Article contents

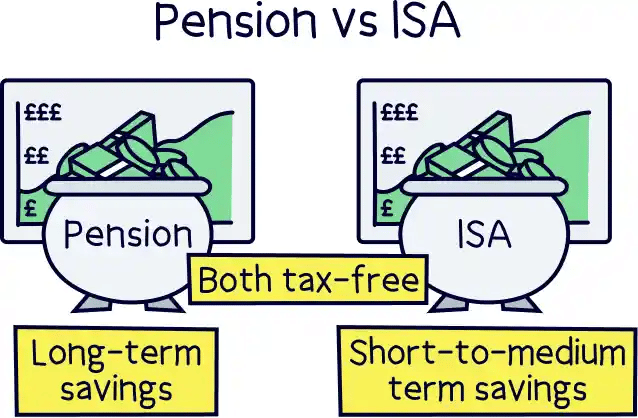

Both have great tax-free benefits. A pension is better for long-term saving, however your money is locked away until you’re 55. An ISA is great for saving too, and perfect if you are looking to spend the cash before you retire. You don’t need to pick between them though, you can have both!

Looking to save and invest your hard earned money but not sure which account is right for you? Maybe a pension, maybe an ISA, or maybe even something else? Let’s run through all your options to help you find the best for your money.

Spoiler: they’re suited to different types of savings goals – and both great in their own right. A pension is perfect for longer-term savings, whereas an ISA gives you the flexibility to withdraw cash when you need it – so short-to-medium term saving.

When we say pension, we mean a personal pension, which is a pension that you manage yourself – you decide how much to pay in, and you decide what pension company to use.

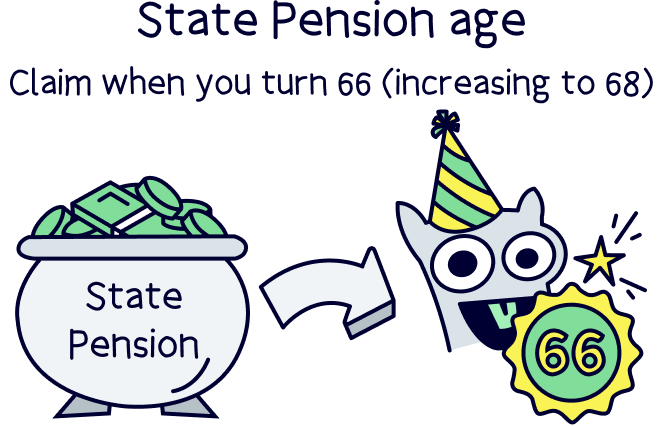

A personal pension is a type of private pension, which simply means a pension in your name (private to you), rather than a public pension, which is the government pension, called the State Pension, which you’ll get when you reach State Pension age – currently 66 (68 in 2046).

A workplace pension, which is a pension your employer sets up for you (if you are an employee) is also a private pension.

A personal pension is a great addition to your workplace pension (if you have one), to help build up your savings for retirement. It’s likely the State Pension and even together with a workplace pension is not going to be enough to sustain a comfortable retirement these days.

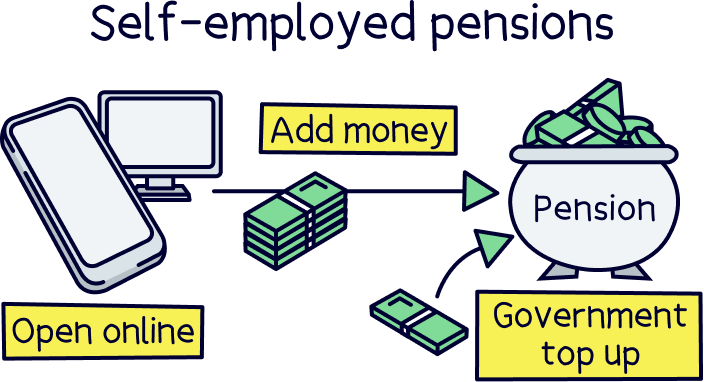

And if you’re self-employed, a personal pension is pretty much your only option to save for retirement. (You should definitely open one if you’re self-employed! Learn more with our guide to self-employed pensions.)

