Article contents

It’s easy to transfer your pension from Aviva these days. All you need to do is find a great new pension provider (we’ve got our top options below), and they’ll handle everything for you. As simple as that, you don't even need to speak to Aviva.

Looking to move your pension away from Aviva? It’s not as complicated as it might sound, and you don’t even have to speak to Aviva (phew). We’ll run through it in 3 easy steps.

Note: it’s not possible to move your current work pension (while you’re still employed) – you’ll need to wait until you change jobs (you can only transfer pensions from old jobs).

Before we get into the details, if you haven’t found a great new pension provider to transfer your Aviva pension to yet, you’re in luck, we’ve reviewed the best just below.

But before that, if you’re planning to transfer your old pension to a pension you’ve got with a new job, well, it’s not always the best idea – you’ve got the freedom to pick any pension provider you like, so can pick a really great one (such as easy to use and low fees).

You’ll still get all the great tax-free saving benefits that a pension with your work has (more on those below).

Also, if you transfer your old Aviva pension to your new job, it will then be stuck there until you change jobs again, and it might not be the best provider for you (often work pensions aren’t the best). We’ll cover this in detail below.

Anyway, here’s the top options for great pension providers to transfer to:

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).

The biggest question is whether you should leave your pension where it is at Aviva, or transfer it to a new provider – and the choice is yours…

Often, it’s a great idea to move your pension away once you leave your job, and transfer it to a personal pension (one you set up yourself).

This is because most people have many jobs in their lifetime, meaning many pensions, making it hard to keep track of them all over the years – you might be retiring in 40 years or more – and your memory might not be what it is now.

If you just use one personal pension, you’ll then never forget where your old pensions are (over 3.3 million pensions are lost according to The Association of British Insurers), totalling a whopping £31.1 billion.

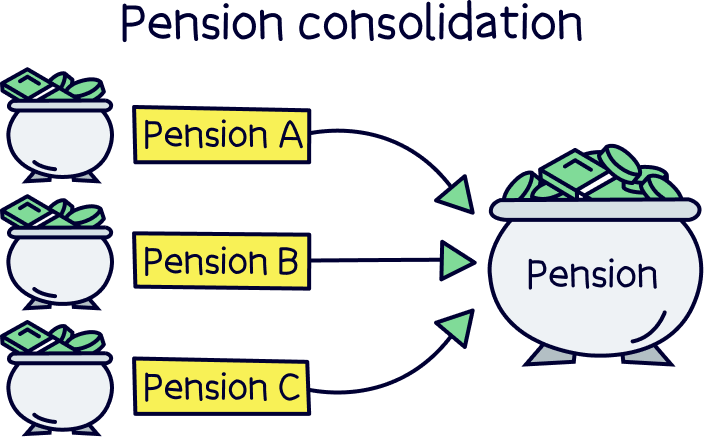

Nuts About Money tip: why not move and combine all of your old pensions over to a single pension pot too (if you have lots lying around).

And, because now you’ve left your job, you get to decide which pension provider to use, so you can pick one that’s easy to use, low cost, has a great track record of growing pensions over time, great customer service and a great mobile app – you can have it all.

Not sure which one to use? We’ve done the research and PensionBee¹ comes out on top for all of those reasons. Plus, we've secured a deal and you'll get £50 added to your pension for free with Nuts About Money.

Right, let’s get to it. How to transfer your pension from Aviva to a new pension provider (a pension company).

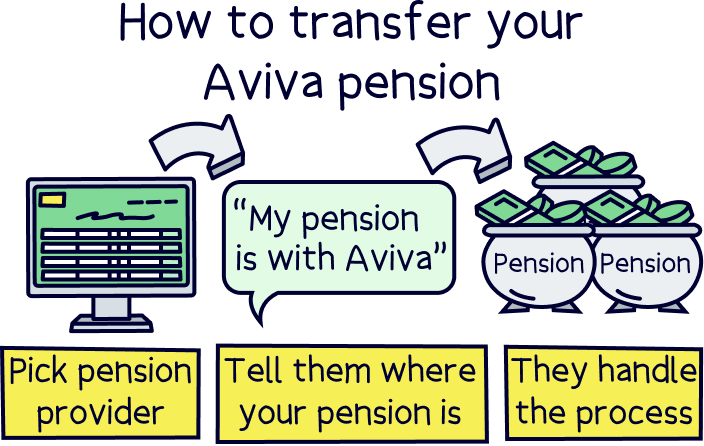

There’s only 3 easy steps:

1. Choose your new pension provider

2. Tell them your pension is with Aviva

3. They’ll handle the whole transfer process, and your money arrives

Simple right? You barely have to lift a finger, your new provider will get in touch with Aviva and handle all the paperwork involved. As an added bonus, there shouldn’t be any extra fees to do this either.

