By the way, ISA stands for Individual Savings Account. It’s a government scheme to help you save and invest. These are also called Stocks & Shares ISAs.

This option is similar to an ISA, except there’s no tax benefits from the government (i.e. £20,000 tax free). Although there can still be many tax advantages.

You can invest as much as you like, and you still have a wide range of investments (also called Unit Trusts – effectively the same investment funds). You might use this account if you have used up your tax-free allowance on your ISA in a given year.

This is a dedicated investment account just for retirement, with a lot of benefits. You won’t pay any tax as the money grows, and the government even gives you a 25% bonus every time you add to it (yes, really!). You can hold a wide range of investments within a pension too.

However, you can’t access the money until you’re 55 (57 from 2028), although if it’s left until you retire it could grow much more. And you can even keep your money invested long after you retire.

Nuts About Money tip: if you’re only looking to save for retirement, and haven’t built up a large pension pot yet, check out PensionBee¹ – it’s 5 rated and easy to use.

If you’re planning to live outside of the UK, an expat, or for various tax reasons, you can also hold investments outside of the UK within an international investment account (bond). There’s a range of investments, including both growth (investments grow in value) and to provide a regular income.

Got a sense of how St. James’s Place works, and their investment options? Let’s see how good the investments actually are.

To do this, we’ll use medium-risk investment options, as they feature in most people’s portfolios – especially pensions.

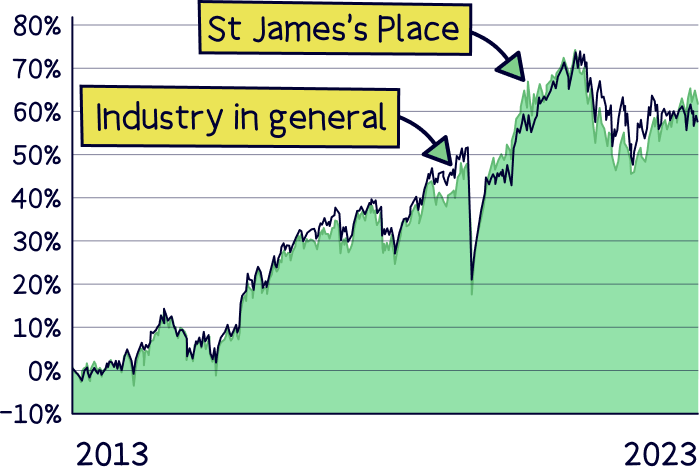

One of the core funds of St. James’s Place is their ‘balanced’ pension fund. And it’s big, with almost £8 billion of customer’s money within it.

It’s also actively managed, which means their experts are constantly reviewing the investments and making changes – so a good one to review their experts’ performance too.

Technically it’s called ‘SJP Balanced Managed Pn Acc’, and you can find the investment performance of all their funds on the St. James’s Place website.

So, let’s compare it with the industry in general – with the average of all similar funds (that aren’t managed by St. James’s Place). Here’s how it looks:

(Data accurate as of October 2023).

Charts can be a bit confusing, but what it shows is that this St. James’s Place fund has grown pretty well over the last 10 years, and in-line with the industry in general.

Currently, the industry average is a 55.1% return (increase) over the last 10 years, and this fund has grown by 61% – so ahead by 6.1% (after fees taken out too). Not bad. In fact, that’s pretty much exactly what you should expect.

Remember, St. James’s Place is all about long-term, safe and sensible growth over time, not growth at all costs and risking too much of your hard earned money. The value is in advisors helping you navigate the complicated world of investing and using the right strategies to grow your wealth.

That’s why looking at specific funds is useful, but in reality you’re going to have your money invested in a range of different funds, in a combination unique to you.

Some funds won’t perform well, and some funds will perform exceptionally well. But importantly, your portfolio will be suitably diversified so that a poor performing fund doesn’t impact your total growth that much – that’s one of the reasons investment advice is so important.

And as a very rough guide, from 2002 to 2022, the average St. James’s Place customer made 7.7% per year after all the fees. That’s pretty good! We would be very happy with that – it means your money would have doubled. Much better than having it sit in a bank account right?