The great thing about a personal pension is you get to decide who your pension provider is (what company to use), and even where you want your pension to be invested. For instance, maybe in socially responsible investments (such as no fossil fuel companies). With your workplace pension, you often don’t have any choice of provider or investment options.

This means you have the ability to choose a low cost provider, which has a great investment track record – with everything managed by the experts, or, you can choose to manage your investments yourself (called a self-invested personal pension).

Note sure what provider to use? A low-cost and great performing pension provider is PensionBee¹ – they’ll handle everything for you too. Here’s our PensionBee review to learn more. Beach¹ is also great, it's an easy to use pension with a great app. Add money or combine old pensions (and find lost pensions). Plus, the customer service is excellent.

Now let’s run through the massive benefits pensions have:

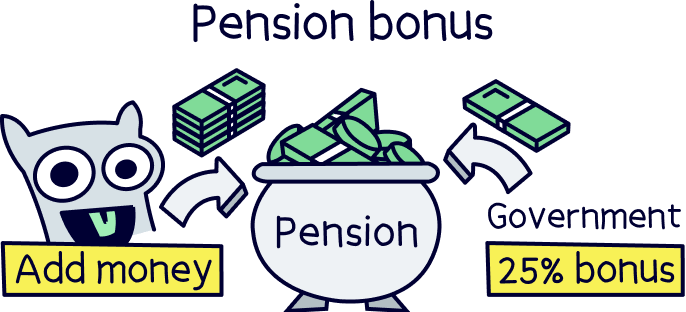

When you save into a pension, it’s intended to be tax-free, so when you pay into a personal pension the government will actually give you the tax that you’ve already paid on your income back as a bonus into your pension pot. It’s like free money, can you believe it?

This is technically called ‘tax relief’, and happens automatically too. So every time you pay into a personal pension, you’ll get a 25% bonus added to your account, completely free. (Which is the tax you’ve paid if you’re a basic rate taxpayer.)

And if you’re a higher rate taxpayer, meaning you earn over £50,270 per year, you can claim tax relief on the tax you’ve paid at 40% too. You’ll do this on your Self-Assessment tax return. And the same applies for additional rate taxpayers (earning over £125,140 and 45% tax).

Getting this bonus can help your savings grow a lot quicker in a very short time frame.

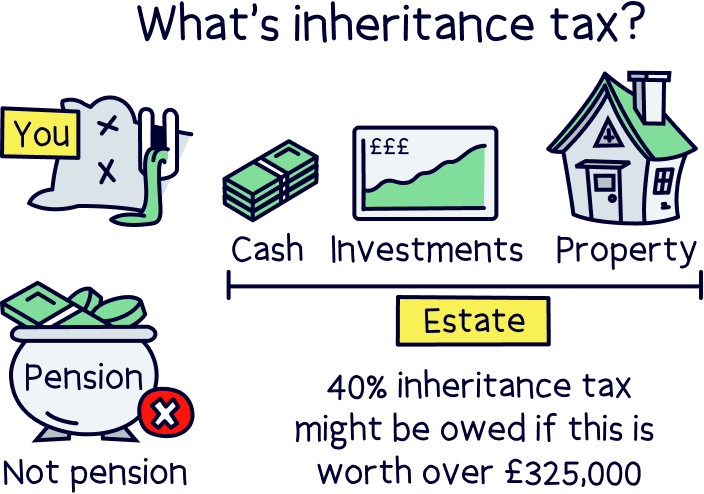

With all pensions, they don’t count as part of your ‘estate’ when you pass away. Your estate is all your money and assets (such as property) added together. And if the total is above £325,000, it will be taxed – and it’s a lot – 40% on anything over that figure!

With a pension the money is passed to whoever you say gets it when you create the pension account. It's often your spouse or civil partner, and of course you can change this. If you pass away when you’re under 75, they won’t pay any tax at all. If you’re over 75, they might have to pay Income Tax.

