Article contents

A mortgage is a type of loan that helps you buy a property. You pay a deposit and borrow the rest of your property’s value from a mortgage lender. This has to be paid back over a set number of years, along with a yearly percentage fee called interest.

The chances are you’ve heard the word ‘mortgage’ crop up again and again. Something to do with buying a home, right?? Right!

Here, we’ll tell you exactly how mortgages work – from what they are, to the different types available and how to get one.

A mortgage is a loan that’s specially designed for helping you to buy a property.

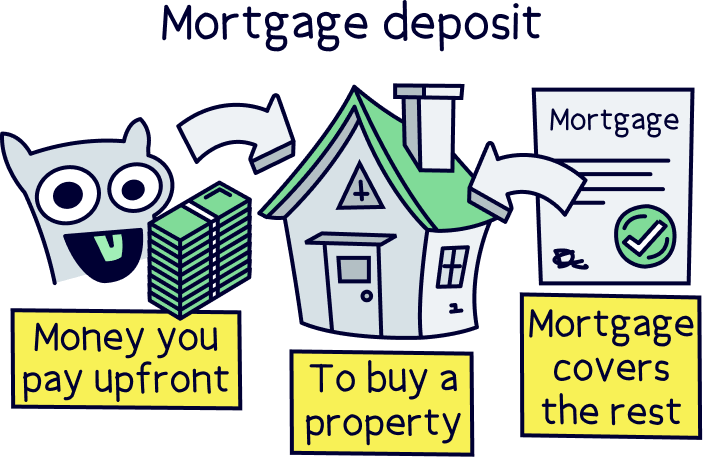

When you’re buying a home, you have to pay a chunk of money upfront, called a mortgage deposit. But you can borrow the rest of your property’s value from a mortgage lender. A mortgage lender is someone who gives out mortgages, and they’re mostly banks or building societies. Think HSBC, Natwest, Leeds Building Society… you get the idea!

Normally, you’ll have to pay back the money you borrow in monthly instalments over the duration of your mortgage, known as your mortgage term (this doesn’t apply to a type of mortgage called an interest-only mortgage, but we’ll tell you about that a bit later). This is normally over many years, most often 25, 30 or 35.

However, as well as paying back the money you’ve borrowed, you’ll also have to pay something called interest. This is a payment that lenders charge you for the pleasure of borrowing their money, and is normally a percentage of what you owe them each year. For example, if your interest rate is 2% and you owe your mortgage lender £200,000, you’ll need to pay £4,000 that year in interest (2% of 200,000 is 4,000).

When you get a mortgage, your property is used as security. That means, if you stop paying your monthly mortgage payments, your lender could be allowed to take ownership of your property and sell it. But don’t panic! It’s an absolute last resort and normally, your lender will try to help out if you can’t afford your repayments first.

Tembo will find your best deal, fast, all with award-winning service.

There are lots of different types of mortgages. And which one you get will affect exactly how your mortgage works. Don’t worry, they’re a lot easier to get your head around than you might think! Here are the main differences.

A repayment mortgage is a mortgage where your monthly repayments are designed to pay off your loan completely. In other words, with a repayment mortgage, by the time you get to the end of your mortgage term, you shouldn’t owe your lender a penny. Most people who buy a home get repayment mortgages.

On the other hand, an interest-only mortgage is a mortgage where your monthly repayments only cover the interest that’s charged on your loan (that percentage payment we told you about that lenders charge you for the pleasure of borrowing their money).

This means that by the end of your mortgage term, you’ll still owe your lender the full amount of money that you’ve borrowed and will have to pay the mortgage off in a lump sum. To get one of these mortgages, you’ll need to prove you’re going to be able to pay off the mortgage when the time comes, perhaps with savings or investments set aside.

Interest-only mortgages are normally more for people who’ve had a few mortgages before and know what they’re doing. They’re also common for landlords who have a special type of mortgage designed to help them rent out their properties, known as a buy-to-let mortgage.

That said, you don’t necessarily have to choose between the two. There’s also something called a part-and-part mortgage, which is a mix of a repayment and interest-only mortgage.