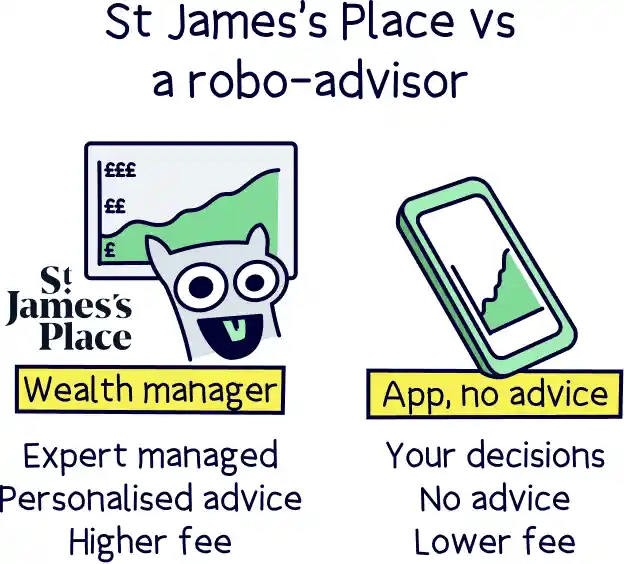

Considering using a robo-advisor such as Nutmeg? Or wondering what the difference is?

St. James’s Place are a financial advice firm, giving real financial advice for your specific financial circumstances and for your life and family. You can talk to them face-to-face and/or over the phone, they will tell you the best investment strategy for you, and then handle everything for you too. Plus, they’re there every step of the way as your wealth grows.

With a ‘robo-advisor’ (or simply called an investment app), they don’t get to know you and don’t partner with you for potentially life like an advisor does (although some offer one-off advice phone calls to advise on your investments). And there’s no advice services such as tax planning.

They are a platform (an app) for you to invest your money, with you making the decisions from a handful of investment options, and these options are often managed by the experts at the platform or a partner (such as J.P. Morgan with Nutmeg).

We think investment apps are great by the way, they’re simple and easy to use, and take the hard work out of investing yourself. They’re perfect if you’re just starting to invest, or are still building up your savings and pension. For instance PensionBee¹ is great for pensions, and highly recommended (5* rated too).

But, they’re not the same as a financial advisor, who can offer a much better service and wider range of options and advice.

If you want to find the best 'robo-advisor' check out our best investment platforms.

When it comes to investment performance, Nutmeg’s fully managed portfolio option, which is their experts managing the investments (so similar to St. James’s Place), on their medium-risk level, has returned 31.9% over the last 10 years.

That’s 29.1% lower than if you had invested in the similar medium-risk balanced fund with St. James’s Place that we reviewed above. That is a massive difference.

Even though Nutmeg fees are lower (1.01-1.15% per year), it doesn’t necessarily mean your money is going to grow more over time. It can be worth paying more for the right advice and better investment management. We’ll run through St. James’s Place fees below.

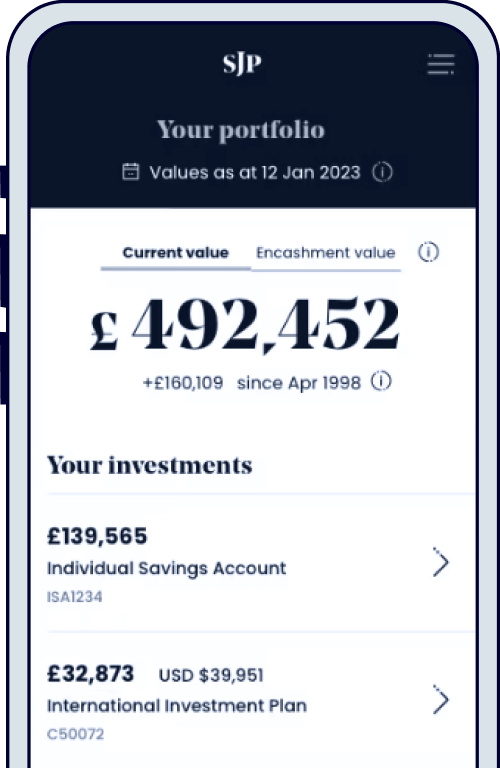

St. James’s Place has a pretty good mobile app for clients to track their investments.

It’s fairly basic for now, but essentially, you can see how much money you have in total, how much you have in each account (for instance an ISA and a pension), and then the investment record of your investments – which is pretty useful, you can periodically check in on your investments to make sure they’re growing as expected, without having to speak to your advisor (unless you want to).

