Article contents

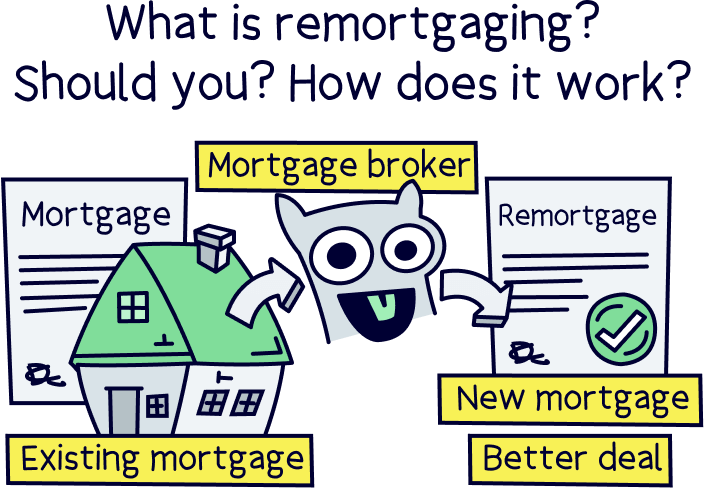

Remortgaging is when you swap your current mortgage for a new one. Most homeowners do it at one point or other, normally to get a better deal and save £100s!

If you’ve got a mortgage, chances are you’ve heard of remortgaging. But what exactly is it? Why would you want to do it? And how does it all work? Don’t worry, you’re in the right place! Here, we’ll answer all your questions about remortgaging and turn you into a total pro.

Remortgaging isn’t as complicated as it might sound. It’s simply swapping your current mortgage for a brand new one.

If you’re like most people, you probably shop around for the best deal on your mobile phone contract or your electricity bills. Remortgaging is pretty much the same but with mortgages!

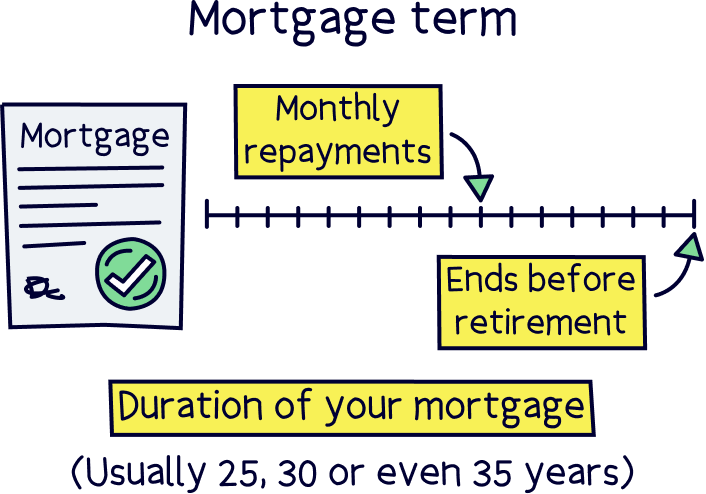

You can either switch to a new deal with your current mortgage lender (the people who give out mortgages) or take out a mortgage with a new lender altogether. By doing so, you could save thousands and thousands of pounds over the course of your mortgage (aka your mortgage term).

Or, you could get some much-needed cash in your pocket by taking out a bigger mortgage than you have right now. We’ll explain it all below!

Nuts About Money tip: get an idea of monthly mortgage repayments by comparing current mortgage rates with our mortgage comparison table.

Tembo will find your best deal, fast, all with award-winning service.

There are tons of benefits of remortgaging. Most of them centre around getting a better deal and saving money. But you may also want to take out a new mortgage with more flexibility, or to take out a bigger mortgage so you can get some money to spend on something else, like a holiday. Here are the main reasons to remortgage.

