Article contents

A General Investment Account is a great addition to your ISA, if you want to save and invest more than £20,000 per year (your ISA allowance). You could also consider a personal pension too – which has massive benefits (such as a 25% government bonus).

Ready to invest but not sure how to get started? Or maybe you’ve been investing for a while but not quite sure if you’re using the right account or not? Well, whatever the reason, here’s everything you need to know to make the right decision for you about a General Investment Account or an ISA.

Let’s run through what both accounts are quickly, and then help you decide which is best for you.

By the way, when we say ISA, we mean a Stocks & Shares ISA. Which, unless you are saving for a new home, is the only ISA you can use for investments (more on other types of ISA later).

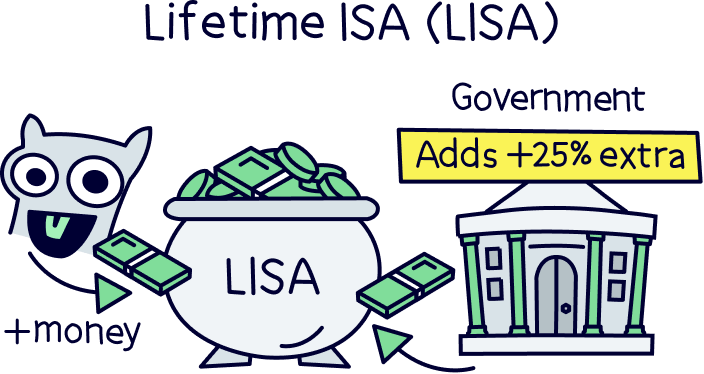

If you are saving for your first home, use a Lifetime ISA – there’s no comparison to be made vs a General Investment Account. You get a free 25% top-up from the government on everything you put in, you can’t beat that! Here’s where to learn more and find the best Lifetime ISAs.

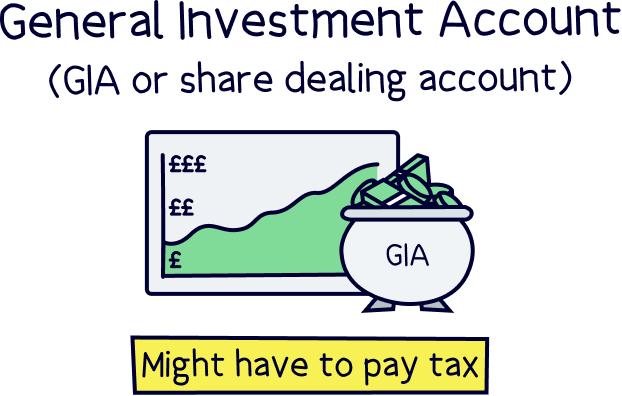

A General Investment Account, or GIA to the pros, and even sometimes called a share dealing account, is simply the bog standard account you’ll get with any investment platform.

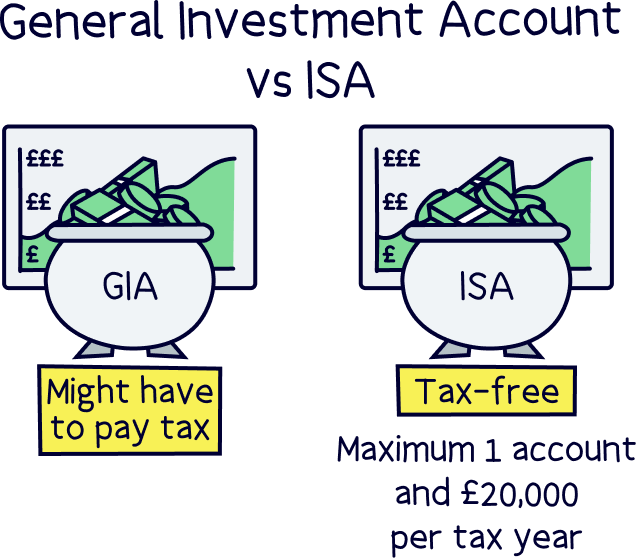

Unfortunately, that means there’s not too many benefits – no tax free benefits, no government bonuses!

All the money you make (gains or interest) from your General Investment Account, will be liable for tax. That means you could potentially have to pay tax on it, but not necessarily, only if you met certain criteria (make lots of profit!).