There are plans to improve the app over time, and we’re told you’ll soon have details on your advisor (such as contact details), and information on the specific investments you have, which will have a breakdown of all the different investments within the fund(s) you have invested in.

Financial advice includes more than just investment advice. Advisors can help with almost everything to do with money, and that includes banking, mortgages and more (well, not every advisor can, they’ll need to be qualified to give advice on each area).

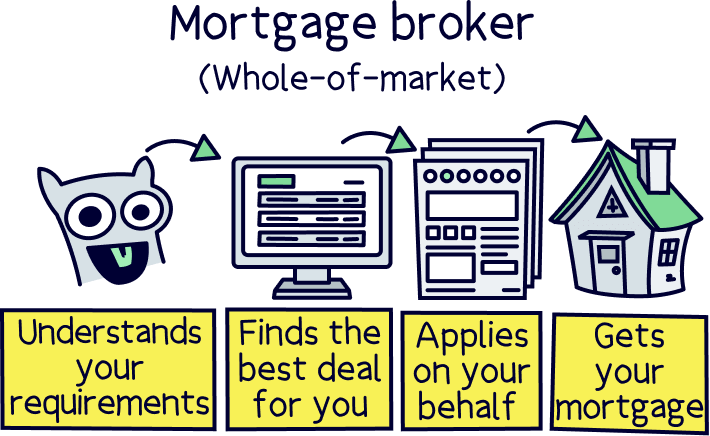

With St. James’s Place, you can search for advisors in your local area who can help with mortgages – and there’s a big range, over 4,500 advisors across the UK. They’ll be able to help if you’re buying your first home, or remortgaging your property (getting a new deal).

We always recommend using a financial advisor or a mortgage broker when searching for a mortgage – they can search every mortgage out there to find the right one for you. There’s over 20,000 mortgages from over 100 different mortgage lenders (e.g. banks), so it can be quite a task doing it yourself.

But more importantly, mortgage brokers (and financial advisors) can search lenders who only work with brokers, so can search even more than you could yourself – and they’ll know all the tricks that mortgage lenders do to look like their mortgage is the best option (for instance lowering the mortgage rate, but increasing the fees) – brokers can look at the total cost of the mortgage, rather than just the interest rate (we recommend doing that too if you are looking yourself).

Plus, the mortgage broker will handle all the paperwork too, and chase the mortgage lender for updates – saving you time better spent elsewhere.

Nuts About Money tip: if you’re looking for a mortgage now, and happy with getting mortgage advice online, check out the best online mortgage brokers to learn more and find out top recommendations.

Having some of your savings in cash plays a very important role in financial planning – and how much you’ll want depends entirely on your own personal circumstances.

These days, having cash doesn’t mean your money will be earning nothing, you’ll still be able to earn a reasonable amount of interest (although not as much as you could expect over the long-term when investing).

St. James’s Place provides a service called the SJP Cash Deposit Service, which is an online service where you can compare interest rates from over 40 banks and building societies in just a few minutes.

You can find some of the top interest rates out there, and save your money across multiple banks and building societies – while managing everything from a single place, without having to fill out lengthy application forms for each savings account.

This means when interest rates change, you can easily and quickly switch to a new higher rate with a different bank (if you want to).

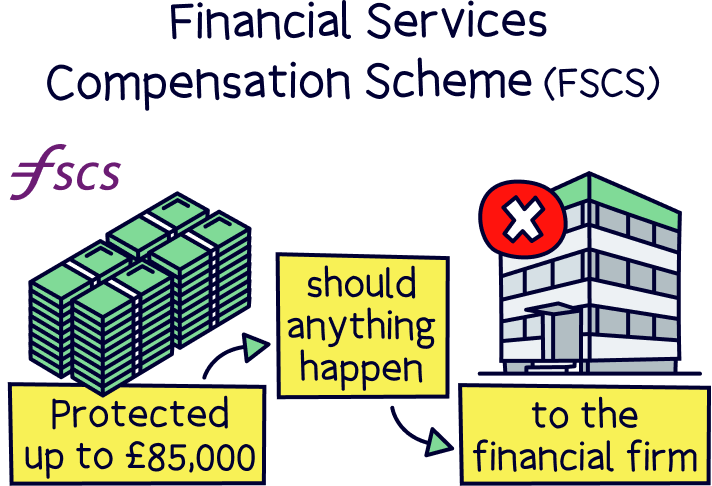

If you’re saving more than £85,000 in cash, you could split this across several banks offering top interest rates, so all of your cash is fully protected by the Financial Services Compensation Scheme (FSCS) – a government scheme which provides compensation up to £85,000 per bank (should the bank close down).