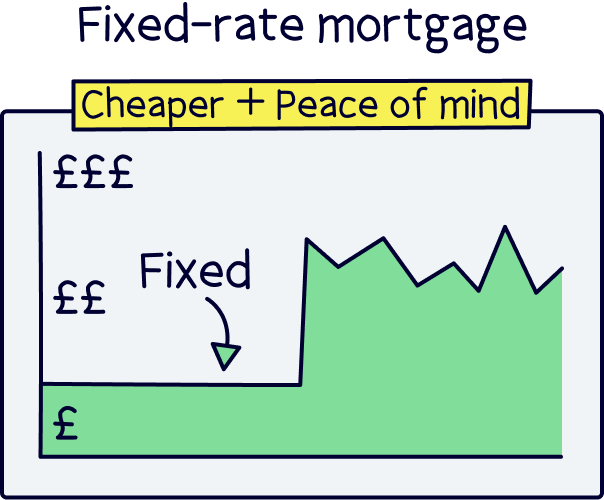

If you’re on a fixed-rate mortgage like most people, your monthly repayments will be set at a fixed price for a certain period of time. Lenders call this the incentive period, as the rates you get will often be discounted to encourage you to sign up with them. Normally, this will be for 2 or 5 years, but it could be longer.

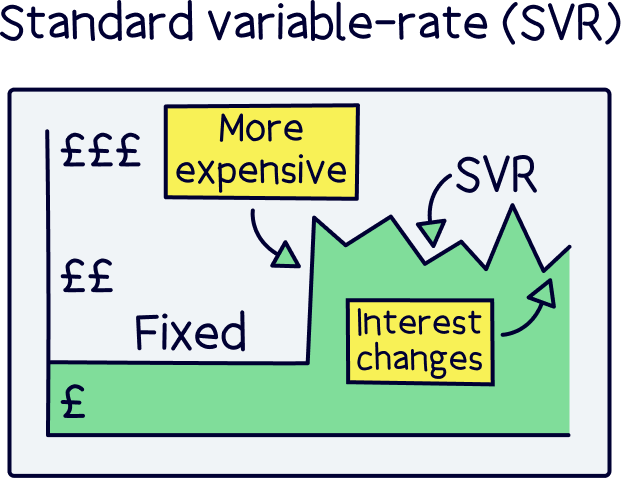

When your fixed-rate period ends, you’ll automatically be moved onto your lender’s standard variable rate (SVR). Basically, this means your repayments could skyrocket and your lender can move them up – or, if you’re luckier, down – whenever they want. Not ideal!

But by taking out a new fixed-rate mortgage instead, you get to benefit from that lovely lower-priced incentive period all over again! Plus, because you’ll (usually) have paid off part of your mortgage by this point, you could find you get an even better deal than the one you were on in the first place (more on this below).

It’s a massive cash saver and you should be doing this every time your fixed-rate period ends. Read our article on what happens when your fixed-rate period ends to find out more.

Even if you’re not on a fixed-rate mortgage, it’s always a good idea to keep your eyes peeled for better deals. Here are some of the times you should think about remortgaging to get a better rate.

Sounds good, right? However, don’t jump in too quickly! Remortgaging can come with fees (we’ll break these down a bit later), so you’ll still need to weigh up the potential savings against the potential costs to make sure it’s worth it. If you’re not a fan of maths then don’t worry – a mortgage broker can do all the sums for you (potentially for free if you pick wisely!).

Tip: Our mortgage comparison table will show you all the fees and monthly repayments.

Not sure what mortgage broker to use? Here’s our recommended mortgage brokers.