Overall, it should take a few weeks (but can take a few months with Aviva). Once the transfer has been completed your money will be in your new pension pot with your new provider.

If you haven’t picked a new provider yet, here’s all the best pension providers – as a recap, we recommend PensionBee¹, it’s easy to use, has low fees, and a great track record of growing pensions over time (plus great customer service). There’s also Beach¹ who can handle all of your savings, not just pensions.

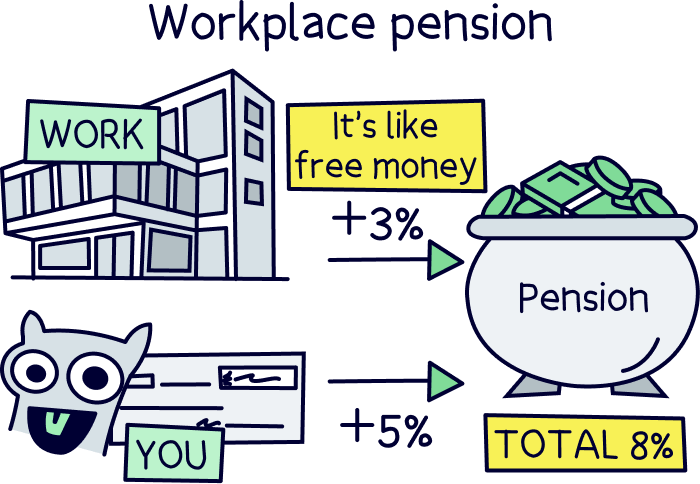

If you’ve changed jobs to a new company and they've set you up with a new pension, called a workplace pension, great!

Why? You’ll be able to benefit from a free 3% of your salary from your employer, if you pay in 5% of your salary, so it’s like a free pay rise.

However, transferring your old pension over to your new workplace pension might not be the best option. When you do this, all your money is now stuck with your new workplace pension provider, and you can’t move it until you change jobs again.

This can seem like a good idea, as you’ll have all your pensions together (which is a great idea). But, often workplace pensions aren’t the best, and most employers don’t typically pick the best ones, they just pick any old one that they’re familiar with in order to get the box ticked (as they’re required to set up the pension by law).

Now, as you left your old job, your pension isn't stuck with Aviva anymore, the world’s your oyster and you can pick a top rated personal pension provider – a pension you set up yourself, you decide which provider, how much to pay in, and even when to start withdrawing from it (as long as you’re over 55 years old).

You can then transfer all your old pensions to your new personal pension (if you have any others), and when you move jobs again, transfer that pension to your personal pension too.

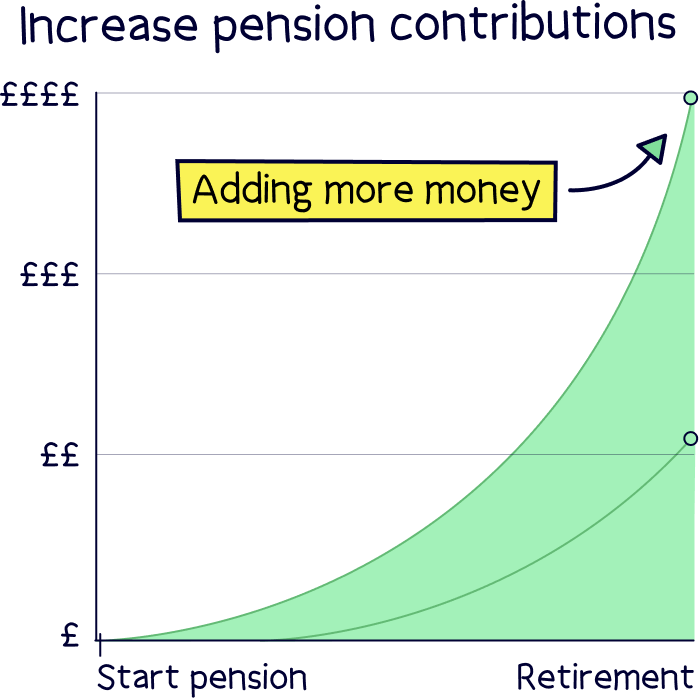

Nuts About Money tip: you can keep making additional top-ups into your personal pension too – to boost your pension pot even more.

And, if you do, you’ll still be able to save into your pension tax-free (just like your workplace pension).

