Article contents

There are 2 ways of adding someone to a mortgage. You can either ask your existing lender if they can add a name to your mortgage. Or you can swap your current mortgage for a new, joint one with a different lender – known as remortgaging.

Do you own your own home? Has your partner or spouse been living with you for a while? If so, you might think it’s romantic (or even just fair!) to add your partner’s name to the mortgage. Especially if they’ve been contributing towards your repayments.

But how do you actually do it? And what do you need to know? Well, you’re in luck! Here, we’ll look at everything to do with adding a name to a mortgage.

First things first, there are 2 different routes you can take if you want to add someone to a mortgage.

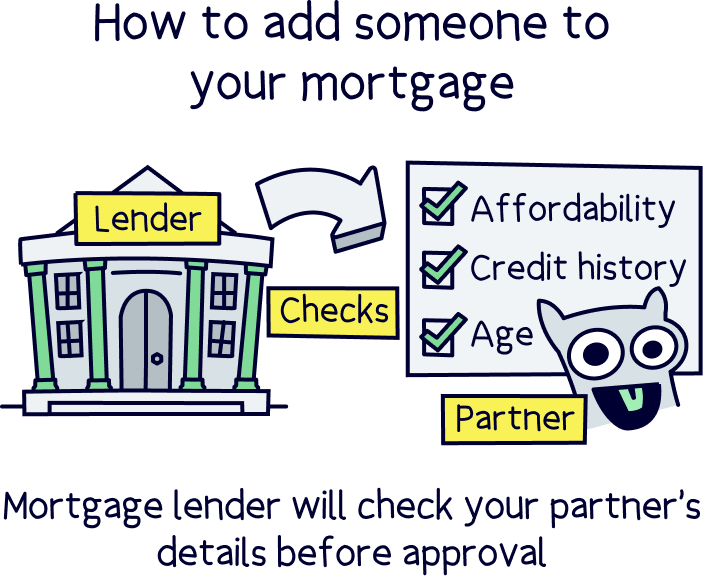

Your current mortgage lender might be happy to add your partner’s name to your existing mortgage (your mortgage lender is the organisation that gave you your mortgage in the first place).

We say they might be happy because before making a decision, they’ll ask you to fill out some forms so they can check your partner’s details. We’re talking about things like your partner’s affordability (whether they can afford the mortgage repayments based on their income and expenses), credit history (how good they’ve been with money in the past) and age (whether the mortgage will be paid off before they hit retirement age).

Basically, they’ll need to complete all those checks on your partner that you went through when you first got your mortgage. Why? Well, it’s because adding someone to your mortgage makes them jointly responsible for the monthly mortgage payments. So, they’re not going to want to add your partner if they think they might run off without paying up (no matter how long you’ve been perfectly paying your mortgage by yourself!).

That said, having 2 of you on the mortgage instead of just 1 makes it more likely that you’ll be able to afford your monthly repayments (after all, that may well mean 2 salaries!). So, if your mortgage lender is happy to consider adding your partner to your mortgage, it won’t normally be too difficult to get approved. If your partner isn’t working and they depend on you for an income though, your mortgage provider might be a little bit harder to persuade!

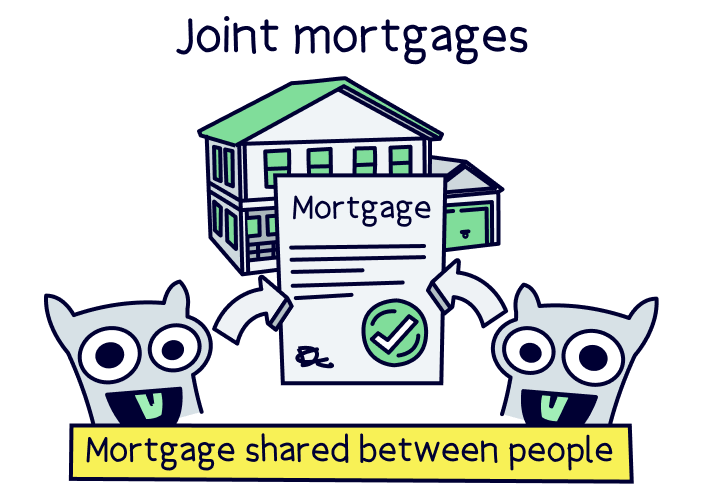

Remortgaging is when you swap your current mortgage to a new one, either with your existing mortgage lender or with a different one altogether. If you want to add a name to your mortgage, you can simply scrap your current single mortgage and apply for a new joint one together with your partner (a joint mortgage is a mortgage that’s shared between 2 or more people).