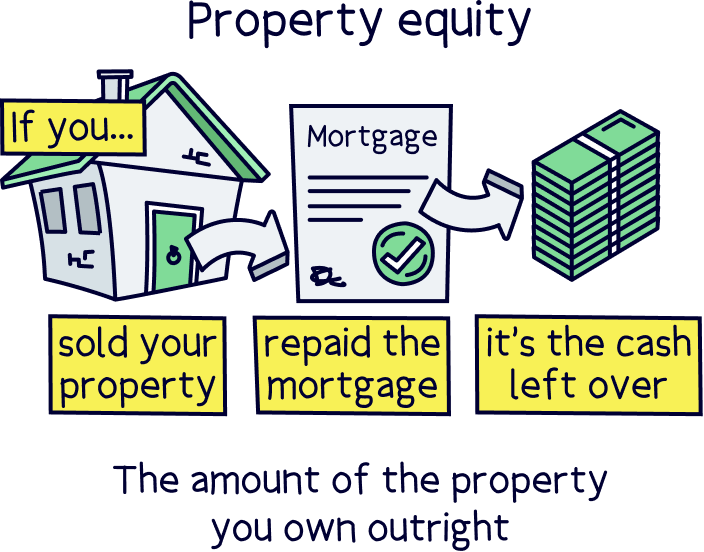

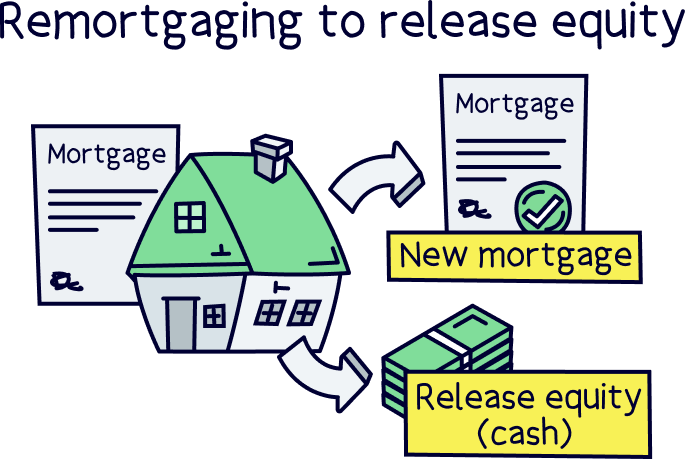

In need of some cash? If you’ve built up enough equity in your home, you could take out a new, bigger mortgage to cover more of the value of your property and therefore reduce the portion you own outright. This will unlock some cash that can go straight into your pocket.

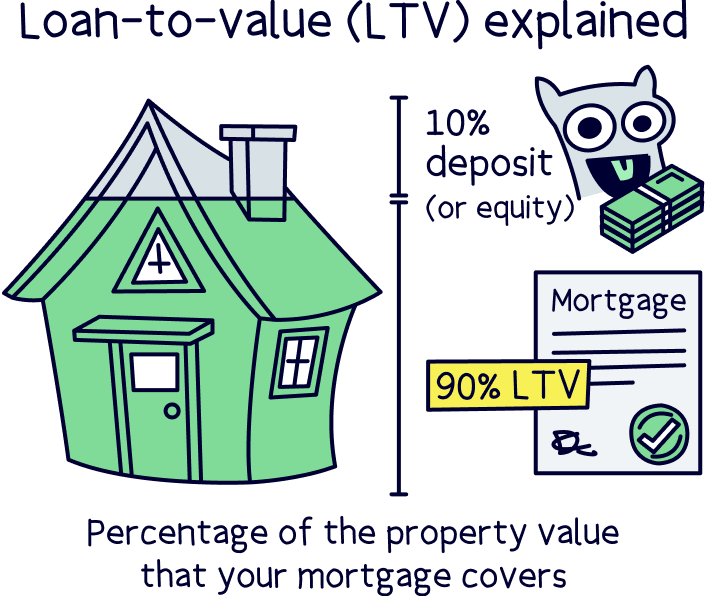

Imagine you own 40% of your house outright and you owe your lender 60% of its value (known as a 60% LTV). If you swapped this for a 70% LTV so that more of your house’s value was covered by your lender, you could get the 10% difference paid to you in cash. Kerching!

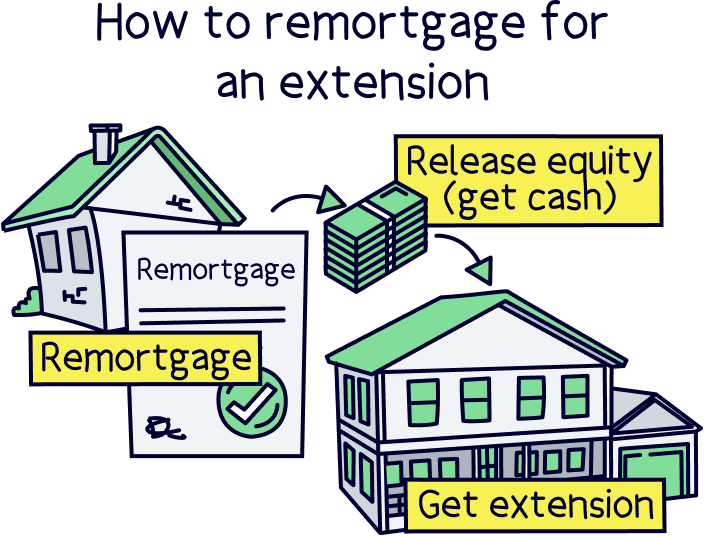

This can be a great way to pay for home renovations or to fund an extension. After all, doing work to your house could increase its value, gaining you more equity in the long run (our guide on how to remortgage for an extension has the full lowdown). That said, you could use the money for absolutely anything – to pay for your child’s uni fees, to buy a new car, to pay for a fancy holiday… you don’t actually need to provide a reason!