It just works a bit differently, whereby, instead of money coming out of your salary (before you pay tax), you’ll pay in after you’ve paid tax on your income, and so the tax is refunded straight into your pension pot from the Government – which works as a 25% bonus on everything you save. How good is that?

We’ll cover this in more details below, and all the other amazing benefits of personal pensions.

If you’re now self-employed, good for you! Being your own boss can be pretty great – although that does mean you’ll need to sort out your own pension. But, don’t worry, it’s easy these days (in fact we’ve got a guide to self-employed pensions).

All you need to do is set up a personal pension yourself, rather than an employer doing it (which is a workplace pension).

That means you get to pick from all the best pension providers, such as our top recommendation PensionBee¹.

If you run a limited company, with PensionBee, you’ll be able to pay in directly from your company too (which means you can save more in tax).

After you’re set up, you can transfer your Aviva pension across easily, just let your new pension provider know that you want to.

Reminder: keep up the pension saving if you can, it will really pay off over time – the more you can save now, the more potential there is for it to grow.

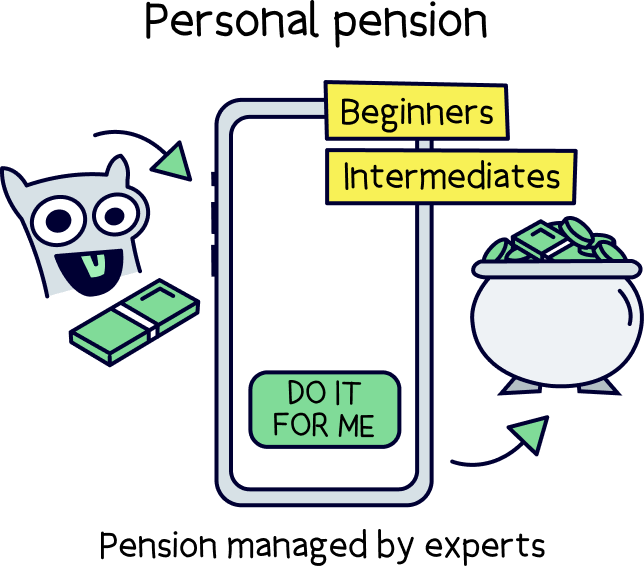

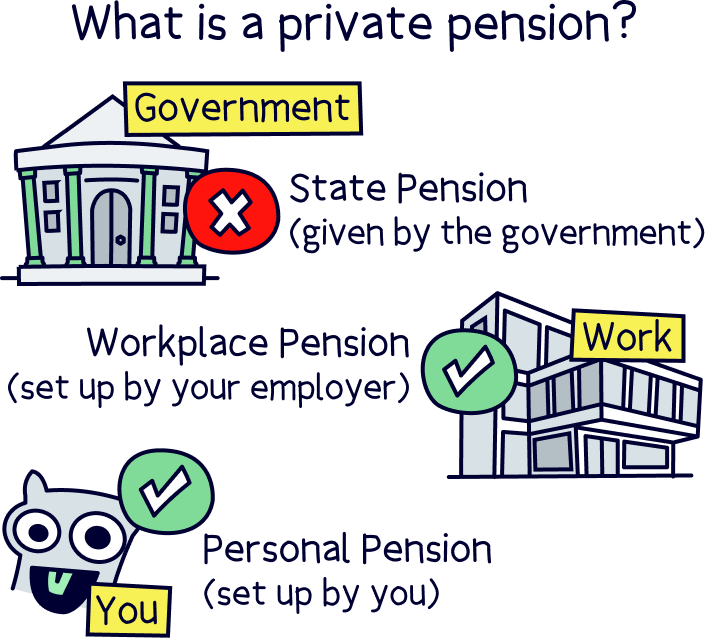

A personal pension is very similar to a pension you might already be familiar with, a workplace pension (one from your work if you’re employed).

However with a personal pension, you open it yourself, and you decide which provider you want to use, how much you want to save into it and when to start withdrawing from it (as long as you’re over 55).

Both a workplace pension and a personal pension are types of private pensions, which simply means a pension that’s in your name (private to you), and all the money is yours, rather than the Government pension, which is called the State Pension.