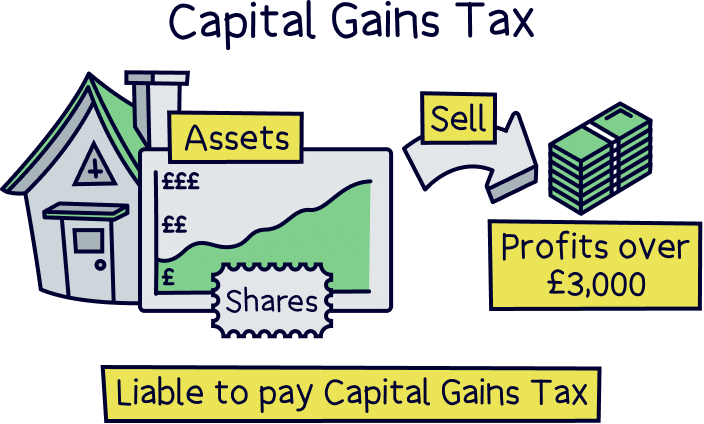

You’ll only pay Capital Gains Tax on your profits within a GIA if they are over £3,000 per tax year, which runs from April 6th to April 5th the following year. And to repeat that’s only on your profits – which means when you sell an investment and it’s gone up in value since you purchased them. If you just hold your investments without selling, you won’t pay any tax until you do.

You might also have to pay Income Tax on any interest you earn from your investments. This works exactly the same way as your regular income, such as your salary (it will be shown on your payslip).

Simply add the interest to your other income, to figure out how much tax you’d pay. It should make sense when you look at the table below:

Unless you’re in Scotland, and then you’ll pay:

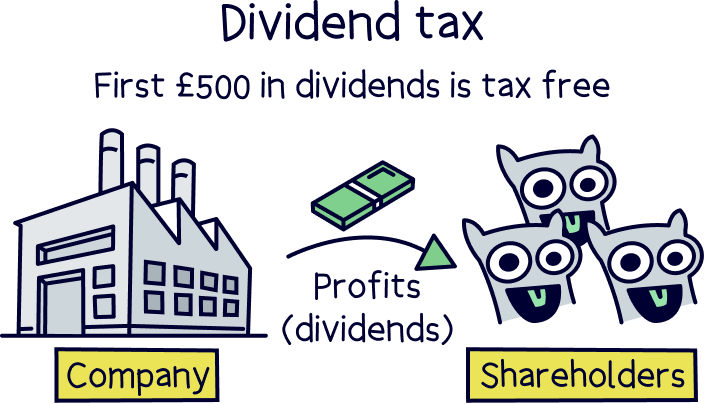

And then there’s Dividend Tax. Dividends are when a company pays out its profits to its owners (its shareholders, so anyone who owns any shares). You are allowed £500 per tax year (your dividend allowance), before you have to pay tax.

Although if you don’t have an income, or a low income, you may not pay any tax on your dividends, as dividends are included within your Personal Allowance, which is the £12,570 you are allowed to make each year before paying tax.

So, providing you are earning an income, you’ll pay tax on dividends depending on which tax band you are in for income. And here’s how much you’ll pay:

Heard enough about GIAs? If not, here’s where to learn even more about General Investment Accounts.

We’ve reviewed and rated the best investment platforms. Make sure you're using the best.

With a Stocks & Shares ISA, you get loads of benefits!

You won’t pay any tax at all on all your investments within the account. So no Capital Gains Tax, no Income Tax and no Dividend Tax. Pretty great right?

Your money can grow much faster without paying tax, meaning more money over the long-term thanks to compound interest, which is where the money you make begins to make you more money, and so on and so on.

Albert Einstein called compound interest the 8th wonder of the world, and he knew a thing or two about maths.

There are limitations with a Stocks & Shares ISA however. You can’t put more than £20,000 into your ISA within a tax year, which runs from April 6th to April 5th the following year.

This is called your ISA allowance, and technically it applies to all of your ISAs – so you can’t put more than £20,000 in total into your ISAs within a year.

The other types of ISAs you could have are a Cash ISA, Lifetime ISA and an Innovative Finance ISA (used for peer-to-peer lending, which is lending money directly to others).

Nuts About Money tip: here’s the best Stocks & Shares ISAs.

Having said there’s no benefits with GIA, and yes you may have to pay tax, a GIA does have its uses!

With Stocks & Shares ISA, you can only pay in a maximum of £20,000 across all of your ISAs.

And that’s where a GIA comes in handy, if you wanted to invest your money across multiple investment platforms, such as maybe you want the experts to manage your Stocks & Shares ISA, but also want to buy some investments yourself, such as some stocks that you think will do well, then you can open a GIA with an investment or trading platform in addition to your ISA.