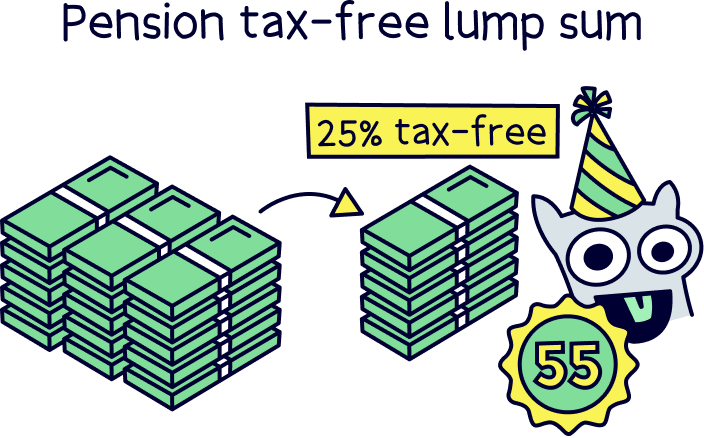

When you want to retire and start taking your cash from your pension (or even if you haven’t retired yet), you can do this from age 55. The first 25% is completely tax-free, and you can take this as a tax free lump sum if you want. After that, you might have to pay Income tax on the remaining 75%.

However, depending on how much you take each year, you may not end up paying any Income Tax as you’ll still have your Personal Allowance of £12,570 of ‘taxable income’ to earn first – just how your income (e.g. salary) works now.

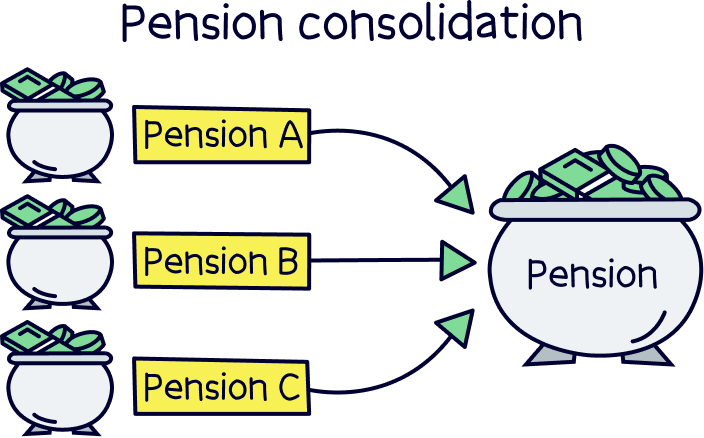

You can also move all of your pensions into the same personal pension scheme (called consolidating your pension), and so potentially benefit from lower fees in total (the more you have saved with a provider, typically the lower the fees). Plus, you’ll be able to manage and view your pension all in one place. And importantly, not forget about any of them!

For instance, you might have had many jobs over the years, all with their own pension. You can actually move all of these over to a personal pension, so they’re all in one, easy to manage, pension pot.

Here’s where to learn more and how to transfer your pension.

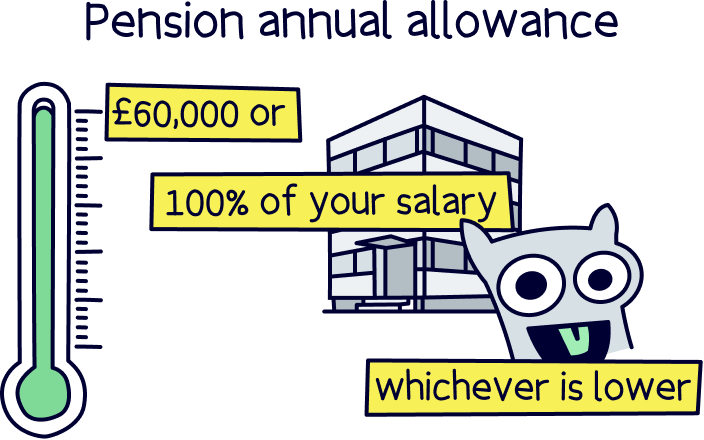

There’s a few things to bear in mind before you start investing your money in a personal pension. There’s a limit on how much you can invest per year, which is £60,000 or 100% of your salary (whichever is lower). This includes your workplace pension too.

