Article contents

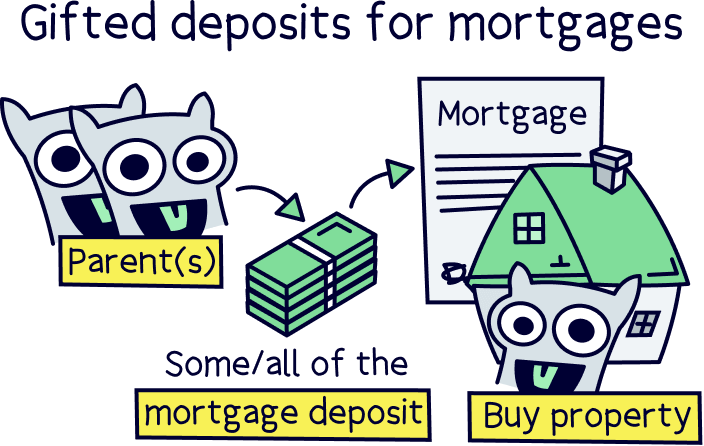

A gifted deposit is when some or all of the money you use for your mortgage deposit has been given to you as a gift, usually by your parents. It’s a great way to get on the property ladder.

Saving up enough money for a house deposit can be hard. So, the chances are you need all the help you can get! In fact, a whopping 56% of first-time property buyers under the age of 35 have financial help from the bank of mum or dad (according to Legal & General).

If you have a parent or relative who wants to help you scrape together a mortgage deposit, lucky you! Keep reading to find out everything you need to know about gifted deposits, from what they are to who can give you one.

A gifted deposit is what it’s called when some or all of the money you use for a mortgage deposit has been given to you as a gift.

Let’s rewind for a second. A mortgage deposit is a sum of money you have to pay upfront when you’re buying a property. In other words, it’s the part of your property’s value that you’re paying straight out of your own pocket, rather than through a mortgage.

Most lenders will only give you a mortgage for a maximum of 95% of your property’s value (lenders are the people who give out mortgages). So, you’ll need to pay at least 5% of the cost of your property yourself through a deposit. We say ‘at least’ because the bigger the deposit you can scrape together, the better the deal you’ll normally be able to get (we’ll talk more about this a bit later).

If someone has kindly given you money as a gift, and you want to use this money to cover some or all of your house deposit, it will count as a gifted deposit.

Firstly, lucky you – that means you’re one step closer to your homeowning dream! But there are a few things you’ll need to know before you use that gifted money to cover your deposit. Here’s the lowdown.

Tembo will find your best deal, fast, all with award-winning service.

Technically, anyone can gift you money for a house deposit. But the reality? Almost all mortgage lenders would prefer it if the person giving you the money is a relative. Think parents, siblings, grandparents… you get the idea!

Some lenders have even tighter criteria and will only accept mortgage deposits gifted by a parent. We know, it’s a bit strict!

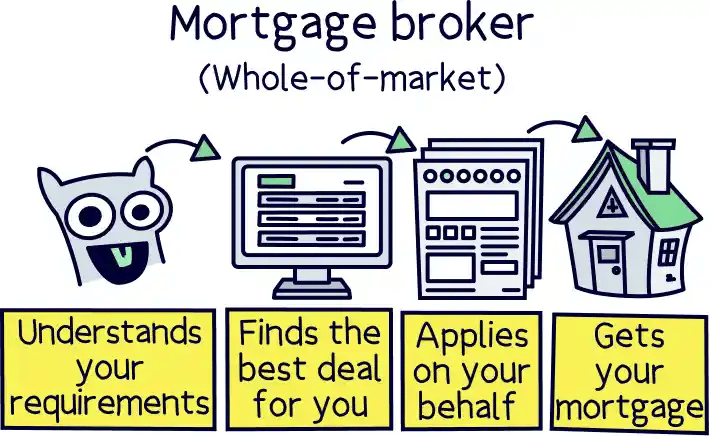

If someone other than a parent or close family member wants to help you with your deposit, the best thing to do is get in touch with a mortgage broker. Mortgage brokers (also known as mortgage advisors) are professionals who help people like you to find a mortgage. So, they should be able to tell you whether there’s a lender out there who’ll let you use the money for your deposit (fingers crossed, all will be fine!).