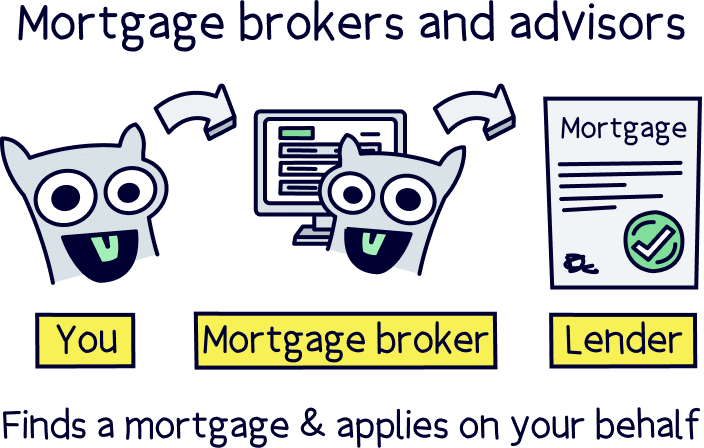

Now, there are 2 ways of applying for a remortgage. You can either apply for the new mortgage directly with a mortgage lender. Or you can get the help of these awesome people called mortgage brokers (also known as mortgage advisors). A mortgage broker is someone who’ll take the time to learn about your personal circumstances before recommending the right lender and deal for you.

Tembo will find your best deal, fast, all with award-winning service.

There are more than 100 mortgage lenders in the UK, so we’d always recommend using a mortgage broker. They’ll have a much better idea than you about which mortgage lender is most likely to approve you and your partner for a joint mortgage. And they’ll normally be able to save you money by helping you find the best deal (plus they’ll sort out the whole application for you, saving you a ton of time and effort!).

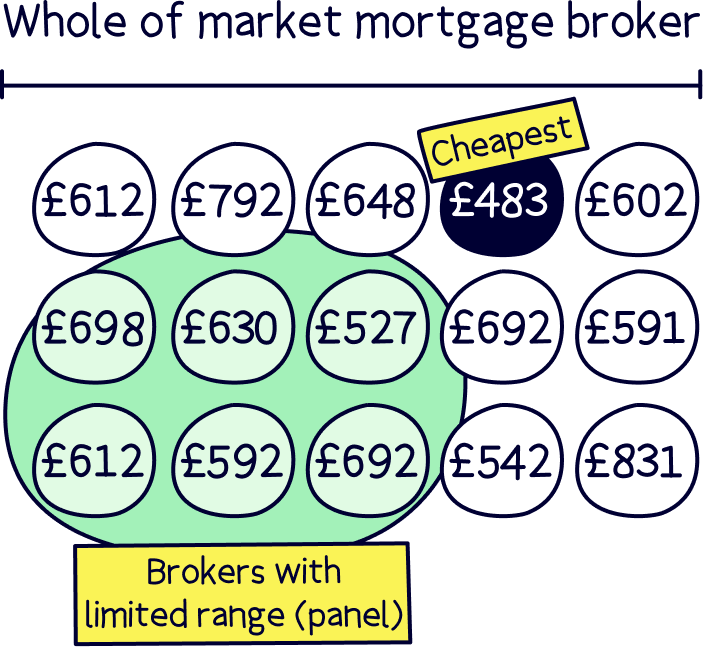

Just make sure that you use a ‘whole of market’ mortgage broker as they can compare all the different mortgages and lenders out there, rather than just a few selected lenders.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service and will guarantee to get you the best mortgage deal. You'll get 50% off their fee with Nuts About Money too.

Once your mortgage broker has sent off your application, your new mortgage lender will need to carry out those same checks we told you about earlier, on both you and your partner. Assuming they’re happy, congrats! You’ve got a new mortgage with both your names on it.

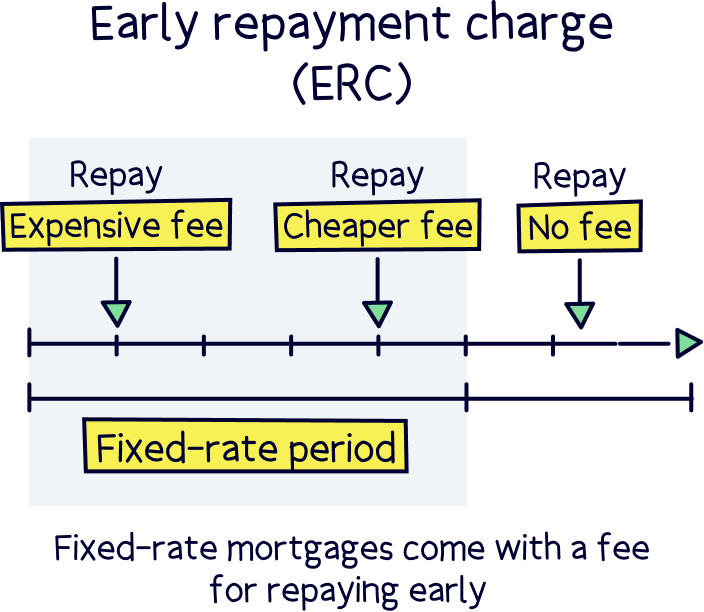

Wondering whether adding someone to your existing mortgage or remortgaging is a better route? Well, that depends on a couple of things. The main one is something called the early repayment charge (ERC).