With a part-and-part mortgage, you pay back part of your loan in your monthly repayments, but not enough to have the entire loan amount repaid by the end of your mortgage term. That means you’ll still have a lump sum to pay your lender at the end of your mortgage term, but a smaller one than you would if your mortgage was interest-only.

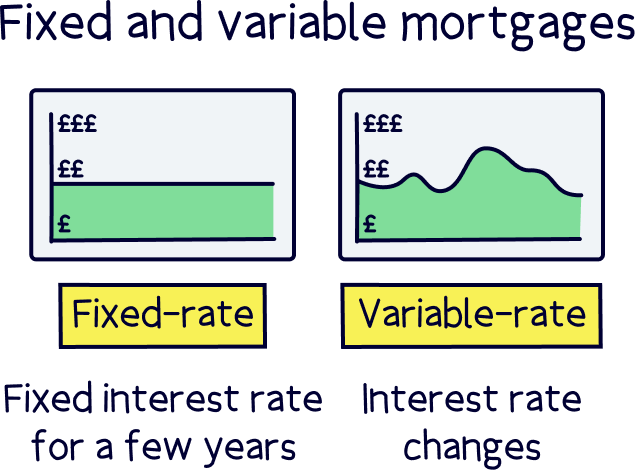

A fixed-rate mortgage is when the interest you’re charged on your loan is fixed at a set amount for a set period of time (known as your fixed-rate period or introductory period). Normally, this will be for 2, 3 or 5 years, but it can also be a lot longer.

The good side? Well, you’ll know exactly how much you’re going to have to pay each month. This makes it easier to budget and it means you’re safe in the knowledge that you’re going to be able to afford your repayments. Most people get a fixed-rate mortgage for exactly this reason!

Most importantly, a fixed-rate mortgage will protect you if interest rates rise. Interest rates are so low now that people are worried that they’ll soon go up. Fixing your mortgage could let you benefit from the current low interest rates for the duration of your fixed period, even if they go up.

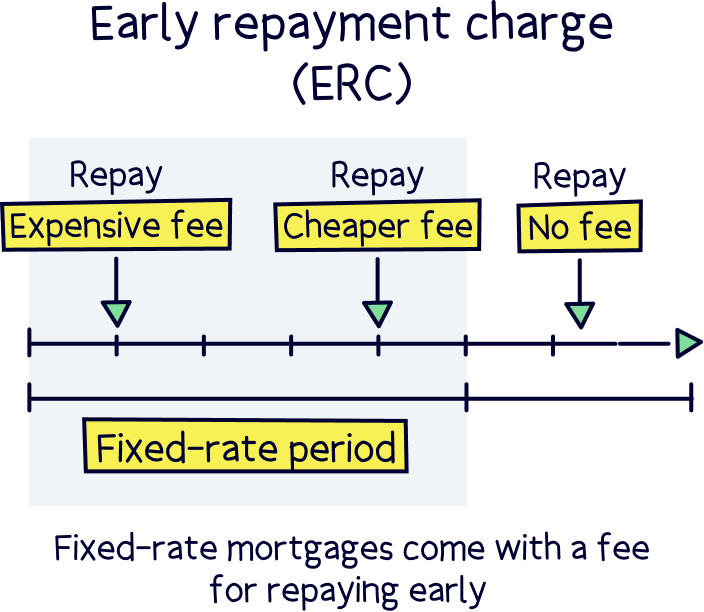

The bad side? Well, if you want to leave your mortgage before your fixed-rate period comes to an end, you’ll normally have to pay a hefty fee called an early repayment charge. Plus, there’s always the chance that interest rates might fall. If this happens, you won’t benefit from the price cut.

On the other hand, a variable-rate mortgage is a mortgage where your interest rates can move up or down. There are lots of different types of variable-rate mortgages though, and some are better than others.

The amount you have to pay in your monthly mortgage repayments will depend on lots of different things. Your mortgage type is just one! Here are some other factors that will play a part.