Just bear in mind that remortgaging to release equity involves taking out a bigger loan. And bigger loans come with higher interest rates, which can add thousands of pounds to your repayments over the lifetime of your mortgage. You may also end up with a worse deal if remortgaging means moving to a higher LTV bracket. So, be careful. It’s often more expensive than it first seems.

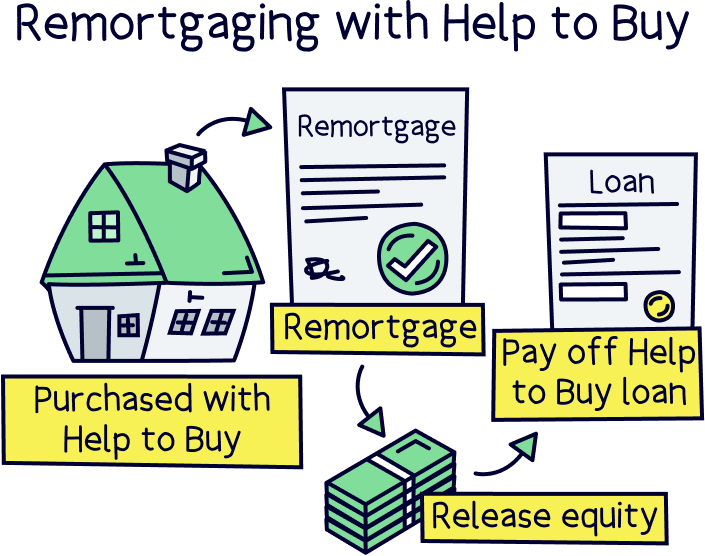

Check our guide on remortgaging to release equity to learn more about it, or if you've got an equity loan, our guide to remortgaging with Help to Buy.

You know what life’s like – things change. When you first took out a mortgage, chances are you picked a mortgage type that worked for you there and then. That doesn’t mean it’s the best type of mortgage for you now!

For instance, most fixed-rate mortgages won’t let you overpay on your monthly repayments. If you’ve suddenly come into a load of cash, you might want to switch to a different kind of mortgage that allows overpayments. That way, you can pay off your mortgage quicker and reduce the amount of interest you have to pay overall.

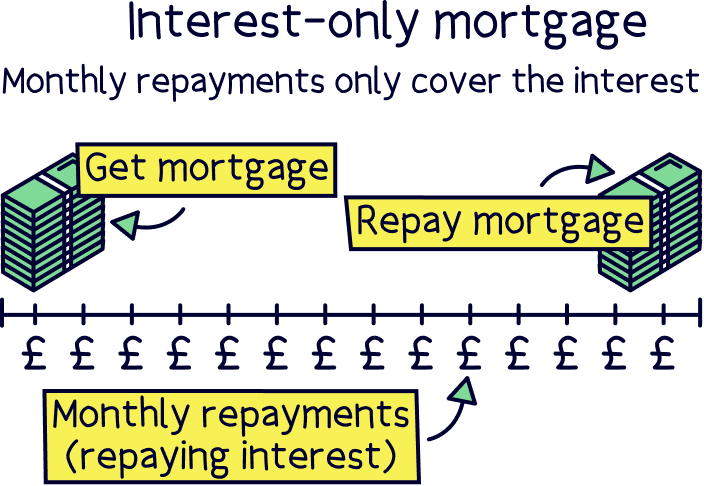

Similarly, you may have taken out an interest-only mortgage (where your monthly repayments only cover the cost of the interest, rather than the loan itself).

If your circumstances have changed, you might want to switch to a repayment mortgage instead, so you can build up more equity (although your current lender will usually be happy to make the change for you, so you might not have to remortgage).

Another option is that you might want a more flexible mortgage that allows you to take payment holidays (where you skip repayments for a month or so). This is likely to cost more, but that might be worth it for you depending on what you’re looking for.

Ultimately, circumstances change and often you end up needing something you didn’t quite expect when you first bought your home. Remortgaging can help you to keep your mortgage up-to-date with your needs.