Note: to provide this service, they partner with a company called Flagstone.

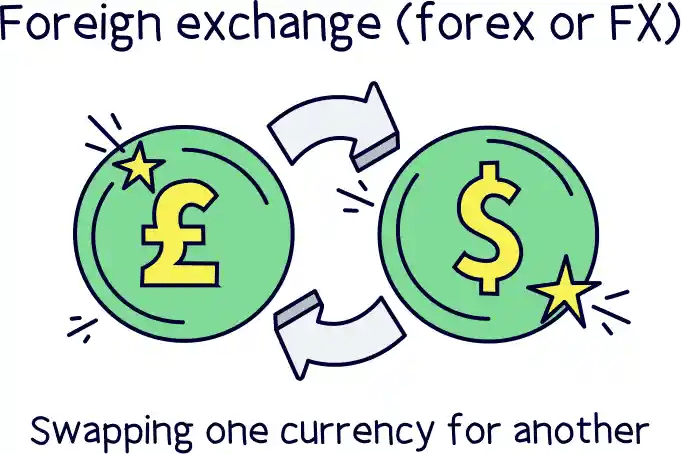

St. James’s Place also offers a service to convert one currency for another, called foreign exchange (e.g. Pounds into Dollars). Often, this is for a holiday, or perhaps you’re going to be working away.

To do this, they work with a range of different providers who offer foreign exchange services, including international payments (sending money abroad).

Nuts About Money tip: if you are spending money abroad often, check out the best travel money cards, you might be able to save a small fortune.

For those with a bit more than the average wealth (the high rollers), St. James’s Place can introduce you to private banks who offer bespoke services to High Net Worth individuals.

Intergenerational wealth management is financial planning not just for you and your money, but planning for your whole family and how to benefit their lives.

That could involve how to pass your money down to your children in the most tax-efficient way (often called estate planning), but it’s much more than that – it can involve how best to insure everyone in your family when it comes to private healthcare and life insurance.

Or, it could be how best to pass money onto your children to help them get a mortgage and onto the property ladder, or how best to pay for your elderly parents' care.

And when it comes to investing, you can save for your children’s future (if you have them), in their own name with a Junior ISA.

Overall, St. James’s Place is only slightly higher than the average fees across all independent advisors, and cheaper compared to other large financial advice firms (Quilter, Rathbones and RBC Brewin Dolphin, among others).

As a quick run through of the larger ones with transparent fees, here’s how it looks (from our research):

There’s been some big changes to the fees St. James’s Place charges recently, and they come into effect from mid 2025 for all new customers, and existing customers making new investments (e.g. adding more money to your account with St. James’s Place).

So, let’s dive into the changes first, then cover the current and previous fees below.

It essentially all revolves around what’s called an ‘early withdrawal charge’, which currently applies to pension and investment bond accounts (not ISAs) – it’s a fee that you would have to pay to withdraw money from your accounts within 6 years of paying it in.

This early withdrawal fee exists now because they actually waive the yearly fee for managing your investments within these accounts (called the product management charge) for the first 6 years.

So, if you moved your money before 6 years, to somewhere else, or withdrew it, it offsets the fees that you should have been paying (if they didn’t waive the fee). Make sense?

It was effectively intended to incentivise you to stay with St. James’s Place for the long term (which is kind of the whole point of investing with them, or any financial advisor).

Let’s be honest, it does get quite confusing, and it’s very hard to compare the fees with other financial advisors easily (as no one else has this fee structure).

So, from mid 2025, instead of this early withdrawal fee, you’ll pay the product management fee (that was previously waived) each year, but this fee is also reduced as well, so in theory, most customers should be paying lower fees than they currently are.

And, they’ve made a few more changes to make things easier to understand, these are broken down into 3 key areas:

Each area will have its own fees, and this will depend on what service, account or investments you and your advisor have determined is best for you – so effectively, the fees are more personalised to you.

Note: this is typically the same structure as most financial advisors, making it easier for you to compare fees (we’ll show you how St. James’s Place compares with other advisors just below).

With St. James’s Place, you’ll pay a fee for your dedicated advisor and their expertise, advice and recommendations – remember they handle everything for you.