It’s unlikely these will affect you, and you’ll probably know if it does – but it's worth considering when planning your savings. And if you are going to pay in a bit too much, that’s where an ISA can come in very handy.

Here’s a quick recap of the pros and cons of pensions:

Beach is an easy to use app allowing you to invest sensibly within a tax-free ISA and a pension pot.

Use a personal pension to save for retirement, and simply long-term savings where you know you won’t need it back for a long-time (after you’re 55). It’s the best option thanks to the government bonus. Your savings can grow much quicker when you’re getting 25% on everything you put in!

Plus not paying Inheritance Tax is also pretty great for your loved ones.

However there’s one point to mention here. If you have a workplace pension with your employer, and they kindly contribute even more than the minimum legal obligation of 3% when you pay in 5%.

For instance, if they match your contributions up to a certain amount (e.g. they’ll match your contributions up to 10%), then you should pay into your workplace pension first before paying into a separate personal pension. It's even more free money!

Other than that, for long-term saving, a personal pension is likely your best option, and best of all, you get to decide which personal pension provider you want – so you can choose one with low fees, great service and a good track record of growing money over time.

By the way, we’ve also done the hard work finding the best providers – here’s the best personal pensions. (Spoiler: PensionBee¹ is top.)

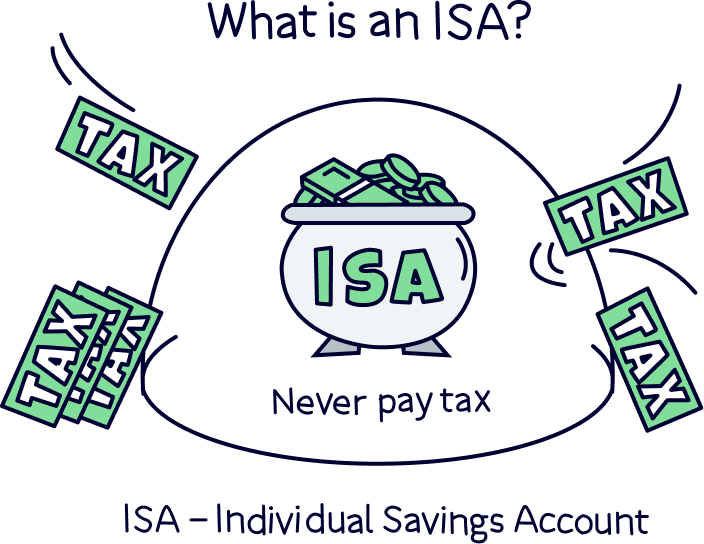

An ISA is another great account to save and grow your cash for the future, tax-free.

There’s actually many types of ISAs out there:

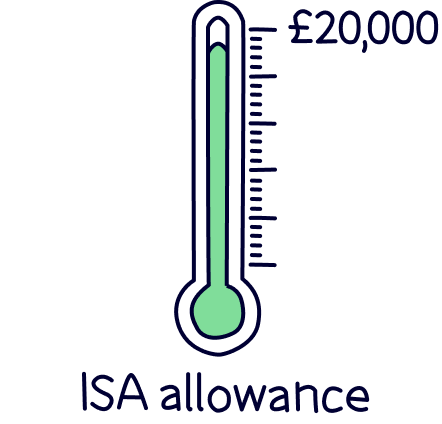

Across all of these ISAs, you have a £20,000 ISA allowance per year. And everything you make is free from tax, forever! Pretty great right?