Let’s rewind a little. When you first get a mortgage, you’ll often get given a specific deal for a set period of time – often 2, 3 or 5 years. This period is called your incentive period because your lender is giving you a special rate to encourage you to choose them.

Sounds good so far, right? The only problem is that if you leave your mortgage before the end of this period, you’ll usually have to pay a hefty fee called the early repayment charge. This can add up to thousands of pounds! Basically, in exchange for a nice, low rate, you get ‘tied in.’ It’s a bit like when you get a mobile phone contract or you sign up with an energy provider.

We know what you’re thinking: what’s this got to do with adding someone to a mortgage?

Well, if you’re in the middle of your incentive period, you’ll want to avoid remortgaging with a new lender if you can help it. That’s because switching to a new lender would mean paying that hefty early repayment charge. Instead, by adding a name to your existing mortgage, you can avoid the early repayment charge.

However, if you’re not in your incentive period (and 46% of us aren’t, according to Experian!), you’ll normally be better off remortgaging. First, there’ll be no early repayment charge stopping you. And second, you’ll be able to compare all the different deals available to you from all the different lenders to find the very best deal out there. So often, it’ll save you a ton of money – potentially thousands a year!

Just bear in mind that early repayment charges usually get lower as time goes on. They’ll often be a percentage of the amount you owe your lender which is roughly in line with the number of years you have left on your incentive period. So, if you have 2 years left, you’ll face an early repayment charge of around 2%. But if you only have 1 year left, you could just face an early repayment charge of around 1%.

That means if you only have a year or so left on your incentive period and you want to add your partner’s name to your mortgage, it’s still worth checking what kind of deals you could get by remortgaging. Yes, it’ll normally be better to stick with your existing deal so you can avoid the early repayment charge. But if switching lenders means you can get your hands on a much cheaper deal, it might still be worth it. A mortgage broker can help you compare and make a decision.

Not sure what to do? Chat to our friends at Tembo¹, you'll get 50% off their standard fee with Nuts About Money.

Umming and ahhing about whether or not to add someone to your mortgage? At the end of the day, there’s no right or wrong answer – everyone’s different so it’s all about what’s right for you. However, there are a few key things you’ll want to bear in mind.

Are you married or in a civil partnership? If so, there may not be much point in adding your partner’s name to your mortgage.

When you’re married, it doesn’t really make a difference whose name the property is under – both of you will have a claim to it regardless. If the property is under your name and you die, the property will automatically pass from you to your spouse (but make sure you have life insurance so that your partner can pay off the mortgage and carry on living here – otherwise, if they can’t afford the mortgage, they won’t be able to keep living there).

Are you unmarried? If so and you want your partner to jointly own your property, then you probably will need to add their name to your mortgage. But without wanting to sound like a killjoy, make sure to think about it carefully first.

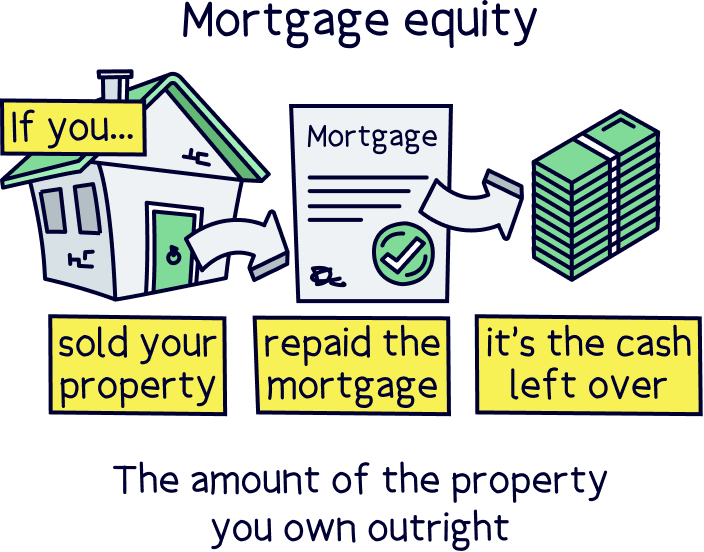

If you bought the property by yourself and you’ve built up a load of equity over the years, it might be a good idea to protect it (equity is the amount of your property’s value that would go straight into your pocket as cash if you sold it). You might be madly in love now, but you never know what could happen later down the line – you might be a bit disgruntled if you break up and your partner gets half of that equity you worked so hard to build!