They’ll also handle the whole process of getting a mortgage for you once you’re ready to go house hunting or you’ve found a house you want.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Gifted deposits are great. Like, really great! But before you get too carried away jumping up and down and celebrating the fact that you’re about to realise your homeowning dream, here are some details you’ll need to bear in mind.

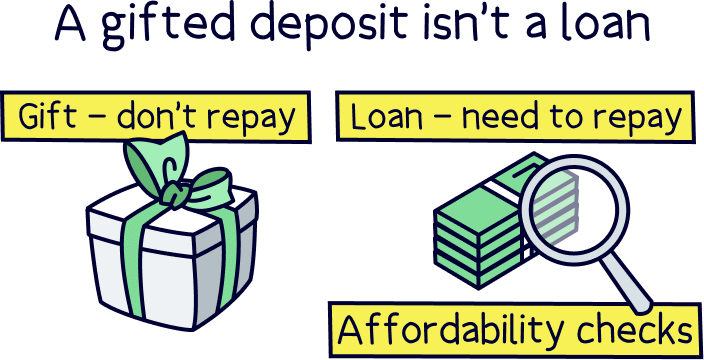

Okay, so this sounds kind of obvious. But you’ll need to be able to prove that the money is a gift. And by ‘gift,’ we mean that the person giving you the money doesn’t expect anything in return.

If your parent (or family member) wants you to pay back the mortgage deposit later down the line, we hate to break it to you, but this isn’t a gift. Instead, it’ll count as a loan. Don’t worry, that doesn’t mean you can’t use the money for your deposit! But it does mean your lender will treat it differently.

Basically, if you’re going to have to pay the money back, your lender will want to take this into account when they’re doing their affordability checks (that’s when they check whether they think you’re going to be able to afford your mortgage repayments, looking at things like your income and expenses). It’ll mean your expenses will be higher and so you’ll have less money left over to pay your mortgage with. And that might mean your lender doesn’t want to give you quite as big a mortgage.

Alternatively, some lenders might not mind as long as your parent or family member is happy to wait until your property is sold to get their money back. In which case, they’ll usually need a written statement confirming it.

Either way, if your deposit is going to count as a gift, your parent or family member also can’t have any interest in the property you’re buying. That means they can’t have any ownership of it, and they can’t expect to get any of the money if you go on to sell it.

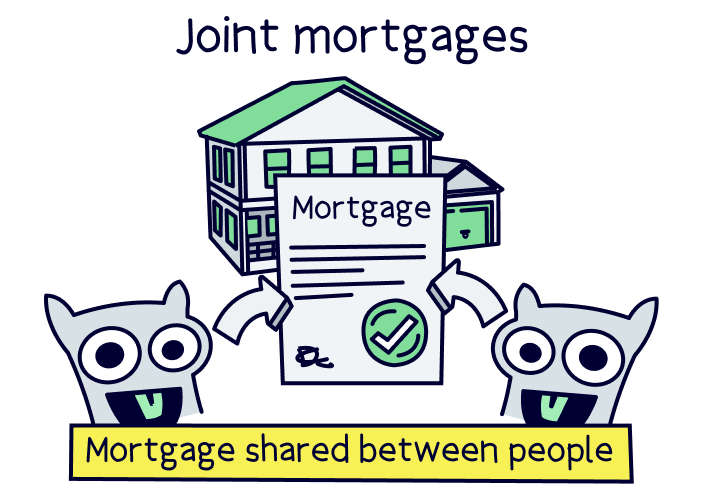

Don’t get us wrong, if your friend or family member does want to jointly own your property with you, that’s totally doable. But you’ll need to look at other options instead of a gifted deposit, like a joint mortgage (where your parent or family member applies for a mortgage with you), or even a guarantor mortgage such as joint borrower sole proprietor mortgage (where you own the property in your name, but a family member can help with the mortgage).