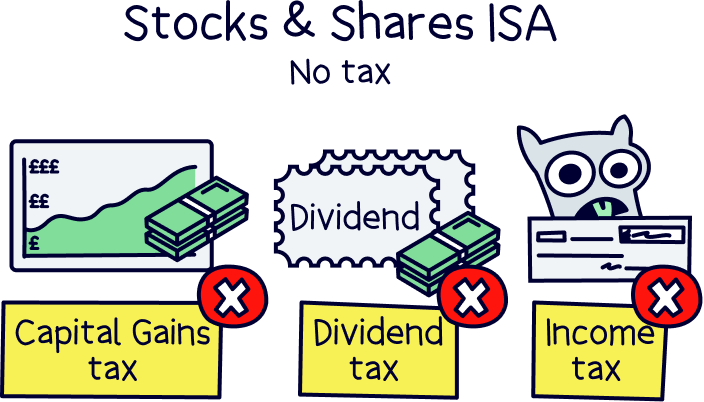

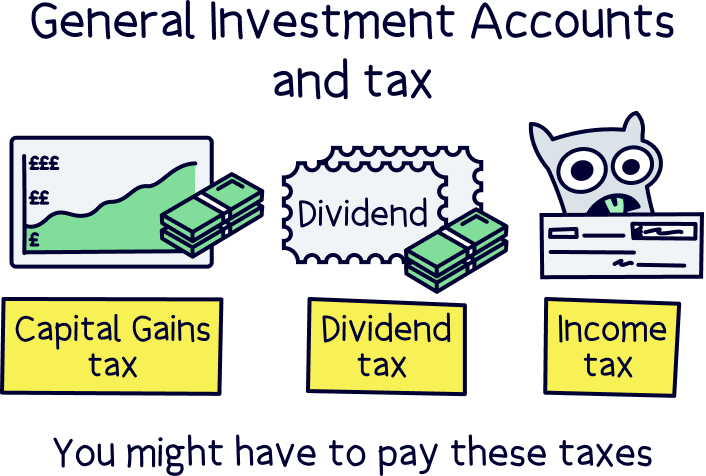

The tax you might otherwise have to pay is Capital Gains Tax, Income Tax and Dividend Tax.

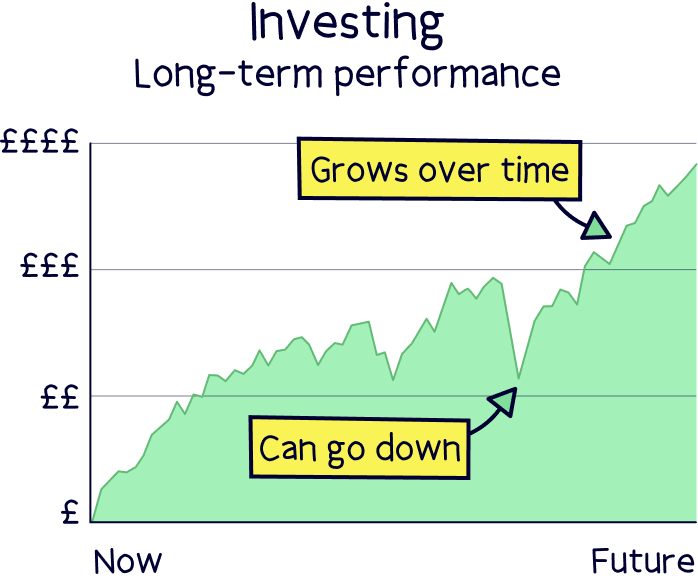

Now when we’re comparing an ISA vs pension, we’re talking about a Stocks & Shares ISA. This is where you can invest your money to grow it further over time, just as you would with a pension.

In fact, you can have exactly the same investments within an ISA as you can with a pension, the only difference is the account type (pension or ISA) which is often called the ‘tax wrapper’.

ISAs are a bit simpler than pensions – the main benefit of an ISA is that everything is completely tax-free. There’s no additional tax benefits such as a bonus from the government (unless you’re using a Lifetime ISA).

But, unlike a pension, you can withdraw your cash whenever you like (with a pension it’s locked away until you’re 55).

Here’s a quick recap of the pros and cons of ISAs:

If you’re keen to get an ISA and not sure where to get started, we’ve reviewed the best investment platforms to help you find the best one for you.