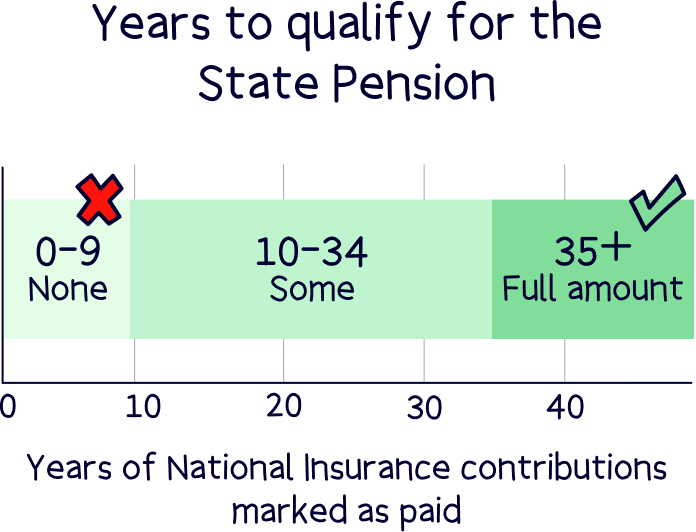

You’ll get the State Pension when you reach State Retirement age, which is currently 66, but only if you made at least 10 years worth of National Insurance contributions, and 35 years to get the full amount.

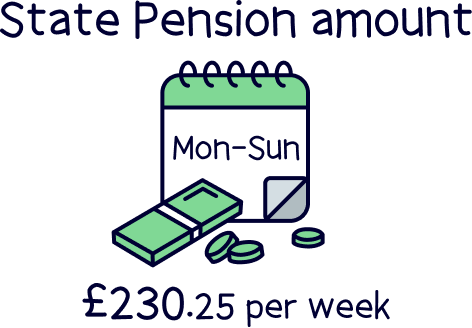

The State Pension is currently £230.25 per week, so not a lot to live off. And that’s where private pensions come in – to build up your pension pot to provide a comfortable retirement.

Personal pensions are pretty great, and there’s lots of tax advantages saving into one…

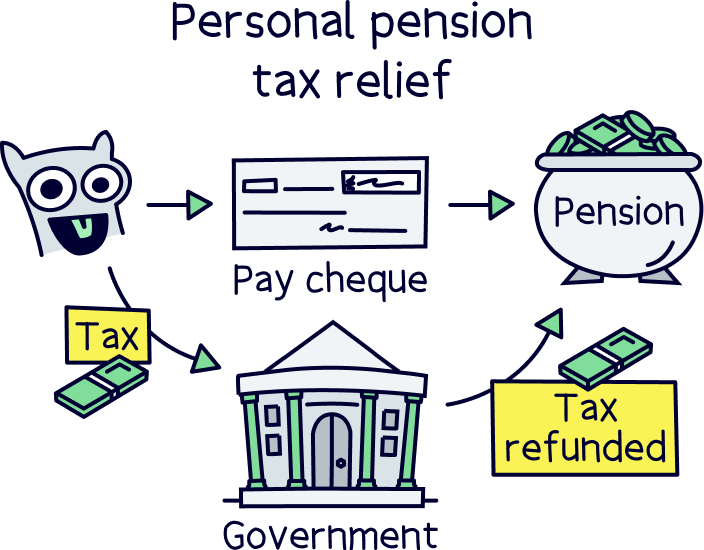

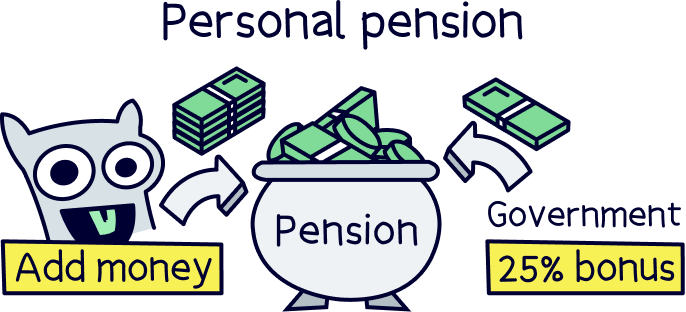

First of all, you’ll get a massive 25% bonus on everything you save (contribute), paid straight into your pension pot directly from the Government.

This is to refund the tax you’ve already paid on your income (e.g. salary), as you’ll only be able to save into your personal pension after you’ve been paid (so you've paid tax on the money).

And, if you’re a higher rate taxpayer (40%) or additional rate taxpayer (45%), you’ll be able to claim some of the tax you’ve paid at those rates too (on a Self Assessment tax return).

Within your personal pension, your money will grow tax-free too, so you don’t have to worry about making any tax payments, and this means your money can grow much more over time (as the tax people won't be taking a cut).