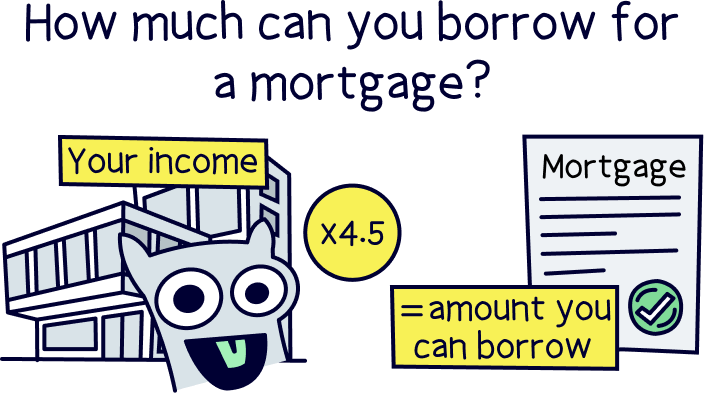

Obviously, the more you borrow from your mortgage lender, the more you have to pay back. So, bigger mortgages will come with bigger monthly repayments, while smaller mortgages will mean a lower amount is spread out over your mortgage term.

Normally, you can borrow around 4.5 x your yearly income. That means if you’re earning £24,000 per year, you’ll probably be able to get a mortgage for around £108,000 (24,000 x 4.5 = 108,000).

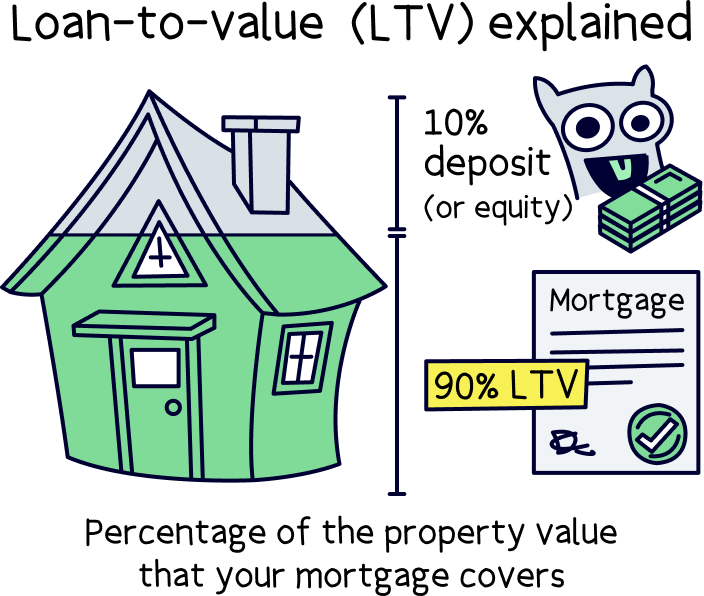

That said, there is something that might be a bit less obvious. It’s called your loan-to-value ratio (LTV). Your LTV refers to how much of your property’s value you cover with a mortgage, versus how much you pay in a deposit. Let’s look at an example.

Say you’re buying a £200,000 property and you have a £20,000 deposit. In this case, you’d need to get a mortgage for the remaining £180,000, which would give you an LTV of 90% (180,000 is 90% of 200,000). Alternatively, if you had a £50,000 deposit, you’d only need to borrow £150,000, which would give you an LTV of 75% (150,000 is 75% of 200,000).

The lower your LTV (and so the less of your property’s value you’re borrowing), the better the deal you’re likely to get. This is because most mortgage lenders prefer borrowers who cover more of their property’s value themselves, through a deposit (it’s a long story, but borrowers who pay more themselves are basically less risky).

Ultimately, that means that if you borrow less of your property’s value, your monthly repayments will tend to be lower, as you’ll generally benefit from lower interest rates.

The longer your mortgage lasts (known as your mortgage term), the smaller your monthly repayments will normally be. That’s because you’ll be able to spread out what you owe over a longer period of time. Makes sense, right?

However, bear in mind that this doesn’t mean you’ll pay less overall. Instead, a longer mortgage term will actually mean you pay more over the whole duration of your mortgage.

Why? Well, it’ll mean you pay interest for longer. Remember that interest is normally charged as a percentage of the amount that you owe your lender each year. So, the more years your mortgage lasts, the more interest you’ll have to pay.

Every lender is different and they’ll each have different deals available for borrowers, with different criteria about who can access them.

