Article contents

Yes, you can apply for a single mortgage if you’re married in the UK. You’ll just have to find a mortgage lender who’s happy to let you do it! That said, it’s not your only option so be sure to explore what else is out there.

Are you married? Are you hoping to get a mortgage in just your name?

There are lots of reasons why a married couple might want to get a mortgage in just one person’s name. Maybe your spouse has a bad credit score (a score that shows how good you’ve been with money in the past). Or maybe they’re unemployed. Here’s all you need to know about submitting a single mortgage application when married in the UK.

Yes! As a married person, you can still apply for a single mortgage in the UK. Hooray! However, it will be a little bit harder to find a mortgage lender who’ll be happy to lend to you (mortgage lenders are the people who give out mortgages).

Basically, most lenders prefer married couples to apply for a mortgage together, known as a joint mortgage. This is because if you’re both going to be living in the property together, getting a mortgage in just one person’s name could lead to disagreements about who has the right to live there later down the line.

Not only that, but if your spouse is giving you some money towards the deposit, that could make things a little bit complicated if your relationship changes in the future. So, a lot of lenders won’t like it.

Don’t get us wrong, there are lenders out there who’ll be happy to give you a single mortgage if you’re married. There are just fewer of them out there!

Tembo will find your best deal, fast, all with award-winning service.

With a single mortgage application, you’ll be applying for a mortgage on your own and buying a property in your name only. In other words, the property will be solely yours and you’ll be the one responsible for keeping up with the mortgage repayments, not your spouse.

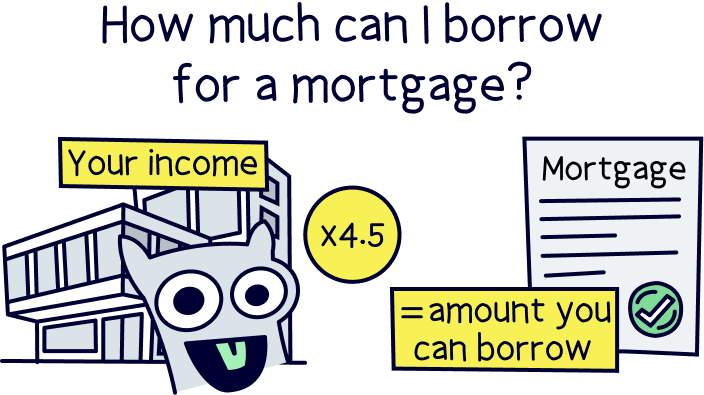

This means that lenders won’t look at your spouse’s details when they’re working out whether or not to approve you for the mortgage. Yes, that can have its benefits (for instance if your partner has a bad credit score – more on that below). But it also has its downsides. For instance, you’ll probably be able to borrow less than you could if you were getting a mortgage together.

Let’s imagine for a moment that you earn £25,000 a year. Most lenders will let you borrow around 4.5x your yearly income, so by yourself, you’d probably be able to get a mortgage for around £112,500.

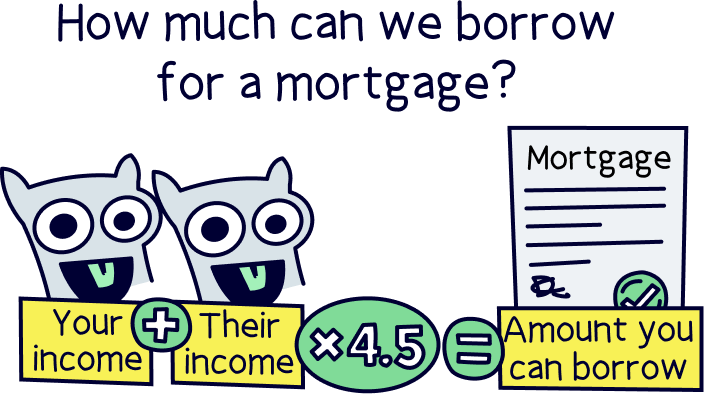

Now let’s imagine your partner also earns £25,000 a year. That means that between you, you earn £50,000 and you’d probably be able to borrow around £225,000. That’s a big difference!