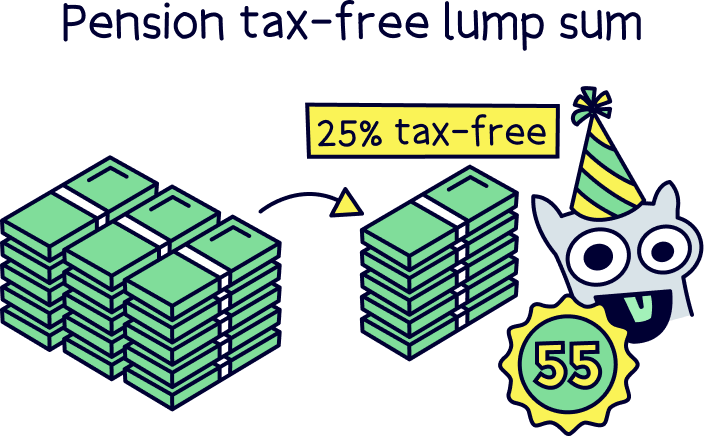

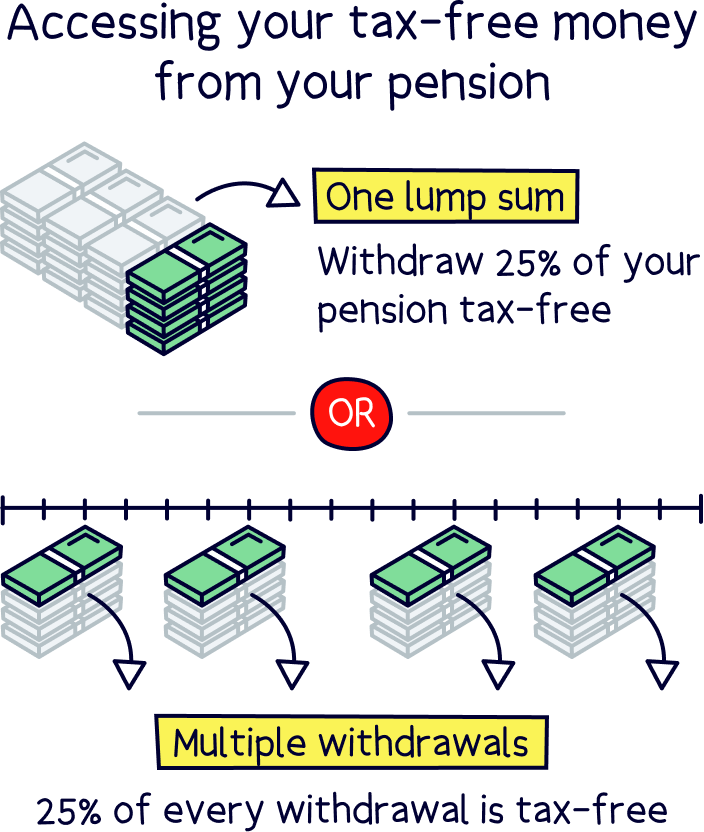

You will likely have to pay tax when you start withdrawing money from your pension, but 25% of it will be tax-free, and you can even take it as a tax-free lump sum if you like.

You might have to pay Income Tax (the same as your job now) on the remaining 75%, when you do start to withdraw it, but it all depends on your income at the time.

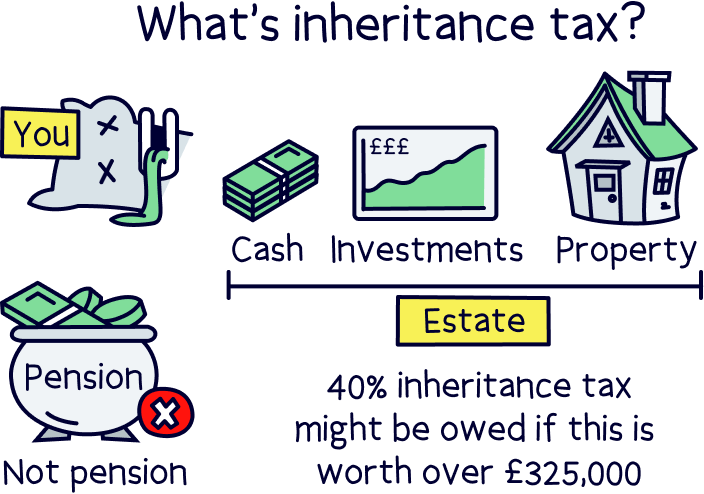

Not to put a downer on things, but when you sadly pass away, there’s no Inheritance Tax to pay on your pension, which is a tax on your ‘estate’ – things like your money and property (another reason why pensions are so great).