You can add your partner’s name to your mortgage and still protect your equity if you want to. This is done using something called a ‘tenants in common’ arrangement, which allows you to state how much of the property you and your partner will each own (rather than automatically splitting it 50/50, which is what a joint agreement would do). We’ll look at these options more carefully in a bit.

When you make your partner the joint owner of your property, you’re doing something called ‘transferring equity.’ Yes, you need your mortgage lender’s permission to add your partner to the mortgage. But you’ll also need the help of a conveyancing solicitor to sort out all the legal bits of changing who actually owns your home.

Don’t worry, the legal stuff is usually pretty straightforward as ‘transferring equity’ is a common process. And anyway, your solicitor will take care of it all for you.

To add a name to your property deeds (the documents showing who owns your property), your solicitor will need to get a copy of the property title through HM Land Registry (a department of the government responsible for registering who owns land and property in England and Wales). Then, they’ll create a ‘Transfer Deed’ that you and your partner will need to sign in front of a witness.

If you’re not married or in a civil partnership, you may also want to think about putting together some documents that aim to protect what’s yours. For example, a solicitor could help you put together a deed of trust (stating how much of the property you’ll each own if you decide to be tenants in common). Or, if you want to protect yourself still further, they can help you with a cohabitation agreement (which lays out your arrangements for finances, property and children while you’re living together as well as if you split up, get ill or die).

Some of that stuff might seem like overkill right now and may even make for some awkward conversations with your partner. But at the end of the day, we think it’s better to be safe than sorry!

Another thing that might affect whether you want to add someone to your mortgage is the cost. You may not be buying a house, but there are still fees involved.

First, a lot of mortgage lenders will charge you fees for either changing your existing mortgage (if you’re just adding your partner’s name to your current one) or for sorting out your new mortgage (if you’re remortgaging). These fees are usually meant to cover admin.

On top of that, there’ll be legal fees for all that legal work we mentioned earlier. And in some cases, there may also be a Stamp Duty tax to pay (Stamp Duty is a tax that’s charged when you buy a property).

Don’t worry, most of the time, you won’t have to pay Stamp Duty if you’re just adding someone’s name to your mortgage. But if you’re giving your partner a bigger proportion of the property than what you’re getting, or your partner is planning on paying you for their share, you might qualify for it. Your solicitor can help advise you on whether it applies to you or not.

What’s your partner’s credit score like? If the answer is ‘bad!’ then you might want to think twice before adding them to your mortgage.

A credit score is a number that lenders use to see how good you’ve been with money in the past. Everyone has one – it’s kind of like a financial footprint. If you have a good credit score, that makes it easier to borrow money. But if you have a bad one, lenders might not be willing to lend to you as they might worry you won’t pay them back.

When you get a joint mortgage, your partner’s credit score will become linked with yours, known as an ‘association of credit.’ That means your partner’s financial information will show up on your credit report (that’s where the information is found that’s used to calculate your credit score). If their credit score is good, that’s no bad thing. But if you have a great credit score and your partner has a bad one, linking your score to theirs is something you’ll probably want to avoid.

Why? Well, because their bad credit score can reflect negatively on you. And ultimately, that can make it harder to remortgage your property or move house in the future.

There are 2 main ways that you can jointly own your property. The first (and most common!) is to become joint tenants. In this case, you’ll both jointly own the whole property, and if one of you dies, the other will automatically own the whole thing.

The second option is to become tenants in common. In this case, you’d both own a set percentage of the property. If you split up or one of you dies, the other will only get to decide what happens to their own share. This is a good option if you want to protect any equity that you built up before you met your partner, or if you want to pass your share of the property onto someone else if you die (normally your children).

Before starting the process of adding someone to your mortgage, it’s really important to get some legal advice. A solicitor will be able to talk you through your options and help you decide what’s right for you. However, here’s a quick lowdown:

Are you ready to add someone to your mortgage? If the answer’s yes, just follow these steps to make sure you’ve thought of everything.

Ta-da! You’ve now added someone to your mortgage. And, most importantly, you’ve done it in a way that’s safe and likely to get you the best deal. Go you!

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Unbiased help you find the right mortgage broker for you from your local area. Their advisors are all rated 5*, fully qualified and search the whole-market (every mortgage deal).

Tembo will find your best deal, fast, all with award-winning service.

If you’re ready and raring to add someone to your mortgage, you know what to do! First things first, get in touch with a conveyancing solicitor to get some legal advice.

Remember, it might not seem important now, but it’s worth thinking about what might happen if things go a bit pear-shaped. A solicitor will be able to advise you on how to make sure you protect yourself (and any children involved!) so that you can live your life with that all-important peace of mind that you’ve sorted out the important stuff!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.