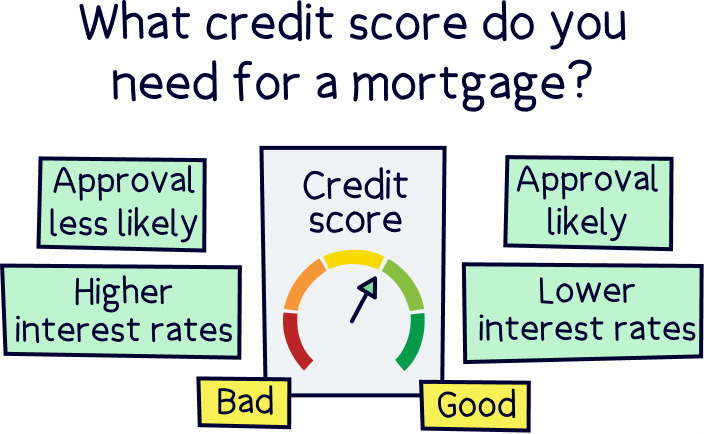

Normally, lenders will give the best deals to people who they see as a really safe bet. In other words, if they think, based on their checks, that you’re very likely to keep up with your mortgage repayments, you’ll get a better deal than someone who they think is a bit riskier.

There are lots of different factors that will contribute to how much of a risk you are to lenders and therefore what deals they’ll be willing to offer you. These include how much you earn, how much you spend, how old you are, your LTV and your credit score (your credit score is a number that shows mortgage lenders how good you’ve been with money in the past).

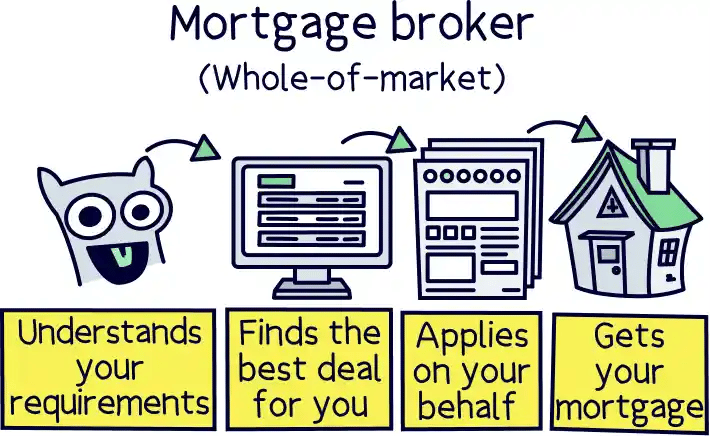

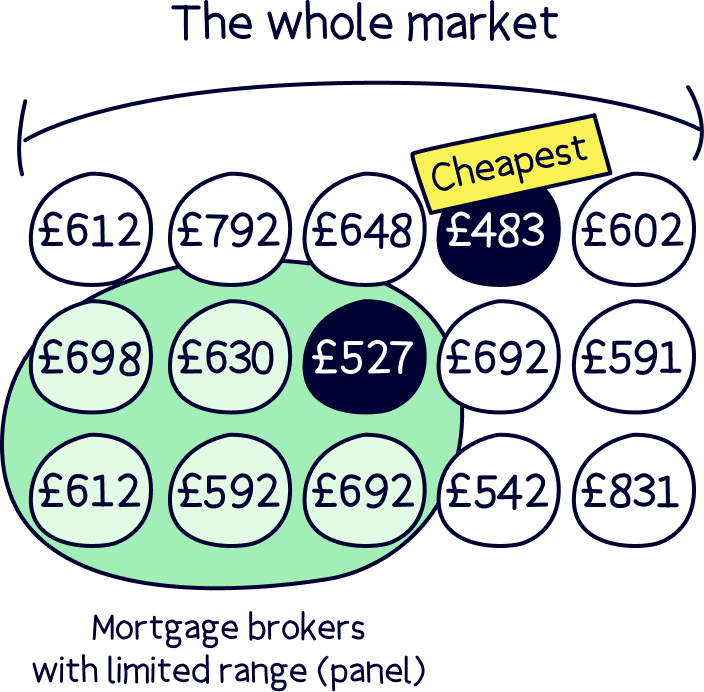

Because every lender’s criteria is different, it’s important to compare lenders to find out who can offer you the best deal, given your circumstances. A whole-of-market mortgage broker (also known as a mortgage advisor) is a professional who can help you find the best mortgage deal for you.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll get 50% off their fee with Nuts About Money too.