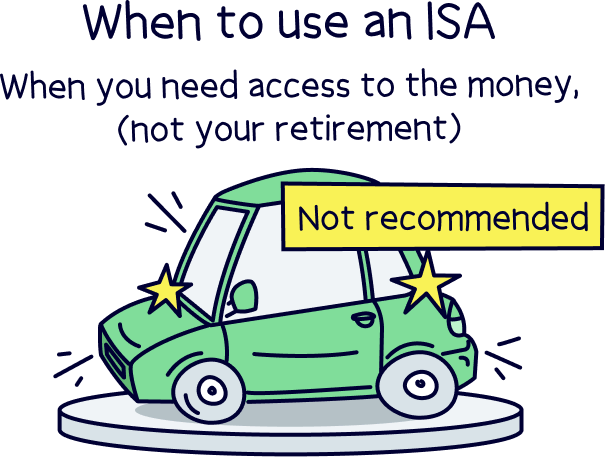

An ISA is a great account to use when saving money for the short-to-medium term.

As everything you make is tax-free, it means your money will grow faster over time thanks to compound interest. That’s when the money you make, such as your investments growing in value over time, or earning interest, makes you more money in the future. If you had to pay tax every year, your money would grow a lot slower!

And with an ISA, you can withdraw the cash whenever you want to. So, they’re a great tool for saving money in general with a view to spending it at some point in the future, perhaps you’re saving for a new car, or a deposit on a home. But of course, we recommended you keep it invested if you can, it can grow to a very large amount over time!

By the way, you can also invest money without an ISA (or into a pension pot), and this is an account called a General Investment Account (GIA) – and you will pay tax on your profits if they exceed £3,000 when you sell your investments (that’s your yearly Capital Gains Tax allowance).

Is there a best account? Well, yes and no!

An ISA and a pension are both great accounts for saving money for the long-term, and growing it by quite a bit too (by investing sensibly).

If you want to solely save for the future and retirement, with no plans to spend your cash any time soon, then a pension is your best option. You’ll get a massive 25% bonus on everything you pay in, and even 40% back if you’re a higher rate taxpayer (45% for additional rate taxpayers).

The downside is that your money is locked away until you’re 55 (57 from 2028). And you might pay tax when you start to withdraw it in the future – it all depends on how much you earn at the time. Although being locked away can actually be beneficial, as you’re not tempted to spend it!

If you think you might need your cash any time soon, or before you’re 55, then an ISA is the better option. Everything is tax-free, and you can withdraw it whenever you like – although when investing, you should try and invest for the medium-to-long-term.

There’s even more good news though, you can have both! You could split your savings between the 2 accounts so you have some cash when you need it (in an ISA), but also make use of all the awesome tax benefits with a pension too.

Note: if you’re lucky enough to have lots of cash to save every year, bear in mind the limit of how much you can pay into a pension (up to your whole salary or £60,000, whichever is lower).

So, an additional ISA is a good idea if you do reach this limit (you can invest a further £20,000 tax-free in an ISA). After that, open a General Investment Account, where you can invest as much as you like, but profit could be taxed.

All make sense? Use a pension for long-term saving, and an ISA for more short-to-medium term saving where you’ll use the cash at some point before you retire.

Decided which account is for you? Or decided on both?

Here’s where to find the best personal pensions, and check our favourites PensionBee¹ and Beach¹ (here’s our PensionBee review and our Beach review).

And for ISAs, here’s the best Stocks and Shares ISAs – our favourites are Beach¹ and Moneyfarm¹ (here’s our Moneyfarm review).

Happy saving!

Beach is an easy to use app allowing you to invest sensibly within a tax-free ISA and a pension pot.

Beach is an easy to use app allowing you to invest sensibly within a tax-free ISA and a pension pot.

Beach is an easy to use app allowing you to invest sensibly within a tax-free ISA and a pension pot.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Beach is an easy to use app allowing you to invest sensibly within a tax-free ISA and a pension pot.