If you’re submitting a single mortgage application, lenders will also want to be sure that you’re going to be able to afford your monthly mortgage repayments by yourself. So, you’ll have to convince them that you’re earning enough to do so. On the other hand, if you apply for a joint mortgage, you’ll only need to prove you can afford the repayments between you. And let’s be honest, with two of you, it’ll probably be easier!

Well, that depends on why you’re thinking of getting a single mortgage. It might very well be the perfect solution for you. But, depending on your reasons, there might be other options that would suit you better. Here’s the full lowdown.

Does your spouse have a bad credit score? If so, this could make it hard for them to get approved for a mortgage. Basically, lenders will worry that your spouse won’t keep up with the monthly mortgage repayments.

If you have a good credit score, you might have a better chance of getting approved for a mortgage if you apply in just your name. That’s because this way, your spouse’s credit score usually won’t be taken into account. Happy days!

However, this isn’t always the case. Some lenders won’t let you apply for a single mortgage at all if the reason is your partner’s credit score. And other lenders will still take your spouse’s credit score into account, which kind of defeats the whole object. Ultimately, it’s just about finding the right lender for you.

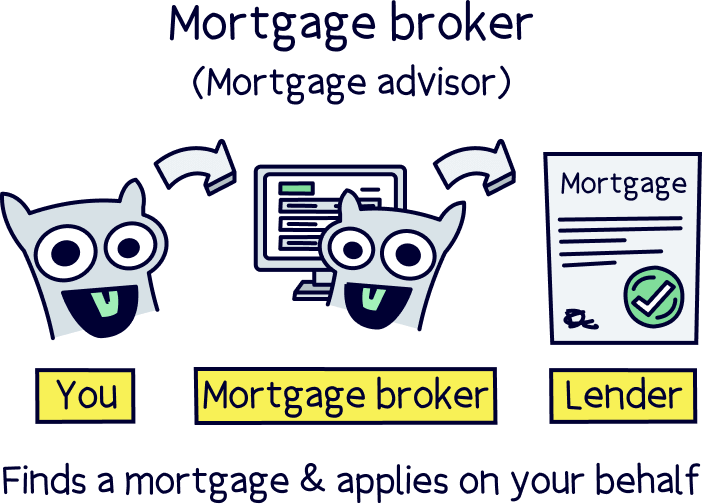

That said, bear in mind that making a single application isn’t your only option. Some lenders specialise in helping people get mortgages with bad credit scores, so you might be able to get just as good a deal on a joint mortgage as you would with a single one. Make sure you talk to a mortgage broker to explore all your options.

Need help finding one of these awesome people? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

If your spouse is unemployed or on a low income, you might think you stand a better chance of getting a mortgage on your own. But that’s not always true.

As long as you can prove that between you, you’re earning enough money to afford the mortgage repayments, most lenders will be happy to add your spouse’s name to the mortgage – even if they’re out of work.

In fact, getting a joint mortgage might actually help your application. If your spouse isn’t on the mortgage, a lender might see them as a financial dependant (which means they rely on you financially for things like food, clothes and money). This could affect how much your lender is willing to let you borrow, as they’ll see your partner as an extra expense that might prevent you from being able to pay as much in monthly mortgage repayments.

First-time buyers don’t have to pay Stamp Duty (a tax that’s charged on property purchases) as long as the property they’re buying is under £625,000. So, if you’re a first-time buyer but your partner isn’t, you might think that by buying a property on your own, you can avoid paying Stamp Duty.

However, that’s not quite how it works!

As you’re married, your spouse will have an interest in the property even if it’s not bought in their name. Unfortunately, that means if they’ve owned a property before, you still won’t be eligible for Stamp Duty relief. In other words, whether you buy the property on your own or not, you’ll get charged the full Stamp Duty tax. Greedy tax man!

Are you separating or in the process of getting a divorce? If so, it makes sense that you’d want to buy a property on your own while you’re still married.