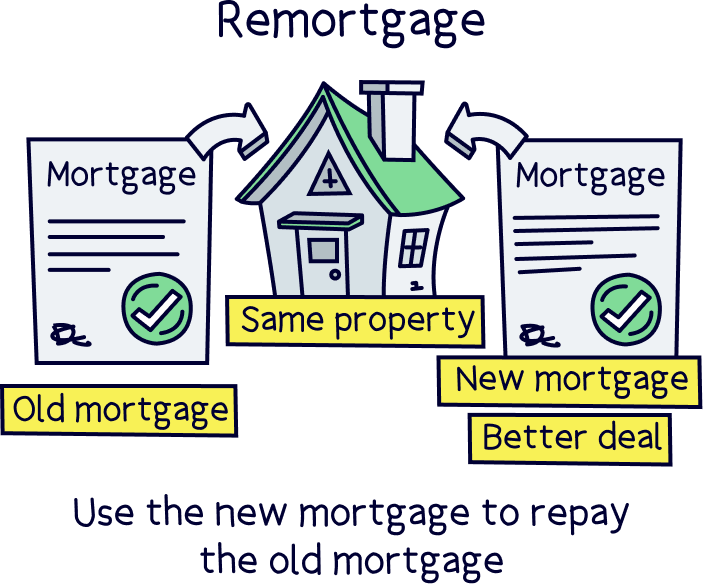

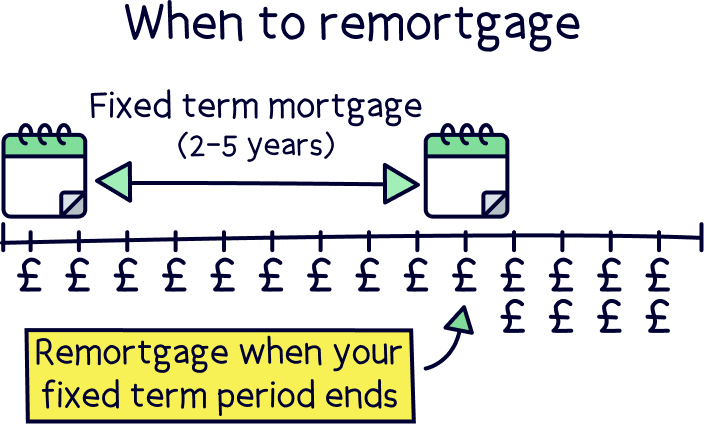

Remortgaging is when you swap your current mortgage deal for a new one, either with your existing lender or with a new one altogether. By switching to a new cheaper deal when your current deal runs out, you’ll be able to save money and therefore lower your monthly repayments.

Let us explain.

Whatever mortgage deal you get, it will normally only last for a set period of time. Remember how we said that fixed-rate mortgages mostly tend to last for 2, 3 or 5 years? Well, the same goes for most variable-rate deals, like the tracker-rate, discount variable-rate or capped-rate mortgages we told you about earlier.

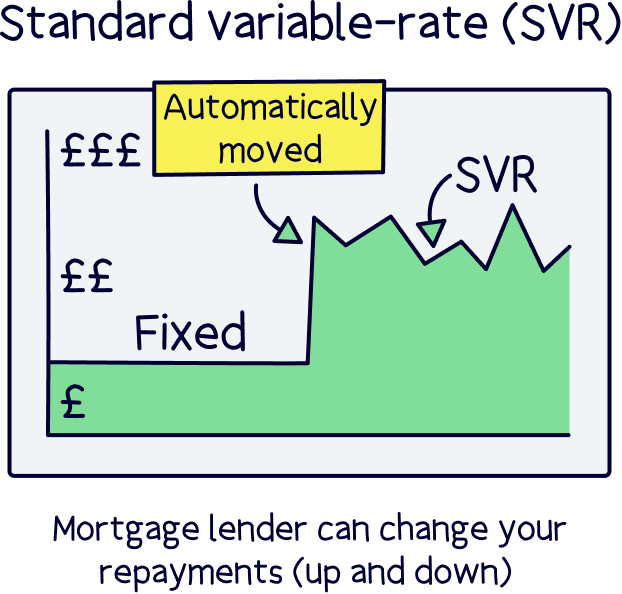

After this period of time, your mortgage lender will automatically move you onto your lender’s SVR – that expensive mortgage type that you don’t want to end up on if you can help it!