Okay, okay. So we know we said remortgaging can be great. And it can! But it’s not for everyone. Here are some of the times where you might be better off not remortgaging.

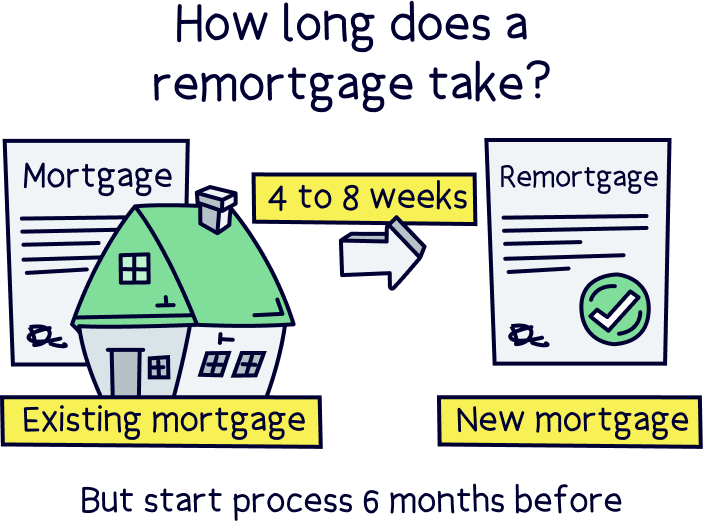

You ideally want to plan a remortgage so that your new mortgage starts immediately after the end of the initial period of your current mortgage - and by immediately, we mean the very next day!

To do this you should start looking to remortgage about 6 months before the end of your fixed term deal, i.e. 18 months into your mortgage that has a 2 year fixed initial period.

Why? Because it can sometimes take a while for a mortgage application to actually go through – a remortgage is actually applying for a new mortgage, the process is similar to when you bought your house but without all the pain of actually finding and moving home, or dealing with slow conveyancers!

But don’t worry if you haven’t got 6 months left to go, anytime before the expiry date of your mortgage deal is fine. Just try not to miss it or you will move onto your standard variable rate and start paying more interest and higher monthly repayments.

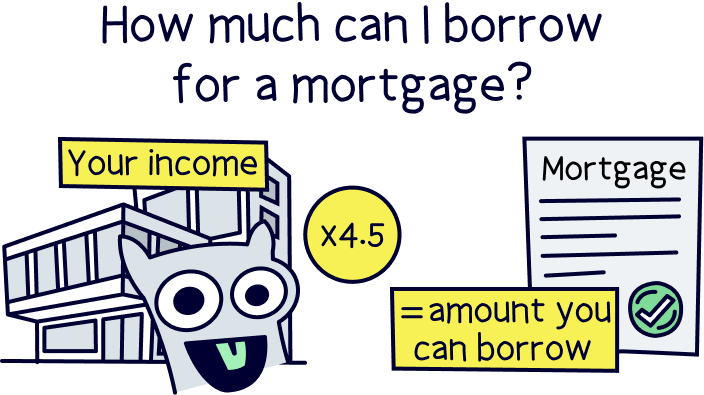

A remortgage is no different to the mortgage you got when you first bought your house. So, you can usually borrow around the same amount (as long as your circumstances haven’t changed). That’s roughly 4.5x your total income.

Got a pay rise since then? Or want to get a mortgage with a partner? If that’s the case, you may even be able to borrow more, which could be handy if you’re looking to release equity. But don’t forget – you’ll want to avoid borrowing so much that you end up slipping into a different loan-to-value bracket, otherwise your rate could get a whole lot more expensive!