For the initial discussion, follow on review and portfolio recommendations, you’ll pay 4.5% of your investment. And for ongoing account management with your advisor, it’s 0.5% per year.

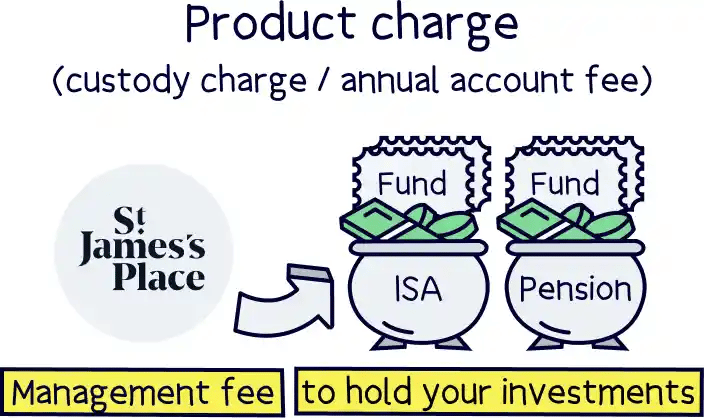

You’ll then pay a product management charge, which is a management fee to hold investments with St. James’s Place – or rather for them to securely hold your investments.

For instance, they could open an ISA or a pension for you and hold your investments within this account (plus all the admin to go with it). This is sometimes called a custody charge, or annual account fee.

With an ISA and Unit Trust accounts, there’s a set up fee of 0.5% of the money you add, and then an ongoing fee depending on where your money is invested (it varies depending on the investment fund), but is typically altogether, a cost of around 1.6 to 1.9% per year. We’ll cover the investment fees below.

There’s no fees to withdraw cash.

With a pension, from mid 2025, this will be very similar to an ISA account, where you’ll pay an annual ongoing fee per year (expected to be 0.65% per year).

Currently, the fee is 1% per year, but waived for the first 6 years, and then reduced to 0.85% per year after 10 years.

There’s also an initial charge of 1.5% of the money you add to your pension (called an initial product charge).

You’ll then also pay a fee depending on which investments you have within your pension.

You’ll pay a fee within the investment funds themselves. Whichever company you invest with (e.g. advisor), and whichever investment fund you invest in, you’ll pay a fee, and these are often called fund fees, admin fees or ongoing charges.

It’s automatically deducted from the money within the fund itself, so you don’t have to worry about manually paying it. There will also be transaction fees when the fund buys and sells investments, and these are automatically collected too (and not generally very much).

These fees vary depending on the investment and the fund itself, how it works and what its goals are – which determines how much resources it needs (people managing it).

There’s different funds for different accounts, for instance ISA funds or pension funds, and each of these have different fees too – pension funds are lower cost as you’re paying more for the pension account, and ISA funds are higher cost.

Overall, expect to pay somewhere between 0.11%-2% in investment fund fees, depending on the investment fund itself.

It’s all quite complicated right? Don’t worry, your financial advisor will run through all the fees to make sure you understand them before you part with any money.

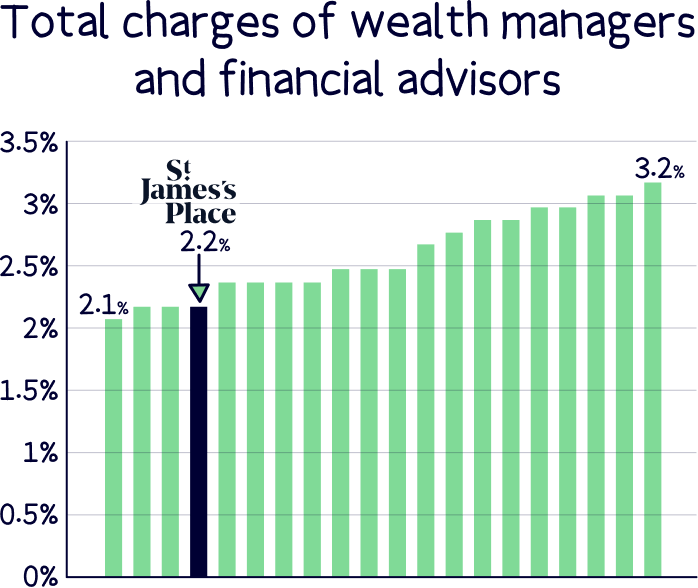

Grouping all those fees together, as an average, expect to pay around 2.2% per year (of your investments) – that’s everything included.