Basically, your lender will lure you in with a lovely deal to encourage you to choose them. Then, once it’s over, they’ll hike your prices up, hoping that you either can’t be bothered to change to a better deal or that you don’t know how. In fact, as of September 2020, 46% of mortgage holders fell into the trap and were paying more than they needed to on their lender’s SVR (according to Experian).

However, by remortgaging whenever your initial mortgage deal comes to an end, you can avoid those price hikes and benefit from a lovely new deal all over again. This could save you thousands of pounds each year in repayments!

Nuts About Money tip: Make sure that you wait until your deal is ending before remortgaging. If you leave your current deal in the middle, you’ll normally have to pay a pesky fee (called the early repayment charge), which could be hundreds or even thousands of pounds.

While we’re on the subject of the early repayment charge, did you know that you don’t just have to pay it if you remortgage early? You also have to pay it if you pay your lender back early for any other reason – hence the name ‘early repayment!’

That said, there is one exception. Most lenders will allow you to pay back a certain percentage of your mortgage early each year, known as overpaying, without having to pay this fee.

We know what you’re thinking: why would I want to overpay for anything?!

Well, by overpaying on your mortgage, you’ll be reducing the amount you owe your lender, which means you’ll have less interest to pay. Normally, you’ll have the option to reduce your monthly repayments or reduce your mortgage term. Want our tip? If you choose to reduce your mortgage term, you’ll usually save a lot more interest!

Most mortgage deals allow you to overpay by 10% of your total mortgage each year before the early repayment charge kicks in. However, some will let you overpay by more than that. Just be aware that those mortgages that let you overpay by more will usually have higher rates to make up for it. So, it’s only worth opting for them if you think there’s a good chance you’ll be able to overpay regularly.

Now you know how mortgages work, you’ll probably want to know what you have to do to get one. And guess what? It’s a lot easier than what you’re probably imagining. Here are the steps you’ll need to take.

This is probably the hardest part of getting a mortgage. After all, we all know how hard saving can be!

To get a mortgage, you’ll need to save up enough money to cover at least 5% of the property you want to buy. This is because the maximum a mortgage lender will normally let you borrow is 95% of your property’s value (known as a 95% LTV).

So, if you want to buy a property that’s worth £200,000, you’ll need to save up at least £10,000 (5% of 200,000). However, the more you can save, the better, as a bigger deposit will normally give you access to better deals.

Once you’ve saved up enough money for a deposit, it’s time to find a mortgage broker. They’ll be able to help you find the best mortgage deal and will sort out your whole application for you.

Don’t get us wrong, you don’t have to use a mortgage broker – you can go straight to individual mortgage lenders. However, there are over 100 mortgage lenders in the UK, each with their own mortgage deals and criteria, so it can be hard to know who to approach. Comparison sites can help, but they won’t take into account all your personal circumstances, which could affect which lender is best for you.

Mortgage brokers are experts in mortgages who’ll take the time to learn all about your individual situation before helping you find the best lender for your needs. In this way, they’ll be able to save you a ton of time, money and stress! Just make sure that you use a whole-of-market mortgage broker as they’ll be able to compare all the different mortgage lenders for you, rather than just a few.

If you’re already house hunting, your estate agent might demand that you use their own mortgage broker who's ‘on your side.’ Sometimes, they’ll even refuse to put your offer forward if you don’t! But don’t fall into this trap.

You don’t have to use any specific mortgage broker. Any estate agents who say otherwise are just telling you porkie pies to try and make extra money off you (they’ll have a deal with a mortgage broker where they get paid a fee for referring you). Yeah, some estate agents really suck!