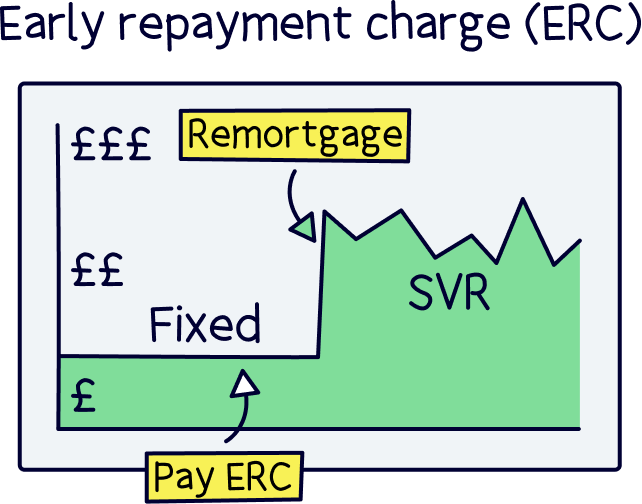

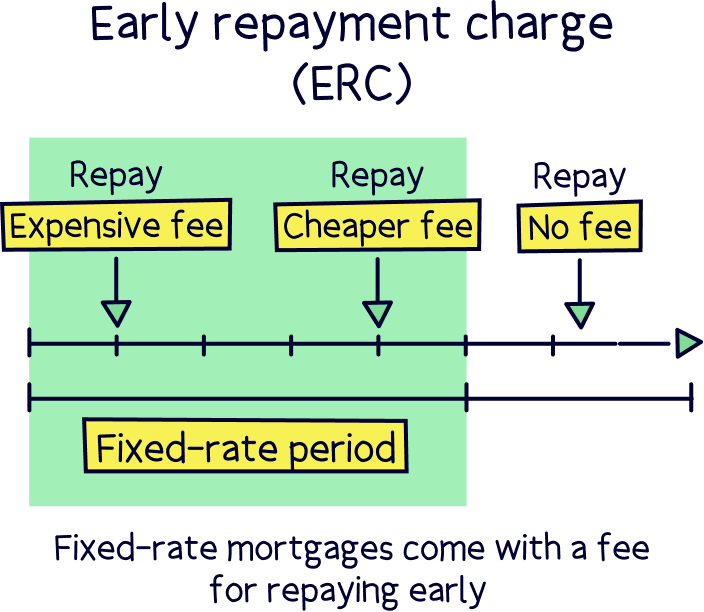

Okay, so this is important: even though you can remortgage whenever you like, if you remortgage during the incentive period of your fixed-rate mortgage, you’ll be hit with an early repayment charge.

Normally, this will be the same percentage as the number of years left on your incentive period – if you have 2 years left, you’ll face fees of around 2%. We don’t mean to scare you, but that’s a lot! So, you’ll probably want to wait until your fixed-rate period is up.

On top of this, you may have to pay an arrangement fee for the new mortgage. Sometimes, you won’t have to pay anything at all, but you could end up having to pay over £1,000. Yes this might seem like a lot, but don’t let it put you off. Assuming you’re remortgaging to get a better deal, you should end up saving a lot more than that over the course of your new mortgage term. We've clearly displayed the fees in our mortgage comparison tool.

There might also be an admin fee for leaving your current mortgage, sometimes called a ‘deeds release fee’. But this isn’t usually big so it’s not normally something to worry about.

The good news is you don’t have to fork out for a solicitor or any costs related to moving home. Instead, you can just go straight to a mortgage broker and they’ll be able to do it all for you.

Note: here's where to learn more about fees to remortgage.

Recently became self-employed? Congrats! However, it’s not all good news when it comes to remortgaging.

When you apply to remortgage with a new lender, they’ll carry out all the same checks that you had done when you first applied for a mortgage. That means they’ll sneak a peek at your credit score, your expenses and, surprise surprise, your income!

Unfortunately, it’s a little harder for self-employed people to prove their income, mainly because you won’t have an employer who can confirm your salary. Your income may also vary from month to month, which can lead mortgage lenders to worry about whether you’re going to be able to consistently afford your repayments (check out our guide to self-employed mortgages and remortgaging when self-employed to learn more).

Don’t get us wrong, you can remortgage when self-employed. It’s just that if you want to switch lenders, it’ll help to have been self-employed for at least a couple of years first, as they’ll want to see your accounts from the last 2 or 3 tax years before approving you.

If that’s not possible, don’t worry. There are lots of lenders out there, including some that specialise in mortgages for the self-employed. Have a chat with a mortgage broker to see if they can help you find one that fits your criteria.

Even if you can’t find a good deal with a new lender, you’ll usually be able to remortgage with your current lender without a problem, as they can treat your application as a straight-up ‘product transfer.’ This means they can simply swap your mortgage to a new one, without having to carry out further checks. Happy days!

If you’re coming to the end of your fixed-rate mortgage, the answer is almost always yes. Your lender’s SVR will usually be a lot more expensive than the rates you’re used to paying. And no-one likes paying more than they have to!