How does that compare with other large wealth managers and financial advisors? Let’s take a look…

(Comparison data provided by EY (Ernst & Young), Sept 2023).

Here we can see St. James’s Place is on the lower end, coming in at an average of 2.2% per year, with the lowest coming in at 2.1% and the highest coming in at 3.2% per year. So overall, fairly reasonable for the service they provide.

The research looked at 20 different companies, so we won’t list them all here as that’s quite a lot, but they include all of the largest companies in the industry, such as Evelyn Partners, Quilter, M&G Wealth Advice, RBC Brewin Dolphin, Rathbones and Charles Stanley.

The research looked at a period of 10 years, and used an example investment of £100,000, receiving advice, and investments into actively managed investment funds (so experts handling things), with all the same example investment growth (5%).

If we then compare them to the average financial advisor (using research from the Financial Conduct Authority) – the average initial advice fee is 2.4%, the average ongoing fee for advice is 0.8%, and the average investment fee from funds that advisors recommend is 1.1%. So, adding all those together over the same 10 year period, that would be 2.14% (so very similar to St. James’s Place at 2.2%).

However, that is an average, you may find some advisors cheaper, and you may find some more expensive.

For the highly rated customer service St. James’s Place offers, it’s looking like pretty good value.

The only big issue was the early withdrawal fee on the pension (and investment bond) – if you wanted to withdraw money before 6 years. So do take this into consideration (until 2025 when it's removed).

So, not only will you benefit from not having the potential to pay the fee (should you want to withdraw money later), it may also work out as lower cost over time too (although it will all depend on where and how your money is invested).

By the way, you should be told all of the fees clearly and up front when you have your initial meeting or any follow up meetings – it’s part of the legal requirements, which applies to all financial advisors. We know it’s all confusing, but hopefully this has helped a bit. If you aren’t sure, just ask your advisor.

Note: if you’re considering whether financial advice is right for you, an independent review (by Numis Securities research), found that it's worth 2% per extra year vs investing yourself (and that’s if you know about investing). Meaning that St. James’s Place made 2% more per year after fees (over the last 10 years). Here’s a summary from the independent review to learn more.

To get a good idea of the level of customer service and customer satisfaction in general, it’s a good idea to find out what their customers think.

We normally use Trustpilot, the popular reviews website, however financial advice has another much more popular review platform, ‘VouchedFor’.

On VouchedFor, St. James’s Place has got an awesome score of 4.9 out of 5! This is from over 30,000 reviews too. What’s great about VouchedFor is you can actually rate your advisor rather than the company itself, and they’re all getting consistently high scores. You can check it out for yourself on the VouchedFor website.

On Trustpilot, they’ve got a rating of 4.5 out of 5, from over 1,500 reviews. That’s great for financial advisors, and lots of the reviews mention the service from advisors (with lots of advisors being called out specifically).

And from a report from its own customers, it’s pretty great too. 80% of people rated St. James’s Place as ‘excellent’ or ‘good’, 15% ‘reasonable’ and 5% ‘poor’. And according to St. James’s Place themselves, just 5% of customers change to a different financial advisor, which is very low.

The customer support in general is great.

On top of your financial advisor, you also get access to a customer support team, which are available during the daytime, and you can request a call back at a time to suit you. Plus, you can even call when you're overseas.

Everything is phone-based, with fast response times (so no waiting on hold). Unfortunately, there’s no email or live-chat support, unless you email your advisor directly.

Yes, it’s perfectly safe to use St. James’s Place. It’s the largest financial advice firm in the UK. It’s so big, it’s actually one of the top 100 companies in the UK.

It’s authorised and regulated by the Financial Conduct Authority (FCA), and the Prudential Regulation Authority (Bank of England), and the Central Bank of Ireland. They’re responsible for making sure that every company that looks after your money and companies that give advice, are treating their customers fairly and properly – that means giving you the right advice for your circumstances and making sure your money is safe.

Your money is also protected by the Financial Services Compensation Scheme (FSCS), which means if something should happen to St. James’s Place, such as going out of business (extremely unlikely), you’ll get back up to £85,000 on any money they hold within your investment accounts, and 100% of your pension.

However, there’s even more protection, as your investments are actually held with a different firm, a very large reputable bank (State Street Bank). The investments are all in your name and can only be returned to you.