Pensions are completely separate, and you can even decide who gets your pension separate from your estate (just let your pension provider know).

And, if you pass away before the age of 75, whoever receives your pension won’t pay any tax at all. If you pass away over 75, they might pay Income Tax when they withdraw from it (it depends on their income at the time).

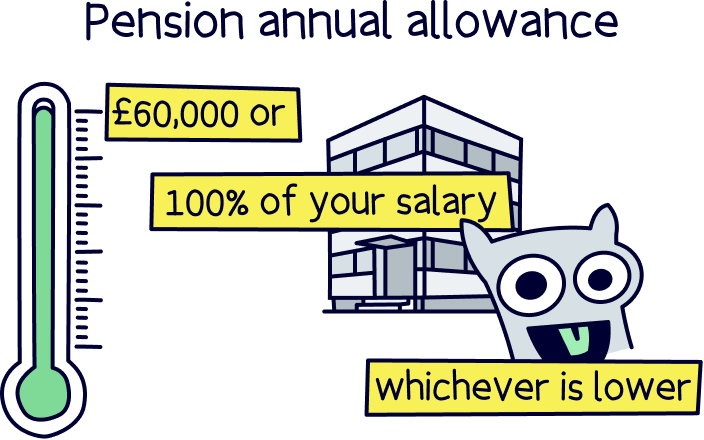

Before you get carried away saving as much as you can into your pension (and you should), there is a limit to be aware of – you can only save as much as your total income each year (e.g. your salary), or up to £60,000, whichever is lower.

And this applies to all of your pensions (so includes your workplace pension too, if you have one).

You also won’t be able to access your money until you’re at least 55 years old (57 from 2028), although if you can wait until you actually retire, it should keep growing a lot more, building up an even bigger pension pot.

Nuts About Money tip: you’ll likely need a very big private pension these days, as much as £853,039 (plus the State Pension) to provide a comfortable retirement of £43,100 per year. Learn more with our guide to how much you’ll need in your pension.

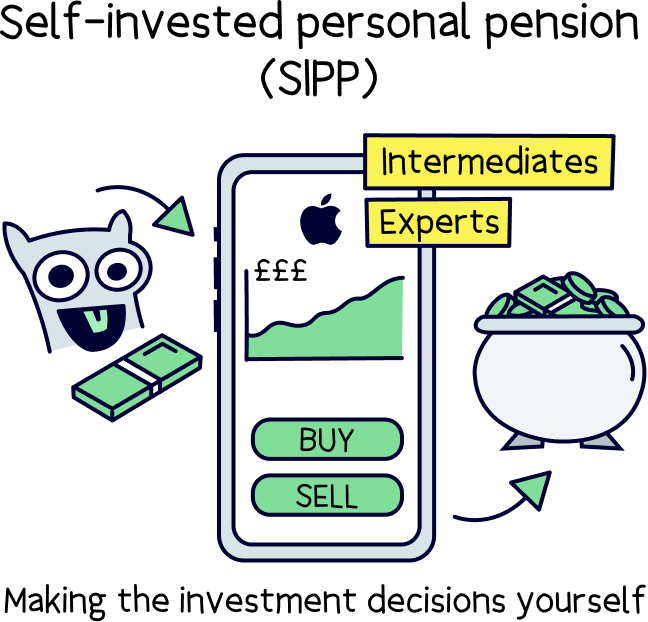

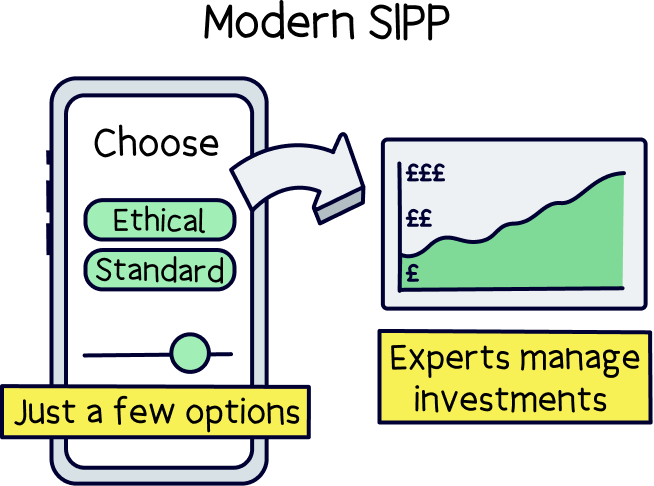

You also have the option to transfer your Aviva pension to a self-invested personal pension, or SIPP. This is exactly the same as what we’ve described above, except that you’ll be the one making the investment decisions – so they’re mainly for experienced investors.