In order to gift you a deposit, your parent or family member has to have enough money to give you. Okay, that might sound like it goes without saying! But there’s a bit more to it than just having enough funds in their bank account.

In a nutshell, your parent or family member can’t do something called ‘depriving themselves of capital.’ That means they can’t give you the money as a gift if it would mean they’d suddenly qualify for state benefits.

To prove that they have enough money to gift you a mortgage deposit, your parent or family member will need to sign a declaration, usually in a written letter known as a gifted deposit letter. As a last resort, they may also be asked to show their bank statements, to prove where they got the money from. This will help with anti-money laundering checks (where people make sure the money wasn’t obtained illegally), which we’ll get to in a bit.

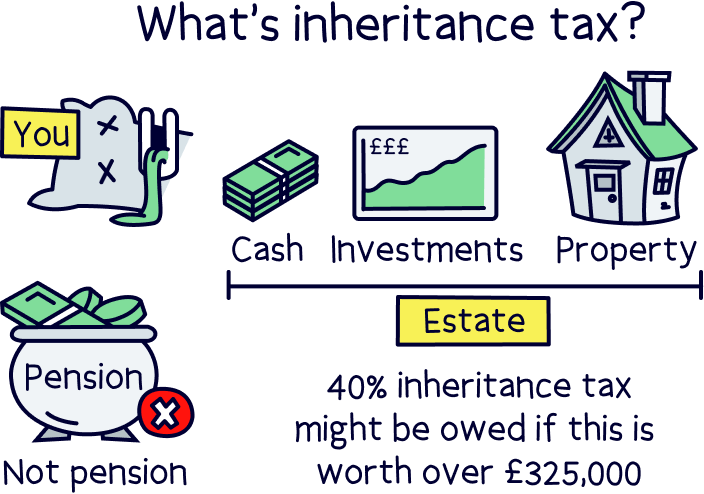

Inheritance tax is a tax that’s charged on the belongings of someone who’s died (yeah, sorry to put a downer on things!). Most of the time, you won’t have to pay tax on your gifted deposit – as long as the person gifting you the money is still alive! However, if they pass away within 7 years of giving you the money, you might have to pay inheritance tax on it.

Everyone is allowed to gift up to £3,000 each year without qualifying for inheritance tax. But other than that, when someone dies, inheritance tax is due if everything they own adds up to more than £325,000 (including the gift). If it does, you’ll need to pay a 40% tax on anything above that amount.

So for example, let’s say the person gifting you the money has property, money and possessions that add up to £400,000 altogether. In this case, there’d be a 40% tax on £75,000 (400,000 minus 325,000 = 75,000).

To be honest, Inheritance tax can be pretty complicated so we won’t go into it all here. After all, fingers crossed, your parent or family member will remain fit and healthy for a long time yet! That said, if they sadly pass away and you think you might have to pay inheritance tax on your gifted deposit, you’re best off speaking to a lawyer to find out exactly how much you owe.

There’s no limit to the amount of money you can be gifted for a mortgage deposit. Hooray!

We mean, technically, it’s up to your lender to decide how much gifted money they’re happy to accept. But they don’t really tend to have any restrictions, so you can generally use as much gifted money for your deposit as you (and, more importantly, the gift giver!) want.