Or, you could do the reverse and manage your own investments with an ISA, and have the experts complement your investment strategy by opening a GIA with an expert-managed investment platform.

Plus, if you’re doing well and wanted to save more than £20,000 per year into investments, you’d have to open a GIA to invest above this. However, you could also consider a personal pension too. Let’s run through that quickly, as they also have amazing tax benefits.

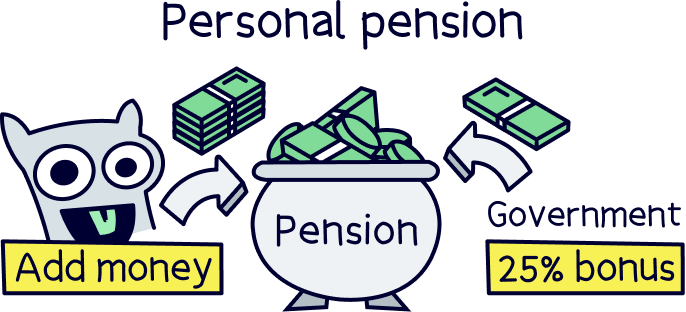

A personal pension, which is a type of private pension (which simply means it’s in your name rather than the State Pension – the one most people will get from the government when they retire), is a great option to invest for the long-term, and retirement.

A personal pension works exactly the same as a Stocks and Shares ISA and a GIA on investment platforms, for instance you can choose which investments to buy, if you want to, or have experts manage everything.

Everything you save is also free from tax, so it can grow much faster than within a GIA account (although you may pay Income Tax tax when you retire. Learn more about tax on pensions).

One major benefit is you get a bonus from the government, a massive 25% of everything you put in. This is normally automatically added to your account by the investment platform. Free money, not bad right?

This is because a pension is intended to be a tax-free savings account, but you’ve already paid tax on your income, and so it’s technically a refund of the basic rate of tax from the government.

And if you’re a higher rate taxpayer, or additional rate taxpayer, you could also claim back 40% and 45% of any tax you’ve paid at that rate! You can do this with a Self-Assessment tax return. If you need help with your tax return speak to our friends at Taxfix¹, their service is rated 5*.

Note: you can put into your pensions, in total, as much as your total income (e.g. your salary), or as much as £60,000 per tax year, whichever is lower.

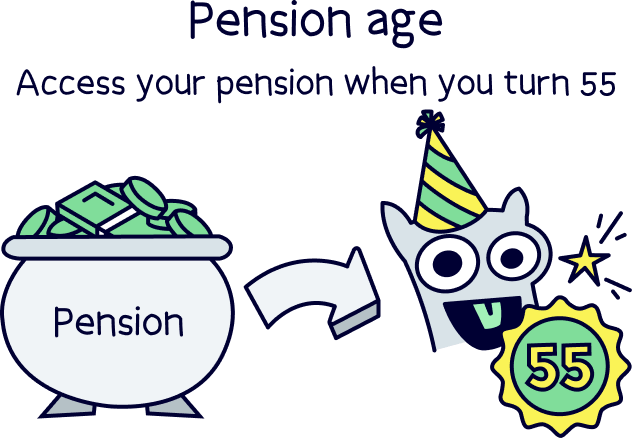

Oh and one last thing, you can’t access the money until you are 55 (57 from 2028). Remember, it’s for long-term investing and retirement… but if you don't want to be working long after your friends retire it's worth saving up for retirement.

We’ve got a guide on pensions and the best private pensions (UK) if you want to learn more.

So there’s all your options when it comes to investing, a General Investment Account, a Stocks & Shares ISA, and a personal pension.

For long-term saving and investing, we’d recommend using a personal pension – the benefits are huge, most notably, the 25% tax bonus you get on everything you put in!

But if you want access to your cash before retirement, then your best option is a Stocks & Shares ISA, where you can benefit from tax-free saving, and grow your money faster.

You can then use a GIA to either top your your investment account if you are saving more than £20,000 per year, or use a GIA if you want to invest on another platform separate to your ISA – such as if you want to manage your own investments, but have the experts manage your ISA.

You’ve got lots of options, and really it’s down to your personal circumstances and how you want to invest, but we hope this helps make the right decision for you.

If you’re looking for places to invest, check out our best investment platforms (UK).

We’ve reviewed and rated the best investment platforms. Make sure you're using the best.

We’ve reviewed and rated the best investment platforms. Make sure you're using the best.

We’ve reviewed and rated the best investment platforms. Make sure you're using the best.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

We’ve reviewed and rated the best investment platforms. Make sure you're using the best.