If you’re not coming to the end of a fixed-rate mortgage, however, the answer will depend on why you’re doing it. If you’re remortgaging because you’ve found a better deal then hurrah! That totally sounds worthwhile, as long as you’re not going to be hit with massive fees. If you’re remortgaging to release equity, the answer will depend on how badly you need to unlock that extra cash, and whether you’ll be able to afford the higher interest rates you might be faced with as a result.

Ultimately, only you can decide whether remortgaging is right for you. But a mortgage broker will be able to help.

If you’re coming to the end of a fixed-rate mortgage, your lender will probably get in touch early to coax you into staying with them. But hold fire!

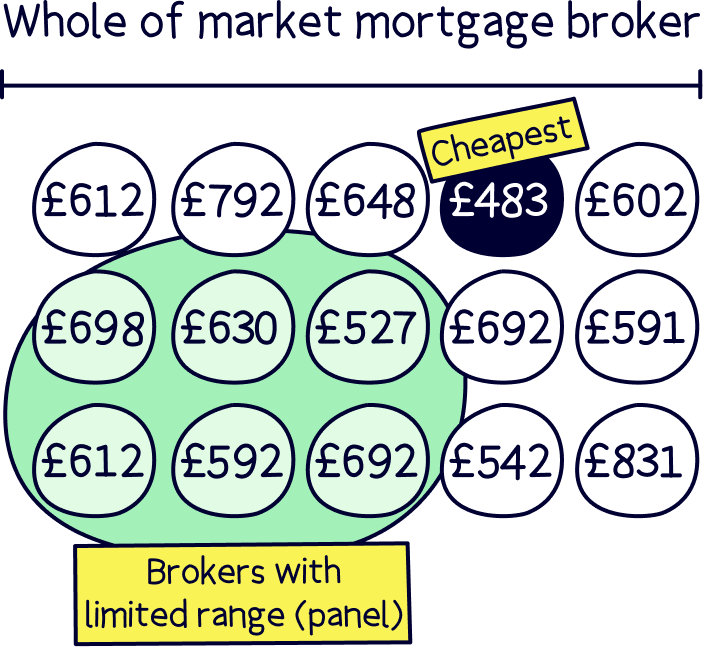

It’s always worth comparing the market, just as you did with your first mortgage. There are thousands and thousands of mortgages from more than 90 lenders, and you want to make sure you’re getting the best deal.

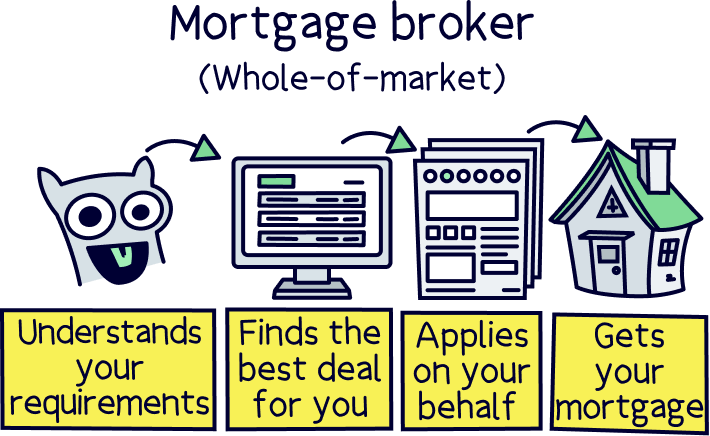

For that reason, the first step in our books is always to talk to an independent whole-of-market mortgage broker. They’ll not only find the best deal for you, but they’ll handle the whole remortgage process for you from start to finish.

We’re serious! They’ll sort out the application for you while you just sit there twiddling your thumbs. Then, roughly 4 to 8 weeks later, voila! Your remortgage will be complete. It really is that easy to save hundreds of pounds per month. Yep, you read that right – not per year but per month! (Or, if you take out a bigger mortgage to release some equity, it really is that easy to give your bank balance that boost it needs!).

So, what do you think? Are you ready to rescue yourself from your lender’s dreaded SVR? To get a better deal that could potentially save you thousands of pounds? To get some much-needed cash in the bank by taking out a bigger mortgage?

Whatever your reasons for remortgaging, start by finding an independent mortgage broker who’ll be able to advise you and find you the best deals. You’ll be swigging champagne out of the bottle before you know it!

As a reminder, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. And, you'll get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.