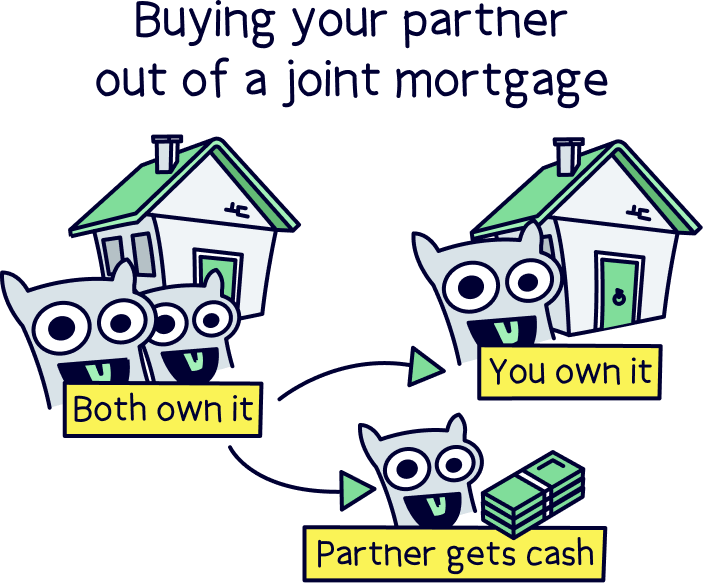

You might want to move out of your current place and buy a new property. Or, if you and your ex jointly own a property you want to carry on living in, you might want to get a new mortgage so that you can buy their share of the property off them (known as buying your partner out or 'transfer of equity'). There’ll normally be lots of options available to you depending on your circumstances and how amicable the breakup is.

Either way though, to get approved for a single mortgage, you’ll need to show that you can afford the monthly repayments on your own. You might also need to show proof of separation. It’s best to get a mortgage broker onboard (also known as a mortgage advisor) to find out exactly what your options are.

Thinking of buying a buy-to-let property or a second home? In this case, it might be more sensible financially to buy it in one person’s name.

If that sounds familiar, you’ll be pretty pleased to hear that getting a single mortgage on a buy-to-let property or second home is a lot easier than getting one on a residential property.

Why? Well, it’s mainly because your spouse won’t be living in the property, so there’s less risk of disputes in the future. On top of that, lenders get that there can be tax benefits when you buy in one person’s name, so they’re generally just a bit more understanding. Woohoo!

Wondering whether your partner would have any rights to the property if you got a single mortgage and then split later down the line? It’s a good question, and exactly why many mortgage lenders won’t want to give you a single mortgage if you’re married.

Technically, the property will be yours – only your name will be on the Title deeds (the documents showing who owns the property) and only you’ll be responsible for paying the mortgage. However, in practice, your ex could still have a legal right to carry on living in the home, regardless of whether they’re a legal owner.

Plus, there are laws in place that mean your home has to be divided fairly if you split with your spouse. Exactly how much goes to each person will depend on things like how long you’ve been married, whether there are any children involved and how much your ex contributed to things like household bills.

Ultimately, things get even more complicated if your ex gifted you money towards the deposit or gave you money towards the mortgage repayments, as you’ll need to prove these contributions were a straightforward gift with no strings attached.

One solution is to get your partner to sign a legal waiver of rights to the property when you first buy it, to confirm that they have no interest in ownership. Most mortgage lenders will also require your partner to sign a ‘gifted deposit’ letter if they’re contributing towards the deposit. This basically just formally confirms that the deposit is a gift and has no influence over their rights to the property. It sounds a little scary but it’s all about making sure things are super clear to avoid conflict later down the line.

Making a single mortgage application can be great for some people, but it’s not for everyone. To help you make a decision about whether or not it’s right for you, brush up on these pros and cons.

As you can see, there are lots of different reasons why you might want to make a single mortgage application when you’re married. And, while some of them are great reasons, a single mortgage isn’t always your only option.

To get some tailored advice about whether it’s the right decision for you, we’d recommend finding a mortgage broker. They’ll take the time to learn about your personal situation and will be able to walk you through all the options. Yup, they really are the superheroes of mortgages!

Our recommendations for mortgage brokers is Tembo¹, they've got award-winning service, and will guarantee to get you the best deal. Get 50% off their fee with Nuts About Money too.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.