To confuse things a little, the personal pensions we’ve been talking about are all managed by the experts (such as PensionBee¹ and Beach¹), and technically, they’re SIPPs too – but a modern version where the experts handle things, and you simply pick from a small range of easy to understand pension plans.

If you think you might be interested in making your own investments, here’s the best SIPP providers, or learn more with our guide to transferring a workplace pension to a SIPP.

With a private pension, when it comes to retirement, you’ll be able to decide how and when you’d like to start taking your pension. That’s as long as you’re over 55 (57 from 2028).

When you retire (or even before), you can take 25% completely tax-free, and as a tax-free lump sum (if you want to). Or, with each withdrawal, 25% will be tax-free, however you might pay tax on the remaining 75%.

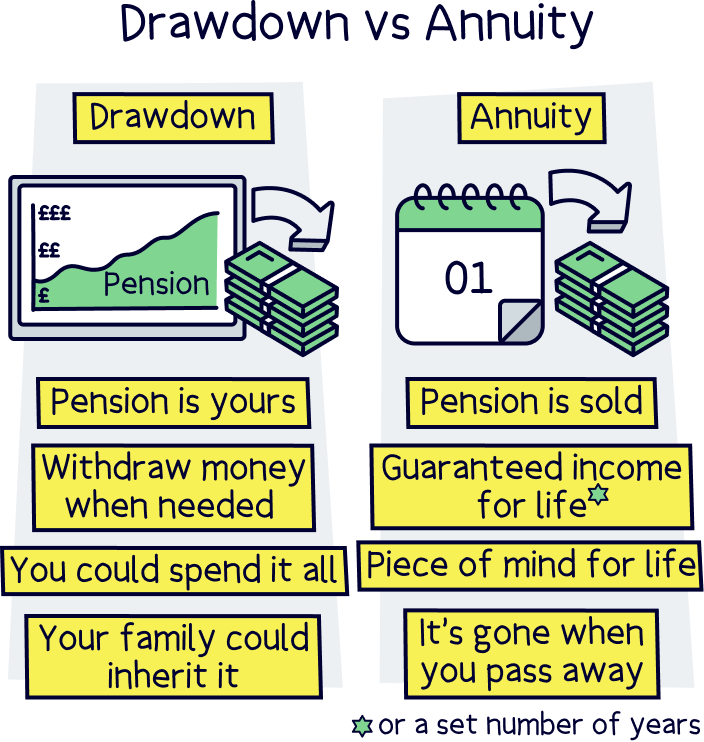

You’ve got two main options when it comes to actually taking your money. You can leave it within your pension account, and simply withdraw money as and when you want to (such as monthly), while letting the rest of it continue to grow over time. This is called pension drawdown.

Or, you can decide to trade in your pension (or some of it), for a guaranteed income for the rest of your life (or a set number of years), which is called a pension annuity.

To learn more, here’s our guide to drawdown vs annuity.