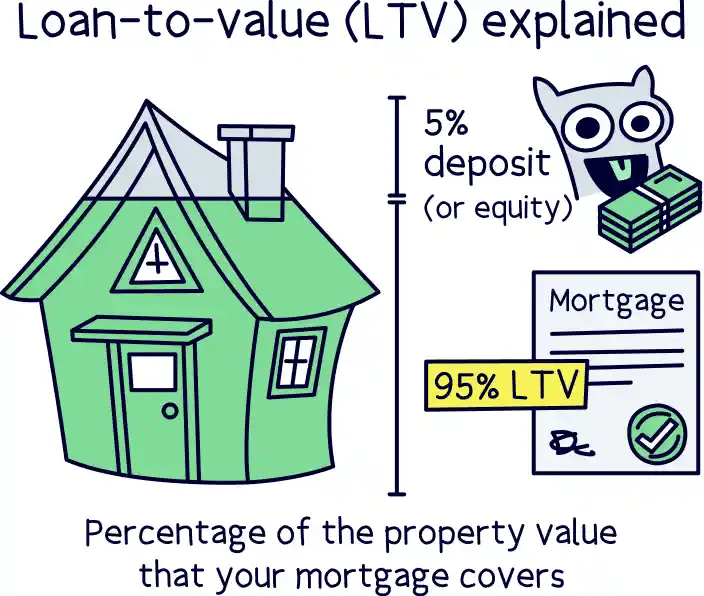

In fact, the bigger you can make your deposit, the better! This is all to do with your loan-to-value ratio (LTV).

Your LTV refers to what percentage of your property’s value you’re borrowing from your lender. If you’re borrowing the maximum of 95% of your property’s value (and forking out a 5% deposit), this is known as a 95% LTV.

For example, for a £200,000 property, this would mean borrowing £190,000 (95% of 200,000 = 190,000) and paying the remaining £10,000 upfront.

However, if you increased the size of your deposit and therefore lowered your LTV, you’d normally be able to access better deals and rates.

Let’s go back to that £200,000 house. If you paid £40,000 upfront instead of £10,000, this would give you an LTV of 80%. Why? Well, you’d be paying a 20% deposit (20% of 200,000 = 40,000) and you’d be borrowing the remaining 80% of your property’s value (80% of 200,000 = 160,000).

By lowering your LTV in this way, you’ll usually be able to find a deal with much lower interest rates (interest is what lenders charge you for the pleasure of borrowing their money), reducing your monthly costs and the amount that you have to pay overall.

Of course, with a bigger deposit, you’ll also be able to afford more expensive properties – this could be a big help if you’re hoping to buy in an expensive area (or you just have expensive taste!).

Got the money in the bank for your gifted deposit (or almost!)? Here’s what you’ll need to do to get the ball rolling so you can use it to buy your dream home.

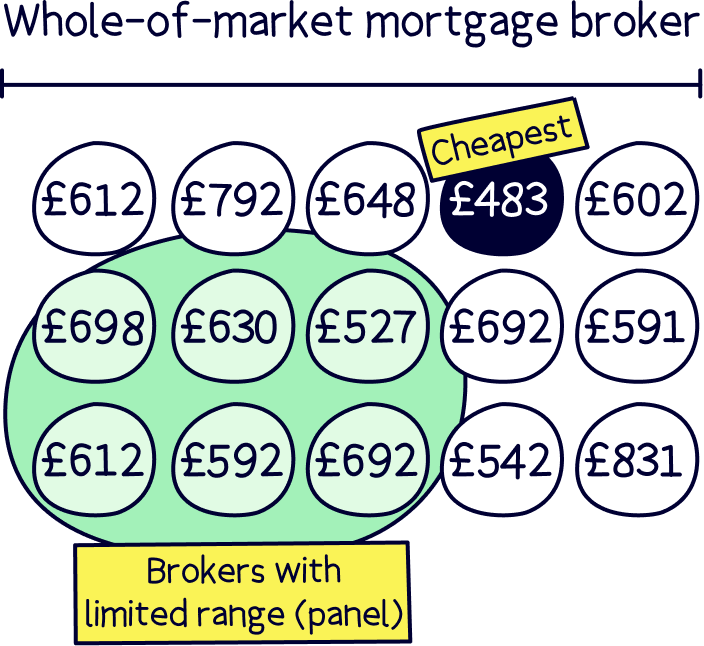

Okay, so you don’t have to get a mortgage broker if you don’t want to (you can just go straight to individual mortgage lenders). But we would really recommend getting one.