Plus, St. James’s Place actually has a lot more money than they actually need – kept as a reserve fund should anything happen. It’s arguably one of the safest places to invest your money in the UK.

St. James’s Place is the largest financial advice firm in the UK, looking after over £168 billion for nearly 1,00,000 investors, and has a very established reputation – it’s not in trouble, or really possible to face much trouble due to its size.

As St. James’s Place is a public company with its own shares that the general public can buy (it’s a FTSE 100 company), their share price can go up and down just like every other company, but that doesn’t affect how your money is looked after, the advice you receive, or affect the investments you hold with St. James’s place.

Their share price can be affected by things like the fees reducing (which is happening in 2025), which likely means less money made by St. James’s Place, and more in their customer’s back pocket. And, news such as a new CEO (the big boss) can affect this too (which happened in 2023).

St. James’s Place also has a charitable foundation: the ‘St. James’s Place Charitable Foundation’. It’s a registered charity and pretty big too – it’s the 3rd largest corporate foundation in the UK and has donated over £120 million to charity – good work guys!

It helps small and medium sized charities across the UK with funding to carry out their own charitable work. Hundreds of charities get cash each year, and these charities include hospices, cancer charities and mental health charities.

You can learn lots more on the St. James’s Place Charitable Foundation website.

Let’s have a quick recap and look at the pros and cons of St. James’s Place.

Investing your money is one of the best decisions you can make for your future, and here at Nuts About Money, we’re big advocates of getting the experts to handle your investments and pension, whether that’s a financial advisor, a ‘robo-advisor’, or anything in between.

It’s very unlikely that by looking after your investments yourself, you’ll be able to make more money than the experts will (even taking into account the fees) – they’ve spent most of their professional lives learning and doing exactly that – growing people's money sensibly over time.

Investing is a complicated area, and there’s a lot to it; the right investment accounts, the right portfolio, the right risk levels for every stage of your life, and your financial goals. And most importantly, using the right risk management techniques within the investments themselves. It takes a long time to master, and believe it or not, most people end up losing money when buying stocks and shares themselves.

Better still, investing and finance in general is often boring and very time consuming. Using experts means you can forget all about it. Let the experts worry about it. If you do it yourself, you need to be constantly monitoring and adjusting your portfolio to reflect your investment strategy.

With St. James’s Place, we think it’s one of the best options out there when it comes to financial advice. One of the key things most people look for is quality of advice and service, and they come out at the very top for both – there’s a reason they’re super popular with nearly 1,000,000 customers.

The investment performance is pretty much what you should expect, which is in-line with the industry and economy in general – steady growth over time (with ups and downs in line with the economy).

With long-term investing, that’s exactly what you want – you’re not looking for the highest return possible every year, that puts too much of your money at risk. That’s for high-risk investors, not people trying to grow their pension to have a better future.

So, peace of mind with your money and investments, great customer service, good investment returns over the long-term, all for a reasonable fee – around 2.2% per year (as an average over 10 years). Which is in line with the average independent financial advisor (2.14%), and actually cheaper than most other large wealth managers. It all sounds pretty great.

The only major downside is the pretty confusing current fee structure, with some fees clear and some fees not so clear. Plus, the ‘early withdrawal fees’ on the pension, which means you can’t move your pension in the first 6 years (unless you pay the fee) – however this is being removed in 2025 as part of a company wide fees shakeup.

In 2025, the fees overall are set to become much clearer, and split into three 3 categories, advice fees, account fees and investment fees, so you can easily compare with other financial advisors. This should also mean lower fees for most customers too.

Overall, we recommend checking out St. James’s Place if you’re looking for a financial advisor, and we’re giving it a solid 4 stars.

If you’re interested in learning more, check out the St. James’s Place website.

To compare more options for financial advisors, check out Unbiased¹, where you can find top rated advisors local to you.

Check out Beach, an easy to use app to invest sensibly with investments managed by experts. There’s a tax-free ISA and a pension pot (combine old pensions too).

Check out Beach, an easy to use app to invest sensibly with investments managed by experts. There’s a tax-free ISA and a pension pot (combine old pensions too).

Check out Beach, an easy to use app to invest sensibly with investments managed by experts. There’s a tax-free ISA and a pension pot (combine old pensions too).

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out Beach, an easy to use app to invest sensibly with investments managed by experts. There’s a tax-free ISA and a pension pot (combine old pensions too).