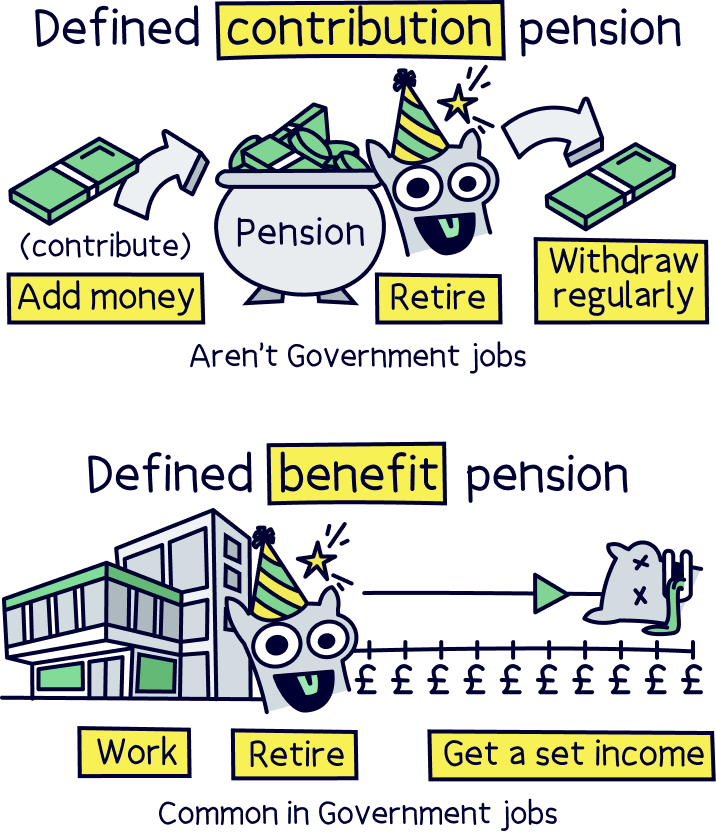

Note: we’re talking about ‘defined contribution’ pensions, which are where you pay into a pension pot throughout your life and has a financial figure (e.g. a £200,000 pension pot). The alternative is a ‘defined benefit’ pension, which are common in government jobs and places like the NHS. You’ll normally get a set retirement amount each year when you retire based on things like how long you’ve worked there and your salary.

Yep, it’s perfectly safe to transfer a pension.

Your money will be sent from Aviva to your new pension provider.

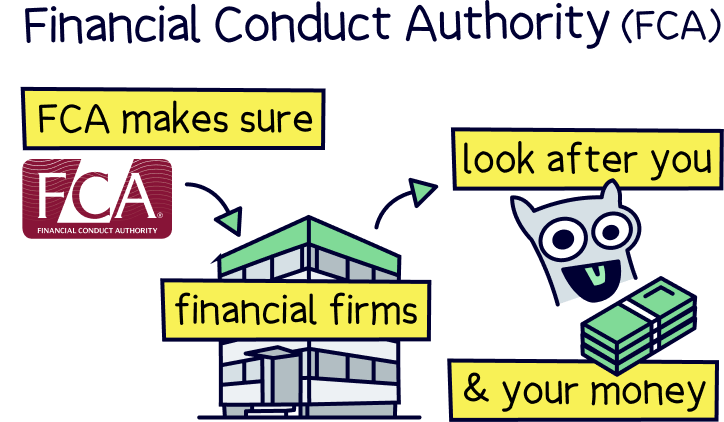

All pension companies need to be authorised by the Financial Conduct Authority (FCA). They’re the people who make sure financial services companies are looking after their customers and their money.

You can check if a company is authorised by the FCA by checking the FCA register.

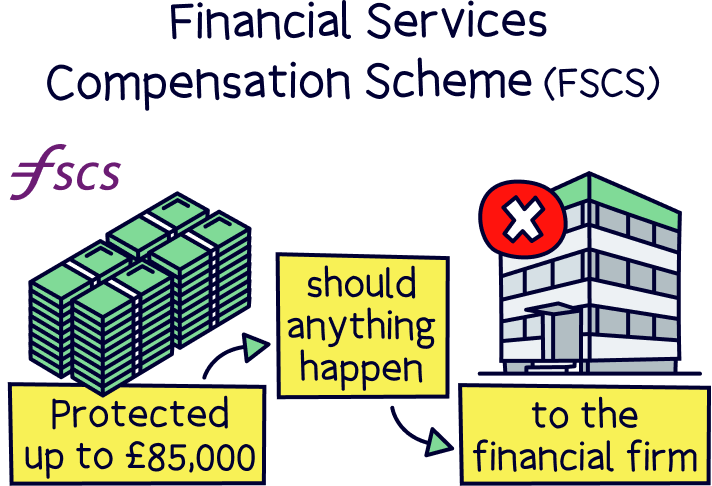

That means you’ll also be protected by the Financial Services Compensation Scheme (FSCS), which can provide up to £85,000 compensation should something happen to your pension provider (such as going out of business).

However, your money is actually within the pension fund itself, which is held with very large banks, all in your name, and can only be returned to you. So overall, pensions are very safe.

There we have it. How to transfer your pension from Aviva. Pretty simple really right?

As a recap, all you need to do is find a great new pension provider, and they’ll handle everything for you – simply let them know you want to transfer your Aviva pension across. Your pension should turn up in a few weeks (but can be a few months with Aviva). And, there shouldn’t be any extra fees either.

If you’re not sure where to find a great pension provider, you’re in luck. We’ve reviewed all the best options, and our top recommendation is PensionBee¹ – it’s easy to use, low cost and has a great record of growing pensions over time. Plus, the customer service is great. As an extra bonus, we've secured a deal where you get £50 added to your pension for free with Nuts About Money.

Beach¹ is another great option, offering pensions and savings accounts like ISAs. For all the top options, here’s the best pension providers.

That’s it. Now you’re all set to enjoy retirement when the time comes!

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out PensionBee – it's easy – they'll handle everything for you. Get £50 added to your pension for free too (with Nuts About Money).