We recommend you check out Tembo¹, they've got award-winning service and you can get 50% off with Nuts About Money.

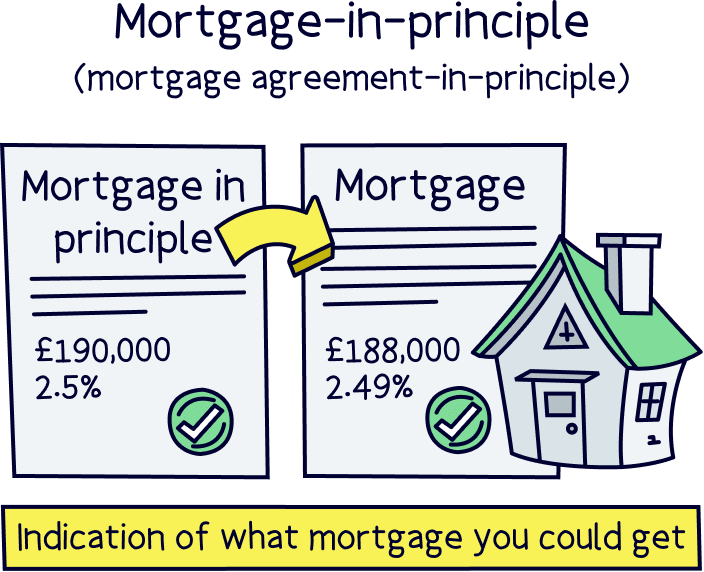

If you use a mortgage broker, they’ll sort this step out for you. A mortgage in principle is an official document from a mortgage lender that says how much they’re willing to lend you, based on what they know about you so far. It’s not a guarantee that you’ll be able to get a mortgage, as they won’t carry out every check on you at this stage. But it is a good sign!

So, why do you need a mortgage in principle? Well, you don’t technically need one. But they are super useful. They give you a good idea about what size mortgage you’ll be able to get, which means you can go and view houses or flats that you actually have a chance of being able to afford!

Plus, it will make you look like a serious buyer. A lot of estate agents and sellers will want to see a mortgage in principle before they accept an offer from you on a property, and some won’t even let you view properties without one!

Now’s the fun part – it’s time to go house hunting! Yep, that’s right, you get to snoop around other people’s homes and picture yourself living there. Once you find the ideal home in your budget, you can put in an offer and, hopefully, it’ll get accepted!

Most mortgages in principle last for around 60 to 90 days. So, in an ideal world, you’ll want to find your dream property and get an offer accepted within this time.

However, don’t panic if that doesn’t happen. You can just apply for a new mortgage in principle or even continue the process without one. It’s certainly not the end of the world!

Now that you’ve found a property to buy, you can actually go ahead and apply for a mortgage.

If you used a mortgage broker for the previous steps, this is super easy. All you have to do is contact them and give them a few details about the property you want to buy. They’ll then go ahead and apply for the mortgage for you. That’s right, they’ll already have all your details on file, so you don’t need to do anything more!

We mean, you will still have some other house buying stuff to sort out, like getting hold of a conveyancer (someone to help with the legal part of buying your property). Your broker should be on friendly terms with a conveyancer you can use if you’re looking. But when it comes to your mortgage, you can just sit back, relax and let your broker do their thing.

Once they receive your application, your mortgage lender will do a few more checks, including a credit check (where they check your credit score) and a valuation survey (where they check that they agree the property is worth what you’re paying for it). Then, assuming everything is okay, you’ll get a mortgage offer between 2 and 20 days later.

At this point, your mortgage is all in place and ready to go. You’ll just need to wait for your conveyancer to finish sorting out the legal side of buying your property (known as conveyancing) and soon enough, you’ll be jangling the keys to your very own home. Congrats!

Been saving up for your deposit? Want to go ahead and find your dream property (or got your eye on a property already)? Then now’s the time to find a mortgage advisor.

They’ll compare all the mortgages and lenders out there to find the best deal for you, and they’ll even sort out the whole mortgage application process for you when the time comes. You just go and pick a home to buy and let them handle the rest!

As a reminder, if you need to find a decent mortgage broker, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best deal. You'll get 50% off their fee with Nuts About Money too.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.