Why? Well, mortgage brokers are experts in mortgages. They’ll know which lenders are most likely to accept your gifted deposit and, as long as you choose a whole-of-market mortgage broker, they’ll be able to compare all the different lenders out there to find you the best deal and (hopefully!) save you a load of money in the long run.

Your mortgage broker will also be able to take care of the whole mortgage application process for you, making your life a lot easier and giving you the best possible chance of getting that mortgage you’re after. Need help finding one?

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. Plus, get 50% off their fee with Nuts About Money.

The main difference if you’re using a gifted deposit as opposed to a deposit from your own pocket is that you’ll need to prove the money is a gift, and show where it’s come from.

Most lenders will just need a gifted deposit letter for this, although some banks will have forms for you to fill out instead. Your gifted deposit letter will need to include:

This might sound scary but don’t worry, you’ll have plenty of help from your conveyancer, who’ll make sure that your letter’s all good from a legal standpoint (your conveyancer, also known as your conveyancing solicitor, is the person who’ll handle the legal side of the property-buying process for you). So, you’ll have all the support you need!

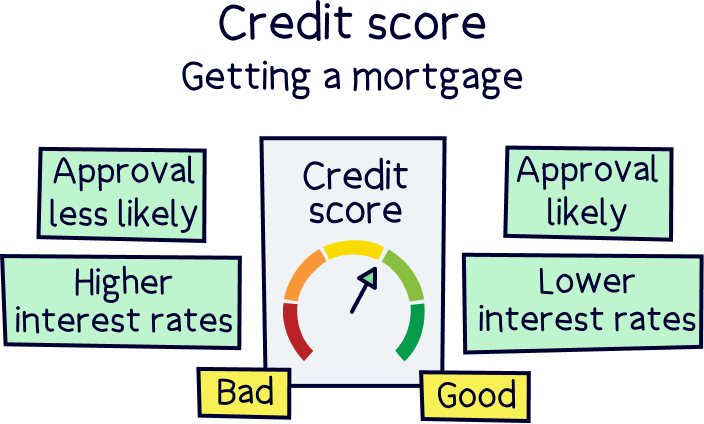

Whether or not you’re using a gifted deposit, your lender will carry out some basic checks to make sure they’re happy to give you a mortgage. This will include checking things like your income, your expenses and your credit score (a score that shows how good you’ve been with money in the past).

However, if you’re hoping to use a gifted deposit, your lender and conveyancing solicitor will also need to carry out some checks on the person gifting you the deposit and their money.

First, they’ll need to see the gift giver’s photo ID and a couple of documents showing proof of address (like utility bills or Council Tax letters). They’ll also want to know where the money has come from, which might mean the person gifting you the deposit has to show their bank statements.

Basically, your lender and conveyancer are checking that the money you’re using for your deposit hasn’t been gained illegally, known as money laundering.

Assuming the gifted money is squeaky clean (and we’re sure it is!) this won’t take long and, fingers crossed, you’ll pass all those pesky checks in no time. In other words, it’s only a matter of time before you’re sitting on the floor of your brand new pad with a takeaway on your lap and boxes all around you. Enjoy!

If you’ve got your gifted deposit all lined up and ready to go, that’s great news! The next step is to find a mortgage advisor who can guide you through every step of the process.

That’s right, you just go and find your dream home and your mortgage broker will sort out all the rest, from finding the best lender for your needs to handling your whole mortgage application for you. You’ll be a homeowner before you know it!

As a reminder, if you need to find a decent mortgage broker, check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.